IDC (Internet Data Center) Market By Services (Hosting, Colocation, CDN, Others), By Deployment (Public, Private, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By End-use (Cloud Service Providers (CSPs), Telecom, Government/Public Sector, BFSI, Media & Entertainment, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

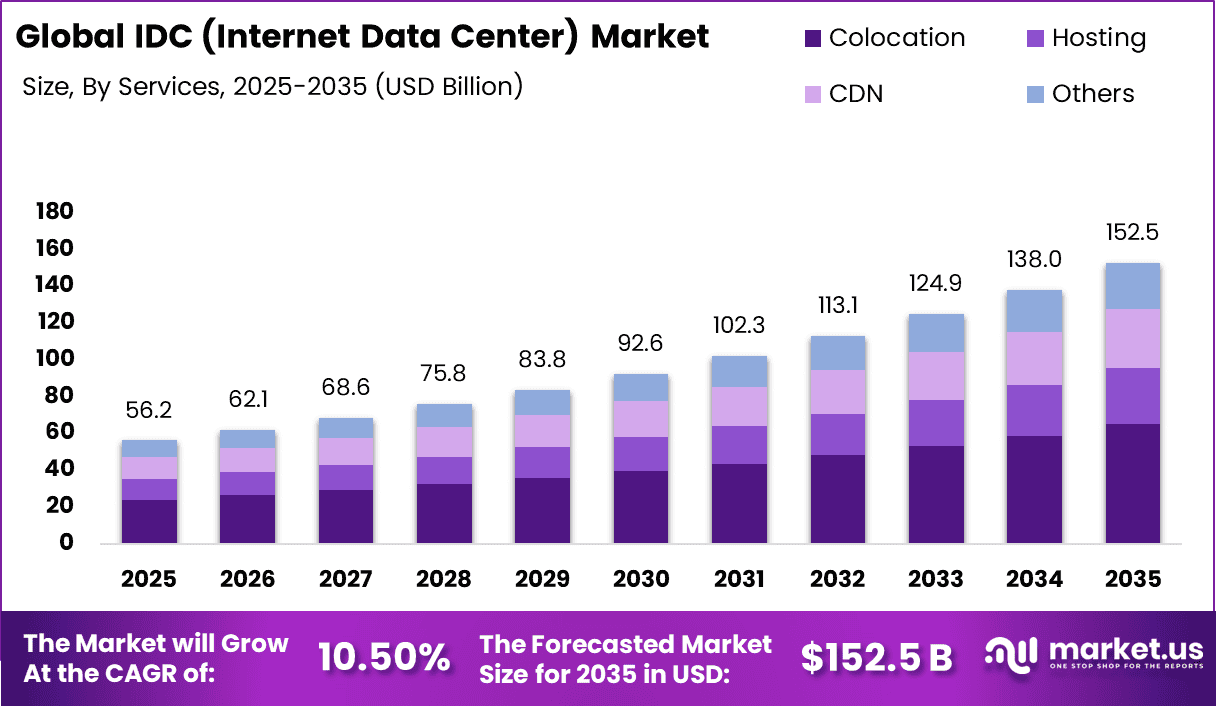

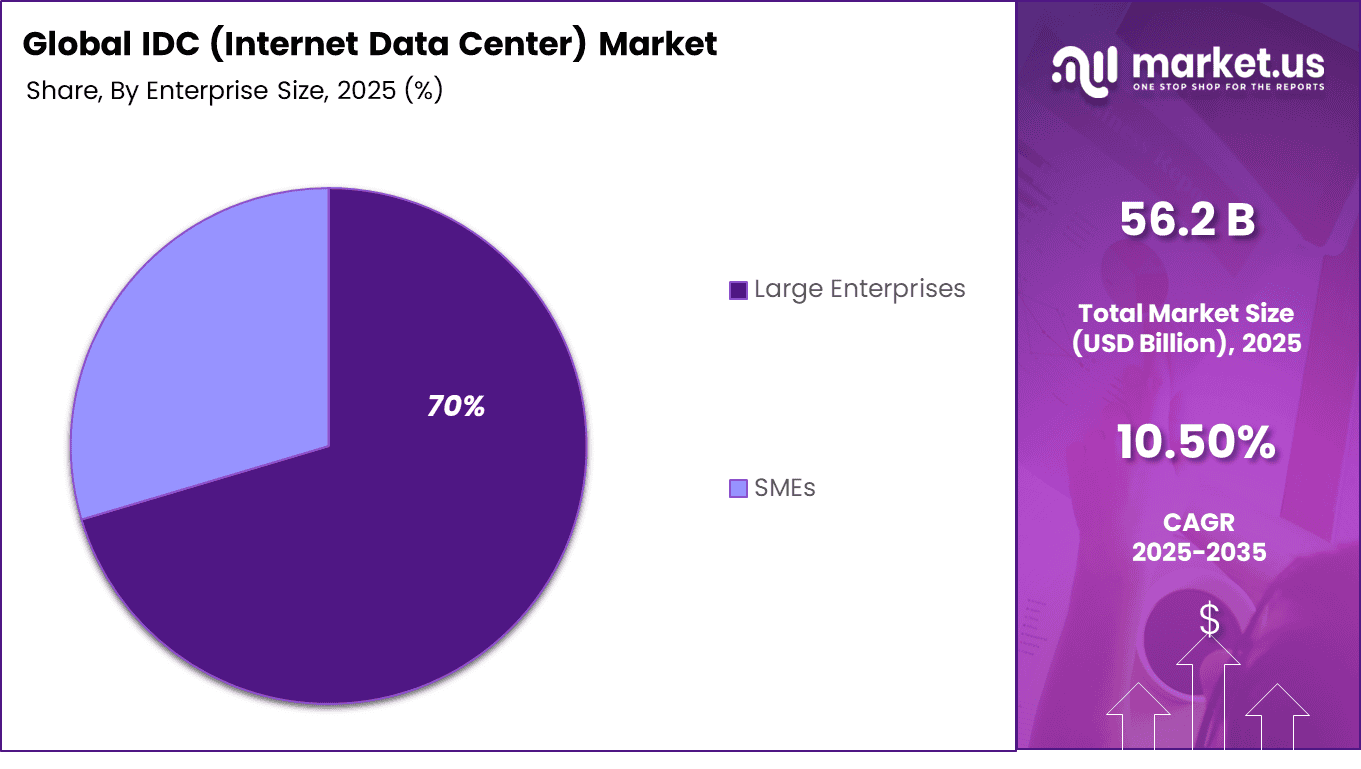

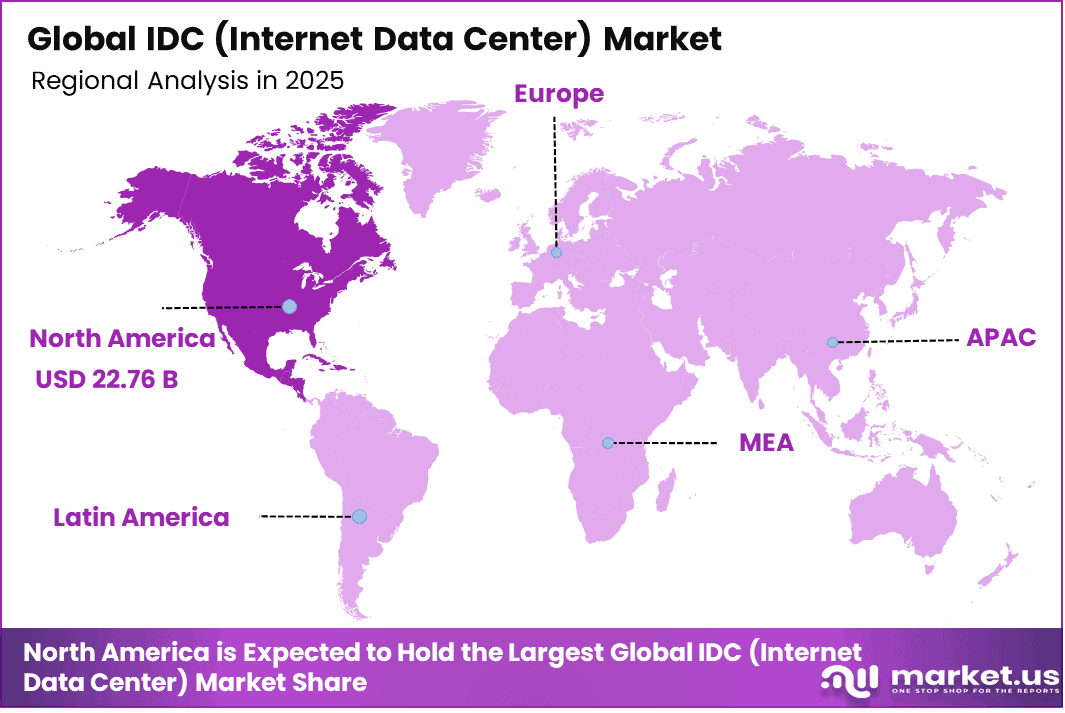

The Global IDC (Internet Data Center) Market generated USD 56.2 billion in 2025 and is predicted to register growth from USD 62.1 billion in 2026 to about USD 152.5 billion by 2035, recording a CAGR of 10.50% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 40.5% share, holding USD 22.76 Billion revenue.

Internet data centers are critical facilities that store, process, and distribute digital information for businesses, governments, and consumers. They provide the computing power, storage systems, and network connectivity needed to support websites, cloud services, enterprise applications, and digital transactions.

