Quick Navigation

Report Overview

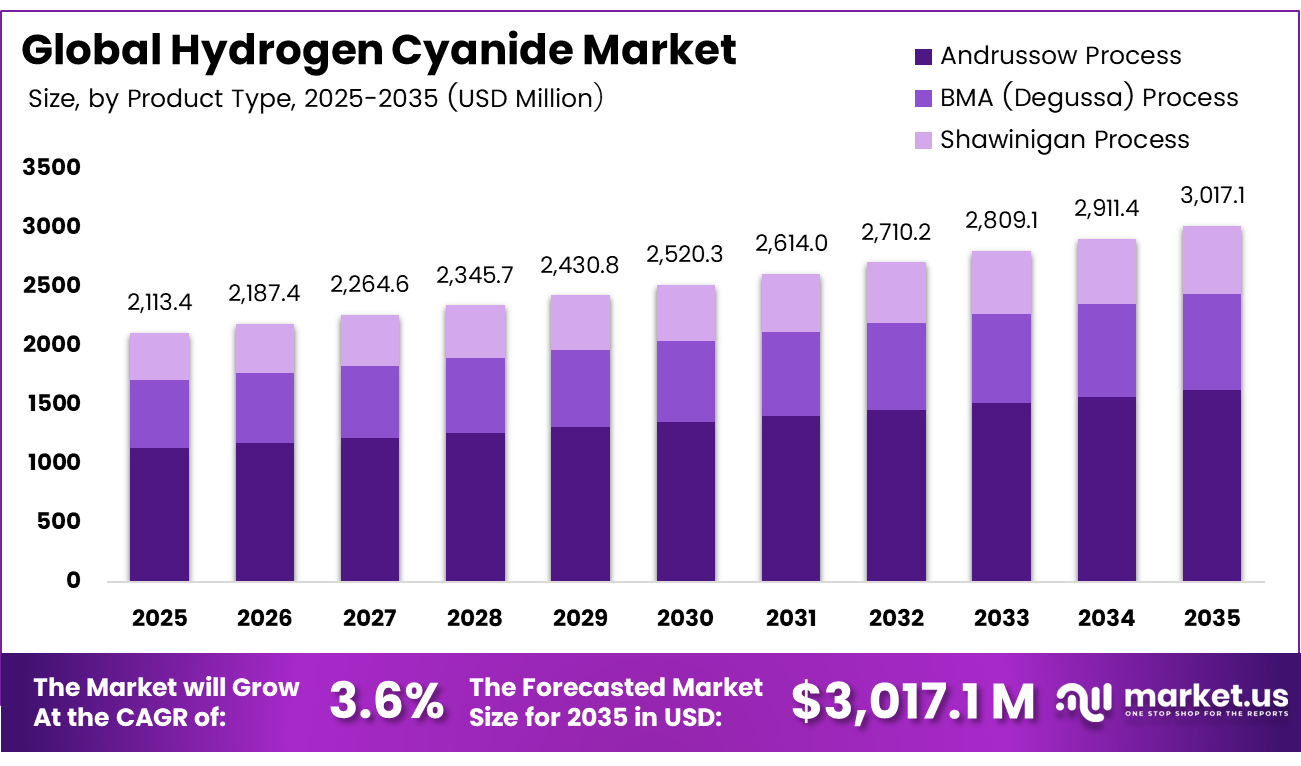

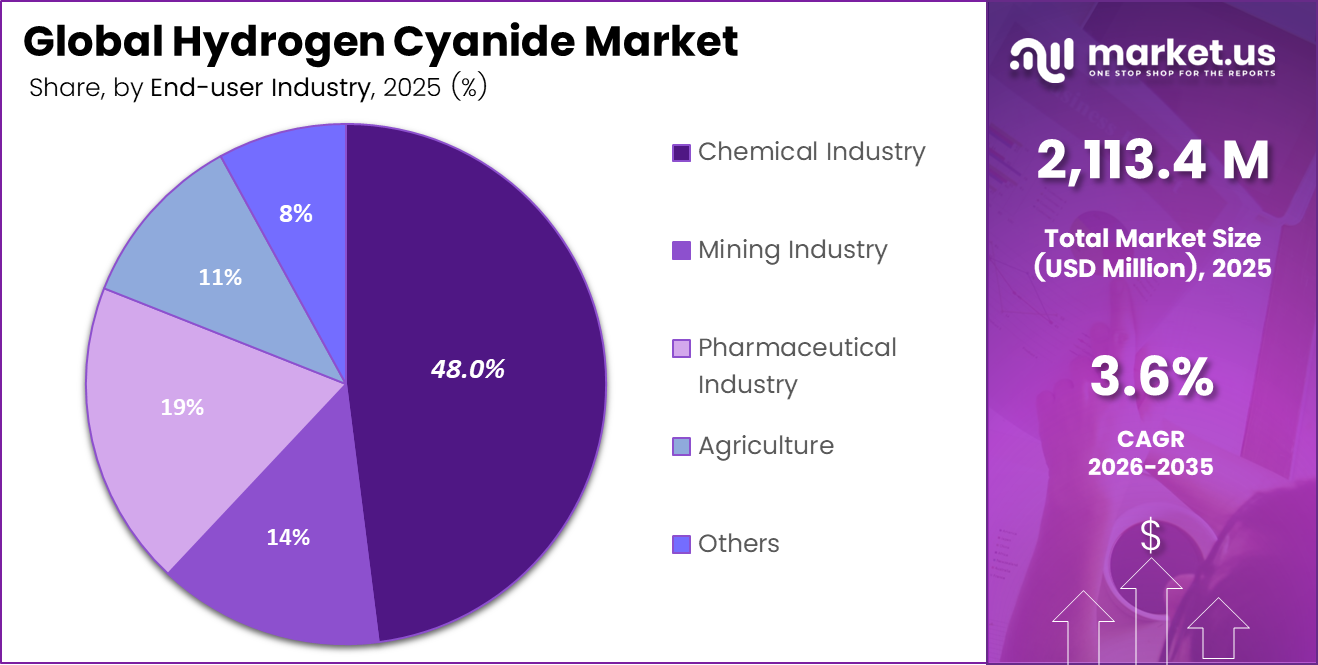

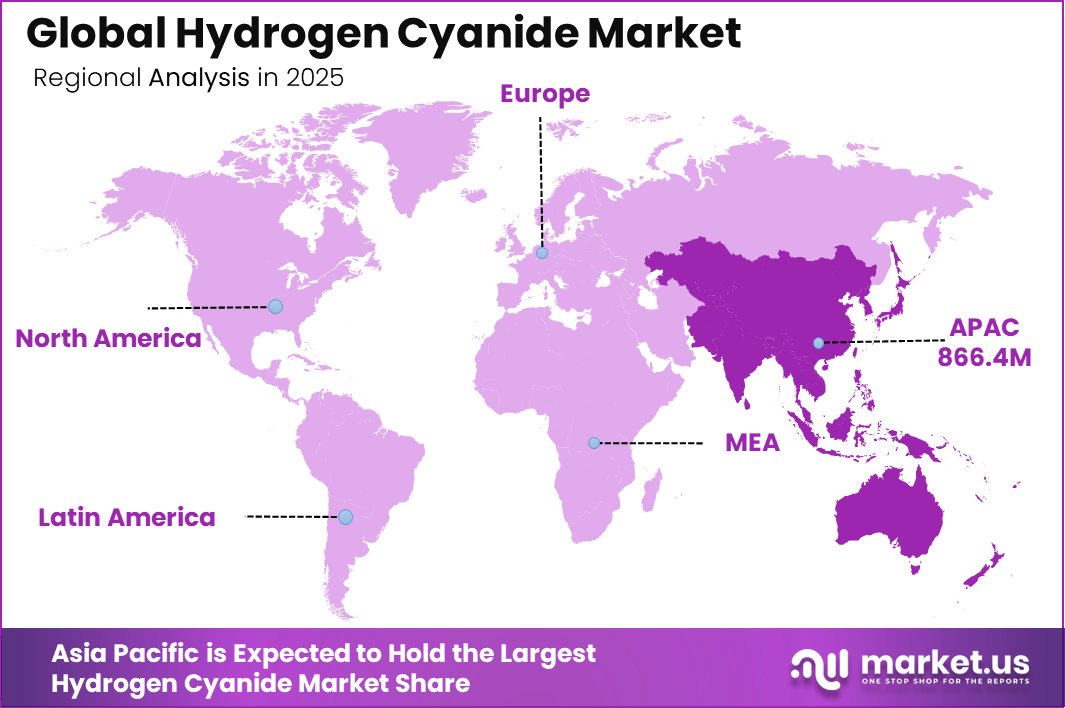

The Global Hydrogen Cyanide Market was valued at USD 2,113.4 million in 2025, and between 2026 and 2035, this market is estimated to register a CAGR of 3.6%, reaching about USD 3,017.1 million by 2035. Asia Pacific held a dominant market position, capturing more than a 41% share, holding USD 866.4 million in revenue.

