Global Laboratory Supplies Market By Product Type (Equipment (Autoclaves & Sterilizers, Centrifuges, Incubators, Lab Air Filtration System, Laminar Flow Hood, Micro Manipulation Systems, Scopes, Sonicators & Homogenizers and Others) and Consumables (Cell Culture Consumables, Cell Imaging Consumables, Dishes, Gloves, Masks, Pipettes, Tips and Tubes)), By End-user (Academic Institutions, Pharmaceutical & Biotechnology Companies and Clinical & Diagnostic Laboratories), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179512

- Number of Pages: 327

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

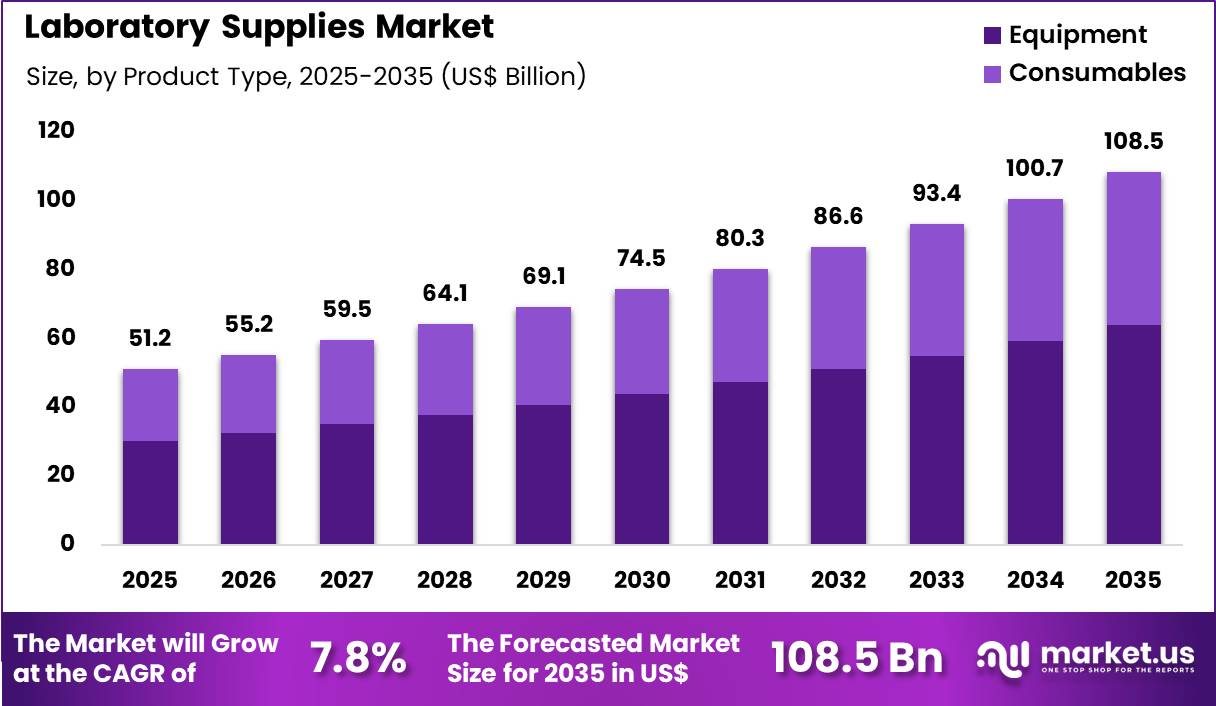

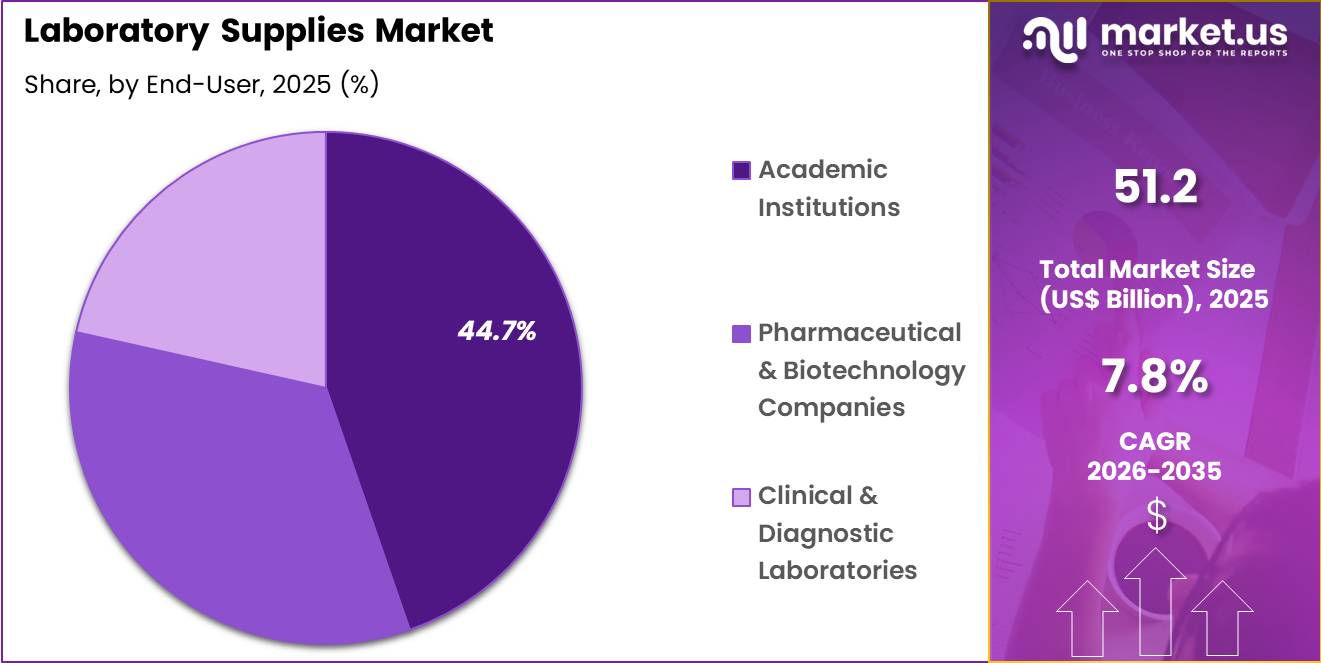

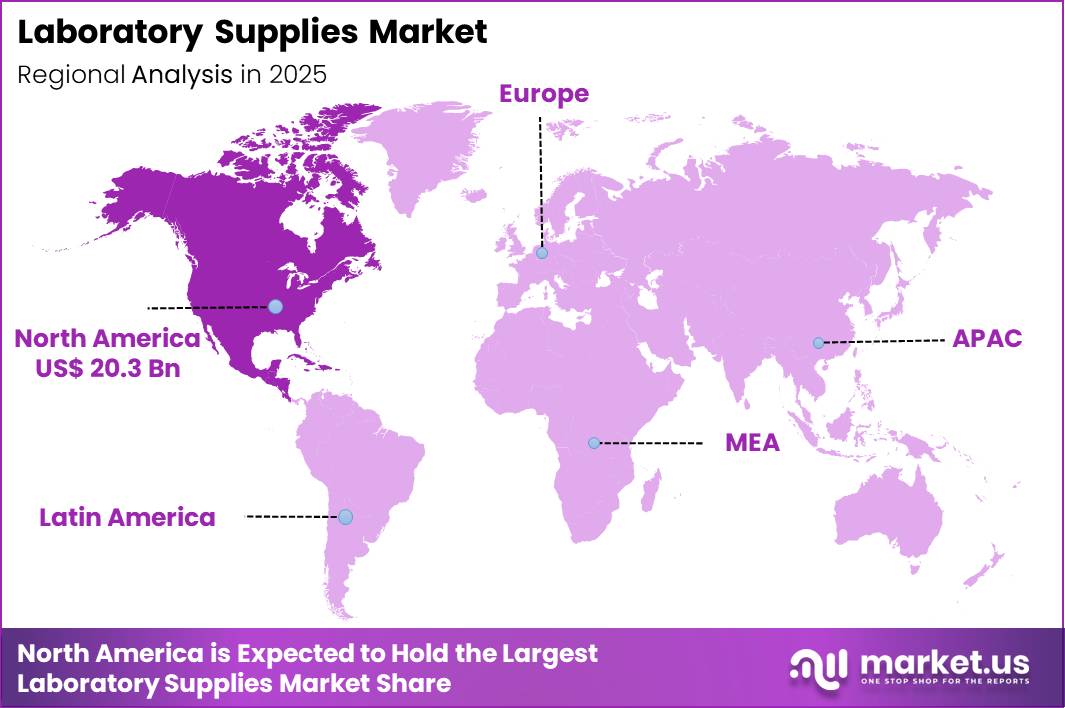

The Global Laboratory Supplies Market size is expected to be worth around US$ 108.5 Billion by 2035 from US$ 51.2 Billion in 2025, growing at a CAGR of 7.8% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.7% share with a revenue of US$ 20.3 Billion.