As organizations move more operations online, data centers have become the backbone of the digital economy. Modern facilities are increasingly designed for higher efficiency, stronger security, and continuous uptime to meet growing data requirements.

One of the main driving factors is the rapid expansion of cloud computing and digital services across industries. Businesses are generating more data and require reliable infrastructure to manage applications, analytics, and customer platforms. In addition, rising use of streaming media, ecommerce, remote work tools, and connected devices is incr

easing the need for high capacity data processing and storage. The growth of artificial intelligence workloads is also supporting demand for advanced facilities with stronger power and cooling capabilities. At the same time, organizations are prioritizing cybersecurity and business continuity, which is encouraging investment in professionally managed data center environments.

Demand for internet data center services is rising as enterprises seek scalable and secure infrastructure without building all systems internally. There is a strong preference for facilities that offer high network connectivity, flexible capacity, disaster recovery support, and efficient operations. Customers are also looking for providers that can support hybrid cloud strategies and low latency performance for critical workloads.

The demand is particularly strong among financial services, telecom, healthcare, retail, media, and technology sectors that rely on uninterrupted digital operations. As global digital activity continues to expand, the need for reliable and high performance data center capacity is expected to grow steadily.

Top Market Takeaways

Colocation services command 42.6%, providing secure rack space, power redundancy, and low-latency interconnectivity for mission-critical workloads.

Public cloud deployment holds 48.2%, enabling elastic scaling, multi-region orchestration, and hybrid connectivity to on-premises systems.

Large enterprises dominate at 70.4% by size, leveraging high-density configurations for enterprise applications, compliance requirements, and disaster recovery.

Cloud service providers capture 36.8% end-use share, powering IaaS/PaaS platforms with direct peering, edge caching, and bare-metal provisioning.

