Global Industrial Heaters Market By Product Type (Pipe Heaters, Immersion Heaters, Duct Heaters, Circulation Heaters, Cartridge Heaters), By Technology (Electric-based, Fuel-based, Hybrid-based, Steam-based), By End-Use Industry (Pharmaceuticals, Oil & Gas, Food & Beverages, Automotive, Other End-Use Industries), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

- Published date: October 2024

- Report ID: 27566

- Number of Pages: 271

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- Type Analysis

- Fuel Source Analysis

- Temperature Range Analysis

- End-Use Analysis

- Key Market Segments

- Market Dynamics

- Restraints

- Opportunity

- Trends

- Geopolitical Impact Analysis

- Regional Analysis

- Key Regions and Countries Covered in this Report

- Market Share & Key Players Analysis

- Key Developments

- Report Scope

Report Overview

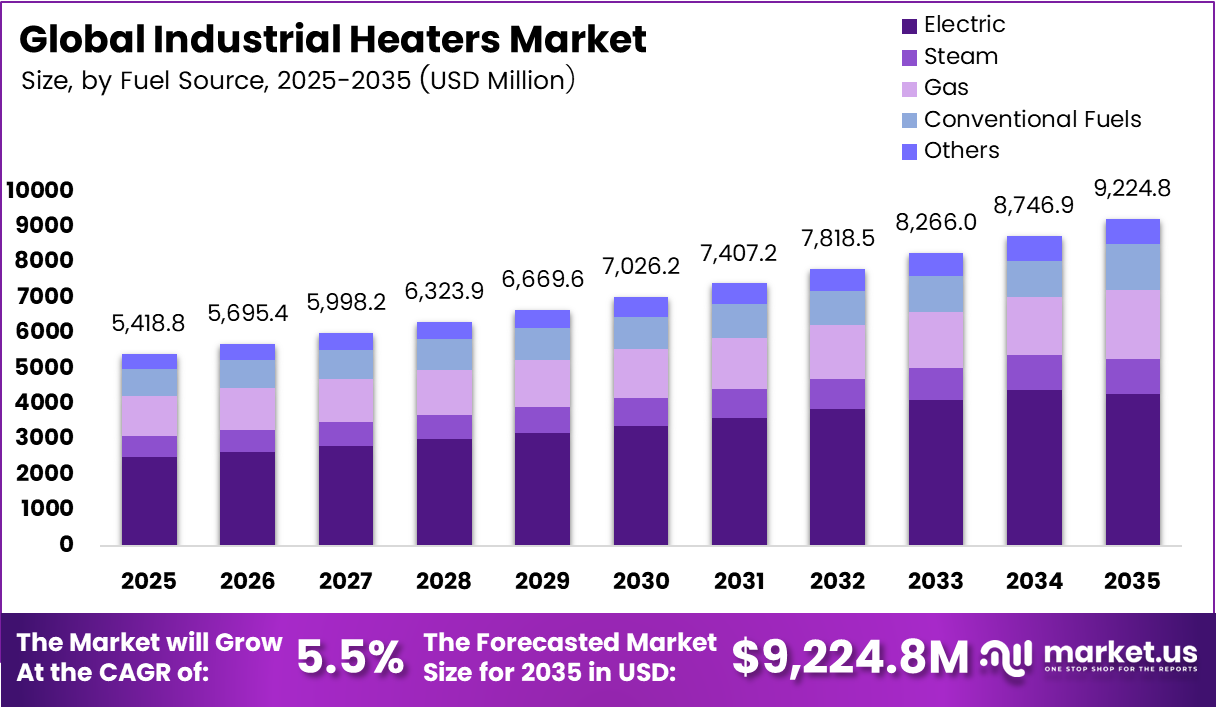

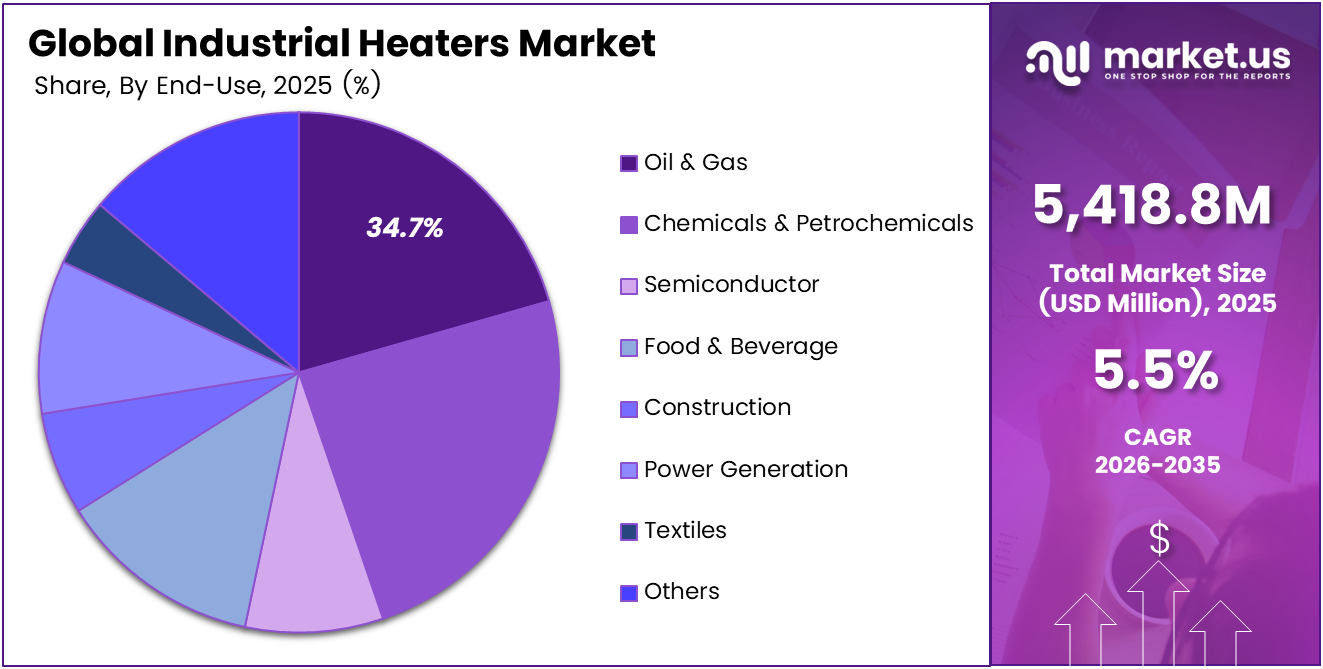

In 2025, the Global Industrial Heaters Market was valued at US$ 5,418.8 million, and between 2026 and 2035, this market is estimated to register a CAGR of 5.5%.

The global industrial heaters market is expanding steadily, driven by the growth of energy-intensive industries and increasing demand for efficient process heating solutions across manufacturing sectors. Industries such as chemicals, oil and gas, steel, cement, food processing, and petrochemicals depend heavily on high-temperature heating systems for processes including drying, distillation, curing, and heat treatment.

Rising industrialization, infrastructure development, and manufacturing expansion—particularly in emerging economies—are further strengthening demand for reliable heating equipment. However, the market faces challenges such as high capital investment requirements and complexities associated with retrofitting existing facilities with advanced heating systems.

Despite these barriers, opportunities are emerging from the expansion of process industries and the growing need for customized heating solutions designed for specific operational requirements. In addition, technological advancements are driving the adoption of smart and connected heaters that enable real-time monitoring, predictive maintenance, and improved energy efficiency. Geopolitical trade policies are also influencing supply chains and cost structures. Regionally, Asia Pacific remains the dominant market due to its large manufacturing base and increasing industrial energy demand.

Key Takeaways

- The global industrial heaters market was valued at US$ 5,418.8 million in 2025.

- The global industrial heaters market is projected to grow at a CAGR of 5.5% and is estimated to reach US$ 9,224.8 million by 2035.

- Between types, the pipe heater accounted for the largest market share of 23.5%.

- Among fuel sources, electric heaters accounted for the majority of the market share at 46.4%.

- Among the temperature range, high-temperature (>400°C) domain dominated the market with a market share of 47.0%.

- Based on end-uses, chemicals & petrochemicals dominated the global industrial heaters market with a 24.2% market share.

