Global Laser Welding Machine Market Size, Share, Growth Analysis By Technology (Fiber, CO₂, Solid-State, Diode, Others), By System Type (Robotic-Integrated Cell, Hand-held / Portable, Stationary Bench-top, Hybrid Multi-Function), By Application (Automotive, Electronics & Electrical, Medical Devices, Aerospace & Defense, Jewelry & Watchmaking, Energy & Power, Shipbuilding & Heavy Machinery, Packaging, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Jan 2026

- Report ID: 175635

- Number of Pages: 306

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

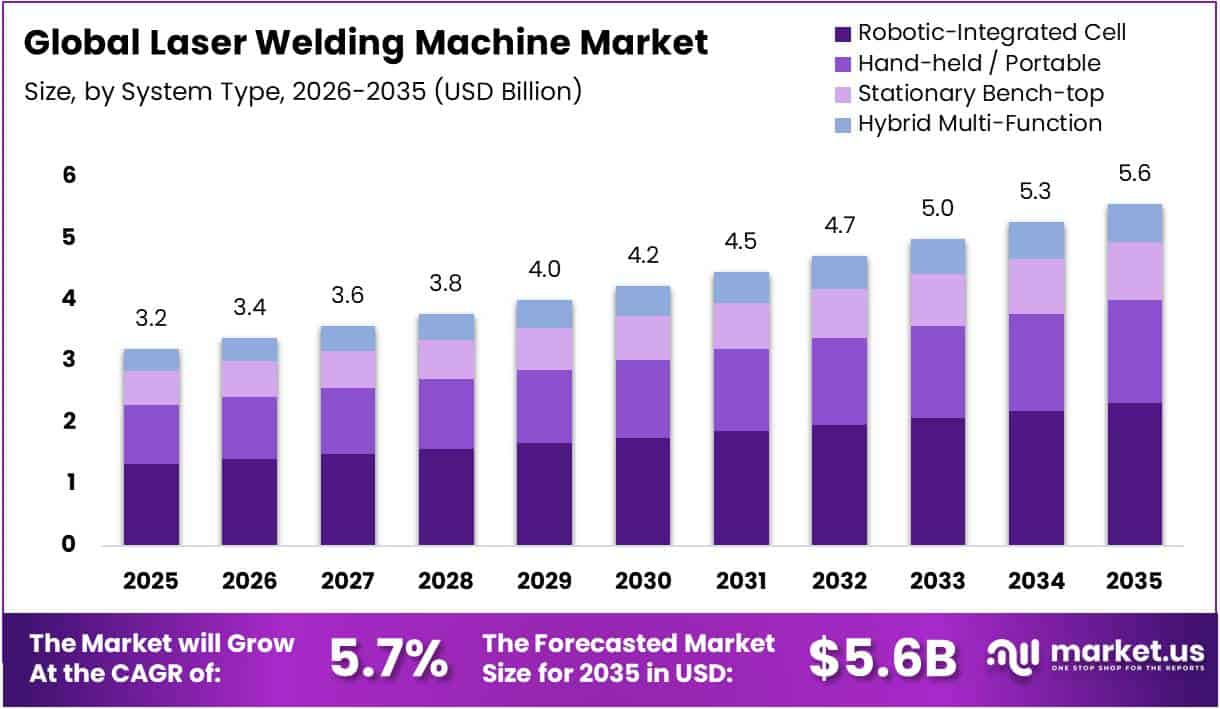

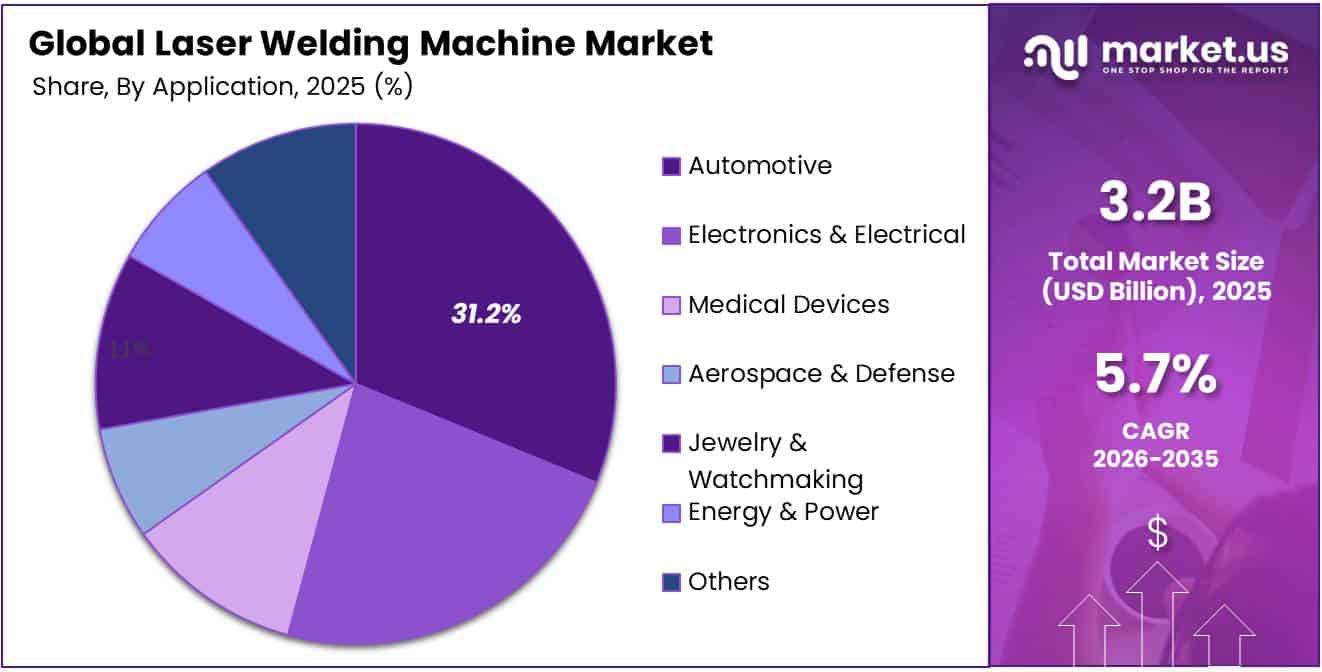

The Global Laser Welding Machine Market size is expected to be worth around USD 5.6 Billion by 2035 from USD 3.2 Billion in 2025, growing at a CAGR of 5.7% during the forecast period 2026 to 2035.

Laser welding machines utilize focused laser beams to join materials through controlled thermal energy. These advanced systems deliver precise, high-quality welds with minimal heat-affected zones. Moreover, they enable non-contact processing that reduces contamination risks and mechanical stress on components.

The technology serves diverse industrial applications requiring clean joining solutions. Industries demand precision welding for dissimilar materials and miniaturized components. Consequently, laser welding addresses critical manufacturing challenges where traditional methods prove inadequate or inefficient.

Market expansion reflects increasing automation integration across manufacturing sectors. Robotic laser welding systems enhance production consistency and throughput significantly. Additionally, the technology supports lightweight material processing essential for modern automotive and aerospace applications.

Government initiatives promoting advanced manufacturing accelerate technology adoption globally. Regulatory frameworks emphasize workplace safety and environmental sustainability in welding operations. Therefore, manufacturers invest in laser solutions that comply with stringent industrial standards and emission requirements.

Growing demand for electric vehicles drives laser welding adoption in battery manufacturing. Energy storage applications require precise joining of thin materials without thermal damage. Furthermore, microfabrication sectors utilize laser welding for medical devices and electronics assembly.

According to research, fully automated laser welding solutions report productivity improvements of 30-40% compared to traditional welding methods, with corresponding reductions in material waste and rework requirements. Robot laser welding machines ensure joint strength consistency with variation of ≤5%, compared to 15-20% for manual welding.

Industrial laser welders range from approximately 500 W to 6000+ W, with less than 500 W for micro-welding, over 2000 W for heavy automotive and aerospace applications, and 1000 W as mid-range. This power versatility enables manufacturers to select appropriate systems for specific application requirements and material thicknesses.

