Global Laser Therapy Devices Market By Device Type (Solid State Laser Systems, Dye Laser Systems and Gas Laser Systems), By Application (Ophthalmology, Cardiovascular, Dentistry, Dermatology, Gynecology, Urology and Others), By End User (Hospitals, Ambulatory Surgical Centers, Specialized Clinics and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179533

- Number of Pages: 351

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

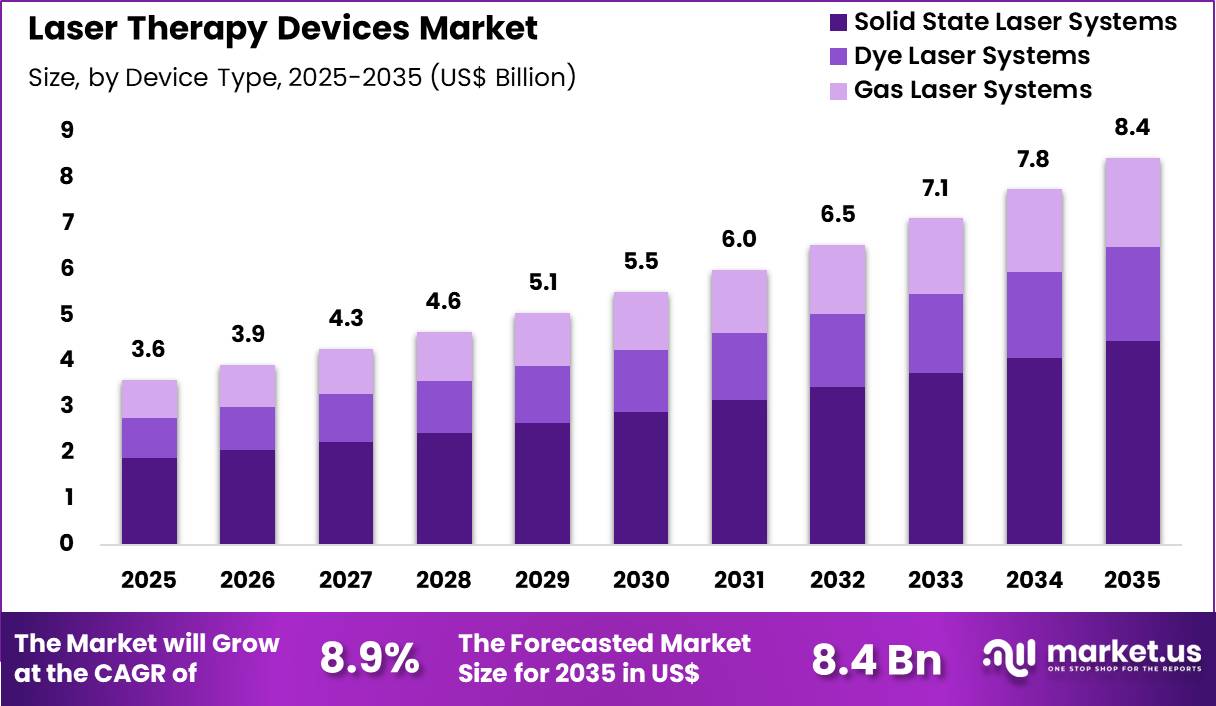

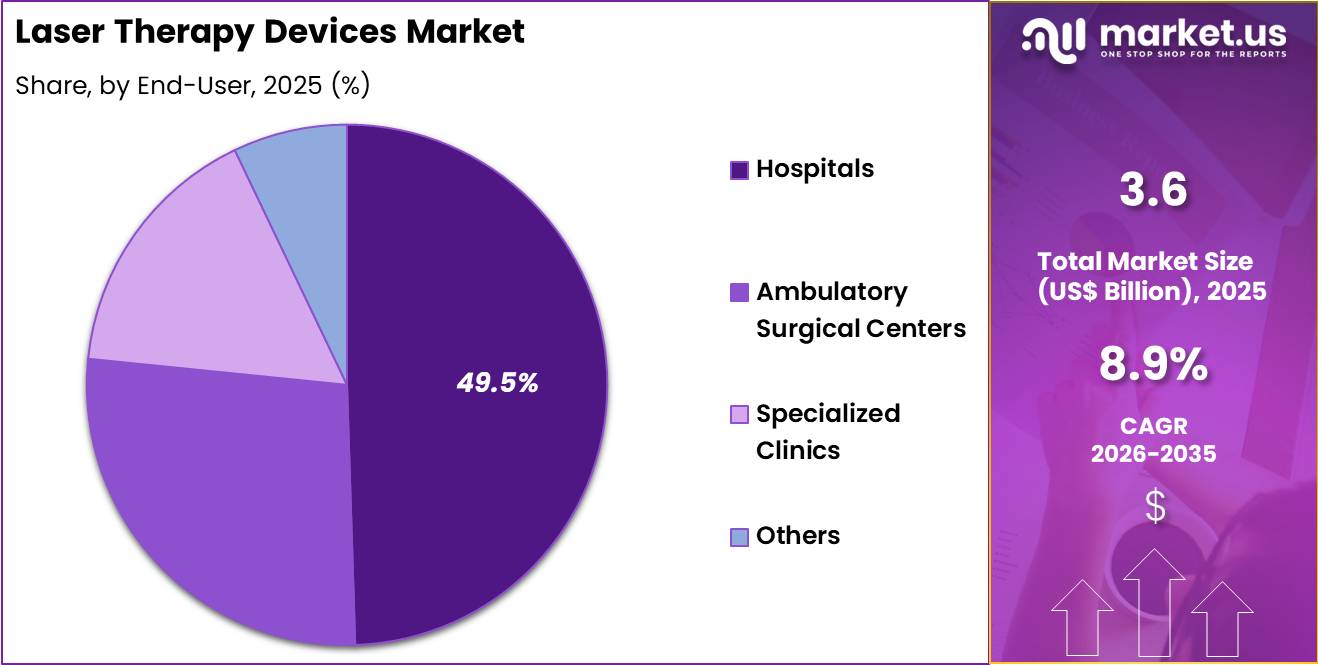

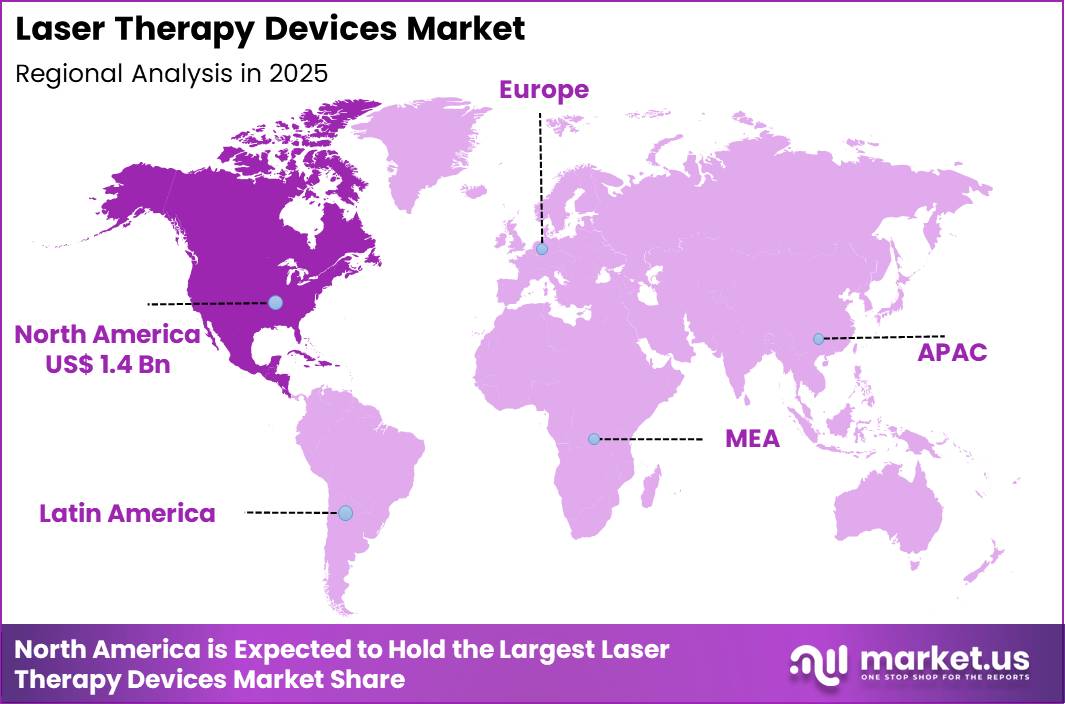

The Global Laser Therapy Devices Market size is expected to be worth around US$ 8.4 Billion by 2035 from US$ 3.6 Billion in 2025, growing at a CAGR of 8.9% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.9% share with a revenue of US$ 1.4 Billion.

Rising prevalence of chronic pain conditions and aesthetic concerns accelerates the laser therapy devices market as healthcare providers and patients seek non-invasive solutions that deliver targeted energy for tissue repair and cosmetic enhancement. Dermatologists increasingly utilize low-level laser therapy devices to stimulate hair follicle growth in androgenetic alopecia, promoting thicker regrowth through photobiomodulation without systemic side effects.