Rising demand for advanced research and diagnostic capabilities drives the laboratory supplies market as scientific institutions and industries require reliable consumables to support high-precision experimentation and quality control.

Researchers increasingly utilize pipette tips and microplates in molecular biology workflows, enabling accurate liquid handling during PCR setup, DNA extraction, and high-throughput screening assays. These supplies support cell culture applications through sterile flasks, dishes, and serological pipettes that maintain contamination-free environments for mammalian and microbial propagation in drug discovery and vaccine development.

Analytical laboratories apply centrifuge tubes and filtration units to process biological samples, facilitating separation of cellular components and purification of proteins or nucleic acids. Clinical diagnostics depend on test tubes, slides, and cuvettes for routine hematology, chemistry, and microbiology testing, ensuring reproducible results in patient sample analysis.

Industrial quality assurance teams use petri dishes and swabs for microbial monitoring in pharmaceutical manufacturing, verifying sterility and environmental safety. Manufacturers pursue opportunities to develop sustainable laboratory supplies with biodegradable plastics and recyclable packaging, expanding applications in eco-conscious research facilities conducting genomics and proteomics studies.

Developers advance ergonomic and low-retention pipette tips that minimize sample loss, broadening utility in sensitive assays involving low-concentration analytes. These innovations facilitate automation-compatible consumables that integrate seamlessly with robotic liquid handlers, accelerating high-throughput drug screening and next-generation sequencing library preparation.

Opportunities emerge in smart consumables embedded with traceability features for chain-of-custody in regulated environments. Companies invest in precision-engineered multi-well plates with optical clarity enhancements, improving imaging and fluorescence-based readouts.

Recent trends emphasize modular, single-use systems and antimicrobial coatings, positioning laboratory supplies as essential enablers of efficiency, reproducibility, and innovation across life sciences research, clinical diagnostics, and industrial testing.

Key Takeaways

- In 2025, the market generated a revenue of US$ 51.2 Billion, with a CAGR of 7.8%, and is expected to reach US$ 108.5 Billion by the year 2035.

- The product type segment is divided into equipment and consumable, with equipment taking the lead with a market share of 58.9%.

- Considering end-user, the market is divided into academic institutions, pharmaceutical & biotechnology companies and clinical & diagnostic laboratories. Among these, academic institutions held a significant share of 44.7%.

- North America led the market by securing a market share of 39.7%.

Product Type Analysis

Equipment accounted for 58.9% of growth in product type. Their adoption is driven by the critical need to sterilize instruments, media, and glassware in laboratories. Increasing safety regulations and compliance standards in academic and research settings fuel demand.

Universities and research institutes prioritize reliable, high-efficiency sterilization systems to support teaching labs and experimental work. Innovations in compact designs, automation, and digital monitoring enhance usability and efficiency, making them more attractive.

Rising laboratory infrastructure investments, especially in emerging regions, further contribute to market expansion. Integration of energy-efficient and user-friendly models encourages broader adoption. Segment growth is projected to strengthen as research programs and practical courses expand globally.

End-User Analysis

Academic institutions led with 44.7% growth among end-users, driven by the rise in laboratory-based teaching and research initiatives. The increasing number of higher education programs in life sciences and biotechnology encourages procurement of modern laboratory equipment. Reliable and long-lasting instruments are prioritized to support multi-year curricula and hands-on training.

Public funding and research grants allow institutions to upgrade laboratories, including autoclaves, centrifuges, and microscopes. Demand is further supported by partnerships with industry and the need for standardized, reproducible laboratory practices.

Segment growth is anticipated to continue as institutions implement eco-friendly, energy-efficient, and automated solutions. Academic adoption often influences trends in other sectors, maintaining strong market presence.

Key Market Segments

By Product Type

- Equipment

- Autoclaves & Sterilizers

- Centrifuges

- Incubators

- Lab Air Filtration System

- Laminar Flow Hood

- Micro Manipulation Systems

- Scopes

- Sonicators& Homogenizers

- Others

- Consumables

- Cell Culture Consumables

- Cell Imaging Consumables

- Dishes

- Gloves

- Masks

- Pipettes

- Tips

- Tubes

By End-user

- Academic Institutions

- Pharmaceutical & Biotechnology Companies

- Clinical & Diagnostic Laboratories

Drivers

Rising number of diagnostic and research laboratories is driving the market.

The steady expansion of diagnostic laboratories and research facilities worldwide has substantially increased the consumption of laboratory supplies, including consumables and basic equipment. Greater investment in healthcare infrastructure has led to more facilities performing routine testing and specialized analyses.