The global hydrogen cyanide industry is supported by its role as a key precursor for adiponitrile, sodium cyanide, acetone cyanohydrin, methionine, and other specialty chemicals. These derivatives are used in nylon 6,6, engineered plastics, synthetic fibers, pharmaceuticals, and precious-metal extraction. In 2024, the European Federation of Pharmaceutical Industries and Associations highlighted continued growth in global pharmaceutical research and development investment, supporting demand for high-purity chemical intermediates such as hydrogen cyanide.

Operational investments are increasing production capacity across the hydrogen cyanide value chain. Australian Gold Reagents is expanding its HCN-integrated sodium cyanide facility, raising annual liquid sodium cyanide capacity from 94,000 tonnes to approximately 130,000 tonnes, an increase of more than 30%.

The same project will expand solid sodium cyanide capacity from 46,000 tonnes to 60,000 tonnes per year, representing an increase of about 30.4%. These additions are intended to support rising demand from gold-mining operations and other industrial users of cyanide-based chemicals.

The expansion also includes environmental and efficiency improvements. AGR’s updated production and incineration configuration is designed to reduce greenhouse-gas emissions intensity by approximately 28%, while more than 70% of the wastewater generated at the facility is already recycled onsite. The lower-emissions incinerator received A$7.5 million in funding through Australia’s Powering the Regions Fund.

Key Takeaways

- The global hydrogen cyanide market was valued at US$ 2,113.4 million in 2025.

- The global hydrogen cyanide market is projected to grow at a CAGR of 3.6% and is estimated to reach US$3,017.1 million by 2035.

- On the basis of production process, the Andrussow Process dominated the global hydrogen cyanide market, constituting 54.0% of the total market share.

- Based on application, Adiponitrile Production dominated the hydrogen cyanide market, with a substantial market share of around 43.0%.

- Based on end-use industry, the Chemical Industry led the market, comprising 48.0% of the total market share.

- Among purity levels, Industrial Grade held a major share in the hydrogen cyanide market, accounting for 76.0% of the market share.

- Among the distribution channels, Direct/Bulk Supply dominated the market, representing 81.0% of the total market share.

- In 2025, Asia Pacific was the most dominant region in the global hydrogen cyanide market, accounting for 41% of the total market share.

Production Process Analysis

Andrussow Process dominated the production process segment.

The Andrussow Process is the main method used in making hydrogen cyanide globally, holding 54% of the market. This process is popular because it is efficient, saves money, and is used a lot in big chemical factories. It works by mixing methane, ammonia, and oxygen in one step with a catalyst, which quickly makes hydrogen cyanide at lower costs for both setting up and running the plant.

The Shawinigan Process accounted for 19% and is the fastest-growing segment. It is used in certain industrial setups where companies prefer using different raw materials or setting up custom production lines. But it uses a lot of energy and isn’t as cost-effective as newer, larger-scale methods, which has limited how widely it’s used.

Application Analysis

Dominance of Adiponitrile production Segment in Global Hydrogen Cyanide Market.

Adiponitrile production was the largest part of the global hydrogen cyanide market, making up 43% of the total share and being the most important use of hydrogen cyanide. This is because adiponitrile is a key material used to make nylon 6,6, which is a strong, high-performance polymer used in many industries like automotive, electronics, textiles, industrial machinery, and consumer products.

Meanwhile, Chelating Agents accounted for 9% of the global hydrogen cyanide market and emerged as the fastest-growing application segment during the forecast period. Growth is being driven by increasing demand for advanced water treatment solutions, stricter environmental regulations, and rising industrial wastewater management requirements across both developed and emerging economies.

End-Use Industry Analysis

Chemical Industry dominated the market.

The Chemical Industry dominated the global hydrogen cyanide market, with 48% of the overall market share. The segment’s success is primarily due to the widespread usage of hydrogen cyanide as a crucial step in the manufacturing of adiponitrile, acetone cyanohydrin, chelating agents, and a variety of specialty chemicals.

