Quick Navigation

Report Overview

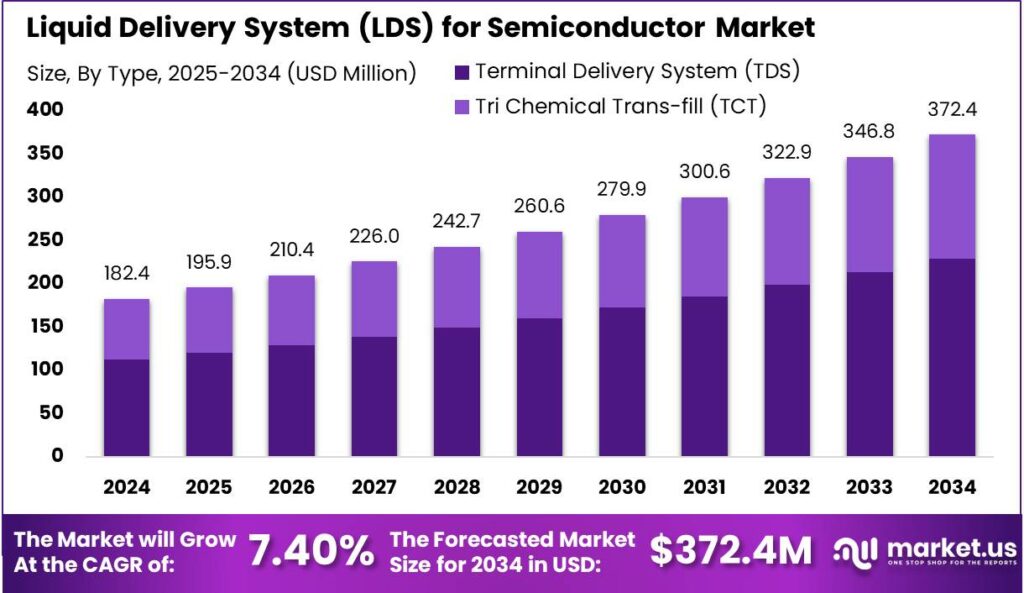

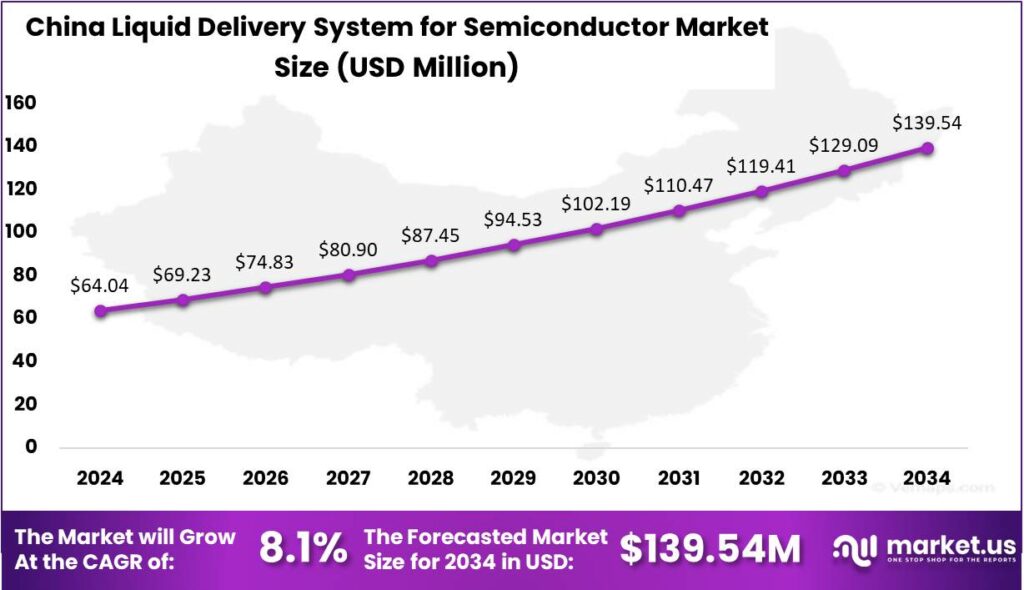

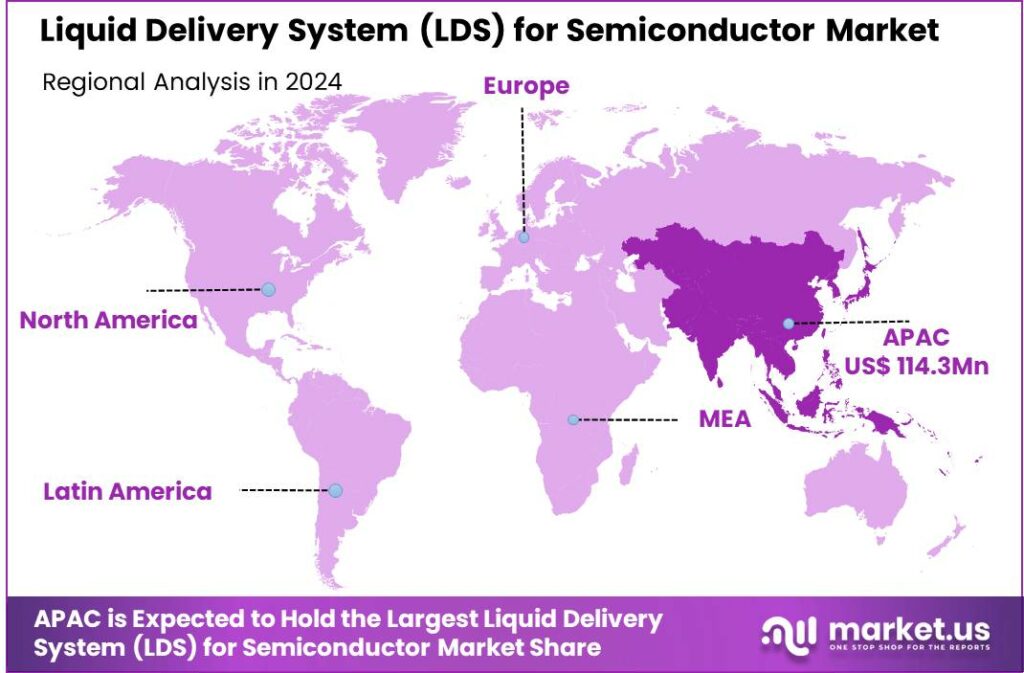

The Global Liquid Delivery System (LDS) for Semiconductor Market size is expected to be worth around USD 372.4 Million By 2034, from USD 182.4 Million in 2024, growing at a CAGR of 7.40% during the forecast period from 2025 to 2034. In 2024, the Asia-Pacific region led the LDS for semiconductors market, holding over 62.7% of the share with USD 114.3 million in revenue. The U.S. market was valued at USD 64.04 million and is expected to grow at a CAGR of 8.1%.

Liquid Delivery Systems (LDS) are critical components within the semiconductor manufacturing sector, primarily facilitating the precise and controlled delivery of liquids necessary for processes like chemical vapor deposition (CVD) and atomic layer deposition (ALD). These systems ensure high levels of accuracy and purity, essential for maintaining the integrity of the semiconductor fabrication process.

The growth of the Liquid Delivery System (LDS) market in semiconductors is driven by the rising demand for advanced, miniaturized devices in sectors like consumer electronics, automotive, and healthcare. This increased demand requires more sophisticated manufacturing equipment, including LDS, to meet the precision and efficiency needs of modern semiconductor production.

Key drivers of the LDS market include advancements in semiconductor technology, particularly the shift towards smaller process nodes below 5nm which require more stringent control over chemical delivery and contamination. Additionally, the growing demand for high-performance electronics fuels the need for more sophisticated manufacturing techniques that rely on precise LDS.