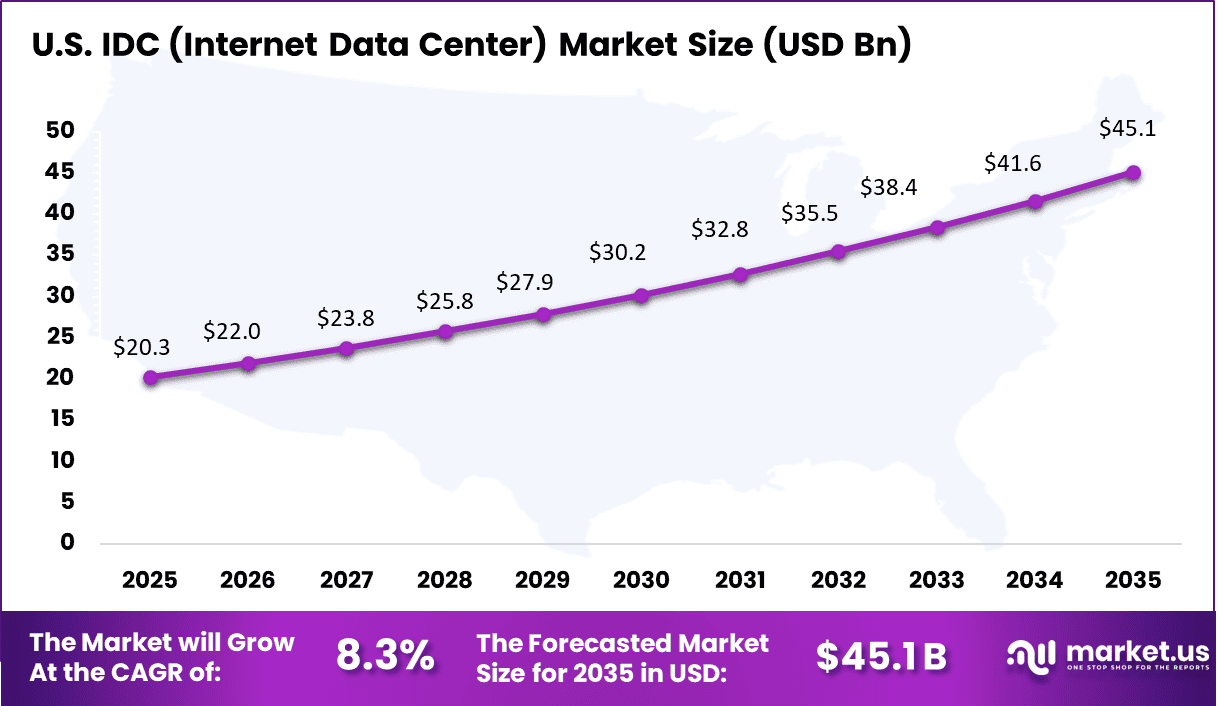

North America drives 40.5% global value, with U.S. market at USD 20.3 billion and 8.3% CAGR, fueled by Virginia/Northern California hub development and 5G edge computing rollout.

Drivers Impact Analysis

Key Driver

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

Rapid growth in cloud computing adoption

+3.8%

North America, Europe, Asia Pacific

Short to medium term

Cloud demand increases data center capacity

Rising AI, big data, and analytics workloads

+3.4%

Global

Medium to long term

High-performance workloads need IDC expansion

Increasing internet penetration and digital services usage

+3.1%

Global

Medium term

More users generate higher data traffic

Expansion of enterprise colocation and outsourcing needs

+2.8%

Developed markets

Medium to long term

Firms prefer outsourced infrastructure

Growing demand for low-latency edge computing facilities

+2.5%

North America, Asia Pacific

Medium to long term

Edge sites improve response speed

Restraints Impact Analysis

Key Restraint

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

High capital expenditure for data center construction

-3.2%

Global

Short to medium term

Large investments slow expansion

Rising energy consumption and power costs

-2.8%

Europe, North America, Asia Pacific

Medium term

Energy costs pressure margins

Land availability and zoning limitations

-2.3%

Urban hubs globally

Medium to long term

Space constraints delay projects

Cybersecurity and data sovereignty concerns

-2.0%

Global

Medium term

Compliance risks affect deployments

Cooling and environmental sustainability challenges

-1.7%

Global

Long term

Sustainability targets raise costs

By Services Analysis

The colocation segment accounted for 42.6% of the market share, reflecting its strong role in helping businesses place servers and network equipment in professionally managed facilities. This dominance is supported by the growing need for secure infrastructure, stable power supply, and high-speed connectivity without the cost of building private data centers. Colocation services allow organizations to improve efficiency while maintaining control over their hardware assets.

Another factor driving this segment is the increasing demand for scalable infrastructure that can expand with business requirements. Companies prefer colocation facilities for their strong security standards, disaster recovery capabilities, and access to multiple network providers. These benefits continue to strengthen the adoption of colocation services across industries.

By Deployment Analysis

The public cloud segment held 48.2% share, driven by the rising demand for flexible and cost-efficient computing resources. Public cloud deployment allows businesses to access storage, processing power, and applications on demand without heavy capital investment. This model supports faster digital transformation and enables organizations to scale operations based on changing workloads.

In addition, businesses are increasingly adopting hybrid and remote operating models that require accessible and centralized digital infrastructure. Public cloud platforms offer easier deployment, rapid updates, and broad service availability. These advantages have significantly increased adoption within the IDC market.