- Asia-Pacific is estimated as the largest market for industrial heaters with a share of 49.9% of the market share.

- North America was estimated second largest market with a CAGR of 5.1%.

Type Analysis

Pipe Heaters dominate with 23.5% due to widespread use in pipeline temperature maintenance across process industries.

Based on type, the market is categorized into pipe heater, process air heater, immersion heater, tubular heater, circulation heater, infrared heater, radiant heater, band heater, strip heater, cartridge heater, drum heater, and others. As of 2025, pipe heaters dominate the industrial heaters market, accounting for 23.5% because they are widely used to maintain the temperature of fluids flowing through pipelines in industries such as oil and gas, chemicals, and manufacturing. Maintaining heat in pipelines is essential to ensure smooth fluid transport and process stability.

Government studies indicate that when fluid temperatures drop, viscosity increases, and certain substances, such as crude oil components, can begin to solidify, making transportation through pipelines difficult or inefficient. Maintaining proper pipeline temperature, therefore, improves flow efficiency, reduces operational disruptions, and ensures continuous industrial processing. Because pipe heaters provide direct and reliable heating along pipelines and are easily integrated into industrial systems, they are widely adopted across process industries, contributing to their dominant share in the industrial heaters market.

Fuel Source Analysis

Electric Heaters dominate with 46.4% due to high efficiency, precise temperature control, and lower environmental impact.

Based on the fuel source, the market is segmented into electric, steam, gas, conventional fuels, and others. As of 2025, electric industrial heaters hold a dominant 46.4% market share, due to their high efficiency, precise temperature control, and lower environmental impact compared with fuel-based heating systems. Industrial process heating is one of the largest energy demands in manufacturing, used to heat or maintain temperatures of materials during production processes such as metals, chemicals, glass, and food manufacturing.

Electric heating technologies are increasingly preferred because they deliver heat directly to the target material, reducing energy losses and improving process efficiency. In addition, electric systems eliminate on-site fuel combustion, which helps industries reduce emissions, simplify maintenance, and improve operational safety. These systems also provide faster response times and precise temperature regulation, which is critical for modern automated manufacturing processes.

Temperature Range Analysis

High-Temperature (>400°C) dominates with 47.0% due to critical thermal requirements in core industrial processes.

Based on the temperature range, the market is further divided into high-temperature (>400°C), medium-temperature (150 – 400°C), & low-temperature (<150°C). Among them, high-temperature (>400°C) heaters dominated the global industrial heaters market with a 47.0% of market share in 2025 because several core industrial processes require extremely high thermal energy for material transformation and chemical reactions.

According to the U.S. Department of Energy, industrial process heat is widely used to alter or manufacture materials in sectors such as steelmaking, petroleum refining, cement production, and chemical processing. These operations often require temperatures ranging from several hundred degrees to well above 1,000°C to enable processes such as metal melting, crude oil separation, and high-temperature chemical reactions.

Because industries such as metals, petrochemicals, glass, and cement production operate at these elevated temperature ranges, they rely heavily on specialized high-temperature heating systems capable of maintaining stable thermal conditions. These processes represent a major share of industrial energy demand and require durable heaters designed for continuous high-heat operation.

End-Use Analysis

Chemicals & Petrochemicals dominate with 24.2% due to consistent demand for process heating in refining and chemical manufacturing.

Based on the end-use, the market is further divided into oil & gas, chemicals & petrochemicals, semiconductor, food & beverage, construction, power generation, textiles, & others. Among end-uses, chemicals & petrochemicals dominated the global industrial heaters market with a 24.2% market share. Industrial heaters play a critical role in applications such as fluid heating, thermal cracking, distillation, and feed preheating, which are essential for producing petrochemicals and chemical intermediates.

Process heating equipment is commonly used in refining operations and chemical manufacturing, where heat is required to enable chemical reactions and prepare process streams for further processing. Because these industries operate large-scale continuous plants that depend heavily on stable thermal energy, demand for reliable industrial heaters remains consistently high, supporting the strong market share of the chemicals and petrochemicals sector.