Strong demand from the nylon 6,6 value chain, engineering plastics, coatings, adhesives, and performance compounds is driving consumption in chemical production facilities around the world. The Pharmaceutical sector accounted for 19% of the global hydrogen cyanide market and was the fastest-growing end-use sector segment during the forecast period.

Purity Level Analysis

Industrial Grade Leads the Segment.

Industrial Grade dominated the global hydrogen cyanide market, with 76% of the overall market share. The segment’s leadership is partly due to its widespread use in large-scale industrial applications such as adiponitrile manufacture, sodium cyanide manufacturing, acetone cyanohydrin synthesis, and various chemical processing operations.

The continuing expansion of nylon 6,6 manufacture, precious metal extraction, and specialized chemical manufacturing has increased global demand for industrial-grade hydrogen cyanide. Its ubiquitous availability, established supply lines, and adaptability for high-volume production methods all help to maintain its market dominance.

Distribution Channel Analysis

Direct/Bulk Supply Maintained Market Leadership Supported by Strong Demand.

Direct/Bulk Supply dominated the global hydrogen cyanide market, with 81% of the overall market share. The segment’s dominance stems mostly from the extremely hazardous nature of hydrogen cyanide, which necessitates specific handling, transportation, and storage infrastructure.

Major chemical manufacturers and major industrial consumers often purchase hydrogen cyanide directly from suppliers under long-term supply agreements to ensure product quality, supply security, and regulatory compliance.

Direct distribution also allows for cost savings for high-volume buyers involved in adiponitrile manufacture, sodium cyanide manufacturing, and other large-scale chemical operations. Furthermore, the integration of many hydrogen cyanide production plants with downstream manufacturing operations has reinforced the industry’s preference for direct and bulk supply channels.

Key Market Segments

By Production Process

- Andrussow Process

- BMA (Degussa) Process

- Shawinigan Process

By Application

- Adiponitrile Production

- Sodium Cyanide Production

- Acetone Cyanohydrin

- Chelating Agents

- Others

By End-Use Industry

- Chemical Industry

- Mining Industry

- Pharmaceutical Industry

- Agriculture

- Others

By Purity Level

- Industrial Grade

- High Purity Grade

By Distribution Channel

- Direct/Bulk Supply

- Chemical Distributors

- Specialty Chemical Suppliers

Market Dynamics

Drivers

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adiponitrile and nylon 6,6 demand | +1.5% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Cyanide salts for gold mining | +0.8% | Latin America, Africa, Australia, Central Asia | Medium term (2–4 years) |

| Engineering plastics in mobility | +0.5% | Europe, Asia-Pacific | Medium term (2–4 years) |

| Hydrogen cyanide by-product recovery | +0.4% | North America, Europe | Short term (≤ 2 years) |

| Expansion in Asia-Pacific chemical hubs | +0.3% | China, India, Southeast Asia | Medium term (2–4 years) |

Adiponitrile and nylon 6,6 demand

Hydrogen cyanide is a critical precursor for adiponitrile via hydrocyanation of butadiene, and industry and technical literature indicate that large-scale applications for adiponitrile and cyanide salts dominate hydrogen cyanide consumption, with adiponitrile feeding directly into nylon 6,6 production for engineering plastics and fibers.

Over the 2024–2026 window, automotive and electrical&electronics sectors have increased nylon 6,6 use for under-the-hood components, lightweight structural parts, and cable insulation, supporting mid-single-digit (3–4%) annual growth in adiponitrile-linked demand across major regions and lifting typical hydrogen cyanide plant utilization from roughly the mid-70% range into the low-80%s, which contributes an estimated incremental +1.5% to the baseline CAGR through higher fixed-cost absorption and improved throughput.

Strategically, this demand concentration has pushed producers toward integrated value-chain models where a significant share of hydrogen cyanide is consumed captively in adiponitrile and nylon units, reducing merchant availability but improving margin structures by an estimated 150–250 basis points compared with standalone hydrogen cyanide sales, and altering commercial behavior toward long-term offtake contracts, capacity-tied pricing mechanisms, and prioritization of downstream polymer debottlenecking over greenfield hydrogen cyanide-only capacity.