Academic institutions are establishing additional research centers focused on biotechnology and life sciences. The correlation between population growth and healthcare service expansion amplifies demand for essential supplies such as pipettes, tubes, and reagents. Government programs supporting medical education and public health surveillance contribute to new laboratory openings.

Laboratory supplies enable consistent performance of analytical procedures across diverse testing volumes. National health statistics indicate ongoing growth in laboratory-based diagnostics. Key suppliers are scaling production to meet this procedural surge. This driver supports steady procurement in both public and private sectors. The number of registered clinical laboratories in the United States increased from approximately 330,000 in 2022 to over 340,000 in 2024.

Restraints

High raw material and logistics costs are restraining the market.

The elevated prices of raw materials used in laboratory consumables, combined with ongoing logistics challenges, have constrained market growth by increasing production expenses. Supply chain disruptions continue to affect availability of critical components for plasticware and glassware. Many manufacturers face higher transportation costs that are passed on to end-users.

The correlation between global commodity price fluctuations and supply pricing further limits affordability for laboratories. Government regulations on material sourcing add compliance costs for suppliers. Smaller laboratories often reduce orders or switch to lower-cost alternatives due to budget constraints. This restraint particularly affects high-volume consumable categories in resource-limited settings.

Industry efforts to localize production provide partial mitigation. Despite consistent demand, cost pressures slow the replacement cycle of laboratory supplies. High raw material and logistics costs remain a primary market restraint.

Opportunities

Expansion of biotechnology research funding is creating growth opportunities.

The allocation of additional public and private funding to biotechnology research presents significant potential for laboratory supplies in academic and industrial settings. Governmental initiatives supporting life sciences innovation encourage procurement of consumables for molecular biology and cell culture applications.

Increasing number of biotech startups amplifies demand for basic laboratory equipment and reagents. Partnerships between research institutions and suppliers facilitate customized supply agreements. The large number of funded projects in genomics and proteomics magnifies prospects for consumable utilization.

Educational programs for researchers promote standardized use of high-quality supplies. This opportunity enables manufacturers to develop specialized product lines for biotechnology workflows. Key companies are establishing dedicated channels for research institutions.

Overall, biotechnology funding growth aligns with efforts to advance scientific discovery. Biotechnology research funding in the United States increased notably between 2022 and 2024 through NIH allocations.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions directly influence the laboratory supplies market by shaping research budgets, procurement cycles, and operational costs for academic, clinical, and industrial labs. Rising inflation and higher interest rates increase the cost of essential consumables, glassware, and reagents, which can delay purchasing and tighten cash flows.

Geopolitical tensions affect the availability of specialty chemicals and imported instruments, creating supply chain disruptions and longer lead times. Current US tariffs on imported lab equipment and raw materials add to procurement costs and put pressure on supplier margins. Smaller labs and startups face higher operational burdens, limiting near-term expansion plans.

On the positive side, manufacturers invest in domestic production and local distribution networks, which improves supply reliability. Increased funding for biotechnology, pharmaceutical, and clinical research sustains consistent demand for laboratory supplies. With strategic sourcing, inventory management, and innovation in sustainable lab products, the market continues to show stable growth potential.

Latest Trends

Adoption of sustainable and eco-friendly laboratory consumables is a recent trend in the market.

In 2024, laboratories increasingly adopted recyclable and biodegradable consumables to reduce plastic waste generated from routine testing and research activities. These products incorporate plant-based materials or designed for recycling without compromising performance. Manufacturers have prioritized certifications for environmental impact in product development.

Clinical and research laboratories benefit from reduced disposal costs and alignment with institutional sustainability goals. The trend responds to growing regulatory pressure on laboratory waste management. Major suppliers introduced lines of recyclable pipette tips and centrifuge tubes in 2024. This development addresses concerns about single-use plastics in scientific workflows.

The trend emphasizes compatibility with existing protocols to ensure seamless adoption. Industry collaborations refine material formulations for durability and cost-effectiveness. These innovations aim to balance laboratory efficiency with environmental responsibility in scientific practice.

Regional Analysis

North America is leading the Laboratory Supplies Market

North America recorded solid expansion in the laboratory supplies market in 2024, underpinned by strong demand across clinical diagnostics, research and industrial laboratories. The region contributed 39.7 % of global market activity, reflecting its substantial role in scientific testing and innovation.

Expansion of healthcare and biotech research infrastructure in the United States and Canada increased demand for consumables, glassware, safety equipment and analytical tools that support clinical workflows and high‑throughput research.