These devices support wound healing applications by accelerating tissue regeneration in diabetic ulcers and surgical incisions, reducing inflammation and enhancing collagen deposition for faster closure. Pain management specialists apply high-intensity laser therapy to treat musculoskeletal disorders, delivering deep penetration that alleviates neuropathic pain and joint inflammation in conditions like osteoarthritis and fibromyalgia.

Ophthalmologists employ selective laser trabeculoplasty to lower intraocular pressure in glaucoma patients, improving aqueous outflow with minimal tissue disruption. Aesthetic practitioners use fractional lasers for skin resurfacing, addressing acne scars, pigmentation disorders, and photoaging by creating controlled microthermal zones that trigger neocollagenesis.

Manufacturers pursue opportunities to develop multi-wavelength platforms that combine ablative and non-ablative modes, expanding applications in vascular lesion treatment and tattoo removal where precise chromophore targeting enhances efficacy.

Developers advance portable, handheld devices with integrated cooling systems, broadening utility in outpatient dermatology and physical therapy clinics for convenient, on-demand sessions. These innovations facilitate combination therapies with topical agents, optimizing outcomes in scar revision and psoriasis management.

Opportunities emerge in AI-assisted dosimetry that personalizes energy delivery based on real-time tissue feedback, improving safety in high-risk skin types. Companies invest in ergonomic designs and user-friendly interfaces that support home-use indications for chronic pain relief. Recent trends emphasize sustainable, energy-efficient lasers and evidence-based protocols, positioning the market for growth in patient-centered, minimally invasive therapeutic and aesthetic care.

Key Takeaways

- In 2025, the market generated a revenue of US$ 3.6 Billion, with a CAGR of 8.9%, and is expected to reach US$ 8.4 Billion by the year 2035.

- The device type segment is divided into solid state laser systems, dye laser systems and gas laser systems, with solid state laser systems taking the lead with a market share of 52.6%.

- Considering application, the market is divided into ophthalmology, cardiovascular, dentistry, dermatology, gynecology, urology and others. Among these, ophthalmology held a significant share of 41.7%.

- Furthermore, concerning the end user segment, the market is segregated into hospitals, ambulatory surgical centers, specialized clinics and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 49.5% in the market.

- North America led the market by securing a market share of 39.9%.

Device Type Analysis

Solid state laser systems accounted for 52.6% of growth within device type and dominate the laser therapy devices market due to their high precision, consistent energy output, and versatility across medical procedures. Their adoption is driven by advancements in cooling systems, portability, and integration with imaging technologies, which improve surgical accuracy.

Hospitals and specialized clinics increasingly prefer solid state lasers for ophthalmology, dermatology, and urology treatments. The segment growth is projected to continue as manufacturers enhance user-friendliness, safety features, and device longevity.

Rising patient awareness of minimally invasive procedures and clinician training programs further support adoption globally. Regulatory approvals and positive clinical outcomes strengthen confidence in solid state systems and drive their sustained demand.

Application Analysis

Ophthalmology accounted for 41.7% of growth within applications and remains the leading segment due to the increasing prevalence of retinal disorders, glaucoma, and cataract cases. Laser interventions provide precise, minimally invasive treatment, reducing recovery times and improving patient outcomes.

Hospitals and eye care clinics implement advanced ophthalmology units to meet rising demand. Segment growth is expected to strengthen as technological improvements, such as enhanced targeting and automated control, increase procedural efficiency.

Awareness campaigns, government initiatives for eye care, and higher reimbursement rates further accelerate adoption. The availability of advanced devices tailored for ophthalmic procedures encourages widespread clinician preference.

End-User Analysis

Hospitals contributed 49.5% of growth within end-users and dominate due to their ability to handle high patient volumes and complex procedures. Hospitals provide access to trained surgical teams, advanced imaging, and integrated rehabilitation services, which supports comprehensive laser therapy treatments.

Growing investment in surgical infrastructure and the expansion of dermatology and ophthalmology departments drive adoption. Segment growth is anticipated to continue as hospitals upgrade older systems, adopt newer solid state lasers, and incorporate multi-specialty procedural capabilities. Partnerships with device manufacturers for staff training and device optimization further enhance clinical confidence and ensure high-quality outcomes.

Key Market Segments

By Device Type

- Solid State Laser Systems

- Dye Laser Systems

- Gas Laser Systems

By Application

- Ophthalmology

- Cardiovascular

- Dentistry

- Dermatology

- Gynecology

- Urology

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialized Clinics

- Others

Drivers

Increasing adoption of minimally invasive procedures is driving the market.