Demand for LDS is primarily driven by the semiconductor industry’s need for high precision and purity in liquid delivery, essential for manufacturing processes like etching, cleaning, and deposition. The transition to more advanced semiconductor nodes and the integration of new materials into manufacturing processes further amplify this demand.

The growing popularity of liquid delivery systems in the semiconductor market is driven by their role in improving product quality and production efficiency. As the semiconductor industry expands, fueled by sectors like automotive, healthcare, and consumer electronics, LDS technology is gaining attention, particularly with the shift to complex integrated circuits and the rise of IoT technologies.

The expansion of the LDS market is tightly connected to global semiconductor trends, such as the growing demand for consumer electronics and the automotive industry’s increasing use of electronic components. To meet these demands, manufacturers are expanding production capacity, particularly in semiconductor hubs like South Korea and Taiwan, which is expected to drive the need for advanced LDS technologies.

Key Takeaways

China Market Leadership

The U.S. Liquid Delivery System (LDS) market for semiconductors was estimated to reach a value of $64.04 million in the year 2024. It is projected to expand at a compound annual growth rate (CAGR) of 8.1%.

Liquid Delivery Systems (LDS) are crucial in semiconductor manufacturing, enabling precise and controlled delivery of chemicals and gases for wafer processing. They ensure the consistency and reproducibility needed for high-quality production standards. The growth of the LDS market is driven by the rising demand for advanced semiconductor devices in sectors such as consumer electronics, automotive, and industrial automation.

The increasing complexity of semiconductor devices and the rise of technologies like 5G, IoT, and AI are driving the demand for advanced liquid delivery solutions. As manufacturers pursue smaller chip sizes and more efficient processes, the reliance on precise LDS systems grows, supporting continued market expansion in the U.S. and fueling technological advancements.

In 2024, Asia-Pacific held a dominant market position in the Liquid Delivery System (LDS) for the Semiconductor Market, capturing more than a 62.7% share with revenue amounting to USD 114.3 million. This substantial market share can be attributed to several key factors that uniquely position Asia-Pacific as a leader in this sector.

Asia-Pacific is a key hub for semiconductor manufacturing, with countries like South Korea, Taiwan, and China hosting major production facilities. The high concentration of fabs in the region drives significant demand for liquid delivery systems (LDS), essential for precise dispensing of chemicals and materials during chip production.

Additionally, the region’s commitment to technological advancement and innovation supports the growth of the LDS market. Governments across Asia-Pacific have been instrumental in promoting semiconductor industries through favorable policies, substantial investments in research and development, and partnerships with global tech companies.

The rapid growth of consumer electronics, automotive, and telecommunications industries in Asia-Pacific boosts semiconductor demand, driving the need for efficient LDS. The rollout of 5G and the rise in IoT devices further increase this demand, requiring advanced liquid delivery systems to meet modern semiconductor process needs.

Type Analysis

In 2024, the Terminal Delivery System (TDS) segment held a dominant market position within the Liquid Delivery System (LDS) market for semiconductors, capturing more than a 61.7% share. This segment’s leadership can be attributed to its critical role in ensuring the precise and contamination-free transfer of high-purity chemicals to the point of use in semiconductor manufacturing.

The substantial share of the TDS segment is further bolstered by its integration in high-volume manufacturing environments where the consistency and quality of chemical delivery are paramount. These systems are designed to minimize chemical waste and reduce downtime by providing faster and more accurate chemical dispensing.

Another factor driving the dominance of the TDS segment is the ongoing miniaturization of semiconductor components. As device geometries shrink, the demand for precise chemical delivery systems increases. TDS systems address this need by providing advanced control features that precisely manage flow rates and chemical volumes, supporting the production of smaller, more efficient semiconductor chips.