Key Market Segments

By Type

- Pipe Heater

- Process Air Heater

- Immersion Heater

- Tubular Heater

- Circulation Heater

- Infrared Heater

- Radiant Heater

- Band Heater

- Strip Heater

- Cartridge Heater

- Drum Heater

By Fuel Source

- Electric

- Nickel-Chromium (NiCr)

- Iron-Chromium-Aluminium (FeCrAl)

- Steam

- Gas

- Propane

- Liquefied Natural Gas

- Others

- Conventional Fuels

- Liquid Fuels

- Coal

- Wood

- Others

- Others

By Temperature Range

- High-temperature (>400°C)

- Medium-temperature (150 – 400°C)

- Low-temperature (<150°C)

By End-use

- Oil & Gas

- Chemicals & Petrochemicals

- Semiconductor

- Food & Beverage

- Construction

- Power Generation

- Textiles

- Others

Market Dynamics

Drivers

Expansion of Energy Intensive Industries Is Driving The Market Growth.

Expansion of energy-intensive industries is a key driving factor for the Global Industrial Heaters Market, as these sectors rely heavily on continuous and high-temperature process heating to sustain production volumes and product quality.

Energy-intensive industries such as chemicals, oil and gas, steel, cement, glass, pulp and paper, and petrochemicals consume a disproportionate share of global industrial energy due to their dependence on thermal processes, including drying, smelting, distillation, cracking, and curing. According to data published by international energy agencies, the industrial sector accounts for nearly 37% of global final energy consumption, with energy-intensive manufacturing segments representing more than half of this demand.

Within manufacturing, process heating alone contributes roughly 30–35% of total industrial energy use, highlighting the central role of thermal equipment. Growth in construction, infrastructure development, urbanization, and downstream manufacturing has accelerated capacity expansion in these industries, particularly in emerging economies. For instance, cement manufacturing, which requires kiln temperatures of around 1,450°C, continues to expand in regions such as Asia-Pacific, where annual cement production growth rates exceed 4–5% in several developing markets.

- In the U.S., energy-intensive manufacturing subsectors such as chemicals, petroleum products, and primary metals consumed about 87% of total manufacturing energy in 2018, with chemicals alone accounting for about 70% of non-fuel energy use.

- In India, the cement industry—classically energy intensive—is projected to grow at roughly 5.1% per year through 2030, driven by residential and infrastructure demand, which will further elevate energy demand levels.

Restraints

High Capital Costs and Retrofitting Challenges May Hamper The Growth Of The Market to a Certain Extent

Despite strong demand fundamentals, high initial capital costs and retrofitting complexities remain a major restraint on the global industrial heaters market. Modern industrial heaters often incorporate advanced control systems, higher-quality materials, integrated safety features, and automation compatibility, all of which contribute to higher upfront equipment costs compared to legacy heating solutions. For instance, installing a mid-sized superheated steam system or a large electric process heater can require high capital expenditure, making such investments prohibitive for facilities operating on tighter budgets or with limited access to financing. This high cost barrier often delays the replacement of older, less efficient heaters and slows the adoption of modern energy-efficient solutions.

- Around 28% of industrial players cite cost as the top barrier to upgrading and modernizing equipment, including thermal systems and processes. This highlights how high upfront investment can slow the adoption of newer heater technologies.

Retrofitting existing plants with new heating systems presents additional challenges that extend beyond simple equipment purchase price. Industrial retrofits frequently involve complex engineering integration, structural modifications, temporary shutdowns, and coordination with existing control systems and safety protocols. These complexities can extend project timelines, increase installation labor costs, and raise the risk of operational disruption, deterring decision makers from pursuing upgrades.

Opportunity

Expansion of Process Industries and Customized Heating Solutions

Expansion of process industries and customized heating solutions represents a strong opportunity for the global industrial heaters market because a growing share of industrial capacity additions is occurring in sectors that depend on tightly specified, application-specific thermal performance. Process industries such as chemicals, oil and gas, food processing, and advanced manufacturing are scaling output while also tightening tolerances for temperature stability, safety, and energy efficiency. This expansion matters because industrial activity remains a major energy consumer globally, with the industrial sector accounting for 37% of global energy use in 2022, and industrial processes responsible for 53% of final energy consumed for heat.