The growing preference for minimally invasive treatments has significantly boosted the demand for laser therapy devices, which enable precise, targeted interventions with reduced recovery times and complications. Enhanced patient outcomes in dermatology, ophthalmology, and urology have led to greater clinical acceptance of these systems.

Healthcare providers are increasingly utilizing laser devices to support outpatient procedures that minimize hospital stays. The correlation between rising aesthetic consciousness and non-surgical options further amplifies the need for versatile laser platforms. Government health initiatives promote safe, effective alternatives to traditional surgery.

Laser therapy devices offer controlled energy delivery for tissue ablation and coagulation. National health policies emphasize innovation in medical technology to improve access. Key manufacturers are developing multi-wavelength systems to meet this clinical requirement. This driver fosters expansion in both therapeutic and cosmetic applications. Minimally Invasive Surgery is gaining popularity, which is propelling the growth of the laser therapy devices market.

Restraints

High cost of laser therapy devices is restraining the market.

The substantial pricing of advanced laser therapy systems, including multi-mode platforms and maintenance contracts, limits their accessibility in resource-constrained healthcare facilities. Complex engineering for wavelength control and safety features contributes to elevated production expenses.

Smaller clinics often defer upgrades, preferring conventional treatments due to financial limitations. Regulatory compliance for laser classification adds to the overall cost structure for suppliers. In public health systems, allocation priorities favor basic equipment over premium laser devices.

Providers must balance therapeutic benefits against economic viability when selecting these systems for routine use. This restraint impacts scalability, particularly in developing economies with limited funding. Industry efforts to introduce entry-level models aim to alleviate pricing pressures partially. Despite procedural advantages, the cost factor hinders universal implementation. The high cost of laser therapy devices is a major restraint in the market.

Opportunities

Expansion into emerging markets is creating growth opportunities.

The rapid development of healthcare infrastructure in Asia-Pacific and Latin America offers avenues for laser therapy devices to penetrate underserved regions with growing medical tourism. Governmental investments in medical technology support the integration of laser systems in new hospitals and clinics.

Increasing disposable incomes in these areas amplify potential for aesthetic and therapeutic laser applications. Partnerships with local distributors facilitate regulatory navigation and customized training. The large patient populations in populous nations magnify prospects for device utilization in diverse specialties.

Educational programs for physicians promote standardized use in emerging healthcare systems. This opportunity enables global firms to diversify beyond mature markets. Key corporations are establishing regional operations to optimize supply and reduce logistics costs.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic trends shape the laser therapy devices market by influencing hospital budgets, elective procedure spending, and clinic investment cycles. Rising inflation and higher interest rates increase the cost of advanced laser systems and slow capital procurement.

Geopolitical tensions disrupt the supply of critical optical components, diodes, and cooling systems, creating intermittent shortages and operational delays. Current US tariffs on imported lasers and related electronics raise acquisition costs, which pressures margins for smaller manufacturers and clinics. These challenges can restrict expansion in price-sensitive regions and delay adoption of next-generation devices.

On the positive side, tariffs encourage domestic assembly, service infrastructure, and local partnerships, strengthening supply reliability. Growing adoption of minimally invasive treatments and rehabilitation applications drives consistent demand. With focused sourcing, technological innovation, and service-led value, the market remains positioned for resilient growth.

Latest Trends

Technological advancements in laser therapy instruments is a recent trend in the market.

In 2024, the introduction of frequency-doubled laser therapy instruments has advanced treatment precision for dermatological and ophthalmic applications. These devices incorporate dual-wavelength capabilities to target specific tissues with minimal damage.

Manufacturers have emphasized portability and user-friendly interfaces for clinic use. Clinical evaluations in 2024 confirmed improved efficacy in skin rejuvenation and retinal procedures. Key players include Han’s Laser and Wuhan Raycus. This development addresses limitations in traditional single-wavelength lasers for multi-layer treatments.

The trend focuses on integration with imaging systems for real-time guidance. Regulatory clearances in 2024 for these instruments have accelerated clinical integration. Industry collaborations refine beam profiles for enhanced safety. These innovations aim to expand therapeutic indications while reducing session times in outpatient settings.

Regional Analysis

North America is leading the Laser Therapy Devices Market

North America experienced significant expansion in the laser therapy devices market in 2024, driven by rising clinical demand for non‑invasive and minimally invasive procedures that improve patient outcomes while reducing recovery times. The region accounted for 39.9 % of global activity, reflecting high adoption rates of advanced laser technologies across dermatology, pain management and surgical specialties.