The TDS segment benefits from substantial R&D investments by major semiconductor manufacturers to optimize the fabrication process. These investments focus on enhancing TDS technology’s efficiency and integration in increasingly automated production lines. The ongoing advancements in TDS systems are key to their market dominance and are expected to maintain their leadership in the future.

Application Analysis

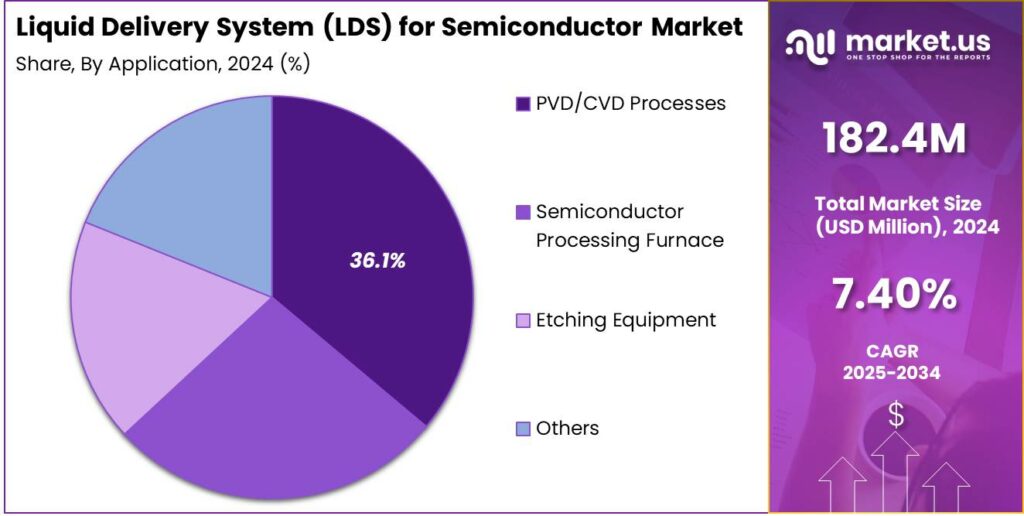

In 2024, the PVD/CVD Processes segment held a dominant market position within the Liquid Delivery System (LDS) for the semiconductor market, capturing more than a 36.1% share. This segment’s leadership is attributed to the essential role that Physical Vapor Deposition (PVD) and Chemical Vapor Deposition (CVD) processes play in semiconductor manufacturing.

The significance of PVD/CVD processes in producing advanced microelectronics is a primary factor contributing to the segment’s dominance. As semiconductors become increasingly integral to a wide array of technologies, from smartphones to sophisticated computing systems, the need for high-quality deposition techniques has surged.

Ongoing advancements in semiconductor materials and the miniaturization of components require improvements in deposition technologies. The PVD/CVD processes segment benefits from continuous innovations that enhance the efficiency and capabilities of deposition systems, helping maintain its leadership by meeting the evolving needs of the semiconductor industry.

The future of the PVD/CVD processes segment looks promising, driven by the growing demand for semiconductors in emerging technologies like AI and IoT. These technologies require more complex semiconductor structures, and the precision provided by advanced LDS in PVD/CVD processes will remain in high demand, ensuring continued growth and relevance in the semiconductor market.

Key Market Segments

By Type

- Terminal Delivery System (TDS)

- Tri Chemical Trans-fill (TCT)

By Application

- Semiconductor Processing Furnace

- PVD/CVD Processes

- Etching Equipment

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Technological Advancements in Semiconductor Manufacturing

The evolution of semiconductor manufacturing has been marked by continuous technological advancements, necessitating precise and reliable liquid delivery systems (LDS). As device architectures become more complex, the demand for accurate deposition of materials has intensified.

Modern LDS provide better control over flow rates and chemical compositions, ensuring uniformity and consistency in processes like CVD and ALD. These systems are integral in achieving the stringent tolerances required for advanced semiconductor nodes, thereby driving their adoption in cutting-edge fabrication facilities.