As heat-intensive production expands, end users increasingly prefer heaters engineered around their process fluid, temperature ramp profile, footprint constraints, corrosion exposure, and control architecture, rather than standard off-the-shelf equipment. Customized heating solutions are particularly relevant in high-growth, precision-driven process environments.

Semiconductor manufacturing is a clear instance where new capacity creation increases demand for highly controlled, contamination-sensitive heating, drying, and thermal conditioning systems. SEMI reported that 18 new semiconductor fab construction projects are expected to start in 2025, with several scheduled to begin operations in 2026 to 2027, supporting sustained demand for specialized thermal systems integrated with fab automation and safety protocols.

Trends

Shift Toward Smart and Connected Heaters

Shift toward smart and connected heaters is a key trend, driven by the broader adoption of digitalization, automation, and Industry 4.0 practices across industrial facilities. Traditional industrial heaters primarily focused on heat generation, but modern systems increasingly incorporate sensors, connectivity, and intelligent control platforms that enable real-time monitoring and dynamic performance optimization. Smart heaters can continuously track parameters such as temperature, pressure, energy consumption, and operating cycles, allowing operators to maintain precise process conditions and reduce variability that can affect product quality. This level of control is particularly valuable in industries such as chemicals, semiconductors, food processing, and pharmaceuticals, where consistent thermal performance is critical.

- Over 86% of manufacturers believe smart factory initiatives will be the primary driver of competitiveness by 2027, with connected process equipment and real-time monitoring identified as core enablers.

- Predictive maintenance enabled by connected equipment can reduce unplanned downtime by 30–50% and lower maintenance costs by 10–40%. Heating systems are commonly included in these monitoring programs due to their critical role in continuous processes.

Connected heaters also support predictive and preventive maintenance strategies. By collecting and analyzing operational data, these systems can identify early signs of component wear, scaling, or performance degradation before failures occur. This reduces unplanned downtime, extends equipment life, and lowers maintenance costs, which are major priorities for energy-intensive and continuous process industries. Integration with plant-wide automation systems and manufacturing execution systems enables centralized control, remote diagnostics, and faster response to process deviations. As a result, heating systems evolve from isolated assets into integral components of digital production environments.

Geopolitical Impact Analysis

Geopolitical Challenges in the Industrial Heaters Market.

Geopolitical developments, particularly U.S. tariff policies, are influencing the industrial heaters market by raising production costs and reshaping global supply chains. Industrial heaters rely heavily on metals such as steel and aluminum for structural components, heating elements, tanks, and enclosures. When tariffs increase on these materials and related imported components, manufacturers face higher input costs that directly affect production economics. As a result, companies must either absorb the additional costs, which reduces profit margins, or transfer them to customers through higher equipment prices. This situation has created cost pressures across the value chain, affecting manufacturers, distributors, contractors, and end-user industries.

Tariffs on electronics and mechanical components have also complicated sourcing strategies, particularly for specialized parts such as sensors, control systems, and motors that are commonly imported. Companies are increasingly required to shift suppliers, diversify procurement sources, or increase domestic production to reduce dependence on tariff-affected imports. However, transitioning to alternative suppliers can involve higher costs, qualification delays, and supply uncertainty. For end-user industries including manufacturing, pharmaceuticals, food processing, and energy, these geopolitical measures translate into higher capital investment for heating equipment, longer lead times for replacement units, and more expensive maintenance. Consequently, geopolitical trade policies are accelerating a broader industry shift toward supply-chain resilience, regional sourcing, and strategic inventory management rather than purely cost-driven procurement.