Institutions and private labs invested in automation and digital laboratory systems to improve efficiency, accuracy and data management, which boosted purchases of modern lab inputs. Increased federal research funding supported academic and government laboratories in acquiring advanced supplies for biotechnology, life sciences and pharmaceutical development.

Contract research organisations and CRO‑driven trials also accelerated procurement of specialised consumables and instruments. Growing biosafety and contamination control focus raised consumption of single‑use items across hospital and diagnostic labs.

Research facilities in North America conducted more than 1 billion diagnostic tests annually, a scale that directly translated into higher laboratory supply utilisation and growth in product procurement from clinical and research end users.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is poised for sustained acceleration throughout the forecast period as healthcare investment and research activities expand rapidly across the region. Governments in China, India, Japan and Southeast Asian nations increased funding and incentives for laboratory infrastructure, prompting hospitals, research institutes and biotech firms to acquire more products for quality testing, research and development applications.

Expansion of pharmaceutical manufacturing and clinical trial capacity created heightened need for reliable laboratory inputs to support quality control, formulation and regulatory compliance processes. Universities and private research centres integrated modern laboratory systems to handle growing study volumes, which elevated demand for consumables and analytical tools.

Regional collaborations with multinational suppliers enhanced technology transfer and availability of cutting‑edge consumables adapted to local research requirements. Rising expenditure on scientific research in Asia Pacific contributed to broader laboratory modernisation, strengthening end‑user capabilities. China alone operated approximately 50,000 active laboratories in 2024, a figure that highlights the depth of infrastructure driving product demand across clinical and research settings.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the laboratory supplies market grow by broadening product assortments to include high‑quality consumables, glassware, and precision instruments that support diverse research, clinical, and industrial workflows. They also strengthen customer value by integrating inventory management solutions, bulk pricing programs, and just‑in‑time delivery services that help labs control costs and reduce operational disruptions.

Firms pursue strategic alliances with academic institutions, biopharma manufacturers, and government research agencies to deepen penetration and embed their offerings into standardized procurement channels. Geographic expansion into North America, Europe, and high‑growth Asia Pacific diversifies revenue streams and captures rising investments in life sciences, diagnostics, and quality‑assurance testing infrastructure.

Thermo Fisher Scientific Inc. exemplifies a global leader with a comprehensive portfolio of laboratory consumables and equipment, extensive distribution networks, and coordinated commercial strategies that align product availability with evolving scientific and regulatory demands.

The company advances its competitive agenda through disciplined investment in product innovation, targeted acquisitions that expand its service footprint, and a customer‑centric approach that translates supply reliability into measurable operational performance.

Top Key Players

- Thermo Fisher Scientific

- Merck KGaA

- Agilent Technologies

- Sigma-Aldrich

- PerkinElmer

- Bio-Rad Laboratories

- VWR International

- Corning Incorporated

- BD Biosciences

- Hamilton Company

Recent Developments

- In March 2025, PHC Corporation of North America introduced the MCO-171AICUVD-PA CO₂ incubator from its PHCbi line, designed for laboratories handling cell cultures. The incubator focuses on preventing contamination and improving operational efficiency, featuring UV-LED disinfection, specialized chamber materials, and a high-temperature sterilization cycle for enhanced safety and reliability.

- In January 2025, Dynarex Corporation launched the LabChoice series, a new set of laboratory tools and equipment tailored for industries such as healthcare, research, education, and food processing, providing adaptable and precise solutions to meet changing laboratory needs.

Report Scope

Report Features Description Market Value (2025) US$ 51.2 Billion Forecast Revenue (2035) US$ 108.5 Billion CAGR (2026-2035) 7.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Equipment (Autoclaves & Sterilizers, Centrifuges, Incubators, Lab Air Filtration System, Laminar Flow Hood, Micro Manipulation Systems, Scopes, Sonicators & Homogenizers and Others) and Consumables (Cell Culture Consumables, Cell Imaging Consumables, Dishes, Gloves, Masks, Pipettes, Tips and Tubes)), By End-user (Academic Institutions, Pharmaceutical & Biotechnology Companies and Clinical & Diagnostic Laboratories) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Thermo Fisher Scientific, Merck KGaA, Agilent Technologies, Sigma-Aldrich, PerkinElmer, Bio-Rad Laboratories, VWR International, Corning Incorporated, BD Biosciences, Hamilton Company Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Thermo Fisher Scientific

- Merck KGaA

- Agilent Technologies

- Sigma-Aldrich

- PerkinElmer

- Bio-Rad Laboratories

- VWR International

- Corning Incorporated

- BD Biosciences

- Hamilton Company

Our Clients

- 179512

- Feb 2026