The integration of smart technologies, including real-time monitoring and adaptive feedback mechanisms, further enhances the efficiency and reliability of LDS, aligning with the industry’s move towards automation and smart manufacturing.

Restraint

High Initial Capital Investment

The implementation of advanced liquid delivery systems in semiconductor fabrication plants entails substantial initial capital expenditure. These sophisticated systems require precision engineering and integration with existing manufacturing processes, leading to elevated costs. These systems demand regular calibration, monitoring, and replacement of components to ensure optimal performance.

For small to medium-sized enterprises (SMEs), this financial barrier can be particularly challenging, potentially hindering their competitiveness in the market. Additionally, the complexity of these systems necessitates specialized personnel for operation and maintenance, further escalating operational costs. The high cost of LDS can be a barrier to entry for some companies, particularly smaller semiconductor manufacturers.

Opportunity

Expansion into Emerging Markets

The global expansion of the semiconductor industry into emerging markets presents significant opportunities for liquid delivery system providers. Regions such as Asia-Pacific are witnessing substantial investments in semiconductor fabrication facilities, driven by increasing demand for consumer electronics, automotive electronics, and IoT devices.

This growth trajectory offers LDS manufacturers the chance to establish a strong presence in these burgeoning markets. Collaborations with local entities and customization of solutions to meet regional manufacturing requirements can further enhance market penetration. The growing investment in semiconductor manufacturing infrastructure, particularly in regions such as Asia-Pacific, is driving the demand for semiconductor chillers.

Challenge

Material Scarcity and Environmental Concerns

The semiconductor industry’s reliance on rare earth elements and other critical materials poses a significant challenge for liquid delivery systems. Material scarcity can lead to supply chain disruptions and increased costs, impacting the overall efficiency of semiconductor manufacturing.

Additionally, environmental concerns associated with the extraction and processing of these materials necessitate the development of sustainable practices. The semiconductor manufacturing process generates a significant amount of waste and energy usage. To address these environmental challenges, investments in cleaner technologies and sustainable practices are needed to reduce the industry’s ecological footprint.

Emerging Trends

One notable trend is the integration of advanced technologies to enhance precision and control in LDS. Technological advancements such as the development of more precise and controllable delivery mechanisms are crucial as they enable manufacturers to meet the stringent requirements of modern semiconductor processes.

Additionally, the drive towards smaller process nodes below 5nm has introduced unique challenges, particularly in maintaining precision, material compatibility, and contamination control.At sub-5nm levels, even slight deviations in liquid dispensing can impact device performance. This drives the development of LDS technologies for precise material delivery, essential for EUV lithography and advanced deposition techniques.

Another emerging trend is the customization of LDS to support a variety of deposition and etch processes in semiconductor manufacturing. Flexible systems that handle various chemistries are gaining popularity for reducing lead times, enhancing integration, lowering maintenance costs, and supporting more efficient production cycles.

Business Benefits

Adopting advanced Liquid Delivery Systems in semiconductor manufacturing offers several business benefits. These systems improve precision and control, leading to higher yields, lower defects, and reduced production costs, which are essential for profitability in the competitive semiconductor market.

Furthermore, systems that provide more outlets and flexible configurations allow for the simultaneous support of multiple production lines, which can reduce capital outlays and streamline operations. This scalability is particularly beneficial for manufacturers looking to expand their production capabilities without a proportional increase in costs.

The ability to integrate seamlessly with existing control systems and the enhanced performance of vaporizers due to consistent delivery pressures also contribute to operational efficiency. These improvements help in maintaining the continuity of production processes, minimizing downtime, and enhancing overall operational autonomy.

Key Player Analysis

Brooks Instrument is a leader in providing precision flow measurement and control solutions. The company offers advanced Liquid Delivery Systems that are known for their accuracy, reliability, and versatility in semiconductor manufacturing. With an extensive range of flow controllers and sensors, Brooks Instrument serves the semiconductor industry by providing solutions that optimize liquid delivery for critical processes.