Regional Analysis

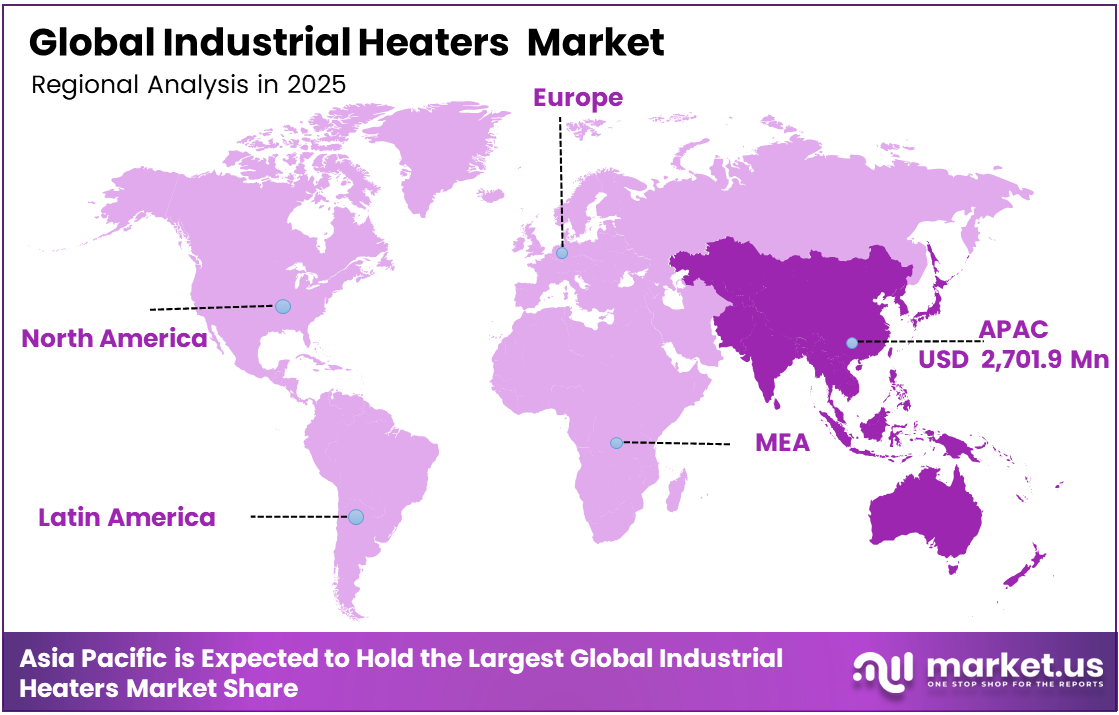

Asia Pacific Held the Largest Share of the Global Industrial Heaters Market

In 2025, the Asia Pacific region dominated the global industrial heaters market with a 49.9% share primarily due to its strong industrial base, expanding manufacturing sector, and large-scale infrastructure development. Countries such as China, India, Japan, and South Korea serve as major global manufacturing hubs, supporting industries such as chemicals, automotive, electronics, metals, food processing, and machinery.

These industries rely heavily on industrial heaters for applications including fluid heating, drying, curing, heat treatment, and temperature control during production processes. China continues to lead the region due to its vast network of manufacturing facilities, refineries, and chemical plants that require reliable heating systems for continuous operations.

Meanwhile, India is experiencing rapid growth in demand for industrial heaters as government initiatives promoting domestic manufacturing and infrastructure expansion encourage the development of pharmaceutical, automotive, and food processing industries. In addition, Southeast Asian economies such as Vietnam, Indonesia, and Thailand are attracting multinational manufacturers seeking to diversify supply chains, leading to the expansion of industrial parks and factories that require advanced heating technologies.

The region is also witnessing increasing adoption of energy-efficient electric and induction heating systems as industries focus on improving productivity, automation, and environmental performance. With Asia Pacific accounting for a significant share of global manufacturing output and industrial energy consumption, demand for industrial heating equipment continues to expand, reinforcing the region’s leading position in the global industrial heaters market.

Key Regions and Countries Covered in this Report

North America

- The US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Product Innovation and Robust Research And Development are Key Strategies Adopted By Major Players to Remain Competitive And Address Evolving Industrial Requirements.

Manufacturers are investing in advanced heating technologies that improve energy efficiency, temperature accuracy, and operational safety across industrial processes. Continuous R&D efforts focus on developing electric, modular, and digitally controlled heaters that enable better process control, lower emissions, and reduced energy consumption. Companies are also integrating smart monitoring systems, automation features, and durable materials to enhance product reliability and lifespan. Through consistent innovation and technological advancement, market leaders strengthen their product portfolios and meet the growing demand for efficient industrial heating solutions.

Key Players

- Yancheng DragonPower Electric Co., Ltd

- Watlow Electric Manufacturing Company

- Elmatic (Cardiff) Ltd

- Chromalox, Inc.