Key Takeaways

- Global Laser Welding Machine Market projected to reach USD 5.6 Billion by 2035 from USD 3.2 Billion in 2025 at 5.7% CAGR

- Fiber technology segment dominates with 42.3% market share in 2025

- Robotic-Integrated Cell system type leads with 41.1% share

- Automotive application holds largest segment with 31.2% market share

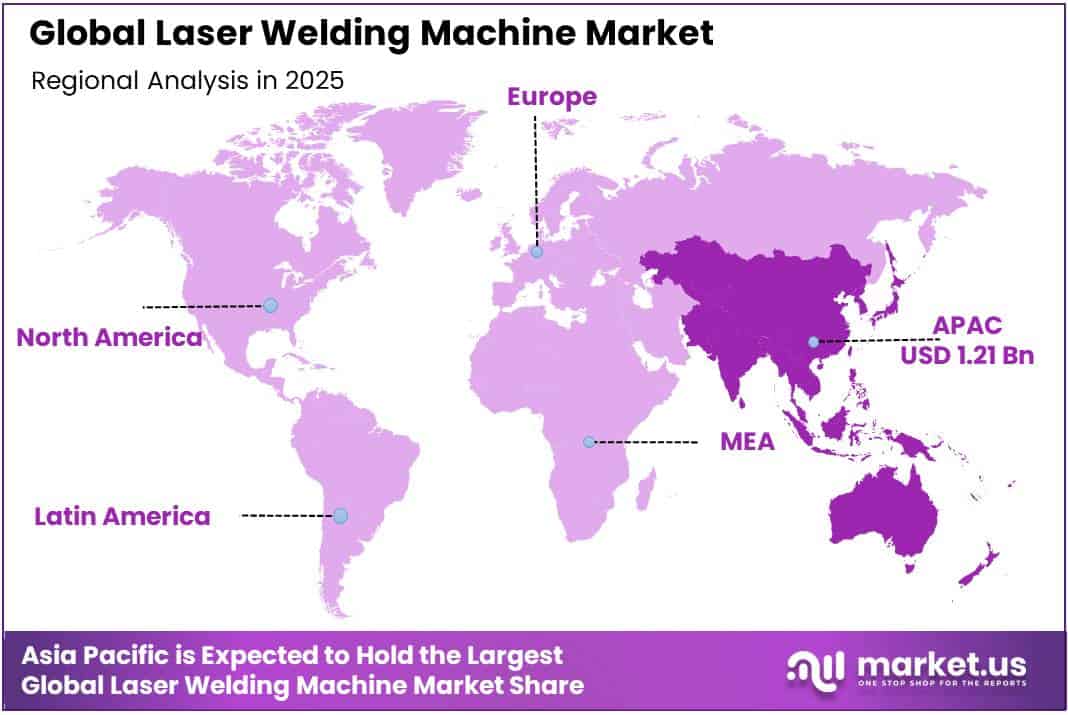

- Asia Pacific region dominates with 38.1% share, valued at USD 1.21 Billion

Technology Analysis

Fiber dominates with 42.3% due to superior beam quality and operational efficiency.

In 2025, Fiber held a dominant market position in the By Technology segment of Laser Welding Machine Market, with a 42.3% share. Fiber laser technology delivers exceptional beam quality and energy efficiency for industrial applications. Additionally, these systems offer lower maintenance requirements and extended operational lifespans compared to alternative technologies.

CO₂ laser systems remain prevalent for thick material processing and specialized industrial applications. These established platforms provide reliable performance for heavy-duty welding operations. However, their market presence gradually declines as fiber technology advances and costs decrease across manufacturing sectors.

Solid-State lasers serve niche applications requiring specific wavelength characteristics and pulse configurations. These systems enable precise control for medical device manufacturing and jewelry applications. Moreover, solid-state technology supports micro-welding operations where thermal management proves critical for component integrity.

Diode lasers offer compact form factors and cost-effective solutions for moderate power welding applications. These systems provide efficient performance for plastic welding and lower-intensity metal joining operations. Furthermore, diode technology enables portable configurations suitable for field service and repair applications.

Others category encompasses emerging laser technologies including excimer and green lasers for specialized applications. These alternative systems address unique material compatibility and processing requirements in niche industrial sectors. Consequently, diverse laser technologies expand overall market capabilities and application possibilities.

System Type Analysis

Robotic-Integrated Cell dominates with 41.1% due to automation capabilities and production consistency.

In 2025, Robotic-Integrated Cell held a dominant market position in the By System Type segment of Laser Welding Machine Market, with a 41.1% share. Robotic integration enables automated production workflows with minimal human intervention. Consequently, manufacturers achieve superior consistency, reduced labor costs, and enhanced safety in welding operations.