Restraints

| Restraint | (~) % Impact on

CAGR |

Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent occupational exposure limits | -1.2% | North America, Europe, selected Asia-Pacific | Short term (≤ 2 years) |

| High compliance and emission control CapEx | -0.9% | OECD markets | Medium term (2–4 years) |

| Transport and storage restrictions | -0.7% | Latin America, Africa, Asia-Pacific | Short term (≤ 2 years) |

| Permitting hurdles for new units | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Customer substitution in sensitive sectors | -0.3% | Europe, North America | Medium term (2–4 years) |

Stringent occupational exposure limits

Regulators set very low permissible exposure limits for hydrogen cyanide because of its acute toxicity, with OSHA listing a permissible exposure limit time-weighted average of 10 ppm (11 mg/m³) and guideline values for short-term exposures in the single-digit ppm range, requiring continuous monitoring, ventilation, and tight process enclosure at production and downstream use sites.

Implementing these controls can add low single-digit percentages to total project capital costs and recurring operating expenses equivalent to tens of dollars per ton of hydrogen cyanide handled, while also imposing throughput constraints such as lower maximum occupancy, mandatory evacuation procedures, and periodic shutdowns for maintenance and testing, together contributing an estimated drag of about -1.2% on the CAGR by discouraging marginal expansions and limiting effective capacity, especially in small or older facilities.

Challenges

| Challenge | (~) % CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Process safety and incident risk | -1.0% | Global | Long term (≥ 4 years) |

| Feedstock and energy price volatility | -0.8% | Global | Medium term (2–4 years) |

| Skilled hazardous-operations labor gap | -0.6% | OECD and emerging industrial hubs | Long term (≥ 4 years) |

| Evolving environmental expectations | -0.5% | Europe, North America | Medium term (2–4 years) |

| Supply chain fragility in mining regions | -0.4% | Latin America, Africa, Asia-Pacific | Medium term (2–4 years) |

Process safety and incident risk

Hydrogen cyanide’s high volatility, low lethal dose, and tendency to form explosive mixtures mean that even small releases can have severe health and environmental consequences, and regulatory economic impact assessments for cyanide manufacturing highlight process vents and equipment leaks as key hazards requiring extensive controls and periodic audits.

Each significant incident can trigger multi-month shutdowns, mandated retrofits, and new site-specific requirements that add perhaps 5–10% to capital budgets for detection, containment, and automation, while also cutting effective capacity utilization by several percentage points due to tighter operating envelopes and more frequent inspections, together imposing an estimated -1.0% drag on the maximum attainable CAGR as firms pace expansions more conservatively.

Opportunities

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| High-purity HCN for specialty intermediates | +0.9% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Emerging-market gold mining expansion | +0.8% | Latin America, Africa, Central Asia | Long term (≥ 4 years) |

| On-site cyanide solution services | +0.7% | Mining hubs worldwide | Medium term (2–4 years) |

| Circular detox and waste treatment offerings | +0.6% | Europe, North America | Long term (≥ 4 years) |

| Portfolio and M&A-driven rationalization | +0.5% | Global | Medium term (2–4 years) |

High-purity HCN for specialty intermediates

Current large-scale hydrogen cyanide production is configured mainly for bulk applications such as cyanide salts for mining and adiponitrile for nylon, while technical overviews note that hydrogen cyanide is also a precursor to a wide range of fine chemicals, pharmaceuticals, and chelating agents via cyanohydrin routes and related chemistries, which typically require tighter impurity control and documentation than standard bulk grades.

Reconfiguring or debottlenecking existing units with additional purification, analytics, and quality assurance capabilities can add low-to-mid single-digit percentages to unit production costs but allows producers to capture higher price points and more resilient demand, potentially expanding gross margins by around 300–500 basis points versus bulk-grade material and contributing an incremental CAGR uplift of roughly +0.9% if a modest share of output is upgraded into these specialty channels.

Geopolitical Impact Analysis

Trade Uncertainty and Energy Market Disruptions Reshaping the Hydrogen Cyanide Industry.

Geopolitical instability is directly influencing the hydrogen cyanide market because HCN production depends on feedstocks such as methane, natural gas, and ammonia. Disruptions in energy markets can raise production costs, reduce supply certainty, and affect chemical manufacturing margins.

The Russia-Ukraine conflict caused major volatility in European gas markets and forced buyers to diversify supply sources, increasing cost pressure on energy-intensive chemical producers. Trade restrictions, sanctions, and shifting international relationships can also affect the movement of raw materials, catalysts, industrial equipment, and downstream chemicals such as sodium cyanide, adiponitrile, and acetone cyanohydrin.