By Enterprise Size Analysis

The large enterprises segment captured 70% of the market, reflecting their extensive need for high-capacity infrastructure and advanced data management solutions. These organizations handle large volumes of data, complex applications, and global operations that require reliable and scalable data center support. IDC solutions help them maintain performance, continuity, and security.

Moreover, large enterprises have the financial and technical resources to invest in premium infrastructure services. They prioritize uptime, compliance, and efficient workload management, which has increased their reliance on modern data center solutions. This continues to support the segment’s leading position.

By End-Use Analysis

The cloud service providers segment accounted for 36.8% of the market share, driven by the rapid expansion of digital services and growing demand for cloud-based applications. CSPs require large-scale data center capacity to host workloads, deliver storage services, and maintain fast connectivity for users. Internet data centers are essential for supporting these operations.

Furthermore, increasing demand for streaming, enterprise software, analytics, and remote collaboration tools has encouraged CSPs to expand infrastructure footprints. Data centers help them ensure service availability, low latency, and efficient resource delivery. This has reinforced strong adoption among cloud service providers.

Investor Type Impact Analysis

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture capital firms

Moderate

High

US, Asia Pacific

Investing in edge and niche IDC startups

Private equity firms

High

Moderate

North America and Europe

Scaling colocation and infrastructure assets

Corporate investors

Very high

Moderate

Global

Strategic investments in cloud and AI capacity

Institutional investors

High

Low to moderate

Developed markets

Prefer stable long-term infrastructure returns

Government and public funding bodies

Moderate to high

Low

Global

Supporting digital infrastructure growth

Technology Enablement Analysis

Technology

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

AI-driven data center management systems

+3.9%

US, Europe, China

Medium to long term

Optimizes power and operations

Advanced liquid and immersion cooling

+3.5%

Global

Medium term

Supports dense compute workloads

Modular and prefabricated data center designs

+3.0%

Global

Short to medium term

Speeds deployment timelines

Renewable energy integration and smart grids

+2.7%

Europe, North America

Medium to long term

Reduces operating emissions

Automation and robotics for facility operations

+2.4%

Developed markets

Long term

Improves maintenance efficiency

Key Challenegs

High construction cost for data center buildings and infrastructure.

Large power consumption increases operating expenses.

Need for reliable cooling systems to manage heat.

Limited availability of suitable land in major cities.

Data security risks from cyberattacks and breaches.

Strict government regulations on data storage and privacy.

Shortage of skilled staff for operations and maintenance.

Downtime risks can affect customer services and trust.

High maintenance cost for servers, networks, and backup systems.

The IDC internet data center market is evolving toward highly efficient, scalable, and intelligent infrastructure designed to support rising digital workloads. One of the key emerging trends is the shift toward AI ready data centers with advanced cooling systems, high density rack designs, and optimized power distribution to handle intensive computing demand.

Another important trend is the growing adoption of modular data center architecture, which allows faster deployment and easier expansion based on changing capacity needs. There is also increasing focus on green operations, where operators are using renewable energy, energy monitoring tools, and smarter cooling controls to reduce environmental impact. In addition, edge integrated IDC models are gaining traction, bringing processing capacity closer to users for lower latency services. Automation is also expanding across facility management, helping improve uptime, predictive maintenance, and operational efficiency.

Growth Factors

The growth of this market is driven by the rapid expansion of cloud computing, digital platforms, and data intensive applications across industries. As businesses generate and process larger volumes of data, demand for reliable and secure data center capacity continues to rise. The increasing use of AI, machine learning, streaming, and enterprise software is also creating stronger need for advanced computing infrastructure.

Another major factor is the growth of remote work, digital commerce, and online services, which depend heavily on stable backend systems. Organizations are also focusing on data security, disaster recovery, and business continuity, encouraging investment in modern IDC facilities. Furthermore, the rollout of faster connectivity networks and the rise of smart devices are increasing traffic loads, supporting continued demand for scalable and high performance internet data centers.