Hand-held / Portable systems provide flexibility for on-site repairs and small-batch production requirements. These mobile solutions enable field welding operations where stationary equipment proves impractical. Additionally, portable systems support maintenance activities and prototyping applications across diverse industrial environments.

Stationary Bench-top configurations serve laboratory settings and precision manufacturing applications. These systems deliver stable platforms for research development and quality control testing. Furthermore, bench-top units accommodate customized tooling and fixture integration for specialized welding processes.

Hybrid Multi-Function systems combine laser welding with complementary processes including cutting, marking, and surface treatment capabilities. These versatile platforms maximize equipment utilization and reduce capital investment requirements for manufacturers. Moreover, hybrid systems enable seamless process transitions and integrated manufacturing workflows within single production cells.

Application Analysis

Automotive dominates with 31.2% due to extensive vehicle assembly and component fabrication requirements.

In 2025, Automotive held a dominant market position in the By Application segment of Laser Welding Machine Market, with a 31.2% share. Automotive manufacturing demands precision welding for body panels, powertrain components, and battery assemblies. Moreover, electric vehicle production accelerates laser welding adoption for lightweight materials and thermal-sensitive battery connections.

Electronics & Electrical sectors utilize laser welding for miniaturized component assembly and circuit board manufacturing. These applications require minimal heat input to protect sensitive electronic elements. Additionally, consumer electronics production benefits from the speed and precision that laser technology delivers consistently.

Medical Devices manufacturing relies on laser welding for hermetic sealing and biocompatible material joining. Regulatory compliance necessitates precise, contamination-free welding processes for implantable devices. Furthermore, surgical instrument production demands the clean joining characteristics that laser systems uniquely provide.

Aerospace & Defense applications require high-reliability welds for critical structural and propulsion components. These sectors demand stringent quality standards and traceability throughout manufacturing processes. Consequently, laser welding addresses aerospace requirements for lightweight materials and complex geometries effectively.

Jewelry & Watchmaking industries utilize laser welding for delicate precious metal joining and intricate component assembly. These applications demand minimal heat-affected zones to preserve aesthetic qualities and material properties. Therefore, laser technology enables repair operations and fine detailing impossible with traditional welding methods.

Energy & Power sectors employ laser welding for renewable energy equipment and power generation component manufacturing. Solar panel production and wind turbine assembly benefit from precise, high-speed welding capabilities. Additionally, nuclear and fossil fuel applications require certified welding processes for pressure vessels and critical infrastructure.

Shipbuilding & Heavy Machinery utilize laser welding for structural fabrication and large-scale component assembly. These industries benefit from deep penetration welding capabilities for thick material sections. Moreover, automation integration reduces manual labor requirements in demanding fabrication environments.

Packaging industry adopts laser welding for hermetic sealing of food containers and pharmaceutical packaging applications. These systems enable contactless processing that maintains sterile production conditions. Furthermore, laser technology supports high-speed production lines with consistent seal quality and minimal material contamination.

Others category includes diverse applications across construction, consumer goods, and specialty manufacturing sectors. These emerging applications expand laser welding adoption into new market segments. Consequently, technology versatility continues driving market diversification and growth opportunities.

Key Market Segments

By Technology

- Fiber

- CO₂

- Solid-State

- Diode

- Others

By System Type

- Robotic-Integrated Cell

- Hand-held / Portable

- Stationary Bench-top

- Hybrid Multi-Function

By Application

- Automotive

- Electronics & Electrical

- Medical Devices

- Aerospace & Defense

- Jewelry & Watchmaking

- Energy & Power

- Shipbuilding & Heavy Machinery

- Packaging

- Others

Drivers

Rapid Integration of Laser Welding with Automated Production Systems Drives Market Growth

Manufacturing sectors increasingly adopt automated laser welding solutions to enhance production efficiency and consistency. Robotic integration enables continuous operation with minimal human intervention and reduced error rates. Consequently, industries achieve significant cost savings through improved throughput and decreased material waste in welding operations.

Automated systems deliver superior quality control compared to traditional manual welding methods. Smart sensors and real-time monitoring capabilities ensure consistent weld parameters throughout production runs. Moreover, integration with digital manufacturing platforms enables data-driven process optimization and predictive maintenance scheduling.