These pressures are encouraging producers to strengthen regional supply chains, expand integrated production models, and improve operational efficiency. While geopolitical disruption creates short-term cost and supply risks, it is also pushing the industry toward more resilient and localized production strategies.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Hydrogen Cyanide Market.

Asia-Pacific dominated the global hydrogen cyanide market, accounting for 41% of the total market share, and is also expected to be the fastest-growing regional market during the forecast period. The region’s leadership is driven by its large and expanding chemical manufacturing base, rapid industrialization, and strong demand from downstream industries such as nylon production, mining, pharmaceuticals, and specialty chemicals.

China, India, Japan, and South Korea represent the major consumption and production hubs, supported by growing investments in chemical processing infrastructure and manufacturing capacity expansion. The region also benefits from cost-competitive production, readily available raw materials, and increasing demand for engineering plastics and industrial chemicals, further strengthening its market position.

North America and Europe continue to be important markets for hydrogen cyanide, supported by their well-established chemical industries, advanced manufacturing capabilities, and strong demand from sectors such as automotive, pharmaceuticals, and specialty chemicals. North America benefits from abundant natural gas resources and integrated chemical supply chains, while Europe’s market is driven by technological innovation, high-quality production standards, and stringent environmental regulations.

Latin America is experiencing steady growth due to expanding mining activities, particularly in major gold- and silver-producing countries such as Brazil, Chile, and Mexico, which support demand for sodium cyanide and related products. The Middle East & Africa is also emerging as a promising market, driven by increasing investments in petrochemicals, industrial diversification programs, mining projects, and infrastructure development.

Key Regions and Countries Covered in this Report

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- North America

- The US

- Canada

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global hydrogen cyanide market is moderately consolidated, with a limited number of large manufacturers accounting for a significant share of total production capacity. Market leadership is primarily determined by production scale, access to feedstocks, integrated manufacturing operations, technological expertise, and long-term relationships with downstream customers.

The market is also characterized by high entry barriers due to stringent safety regulations, specialized production technologies, and substantial capital investment requirements. Leading market participants are focused on expanding production capacities, improving process efficiency, and strengthening their positions in high-growth end-use sectors such as chemicals, mining, pharmaceuticals, and specialty materials.

Strategic investments in advanced manufacturing technologies, emission reduction initiatives, and supply chain optimization are helping companies enhance competitiveness and meet evolving regulatory requirements. In addition, manufacturers are increasingly emphasizing high-purity product offerings and sustainable production practices to address growing demand from specialty chemical and pharmaceutical applications.

Major Players in the Industry

- INEOS Group

- Evonik Industries

- Ascend Performance Materials

- Butachimie

- Cyanco

- Draslovka Holding

- Taekwang Industrial

- Cornerstone Chemical Company

- Kuraray Co., Ltd.

- CSBP Limited

- Lukoil

- Sterling Chemicals

- Formosa Plastics Corporation

- Sinopec

- Air Liquide

Key Development

- In March 2025, Ascend Performance Materials implemented operational improvement initiatives at its integrated adiponitrile and hydrogen cyanide manufacturing facilities to enhance production reliability, optimize process efficiency, and support increasing demand from the global nylon 6,6 industry.

- In May 2024, INEOS Group continued expanding its specialty chemicals portfolio through process optimization and sustainability initiatives aimed at improving production efficiency and reducing emissions across its chemical manufacturing operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2,113.4 Mn |

| Forecast Revenue (2035) | USD 3,017.1 Mn |

| CAGR (2026-2035) | 3.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Production Process (Andrussow Process, BMA (Degussa) Process, and Shawinigan Process), By Application (Adiponitrile Production, Sodium Cyanide Production, Acetone Cyanohydrin, Chelating Agents, and Others), By End-Use Industry (Chemical Industry, Mining Industry, Pharmaceutical Industry, Agriculture, and Others), By Purity Level (Industrial Grade and High Purity Grade), By Distribution Channel (Direct/Bulk Supply, Chemical Distributors, and Specialty Chemical Suppliers) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | INEOS Group, Evonik Industries, Ascend Performance Materials, Butachimie, Cyanco, Draslovka Holding, Taekwang Industrial, Cornerstone Chemical Company, Kuraray Co., Ltd., CSBP Limited, Lukoil, Sterling Chemicals, Formosa Plastics Corporation, Sinopec, Air Liquide, and other key players. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, we can provide further customization to meet your requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |