Global Insect Repellent Active Ingredients Market Size, Share, And Industry Analysis Report By Type (DEET, Picaridin, IR3535, P-Methane 3,8-DIOL (PMD), DEPA, Others), By Insect Type (Mosquitoes, Bugs, Ticks, Flies), By Concentration (Less than 10, Between 10-50, More than 50), By Application (Creams and Lotions, Pump Sprays, Gels, Wet Wipes, Aerosols), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181025

- Number of Pages: 313

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

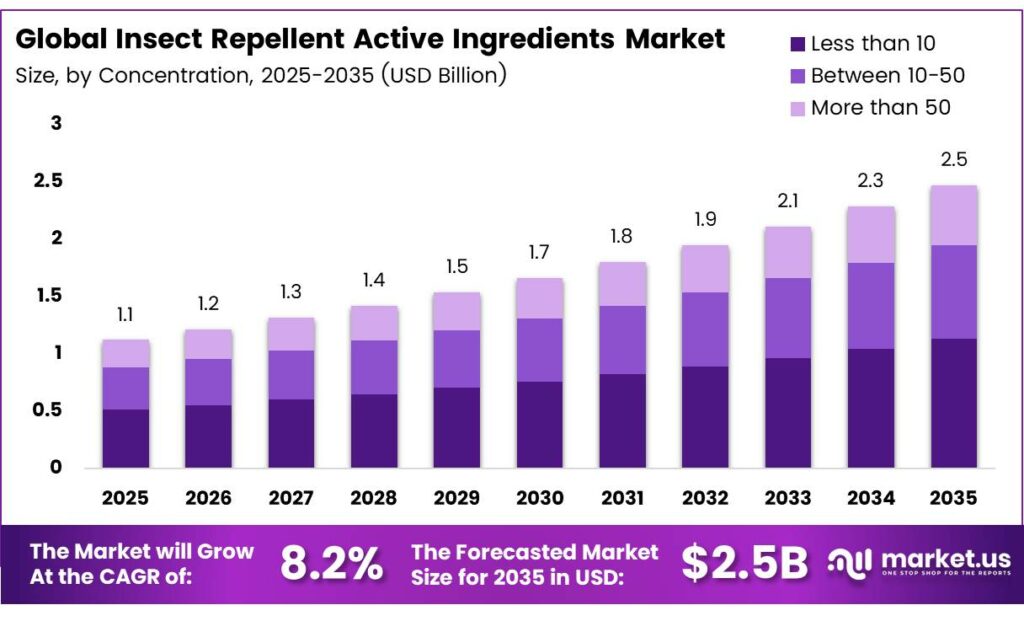

The Global Insect Repellent Active Ingredients Market size is expected to be worth around USD 2.5 billion by 2035 from USD 1.1 billion in 2025, growing at a CAGR of 8.2% during the forecast period 2026 to 2035.

The insect repellent active ingredients market covers chemical and botanical compounds used to deter insects in personal care and household products. These ingredients form the core of creams, sprays, and wearable solutions. Demand spans residential, commercial, and public health applications globally.

Active ingredients include synthetic compounds such as DEET and Picaridin, alongside natural alternatives like PMD and IR3535. Manufacturers continuously refine formulations for safety, duration, and efficacy. Regulatory approval shapes which ingredients reach consumers in different markets.

- Estonia 782.5 tonnes of pesticide active substances entered the Estonian market in 2024, a 10% increase, signaling a broader rebound in regional pesticide and repellent-adjacent demand. This trend reflects renewed commercial activity across European distribution channels.

Rising awareness of vector-borne diseases drives consumers and governments to invest heavily in repellent solutions. Malaria, dengue, and Zika remain serious public health concerns across tropical and subtropical regions. Consequently, health agencies promote repellent use as a core prevention tool.

- China remained the world’s largest pesticide exporter in 2024 at $10.1 billion, highlighting its central role in supplying insecticide and repellent active ingredient value chains. This export strength directly influences global pricing, availability, and supply security for formulation manufacturers worldwide.

Climate change expands mosquito and tick habitats into previously unaffected regions. This geographic shift creates new demand pockets in North America and Europe. Additionally, urbanization concentrates populations in areas where insect exposure risks are higher.

Key Takeaways

- The Global Insect Repellent Active Ingredients Market is valued at USD 1.1 billion in 2025 and is projected to reach USD 2.5 billion by 2035, growing at a CAGR of 8.2%.

- DEET leads with a dominant share of 44.7% in 2025.