Rising labor costs and skilled welder shortages accelerate automation adoption across global manufacturing facilities. Companies invest in robotic laser welding cells to maintain competitive production capabilities. Therefore, automated laser welding technology becomes essential for manufacturers seeking operational excellence and market competitiveness.

Restraints

Technical Complexity in Process Parameter Optimization Limits Market Adoption

Laser welding requires precise control of multiple interdependent parameters including power, speed, and focal position. Inexperienced operators struggle to optimize settings for different materials and joint configurations. Consequently, manufacturers face extended learning curves and potential quality issues during initial implementation phases.

Process development demands significant engineering expertise and iterative testing to achieve desired weld characteristics. Material variations and design changes necessitate parameter adjustments that challenge production consistency. Additionally, limited in-house technical knowledge forces companies to rely on external consultants and equipment suppliers.

High initial investment costs for training programs and process development deter smaller manufacturers from adoption. Companies must balance equipment expenses with ongoing workforce development and technical support requirements. Therefore, technical complexity creates barriers particularly for small and medium enterprises entering laser welding markets.

Growth Factors

Expanding Application Scope in Microfabrication and Miniaturized Components Accelerates Market Expansion

Electronics miniaturization drives demand for precision welding technologies capable of joining microscopic components. Laser systems enable controlled energy delivery essential for micro-scale applications without thermal damage. Moreover, medical device manufacturers increasingly adopt laser welding for miniaturized implantable devices and surgical instruments.

Growing Internet of Things and wearable technology markets create new opportunities for micro-welding applications. These emerging sectors require hermetic sealing and reliable electrical connections in compact form factors. Additionally, sensor manufacturing and semiconductor packaging utilize laser welding for precise component assembly.

Battery technology advancement for electric vehicles and energy storage demands sophisticated joining techniques. Laser welding addresses critical requirements for thin foil materials and thermal-sensitive connections in battery cells. Therefore, expanding microfabrication applications position laser welding as essential technology for next-generation manufacturing processes.

Emerging Trends

Integration of Smart Sensors for Enhanced Weld Quality Consistency Reshapes Market Landscape

Manufacturing facilities increasingly implement intelligent monitoring systems for real-time weld quality assessment and control. Smart sensors detect process variations and automatically adjust parameters to maintain optimal welding conditions. Consequently, manufacturers achieve unprecedented consistency and reduce defect rates throughout production operations.

Digital twin technology enables virtual process simulation before physical production implementation. Engineers optimize welding parameters through computational modeling that predicts thermal behavior and joint characteristics. Moreover, simulation-based approaches significantly reduce development time and material costs during process qualification phases.

Hybrid laser welding techniques combine multiple energy sources to expand process capabilities and material compatibility. These innovative approaches address challenges in dissimilar material joining and thick section welding. Therefore, technological convergence creates new application possibilities and competitive advantages for early adopters.

Regional Analysis

Asia Pacific Dominates the Laser Welding Machine Market with a Market Share of 38.1%, Valued at USD 1.21 Billion

Asia Pacific commands the largest market position with 38.1% share, valued at USD 1.21 Billion, driven by extensive manufacturing activity and automotive production. China, Japan, and South Korea lead regional adoption through government initiatives supporting advanced manufacturing technologies. Moreover, growing electronics production and electric vehicle manufacturing accelerate laser welding system deployment across the region.

North America Laser Welding Machine Market Trends

North America demonstrates strong market presence through aerospace, defense, and medical device manufacturing sectors. Advanced research facilities and technology leadership drive innovation in laser welding applications. Additionally, reshoring initiatives and automation investments support sustained market growth across United States and Canadian manufacturing industries.

Europe Laser Welding Machine Market Trends

Europe maintains significant market share through automotive excellence and precision engineering capabilities. Germany leads regional adoption with established manufacturing infrastructure and Industry 4.0 initiatives. Furthermore, stringent quality standards and environmental regulations encourage laser welding technology adoption throughout European industrial sectors.

Middle East & Africa Laser Welding Machine Market Trends

Middle East and Africa exhibit emerging market potential through infrastructure development and industrial diversification efforts. Energy sector investments and shipbuilding activities drive laser welding adoption in Gulf Cooperation Council nations. However, market growth remains constrained by limited manufacturing infrastructure and technical expertise availability.