Large hospital networks and outpatient clinics invested in next‑generation laser platforms that offer improved precision and versatility, responding to clinician preferences and patient demand for efficient treatments. Growth in cosmetic and aesthetic procedures, including skin resurfacing and hair removal, further bolstered utilisation of therapeutic laser systems in specialised clinics and med spas.

Government support for medical innovation and favourable reimbursement frameworks encouraged wider integration of laser applications into routine clinical practice. Equipment manufacturers introduced portable and multi‑platform solutions that enabled flexibility across care settings, increasing overall procedural volumes.

Training programs for clinicians on emerging laser protocols strengthened clinical confidence and adoption. A supporting statistic is that the U.S. medical lasers market was valued at USD 1.89 billion in 2022, underscoring the robust base from which regional growth continued into 2024.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is forecast to register strong growth throughout the forecast period as healthcare infrastructure modernises and consumer demand for advanced therapeutic options expands. Rapid increases in elective and therapeutic laser treatments across countries such as China, Japan, South Korea and India have encouraged hospitals and specialty clinics to adopt a broader range of laser platforms.

Rising disposable incomes and greater healthcare spending enabled more patients to access treatment options that offer reduced discomfort and shorter recovery periods compared to traditional surgical approaches. Local manufacturers and international firms expanded distribution networks and tailored laser solutions to meet diverse clinical needs, from pain management to dermatological care.

Training initiatives and partnerships between regional providers and global experts improved clinician skills and confidence with laser applications. Public awareness campaigns emphasising non‑invasive care options further stimulated patient uptake.

A verifiable data point supporting this trend is that the Asia‑Pacific region accounted for 40 % of global non‑invasive procedures in 2022, reflecting strong acceptance and utilisation of advanced treatments across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the laser therapy devices market grow by enhancing energy delivery accuracy, optimizing wavelength specificity, and expanding application‑focused platforms that support pain management, wound healing, and musculoskeletal rehabilitation with improved clinical outcomes.

They also strengthen value propositions by integrating intuitive user interfaces, safety features, and data tracking tools that help clinicians standardize treatment protocols and demonstrate efficacy to referral sources. Firms pursue strategic partnerships with physical therapy networks, sports medicine clinics, and pain management centers to embed their technologies into broader care pathways and secure recurring utilization.

Geographic expansion into North America, Europe, and high‑growth Asia Pacific diversifies revenue bases and captures rising adoption driven by aging populations and demand for non‑invasive therapies. Zimmer Biomet Holdings, Inc. exemplifies a diversified musculoskeletal health company with a growing portfolio of therapeutic laser systems, strong global distribution channels, and coordinated commercial strategies that align product innovations with clinician preferences.

The company advances its competitive agenda through disciplined investment in R&D, targeted collaborations that extend procedural reach, and a customer‑centric approach that aligns technical enhancements with measurable clinical and operational value.

Laser Therapy Devices Market

- Lumenis

- Cynosure

- Syneron Candela

- Fotona

- Cutera

- BIOLITEC

- Quanta System

- Asclepion Laser Technologies

- El.En. Group

- Fotofinder Systems

Recent Developments

- In February 2024, Iridex Corporation obtained a European patent (EP 3009093) for its MicroPulse short-pulse laser technology. The innovation allows highly controlled laser bursts that reduce retinal damage compared to conventional laser treatments. Clinical evaluations have confirmed the system’s safety and efficacy for retinal and glaucoma procedures, representing a notable step forward in precision ophthalmic therapy.

- In May 2023, Norlase raised USD 11 million in its largest funding round, led by West Hill Capital in London. Following FDA clearance and CE mark approval for its ECHO pattern laser, the investment will support scaling production of the ECHO device and development of additional laser-based oncology treatments, advancing precision therapies for cancer care.

Report Scope

Report Features Description Market Value (2025) US$ 3.6 Billion Forecast Revenue (2035) US$ 8.4 Billion CAGR (2026-2035) 8.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Device Type (Solid State Laser Systems, Dye Laser Systems and Gas Laser Systems), By Application (Ophthalmology, Cardiovascular, Dentistry, Dermatology, Gynecology, Urology and Others), By End User (Hospitals, Ambulatory Surgical Centers, Specialized Clinics and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Lumenis, Cynosure, Syneron Candela, Fotona, Cutera, BIOLITEC, Quanta System, Asclepion Laser Technologies, El.En. Group, Fotofinder Systems Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Laser Therapy Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Laser Therapy Devices MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Lumenis

- Cynosure

- Syneron Candela

- Fotona

- Cutera

- BIOLITEC

- Quanta System

- Asclepion Laser Technologies

- El.En. Group

- Fotofinder Systems

Our Clients

- 179533

- Feb 2026