Key Market Segments

By Services

Hosting

Colocation

CDN

Others

By Deployment

Public

Private

Hybrid

By Enterprise Size

Large Enterprises

SMEs

By End-use

Cloud Service Providers (CSPs)

Telecom

Government/Public Sector

BFSI

Media & Entertainment

E-commerce & Retail

Others

Regional Analysis

North America accounted for 40.5% of the IDC (Internet Data Center) market, supported by strong cloud adoption, advanced digital infrastructure, and high enterprise demand for data storage and computing capacity. The region has a mature technology ecosystem with widespread use of colocation, hyperscale facilities, and managed data center services.

Rapid growth in artificial intelligence workloads, streaming traffic, e-commerce activity, and enterprise digital transformation is increasing the need for scalable and secure data center capacity. In addition, strong investments in renewable energy integration, network connectivity, and disaster recovery capabilities are reinforcing regional leadership in the market.

The U.S. market reached USD 20.3 Billion and is projected to grow at a CAGR of 8.3%, driven by rising demand for cloud services, edge computing, and high-performance processing environments. Enterprises are expanding data center usage to support hybrid IT models, business continuity needs, and data-intensive applications.

The growth of generative AI, financial technology platforms, healthcare digitization, and connected devices is also increasing infrastructure requirements. In addition, continuous investment by hyperscale operators and colocation providers is expected to support steady growth of the IDC market in the US over the coming years.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The competitive landscape of the IDC (Internet Data Center) Market is shaped by a mix of global cloud providers, colocation operators, and telecom infrastructure companies. Companies such as Amazon Web Services, Inc., Microsoft, Google Cloud, Alibaba Cloud, IBM, Oracle, and Tencent Cloud focus on large-scale data center networks that support cloud computing, storage, and enterprise workloads.

These players invest heavily in capacity expansion, energy efficiency, and advanced infrastructure to meet rising demand for digital services. Their strong global reach and integrated cloud ecosystems help them maintain a leading position in the market.

At the same time, companies such as Equinix, Inc., Digital Realty, CyrusOne, CoreSite, NTT Communications Corporation, AT&T Intellectual Property, Lumen Technologies (CenturyLink), and China Telecom Americas, Inc. compete by offering colocation, interconnection, and managed hosting services for enterprises and network operators.

These players focus on secure facilities, low-latency connectivity, and flexible deployment models across multiple regions. Competition in this market is driven by scalability, uptime reliability, network connectivity, and the ability to support growing demand for AI, cloud, and data-intensive applications.

The future outlook for the IDC (Internet Data Center) Market looks very strong as demand for cloud computing, AI workloads, and digital services continues to rise. The market is expected to grow with increasing need for secure data storage, high-speed processing, and reliable network connectivity. Businesses are anticipated to invest more in modern data centers to support remote work, streaming, e-commerce, and enterprise applications. In the coming years, adoption of green infrastructure, edge data centers, automation, and advanced cooling systems is expected to improve efficiency and capacity, making internet data centers a key part of global digital infrastructure.

Recent Developments

March, 2026 – Alibaba Cloud launches 4th Malaysia data center marking largest SEA presence plus new facilities in Mexico, Japan, South Korea, Dubai. Partners NVIDIA for AI development while 91 availability zones span 29 regions globally. APAC cloud leader.

February, 2026 – AWS accelerates growth hitting $33B quarterly revenue, fastest since 2022 via AI demand with $200B backlog. Q4 guidance projects $206-213B while operating income hits $11.4B; heavy CapEx fuels 2026 AI surge. Cloud computing giant.

Report Scope

Report Features

Description

Market Value (2025)

USD 56.2 Billion

Forecast Revenue (2035)

USD 152.5 Billion

CAGR(2025-2035)

10.50%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2025-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Services (Hosting, Colocation, CDN, Others), By Deployment (Public, Private, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By End-use (Cloud Service Providers (CSPs), Telecom, Government/Public Sector, BFSI, Media & Entertainment, Others)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA

Competitive Landscape

Alibaba Cloud, Amazon Web Services, Inc., AT&T Intellectual Property, Lumen Technologies (CenturyLink), China Telecom Americas, Inc., CoreSite, CyrusOne, Digital Realty, Equinix, Inc., Google Cloud, IBM, Microsoft, NTT Communications Corporation, Oracle, Tencent Cloud, Others

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Purchase Options

We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

Market")