Latin America Laser Welding Machine Market Trends

Latin America shows gradual market development through automotive manufacturing and energy sector applications. Brazil and Mexico attract foreign manufacturing investments that incorporate advanced welding technologies. Nevertheless, economic volatility and capital constraints moderate the pace of laser welding system adoption across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

TRUMPF Group maintains global leadership in laser technology through comprehensive product portfolios and continuous innovation investments. The company delivers integrated laser welding solutions for automotive, electronics, and medical device manufacturing sectors. Moreover, TRUMPF provides extensive technical support and training programs that enhance customer productivity and process optimization capabilities across diverse industrial applications.

IPG Photonics Corporation specializes in high-power fiber laser systems that deliver superior performance and reliability. Their advanced photonics technology enables efficient energy conversion and exceptional beam quality for demanding welding applications. Additionally, IPG focuses on expanding market presence through strategic partnerships and development of application-specific laser solutions.

Han’s Laser Technology Group represents Asia’s leading laser equipment manufacturer with extensive domestic and international market presence. The company offers cost-competitive solutions that address diverse industrial welding requirements across multiple sectors. Furthermore, Han’s Laser invests significantly in research development to advance laser technology capabilities and expand application portfolios.

Coherent Corp. provides precision laser systems and components for scientific, industrial, and commercial applications worldwide. Their laser welding solutions emphasize process control and quality consistency for high-reliability manufacturing operations. Consequently, Coherent serves demanding aerospace, medical, and semiconductor sectors requiring stringent performance standards and traceability.

Key players

- TRUMPF Group

- IPG Photonics Corporation

- Han’s Laser Technology Group

- Coherent Corp.

- Jenoptik AG

- Emerson Electric (Branson)

- FANUC Robotics

- Panasonic Smart Factory

- Huagong Laser Engineering

- Wuhan Golden Laser

- LaserStar Technologies

- Amada Miyachi

- Baison Laser

- Alpha Laser GmbH

- NLight Inc.

- Other Key Players

Recent Developments

- In November 2025, Prima Additive was fully acquired by Sodick and rebranded as AltForm, expanding its portfolio to include laser remote welding and other advanced laser production technologies for enhanced manufacturing capabilities.

- In March 2025, Hymson Novolas AG, a subsidiary of the globally active technology group Hymson Laser Technology Group Co. Ltd., acquired the laser plastic welding business from Leister Technologies AG to strengthen its market position.

- In March 2025, Laserax acquired leading UV laser manufacturer DPSS Lasers Inc. to broaden its technology offerings and expand capabilities in precision laser processing applications across multiple industrial sectors.

Report Scope

Report Features Description Market Value (2025) USD 3.2 Billion Forecast Revenue (2035) USD 5.6 Billion CAGR (2026-2035) 5.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Technology (Fiber, CO₂, Solid-State, Diode, Others), By System Type (Robotic-Integrated Cell, Hand-held / Portable, Stationary Bench-top, Hybrid Multi-Function), By Application (Automotive, Electronics & Electrical, Medical Devices, Aerospace & Defense, Jewelry & Watchmaking, Energy & Power, Shipbuilding & Heavy Machinery, Packaging, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape TRUMPF Group, IPG Photonics Corporation, Han’s Laser Technology Group, Coherent Corp., Jenoptik AG, Emerson Electric (Branson), FANUC Robotics, Panasonic Smart Factory, Huagong Laser Engineering, Wuhan Golden Laser, LaserStar Technologies, Amada Miyachi, Baison Laser, Alpha Laser GmbH, NLight Inc., Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Laser Welding Machine MarketPublished date: Jan 2026add_shopping_cartBuy Now get_appDownload Sample

Laser Welding Machine MarketPublished date: Jan 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- TRUMPF Group

- IPG Photonics Corporation

- Han's Laser Technology Group

- Coherent Corp.

- Jenoptik AG

- Emerson Electric (Branson)

- FANUC Robotics

- Panasonic Smart Factory

- Huagong Laser Engineering

- Wuhan Golden Laser

- LaserStar Technologies

- Amada Miyachi

- Baison Laser

- Alpha Laser GmbH

- NLight Inc.

- Other Key Players

Our Clients

- 175635

- Jan 2026