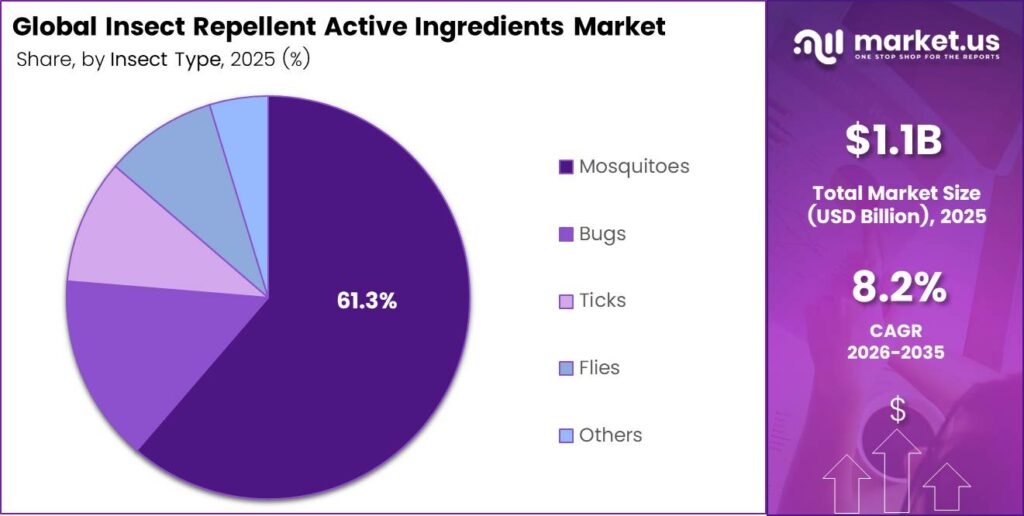

- Mosquitoes hold the leading position with 61.3% market share.

- The 10-50 segment captures 61.9% share.

- Creams and Lotions account for 31.4% share in 2025.

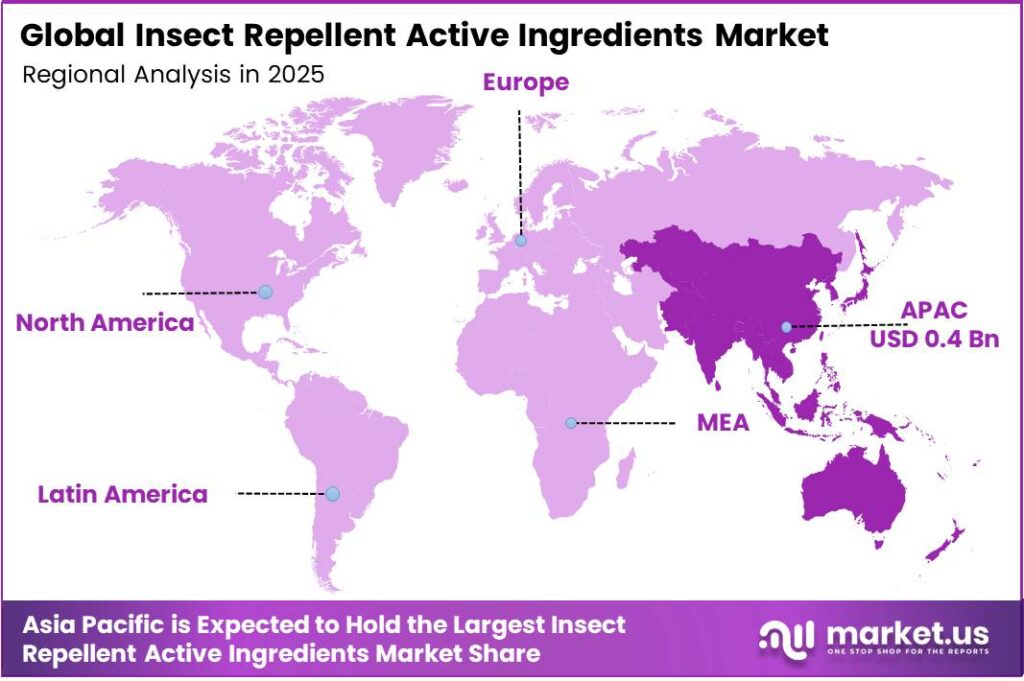

- Asia Pacific dominates the regional landscape with a 32.6% share, valued at USD 0.4 billion.

By Type Analysis

DEET dominates with 44.7% due to its proven broad-spectrum efficacy and long-standing regulatory acceptance globally.