- DwyerOmega

- Komax Systems

- Tempsens Instrument Pvt. Ltd.

- Thermal Flow Technologies

- Winterwarm Heating Solutions BV

- Powrmatic Ltd.

- Tempco Electric Heater Corporation

- Durex Industries

- Indeeco

- Dalton Electric

- Backer Hotwatt

- Pirobloc, S.A.

- Rama Corporation

- TUTCO Conductive

- Honeywell International

- Thermal Corporation

- Other Key Players

Key Developments

- May 2025: Watlow Electric Manufacturing Company expanded its operations in India with the opening of a new facility in Bangalore on April 3, 2025. Located at Rathi Legacy–Rohan Tech Park, the office marked a major investment in India’s growing technology and manufacturing ecosystem and strengthened the company’s South Asia strategy alongside its Chennai presence established in 2021. The Bangalore facility supported product development, customer support, market research, and R&D activities, particularly for the semiconductor sector. It also focused on energy-efficient and sustainable thermal solutions while enabling faster local engineering, prototyping, and customer service.

- January 2025: Indeeco expanded its Ultra-Safe Explosion-Proof Unit Heater (233 Series) portfolio with the launch of a higher-capacity 35 kW model. The new variant was designed to address larger and more demanding industrial applications operating in hazardous environments. Certified for Class I and II, Division 1 and 2 locations across multiple gas and dust groups, the heater offers enhanced thermal output while maintaining strict safety and durability standards. This expansion strengthened Indeeco’s position in the explosion-proof heating segment and reflected the company’s ongoing focus on advancing safe, high-performance heating solutions for extreme and regulated industrial environments.

- September 2024: TUTCO strengthened its global position in electric heating solutions through the acquisition of WATTCO, a Montreal-based electric heating manufacturer. This strategic move expanded TUTCO’s product portfolio and enhanced its technological capabilities, reinforcing its commitment to innovation and customer service. The acquisition also extended TUTCO’s manufacturing footprint across North America, complementing its existing global operations. By integrating WATTCO’s expertise and shared customer-focused culture, TUTCO further solidified its leadership in delivering high-quality, custom electric heating solutions for industrial, commercial, and mission-critical applications worldwide.

Report Scope

Report Features Description Market Value (2025) US$ 5,156.6 Mn Forecast Revenue (2035) US$ 9,224.8 Mn CAGR (2026-2035) 5.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Pipe Heater, Process Air Heater, Immersion Heater, Tubular Heater, Circulation Heater, Infrared Heater, Radiant Heater, Band Heater, Strip Heater, Cartridge Heater, Drum Heater, Others), By Fuel Source (Electric, Steam, Gas, Conventional Fuels, Others), By Temperature Range (High-Temperature (>400°C), Medium-Temperature (150 – 400°C), & Low-Temperature (<150°C)) By End-use (Oil & Gas, Chemicals & Petrochemicals, Semiconductor, Food & Beverage, Construction, Power Generation, Textiles, & Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa, & Rest of MEA Competitive Landscape Yancheng DragonPower Electric Co., Ltd, Watlow Electric Manufacturing Company, Elmatic (Cardiff) Ltd, Chromalox, Inc., DwyerOmega, Komax Systems, Tempsens Instrument Pvt. Ltd., Thermal Flow Technologies, Winterwarm Heating Solutions BV, Powrmatic Ltd., Tempco Electric Heater Corporation, Durex Industries, Indeeco, Dalton Electric, Backer Hotwatt, Pirobloc, S.A., Rama Corporation, TUTCO Conductive, Honeywell International, Thermal Corporation, & Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Industrial Heaters MarketPublished date: October 2024add_shopping_cartBuy Now get_appDownload Sample

Industrial Heaters MarketPublished date: October 2024add_shopping_cartBuy Now get_appDownload Sample -

-

- Dragon Power Electric Co. Ltd.

- Watlow Electric Manufacturing Company

- Wattco

- Elmatic Ltd.

- Chromalox

- Auzhan Electric Appliances Co.Ltd

- Thermal Flow Technologies

- Winterwarm

- Powrmatic Ltd.

- Other Key Players

Our Clients

- 27566

- October 2024