Entegris is another top player in the LDS market. They specialize in providing high-performance materials and solutions for semiconductor manufacturing. Entegris’ Liquid Delivery Systems are built to handle the complex chemical needs of semiconductor production, offering highly accurate and contamination-free delivery.

HORIBA is a global company that has made significant strides in the semiconductor industry, particularly with its liquid delivery solutions. Known for its advanced technology, HORIBA provides a range of LDS products that offer high accuracy and consistency. Their solutions are widely used in semiconductor fabs for critical applications like wafer cleaning, photoresist coating, and etching.

Top Key Players in the Market

- Brooks Instrument

- Entegris

- HORIBA

- Air Liquide

- CSK

- SVCS Process Innovation

- Bronkhorst

- SEMPA

- SIGA GmbH

- Fujifilm

- Stainless Design Concepts (SDC)

- CollabraTech Solutions, LLC

- Foures Co., Ltd

- Other Major Players

Top Opportunities Awaiting for Players

In the landscape of the Liquid Delivery System (LDS) for the semiconductor market, several key opportunities for industry players emerge from current trends and advancements.

- Technological Advancements in LDS: There is a notable push towards enhancing the precision and control of LDS technologies. These improvements are pivotal for manufacturers who aim to increase the efficiency of semiconductor production processes. Advances include better flow control and droplet formation in systems such as Direct Liquid Injection (DLI), which are essential for high-quality semiconductor manufacturing.

- Demand for Miniaturization: The semiconductor industry’s trend towards miniaturization continues to drive the need for highly accurate liquid delivery systems. As devices become smaller, the precision in chemical delivery becomes critical, making advanced LDS technologies indispensable for meeting the stringent requirements of modern semiconductor fabrication.

- Sustainability Initiatives: Environmental sustainability is becoming increasingly crucial. In response, companies are focusing on developing more sustainable and environmentally friendly LDS solutions. This includes reducing the environmental impact of the chemicals used, improving recycling processes, and minimizing waste.

- Expansion of Manufacturing Facilities: With the continuous growth in semiconductor demand, companies are expanding their manufacturing capabilities. This expansion is not just in terms of physical space but also in enhancing the capacity to meet the growing needs of the market. Companies such as Linde Electronics and Entegris have been proactive in this area, setting up larger production facilities to handle increased volumes.

- Integration of IoT and Industry 4.0: The adoption of Internet of Things (IoT) and Industry 4.0 technologies in LDS systems is a transformative trend. These technologies enable remote monitoring, predictive maintenance, and data-driven optimization, which significantly enhance operational efficiencies and reduce downtime in semiconductor manufacturing.

Recent Developments

- HORIBA released the LU-A1000 series in their Liquid Auto Refill System range in 2025, featuring improved automation to prevent operational errors and touch panel controls for enhanced usability. This system supports a variety of liquid precursors used in semiconductor manufacturing, reflecting HORIBA’s commitment to innovation in fluid handling.

- Air Liquide advanced its capabilities in the Direct Liquid Injection (DLI) system market with significant upgrades to their systems in 2025, tailored for high-purity applications in semiconductor production. These enhancements are part of Air Liquide’s broader strategy to support critical processes in semiconductor manufacturing with high reliability and efficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 182.4 Mn |

| Forecast Revenue (2034) | USD 372.4 Mn |

| CAGR (2025-2034) | 7.40% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Terminal Delivery System (TDS), Tri Chemical Trans-fill (TCT)), By Application (Semiconductor Processing Furnace, PVD/CVD Processes, Etching Equipment, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Brooks Instrument, Entegris, HORIBA, Air Liquide, CSK, SVCS Process Innovation, Bronkhorst, SEMPA, SIGA GmbH, Fujifilm, Stainless Design Concepts (SDC), CollabraTech Solutions, LLC, Foures Co., Ltd, Other Major Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

for Semiconductor Market")