In 2025, DEET held a dominant market position in the By Type segment of the Insect Repellent Active Ingredients Market, with a 44.7% share. DEET remains the most widely tested and trusted synthetic repellent compound worldwide. Its effectiveness against mosquitoes, ticks, and flies makes it the preferred choice for public health programs and consumer products alike.

Picaridin continues gaining acceptance as a DEET alternative, particularly among consumers seeking skin-friendly formulations. It offers comparable efficacy with a lighter skin feel and a lower odor profile. Moreover, regulatory bodies in North America and Europe increasingly recommend Picaridin for family use.

IR3535 appeals to the natural-leaning consumer base due to its amino acid-based chemical structure. It performs well against mosquitoes and is widely used in European personal care markets. Additionally, its favorable toxicological profile supports use in pediatric and sensitive-skin formulations.

P-Methane 3,8-DIOL (PMD) represents the leading plant-derived active ingredient in this segment. Derived from lemon eucalyptus oil, it offers CDC-recognized protection against disease-carrying insects. Consequently, PMD drives growth in the natural and clean-label repellent category.

DEPA and Others collectively address niche formulation needs across specialty and regional markets. DEPA finds application in combination formulations where enhanced persistence is required. Other emerging actives continue entering the pipeline as manufacturers seek differentiated, proprietary solutions.

By Insect Type Analysis

Mosquitoes dominate with 61.3% due to their direct link to life-threatening vector-borne diseases worldwide.

In 2025, Mosquitoes held a dominant market position in the By Insect Type segment of the Insect Repellent Active Ingredients Market, with a 61.3% share. Mosquitoes transmit malaria, dengue, Zika, and chikungunya, driving persistent public health demand for effective repellent actives. Government-led vector control programs significantly reinforce this segment’s leadership position globally.

Bugs represent a growing concern in residential and hospitality environments across developed markets. Consumers increasingly seek targeted solutions for bed bugs and household pests. Additionally, the hospitality sector drives demand for discreet and residue-free active formulations.

Ticks and Flies form important sub-segments, especially in North America and Europe, where Lyme disease awareness has surged. Tick repellents require higher concentration actives with longer residual activity on fabric and skin. Consequently, this segment supports premiumization trends in outdoor and sporting goods retail channels.

The Others category includes sand flies, gnats, and agricultural pest repellent applications. Niche demand from farming communities and travelers fuels steady growth in this segment. Moreover, expanding travel to tropical regions creates sustained consumer interest in broad-spectrum repellent formulations.

By Concentration Analysis

Between 10-50, concentration dominates with 61.9% as it balances efficacy and safety for mainstream consumer use.

In 2025, Between 10-50 concentration held a dominant market position in the By Concentration segment of the Insect Repellent Active Ingredients Market, with a 61.9% share. This range provides sufficient protection duration for most consumer applications without triggering safety concerns associated with high-concentration formulations. Regulatory agencies frequently recommend this band for adult use in endemic regions.

The Less than 10 concentration segment serves the pediatric and sensitive-skin categories. Parents and caregivers prefer lower-concentration products for children under twelve years. Moreover, this segment benefits from the growing clean-label and plant-derived ingredient trend in family-oriented repellent lines.

The More than 50 concentration tier addresses professional, military, and high-risk environment users. Extended field missions, tropical expeditions, and occupational health use cases drive demand for ultra-high-concentration actives. Consequently, this premium segment supports higher unit margins for manufacturers despite its smaller volume contribution.

By Application Analysis

Creams and Lotions dominate with 31.4% due to their skin-friendly application and broad consumer acceptance.

In 2025, Creams and Lotions held a dominant market position in the By Application segment of the Insect Repellent Active Ingredients Market, with a 31.4% share. These formats offer controlled dosage, even coverage, and compatibility with skincare ingredients. Consequently, they remain the preferred delivery system for both everyday and travel-focused repellent products.

Pump Sprays provide convenience and fast application, making them popular in the outdoor recreation and travel categories. Their easy-to-use format appeals to active consumers who need quick reapplication. Additionally, pump sprays generate lower inhalation exposure compared to aerosol formats, supporting regulatory preference.

Gels and Wet Wipes address on-the-go consumer needs with portable, mess-free formats. Wet wipes gain particular traction in travel retail and family travel scenarios. Moreover, gel formats allow targeted application on specific body areas, supporting premium positioning in sports and outdoor segments.

Aerosols and Others round out the application landscape, with aerosols facing headwinds from eco-packaging trends. However, aerosols maintain strong positions in household pest control and institutional markets. Other emerging formats include wearable patches and impregnated clothing, which represent the next generation of repellent delivery systems.

Emerging Trends

Clean Label Movement and Eco-Friendly Formats Reshape the Insect Repellent Ingredients Landscape

The clean label movement actively reshapes consumer expectations for repellent formulations. Shoppers increasingly demand transparent ingredient lists with recognizable, naturally-derived compounds. Australia reported A$164,653,814 of household insecticide sales in FY2023-24 across 628 registered products, confirming strong consumer engagement with regulated, label-transparent repellent categories.

Brands shift toward non-aerosol and eco-friendly packaging formats to meet sustainability commitments. Pump sprays, biodegradable wipes, and refillable containers gain shelf space across major retail channels. Moreover, this packaging transition aligns with emerging EU and North American environmental regulations targeting propellant-based delivery systems.

Premium and specialty repellents for travel and outdoor recreation drive above-average growth in developed markets. Additionally, pediatric-safe and family-oriented repellent solutions expand the addressable consumer base for manufacturers. These product categories support higher price points, improved margins, and stronger brand loyalty across retail and e-commerce channels.

Drivers

Rising Vector-Borne Disease Burden and Natural Ingredient Demand Drive Insect Repellent Active Ingredient Growth

Vector-borne diseases, including malaria, dengue, and Zika, continue to threaten millions of lives annually. Governments and global health organizations increase funding for prevention programs that rely on repellent active ingredients. The United States exported $4.7 billion of pesticides in 2024, with Canada absorbing $1.43 billion, demonstrating the scale of active ingredient trade flows that underpin this global health response.

Consumer demand for plant-based and naturally-derived repellent formulations accelerates across all major markets. Ingredient brands invest in botanical actives such as PMD and IR3535 to address this shift. Consequently, formulators reformulate existing product lines and launch new SKUs targeting health-conscious and eco-aware consumer segments.

Rapid urbanization and climate change expand the geographic range of mosquitoes and ticks. New transmission zones emerge in temperate regions previously considered low-risk. Therefore, demand for repellent active ingredients rises not only in endemic tropical markets but also in North America and Northern Europe.

Restraints

Regulatory Complexity and Insect Resistance Mechanisms Constrain Market Expansion

Stringent regulatory hurdles significantly delay the commercialization of new active ingredients. Registration processes through agencies such as the EPA, ECHA, and national bodies require extensive toxicological and environmental data. Consequently, innovation cycles lengthen, and competitive barriers to entry remain high across regulated markets.

- Prolonged approval timelines increase research and development costs for manufacturers seeking to introduce novel actives. Small and mid-sized ingredient producers face disproportionate cost burdens compared to large multinational chemical companies. Ireland recorded 2,139 tonnes of pesticide active substances sold in 2024, a 6% year-over-year decline, reflecting how tightening regulatory environments suppress commercial activity even in mature European markets.

Emerging resistance mechanisms in target insect populations to conventional actives pose a long-term challenge to market efficacy. Insect populations exposed to DEET and pyrethroids over multiple generations develop behavioral and physiological resistance. Therefore, manufacturers must continuously invest in new molecule development and combination formulation strategies to maintain product performance.

Growth Factors

Emerging Market Expansion and Wearable Repellent Technologies Accelerate Market Opportunities

Developing regions across Africa, South Asia, and Latin America present significant untapped market potential for repellent active ingredients. Expanding distribution networks and rising disposable incomes improve product accessibility in rural and peri-urban areas. These partnerships reduce time-to-market for novel actives while sharing regulatory and research costs.

- Strategic collaborations between chemical companies and biotechnology firms drive the development of proprietary synthetic molecules that mimic natural compounds. India imported pesticides primarily from China in 2024, with Chinese shipments valued at $491 million, underscoring how emerging market import dependency creates long-term commercial opportunities for established ingredient suppliers.

Integration of repellent technologies into smart wearables and connected devices opens an entirely new product category. Brands collaborate with technology companies to embed active ingredients into patches, bracelets, and fabric treatments. Additionally, the development of combination products offering both sun protection and insect repellency expands per-unit revenue potential and broadens the addressable consumer market.

Regional Analysis

Asia Pacific Dominates the Insect Repellent Active Ingredients Market with a Market Share of 32.6%, Valued at USD 0.4 Billion

Asia Pacific leads the global insect repellent active ingredients market, holding a 32.6% share valued at USD 0.4 billion in 2025. The region’s dominance reflects its high disease burden from mosquito-transmitted illnesses across South and Southeast Asia. Additionally, major ingredient manufacturing hubs in China and India supply both domestic markets and global export channels efficiently.

North America represents a mature and innovation-driven market for repellent active ingredients. Consumer preference for premium and natural formulations fuels ongoing product development in the United States and Canada. Moreover, heightened awareness of Lyme disease and West Nile Virus sustains demand for high-efficacy tick and mosquito repellent actives across outdoor recreation segments.

Europe maintains a strong regulatory framework that shapes ingredient selection across personal care and household product categories. The ECHA approval process favors well-characterized actives such as IR3535 and Picaridin over older synthetic compounds. Consequently, European manufacturers invest in reformulation to comply with evolving biocide regulations while meeting consumer demand for cleaner ingredient profiles.

Latin America sustains a steady demand for repellent active ingredients due to persistent mosquito-borne disease transmission across Brazil, Colombia, and Mexico. The Zika outbreak legacy increased long-term consumer awareness and government investment in repellent distribution programs. Additionally, rising middle-class populations in urban centers drive growth in premium personal care repellent product categories.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Sumitomo Chemical Co., Ltd operates a broad Agro and Life Solutions portfolio that includes household insecticides and pyrethroid agents used in repellent devices. The company’s FY2024 Agro and Life Solutions sector recorded sales and core operating income, confirming its scale in the insect-control active ingredient supply chain. Sumitomo’s global distribution network supports formulation partners across Asia, Europe, and the Americas.

BASF SE brings deep synthetic chemistry expertise to the insect repellent active ingredients space, supplying raw materials to formulators across multiple application categories. The company’s crop science and consumer care divisions both contribute to its repellent-adjacent ingredient portfolio. BASF’s investment in sustainable chemistry aligns with growing industry demand for biodegradable and low-toxicity active molecule innovation.

Spectrum Brands, Inc. competes across the consumer household segment with established repellent brands backed by broad retail distribution in North America and international markets. The company leverages strong category management capabilities to drive shelf presence across mass retail, e-commerce, and outdoor specialty channels. Spectrum Brands continuously invests in product reformulation to meet evolving regulatory and consumer preference standards.

Reckitt Benckiser Group PLC holds a significant position in the insect-control market through its Mortein brand, which operates within the Essential Home portfolio. Reckitt generated group, with Essential Home contributing, covering Mortein’s presence across North America, Europe, and Latin America. Reckitt’s scale enables sustained investment in active ingredient sourcing and product innovation globally.

Top Key Players in the Market

- Sumitomo Chemical Co., Ltd

- BASF SE

- Spectrum Brands, Inc.

- Reckitt Benckiser Group PLC

- Henkel AG & Co.

- S C Johnson & Sons Inc.

- Dabur

- Godrej Consumer Products Limited

- Enesis Group

- Bugg Products LLC

Recent Developments

- In 2025, Sumitomo Chemical UK is actively supporting its customers through the EU Biocidal Product Regulation (BPR) approval process by offering a Product Dossier License Scheme (PDLS). This scheme provides access to formulated product dossiers featuring their active substances.

- In 2025, BASF SE will launch a new application for pesticidal mixtures combining an isochinoline compound with existing actives like fipronil and various pyrethroids. A granted patent for pesticidal mixtures involving a pyrazole compound. New patent applications for substituted benzothiazine pyridine compounds designed to combat phytopathogenic fungi.

Report Scope

Report Features Description Market Value (2025) USD 1.1 Billion Forecast Revenue (2035) USD 2.5 Billion CAGR (2026-2035) 8.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (DEET, Picaridin, IR3535, P-Methane 3,8-DIOL (PMD), DEPA, Others), By Insect Type (Mosquitoes, Bugs, Ticks, Flies, Others), By Concentration (Less than 10, Between 10-50, More than 50), By Application (Creams and Lotions, Pump Sprays, Gels, Wet Wipes, Aerosols, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Sumitomo Chemical Co. Ltd, BASF SE, Spectrum Brands Inc., Reckitt Benckiser Group PLC, Henkel AG & Co., S C Johnson & Sons Inc., Dabur, Godrej Consumer Products Limited, Enesis Group, Bugg Products LLC Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Insect Repellent Active Ingredients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Insect Repellent Active Ingredients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Sumitomo Chemical Co., Ltd

- BASF SE

- Spectrum Brands, Inc.

- Reckitt Benckiser Group PLC

- Henkel AG & Co.

- S C Johnson & Sons Inc.

- Dabur

- Godrej Consumer Products Limited

- Enesis Group

- Bugg Products LLC

Our Clients

- 181025

- March 2026