Global Liquid Waste Management Market Size, Share, And Enhanced Productivity By Waste Type (Hazardous Liquid Waste, Non-Hazardous Liquid Waste), By Source (Residential, Commercial, Industrial), By Service (Collection, Transportation/Hauling, Disposal/Recyling), By Treatment Method (Physical, Chemical, Biological, Others), By End-User (Food and Beverage, Leather, Textile, Paper and Pulp, Power Generation, Chemical Industry, Sugar Industry, Petrochemical and Refinery, Metal Refining including Iron and Steel, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: January 2026

- Report ID: 174969

- Number of Pages: 321

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

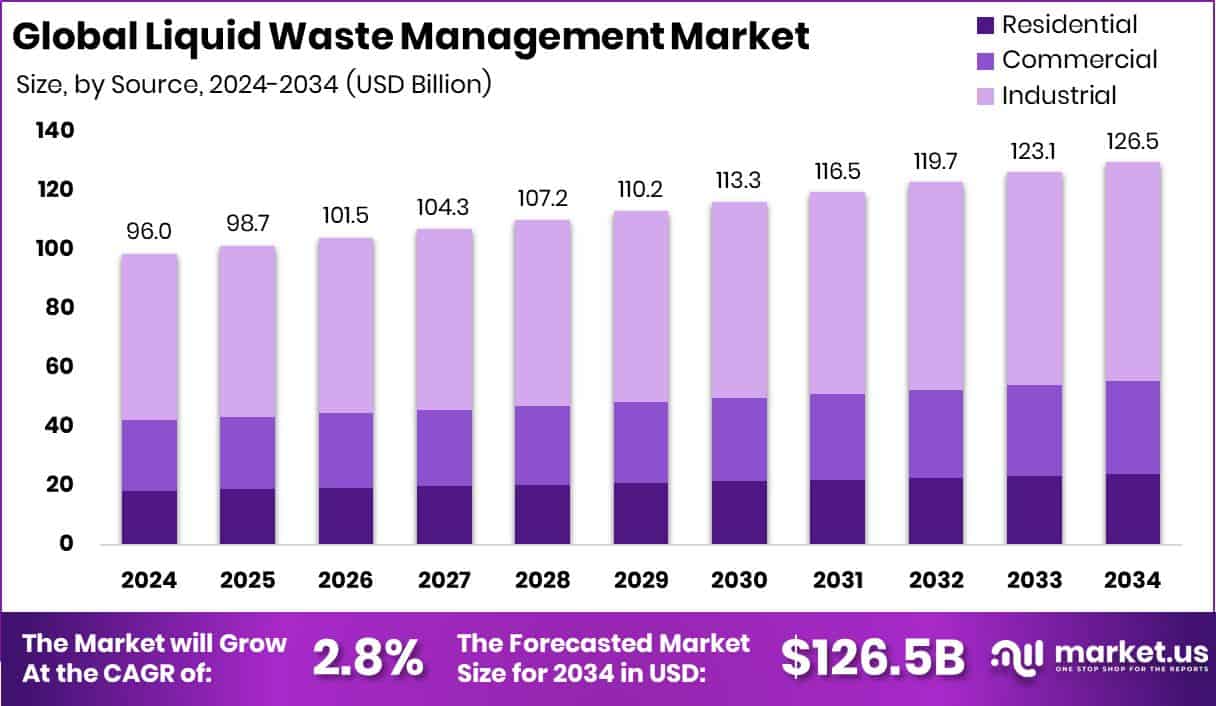

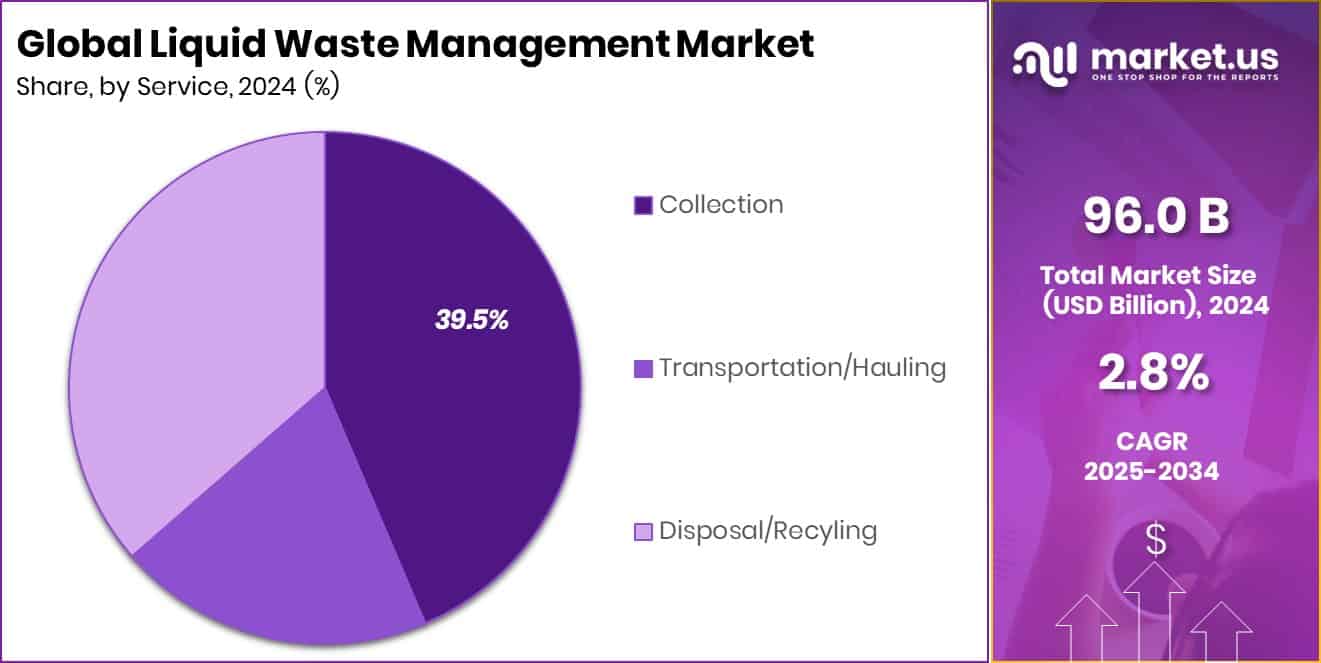

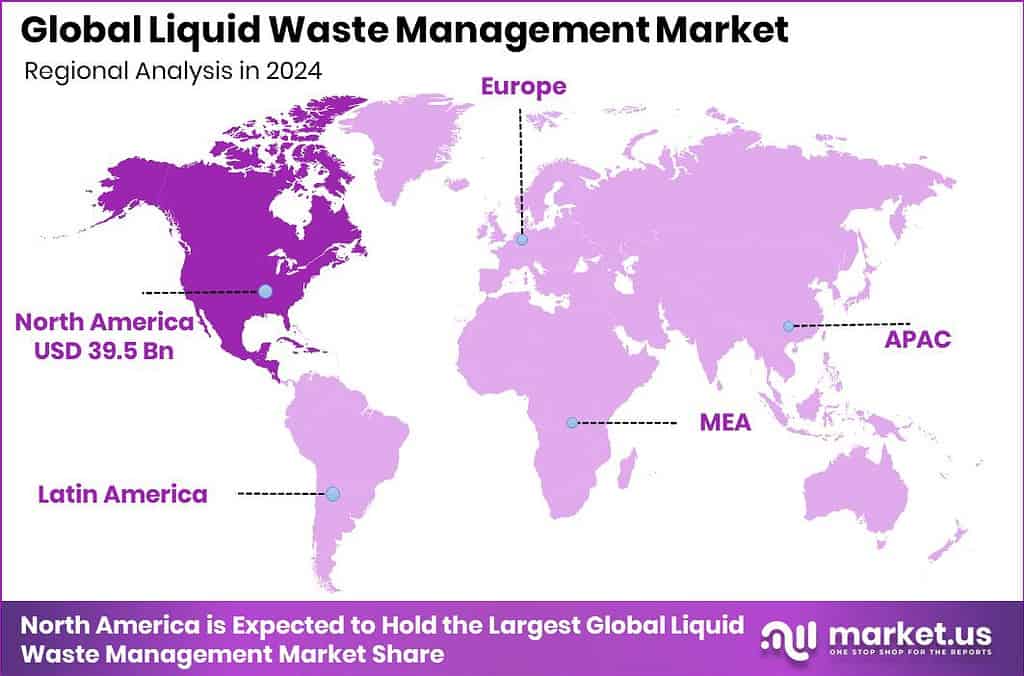

The Global Liquid Waste Management Market is expected to be worth around USD 126.5 billion by 2034, up from USD 96.0 billion in 2024, and is projected to grow at a CAGR of 2.8% from 2025 to 2034. Liquid Waste Management in North America held 41.20%, valued at USD 39.5 Bn in 2024.

Liquid waste management refers to the safe collection, transport, treatment, recycling, and disposal of liquid-based wastes generated from households, industries, agriculture, and commercial activities. These wastes include wastewater, effluents, oils, sludge, and contaminated liquids that can harm soil and water if unmanaged. Proper systems help protect public health, prevent pollution, and ensure regulatory compliance, while supporting water reuse and environmental restoration.

The Liquid Waste Management Market covers services and technologies used to handle these waste streams at scale. It includes physical, chemical, and biological treatment processes, along with infrastructure for collection and recovery. Governments and local authorities play a central role, supported by targeted funding programs and site rehabilitation projects aimed at reducing long-term environmental damage and restoring affected ecosystems.

Market growth factors are strongly linked to cleanup and remediation initiatives. The rehabilitation of Sovjak, where 40,000 tons of liquid waste and soft tar will be removed, reflects rising investment in legacy pollution removal. Similarly, $40 million recovered for restoration in three states and a $4 million release to clean up abandoned industrial sites in Northeast Ohio highlight sustained public-sector commitment to environmental recovery.

Rising demand is driven by infrastructure upgrades and recycling expansion. North Carolina’s $25 million in grant funding strengthens recycling and waste management systems, while a new recycling plant receiving a $1.34 million grant ahead of its 2024 opening supports localised liquid waste processing capacity.

Key opportunities are emerging through asset restructuring and reinvestment. The sale of an environmental services business in a $5.6 billion deal to reduce debt signals capital realignment, enabling future investments in efficient, compliant liquid waste solutions.

Key Takeaways

- The Global Liquid Waste Management Market is expected to be worth around USD 126.5 billion by 2034, up from USD 96.0 billion in 2024, and is projected to grow at a CAGR of 2.8% from 2025 to 2034.

- The liquid waste management market grows rapidly as non-hazardous liquid waste reaches a 65.2% share.

- Industrial activities dominate the liquid waste management market, contributing a strong 58.8% to global demand.

- Collection services lead the Liquid Waste Management Market, holding a considerable 39.5% market share worldwide.

- Physical treatment methods remain essential in the liquid waste management market, accounting for 38.1% overall usage.

- The chemical industry drives expansion of the liquid waste management market, representing 19.4% of the end-user share.

- North America dominated liquid waste management at 41.20%, reaching USD 39.5 Bn in 2024.

By Waste Type Analysis

Liquid Waste Management Market sees non-hazardous waste dominating with 65.2% share.

In 2024, the Liquid Waste Management Market was largely shaped by the strong dominance of non-hazardous liquid waste, which accounted for 65.2% of total waste processed. This category includes domestic wastewater, industrial effluents with low toxicity, and municipal liquid waste streams that are easier and safer to treat compared to hazardous materials.

Growing urbanisation and rapid expansion of residential townships increased municipal wastewater volumes, pushing utilities to enhance their collection and treatment systems. Industries also focused on compliant disposal practices to meet environmental norms, further increasing the flow of non-hazardous waste into formal management channels. As regulatory bodies tightened discharge limits, demand for efficient treatment technologies rose, reinforcing this segment’s leading position within the market.

By Source Analysis

Liquid Waste Management Market shows industrial sources leading generation at 58.8%.

In 2024, industrial activities accounted for a significant share of the Liquid Waste Management Market, contributing 58.8% of total liquid waste generated. Sectors such as chemicals, food processing, pharmaceuticals, textiles, and oil & gas discharged large volumes of wastewater requiring specialised treatment. Stricter compliance requirements, including zero-liquid-discharge (ZLD) mandates in key manufacturing hubs, pushed industries to invest in robust wastewater processing systems.

Increasing production output and facility expansions across emerging economies also amplified wastewater generation. Companies increasingly partner with professional waste management service providers to meet environmental standards and avoid penalties. This resulted in a strong pipeline of industrial liquid waste entering collection, recycling, and reuse processes, supporting the segment’s market leadership throughout the year.

By Service Analysis

Liquid Waste Management Market highlights collection services holding demand at 39.5%.

In 2024, the collection segment held a dominant position in the Liquid Waste Management Market with 39.5% share, reflecting the essential role of structured waste handling before treatment or disposal. Efficient collection services ensured safe transport of both domestic and industrial wastewater, preventing contamination of soil and water bodies. Growing dependence on outsourced waste management operators improved process reliability and compliance.

Municipal bodies and private firms expanded their tanker fleets and pipeline networks to manage rising liquid waste volumes, especially in industrial clusters and densely populated cities. With increasing awareness of environmental obligations, households, commercial units, and industries opted for regular scheduled pickups, strengthening the overall effectiveness of the waste management chain and supporting this segment’s strong growth.

By Treatment Method Analysis

The Liquid Waste Management Market indicates that physical treatment methods are used at 38.1%.

In 2024, physical treatment methods led the Liquid Waste Management Market with 38.1% share, supported by their cost-effectiveness and ability to handle diverse wastewater streams. Processes such as sedimentation, filtration, flotation, and screening remained widely used as preliminary and primary treatment steps across municipal and industrial facilities. Physical methods also enabled the removal of suspended solids, oils, and debris, improving efficiency for downstream biological or chemical processes.

Industries with high wastewater discharge favoured these systems for their low maintenance and scalability. The rise of membrane-based filtration further strengthened this segment’s relevance, especially in large urban wastewater treatment plants. As both public and private players upgraded infrastructure, physical treatment maintained its role as a critical first-stage solution.

By End-User Analysis

Liquid Waste Management Market notes the chemical industry as an end-user at 19.4%.

In 2024, the chemical industry emerged as the leading end-user in the Liquid Waste Management Market, accounting for 19.4% of demand. This sector produces complex effluents containing solvents, acids, alkalis, and organic residues that require specialised handling and treatment. Increasing chemical production capacity in Asia, Europe, and North America drove higher wastewater volumes, compelling companies to adopt advanced purification and recycling technologies.

Environmental authorities strengthened monitoring of effluent discharge, pushing chemical manufacturers to improve compliance through partnerships with certified waste management service providers. The shift toward sustainable manufacturing, including water-reuse practices, further increased demand for professional wastewater treatment solutions, solidifying the chemical industry’s position as the largest contributor within the end-user landscape.

Key Market Segments

By Waste Type

- Hazardous Liquid Waste

- Non-Hazardous Liquid Waste

By Source

- Residential

- Commercial

- Industrial

By Service

- Collection

- Transportation/Hauling

- Disposal/Recycling

By Treatment Method

- Physical

- Chemical

- Biological

- Others

By End-User

- Food and Beverage

- Leather

- Textile

- Paper and Pulp

- Power Generation

- Chemical Industry

- Sugar Industry

- Petrochemical and Refinery

- Metal Refining, including Iron and Steel

- Others

Driving Factors

Rising Industrial Expansion Boosts Waste Treatment Demand

Northern Pulp’s request for $2.5 billion in funding to build a new pulp mill reflects how industrial expansion increases the need for strong liquid waste treatment systems. Large mills and manufacturing units generate high volumes of wastewater that must be collected and treated safely.

When companies plan major new facilities, governments and regulators expect them to invest in updated waste handling technologies. This push encourages industries to adopt cleaner and more efficient treatment solutions.

As more industrial projects seek funding and move toward construction, the demand for professional liquid waste management grows naturally. This trend strengthens the overall market, as every new plant requires reliable wastewater systems to operate responsibly.

Restraining Factors

High Modernisation Costs Limit Treatment Capacity

The industry faces challenges when treatment facilities struggle with high modernisation and upgrade costs. For example, AlterEco Pulp raising €3.5 million for eco-sustainable packaging and the $5 million support to modernise Thunder Bay mill electrical systems show how costly improvements can become. Many liquid waste handling plants require similar upgrades—such as new filtration equipment, safer pipelines, and energy-efficient processing units.

Smaller operators often delay these improvements because they cannot match these funding levels. When plants operate with outdated systems, the risk of inefficiency and slower processing increases. These financial pressures act as a restraint, as not all regions or facilities can secure the large investments needed to maintain advanced treatment operations.

Growth Opportunity

Government Support Creates Expansion Potential

Strong market opportunities arise when governments and industries invest directly in cleaner systems. The €3.5 million funding raised by AlterEco Pulp for eco-friendly packaging highlights the growing demand for sustainable waste solutions.

Meanwhile, the $29-million aid provided to reopen an Ontario paper mill shows that governments are willing to support industrial recovery tied to improved waste handling standards. These actions encourage companies to upgrade wastewater systems, integrate recycling loops, and adopt safer disposal steps.

As more industries reopen or expand with government backing, the need for advanced liquid waste management grows. This environment creates wide opportunities for service providers offering efficient, compliant, and scalable treatment solutions.

Latest Trends

Large-Scale Mill Modernisation Drives New Practices

Modernisation of mills and industrial facilities is shaping new trends in liquid waste management. The Canada Infrastructure Bank’s $660 million loan for Irving Pulp & Paper and the company’s separate $1.1 billion upgrade for its Saint John mill show how major investments are shifting operations toward cleaner and more efficient systems. These large projects usually integrate advanced wastewater treatment, closed-loop recycling, and reduced-effluent technologies.

As companies modernise, they adopt digital monitoring, improved filtration, and energy-efficient equipment. This trend is becoming more common as industries try to meet stricter environmental expectations. These major upgrades signal a shift toward long-term sustainable practices across liquid waste operations.

Regional Analysis

In 2024, North America led liquid waste management with 41.20%, USD 39.5 Bn.

In 2024, North America dominated the Liquid Waste Management Market, securing a 41.20% share valued at USD 39.5 billion. The region’s lead was supported by strong industrial wastewater generation and mature municipal treatment infrastructure. Europe followed with steady expansion driven by strict environmental directives and a rising focus on wastewater reuse across manufacturing clusters.

In the Asia Pacific, rapid industrialisation and dense populations continued to elevate liquid waste volumes, prompting countries to strengthen formal collection and treatment systems. The Middle East & Africa region showed gradual improvement as industrial zones increased adoption of structured wastewater handling.

Latin America also progressed with growing emphasis on municipal and industrial waste management, supported by rising treatment capacity. Across all regions, higher wastewater generation from urban, commercial, and manufacturing activities shaped the market’s overall direction.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Befesa strengthened its position by focusing on liquid waste generated from industrial processes, particularly metal and steel operations. Its treatment capabilities and emphasis on environmentally responsible recovery helped the company maintain relevance as industries sought safer and compliant disposal solutions.

Bion Environmental Technologies, Inc. advanced its contribution by developing treatment approaches aimed at reducing nutrient-rich liquid waste, particularly from agricultural and livestock operations. The company’s technology-driven solutions positioned it well as demand increased for systems that support cleaner discharge and protect water bodies from contamination.

Clean Harbours, Inc. continued to lead with its extensive service network covering collection, transport, and treatment of diverse liquid waste streams. The company’s ability to manage large volumes, including complex industrial liquids, supported its strong performance in 2024. Its established infrastructure and integrated service model enabled it to meet rising requirements from manufacturing, commercial, and municipal clients. Together, these companies played a crucial role in advancing operational efficiency and compliance in liquid waste management globally.

Top Key Players in the Market

- Befesa

- Bion Environmental Technologies, Inc.

- CLEAN HARBORS, INC.

- Cleanaway

- Cleanaway Daniels

- SENVA

- EnviroServe

- FCC Recycling (UK) Limited

- GFL Environmental Inc.

- Ovivo Inc.

Recent Developments

- In June 2024, Befesa completed the acquisition of full ownership of its French joint venture, Recytech, strengthening its presence in Europe and expanding its recycling operations for steel and aluminium waste streams. This strategic move gave Befesa complete control of a key facility in the hazardous waste recycling space, improving operational flexibility and increasing capacity in the region. The acquisition reflects Befesa’s focus on growth in regulated waste management and recovery services.

- In March 2024, Clean Harbours completed its $400 million acquisition of HEPACO, an environmental field services and emergency response provider in the Eastern U.S. This expanded Clean Harbours’ ability to serve industrial and hazardous liquid waste collection, emergency response, and remediation with a larger fleet and national footprint.

- In January 2024, Bion was issued a new patent that expanded the coverage of its Ammonia Recovery System (ARS) to include industrial and municipal wastewater streams in addition to agricultural waste. This development helps the company apply its technology to a wider range of liquid waste sources and boosts its potential role in water treatment and resource recovery.

Report Scope

Report Features Description Market Value (2024) USD 96.0 Billion Forecast Revenue (2034) USD 126.5 Billion CAGR (2025-2034) 2.8% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Waste Type (Hazardous Liquid Waste, Non-Hazardous Liquid Waste), By Source (Residential, Commercial, Industrial), By Service (Collection, Transportation/Hauling, Disposal/Recyling), By Treatment Method (Physical, Chemical, Biological, Others), By End-User (Food and Beverage, Leather, Textile, Paper and Pulp, Power Generation, Chemical Industry, Sugar Industry, Petrochemical and Refinery, Metal Refining including Iron and Steel, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Befesa, Bion Environmental Technologies, Inc., CLEAN HARBORS, INC., Cleanaway, Cleanaway Daniels, SENVA, EnviroServe, FCC Recycling (UK) Limited, GFL Environmental Inc., Ovivo Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Liquid Waste Management MarketPublished date: January 2026add_shopping_cartBuy Now get_appDownload Sample

Liquid Waste Management MarketPublished date: January 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Befesa

- Bion Environmental Technologies, Inc.

- CLEAN HARBORS, INC.

- Cleanaway

- Cleanaway Daniels

- SENVA

- EnviroServe

- FCC Recycling (UK) Limited

- GFL Environmental Inc.

- Ovivo Inc.

Our Clients

- 174969

- January 2026