Global Hospital Bed Management Systems Market By Component (Software, Hardware and Services), By Deployment Mode (Cloud-based and On-premises), By Type (Real-Time Bed Tracking Systems, Patient Flow Management Systems, Bed Capacity Planning Systems and Integrated Bed Management Platforms), By Hospital Size (Small Hospitals, Medium-sized Hospitals and Large Hospitals), By End User (General Hospitals, Specialty Hospitals, Ambulatory Surgical Centers and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 183089

- Number of Pages: 200

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

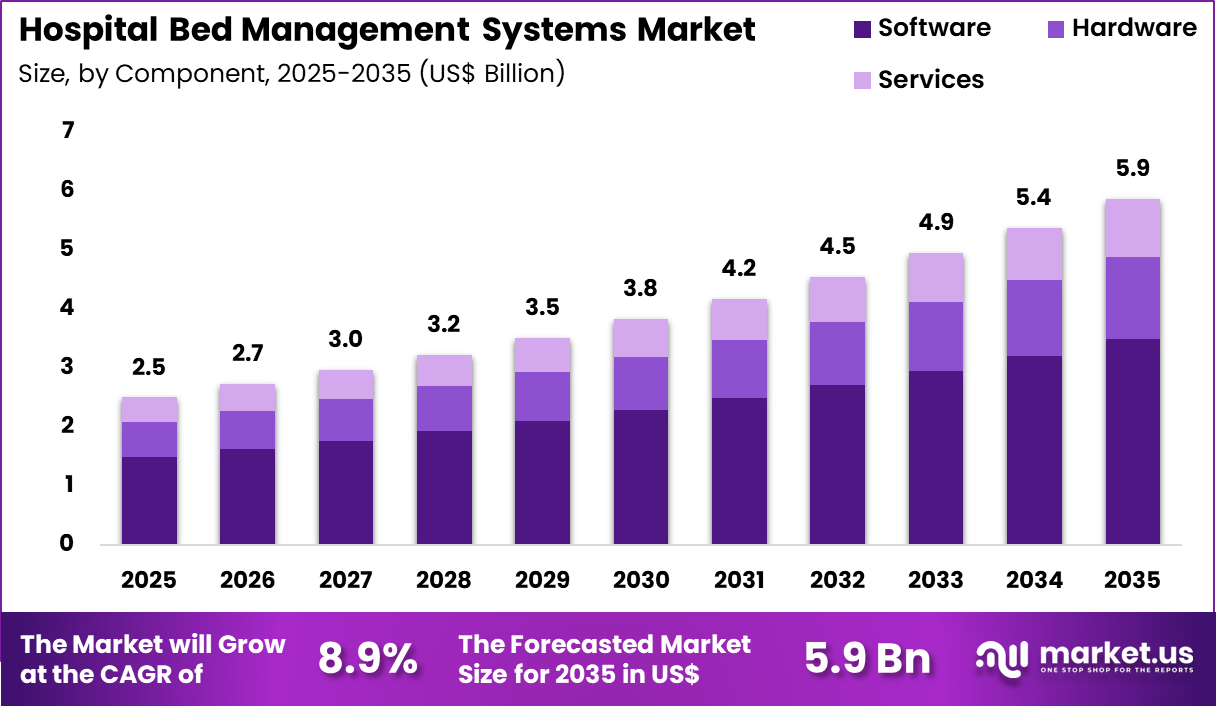

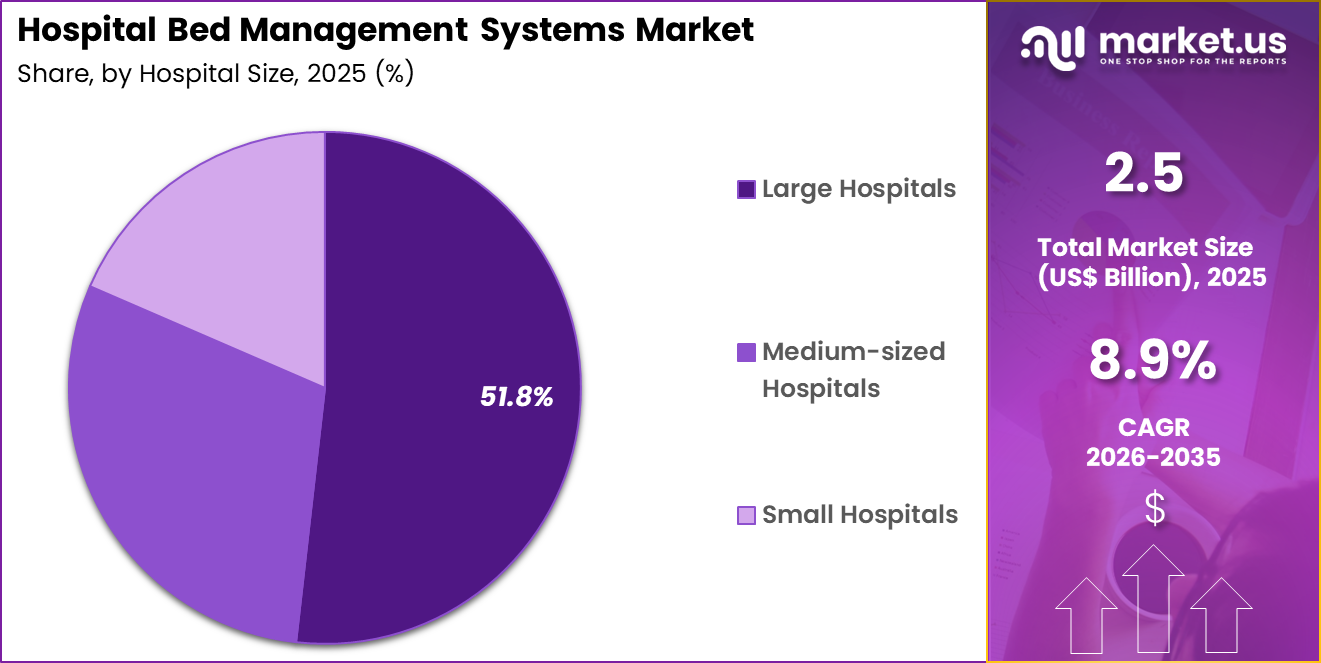

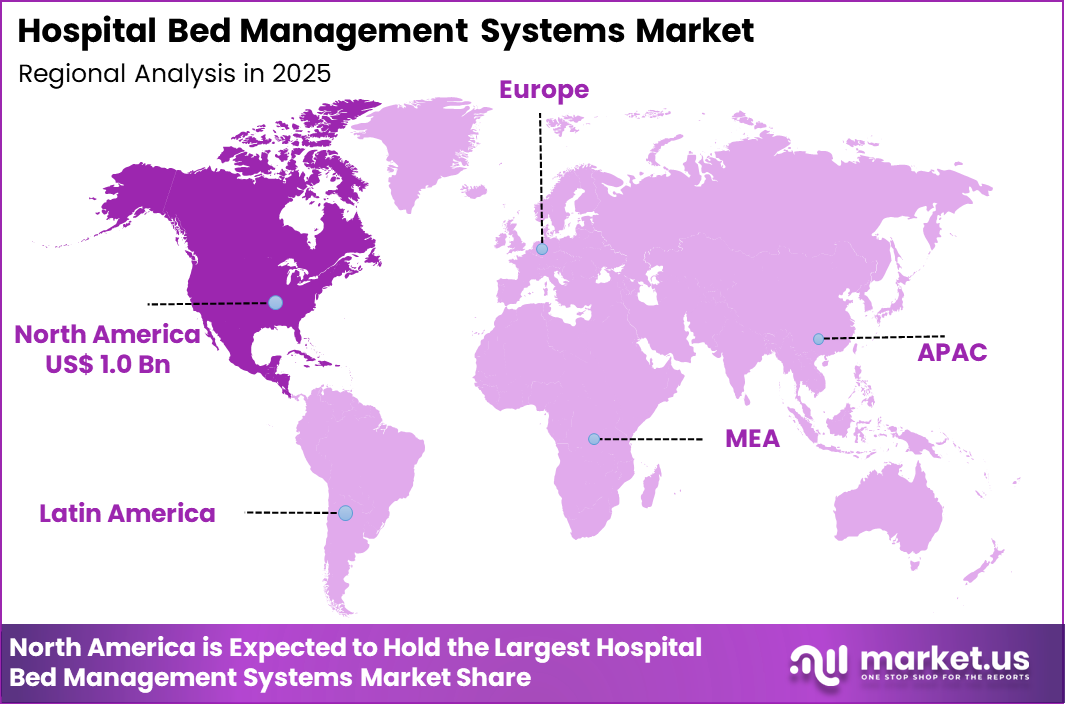

The Global Hospital Bed Management Systems Market size is expected to be worth around US$ 5.9 Billion by 2035 from US$ 2.5 Billion in 2025, growing at a CAGR of 8.9% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 41.5% share with a revenue of US$ 1.0 Billion.

Rising pressure on hospital capacity and the need for efficient patient flow drive the Hospital Bed Management Systems market as healthcare organizations seek integrated platforms that optimize bed utilization, reduce length of stay, and improve overall operational performance.

Hospital administrators increasingly deploy these systems to provide real-time visibility into bed availability across medical, surgical, and critical care units, enabling rapid placement of admitted patients and minimizing emergency department boarding times. Care teams utilize the platforms to coordinate multidisciplinary discharge planning, tracking barriers such as pending consultations, test results, and transportation arrangements to facilitate timely transitions to post-acute settings.

These solutions support predictive analytics that forecast admission surges and capacity constraints, allowing hospitals to adjust staffing and resource allocation proactively during peak periods. In high-acuity environments, bed management systems integrate with electronic health records to prioritize patients based on clinical acuity and infection control requirements, enhancing safety and throughput. The systems also enable command-center operations that centralize oversight of patient movement, improving communication between nursing, case management, and environmental services teams.

Technology providers pursue opportunities to embed artificial intelligence and machine learning capabilities that enhance predictive accuracy and automate workflow orchestration, expanding applications in complex academic medical centers and large health systems managing high patient volumes. These advancements support scenario modeling that simulates the impact of staffing changes or service line expansions on bed utilization.

In November 2025, TeleTracking introduced Decision IQ, an artificial intelligence–driven platform designed to improve patient flow within hospitals. The system creates a dynamic digital model of hospital operations, enabling care teams to anticipate discharge timing, forecast capacity constraints, and address bottlenecks before they affect patient care delivery.

Opportunities emerge in integrating bed management platforms with telehealth and remote monitoring tools to support hospital-at-home programs and virtual care transitions. Companies invest in user-friendly dashboards and mobile interfaces that empower frontline staff to make data-driven decisions in real time.

Recent trends emphasize predictive capacity management, seamless interoperability with electronic health records, and AI-supported decision intelligence, positioning hospital bed management systems as essential infrastructure for resilient, efficient, and patient-centered hospital operations.

Key Takeaways

- In 2025, the market generated a revenue of US$ 2.5 Billion, with a CAGR of 8.9%, and is expected to reach US$ 5.9 Billion by the year 2035.

- The component segment is divided into software, hardware and services, with software taking the lead with a market share of 59.6%.

- Considering deployment mode, the market is divided into cloud-based and on-premises. Among these, cloud-based held a significant share of 61.5%.

- Furthermore, concerning the type segment, the market is segregated into real-time bed tracking systems, patient flow management systems, bed capacity planning systems and integrated bed management platforms. The patient flow management systems sector stands out as the dominant player, holding the largest revenue share of 44.3% in the market.

- The hospital size segment is segregated into small hospitals, medium-sized hospitals and large hospitals, with the large hospitals segment leading the market, holding a revenue share of 51.8%.

- Considering end user, the market is divided into general hospitals, specialty hospitals, ambulatory surgical centers and others. Among these, general hospitals held a significant share of 42.1%.

- North America led the market by securing a market share of 41.5%.

Component Analysis

Software accounted for 59.6% of growth within component and dominates the hospital bed management systems market due to its central role in coordinating patient flow, bed allocation, and real-time operational visibility. Hospitals increasingly rely on software platforms to track bed occupancy, manage admissions and discharges, and reduce patient wait times.

Healthcare systems continue to face capacity constraints, which increases the need for efficient digital solutions. Software-based systems are expected to expand as hospitals adopt data-driven decision-making tools to optimize resource utilization. Clinicians and administrators use these systems to improve coordination between departments and reduce bottlenecks.

The segment is likely to benefit from integration with electronic health records and hospital information systems. Continuous advancements in analytics and dashboard capabilities are projected to enhance system performance. As hospitals focus on improving efficiency and patient outcomes, software solutions are estimated to remain the dominant component in this market.

Deployment Mode Analysis

Cloud-based accounted for 61.5% of growth within deployment mode and dominates the hospital bed management systems market due to its scalability, flexibility, and lower upfront infrastructure requirements. Healthcare providers increasingly prefer cloud solutions as they enable real-time data access across multiple departments and locations.

Cloud-based systems are expected to grow as hospitals aim to improve interoperability and remote accessibility of operational data. These platforms allow faster deployment and easier updates compared to traditional systems. The segment is likely to benefit from increasing adoption of digital health infrastructure and smart hospital initiatives.

Cloud solutions also support centralized monitoring, which improves decision-making efficiency. As healthcare organizations continue to modernize IT systems, cloud-based deployment is anticipated to maintain its leading position in this market.

Type Analysis

Patient flow management systems accounted for 44.3% of growth within type and dominate the hospital bed management systems market due to their ability to streamline patient movement across departments and reduce overcrowding. Hospitals face increasing pressure to manage admissions, transfers, and discharges efficiently, which drives demand for these systems.

Patient flow solutions are expected to expand as healthcare facilities focus on reducing length of stay and improving throughput. These systems provide real-time visibility into bed availability and patient status, which enhances coordination.

The segment is likely to benefit from rising patient volumes and increasing emergency department visits. Improved workflow management is projected to support better patient outcomes and operational efficiency. As hospitals prioritize seamless care delivery, patient flow management systems are estimated to remain the leading type segment.

Hospital Size Analysis

Large hospitals accounted for 51.8% of growth within hospital size and dominate the hospital bed management systems market due to their high patient volumes and complex operational structures. These facilities require advanced systems to manage large numbers of beds, departments, and patient transitions.

Large hospitals are expected to adopt bed management systems extensively to optimize resource utilization and reduce inefficiencies. The segment benefits from higher investment capacity in digital infrastructure and advanced technologies.

Large institutions are likely to prioritize integrated systems that support real-time decision-making and coordination across multiple units. Increasing demand for efficient hospital operations is projected to drive adoption in this segment. As healthcare delivery becomes more complex, large hospitals are anticipated to maintain their dominant position.

End User Analysis

General hospitals accounted for 42.1% of growth within end user and dominate the hospital bed management systems market due to their broad service offerings and high patient intake across multiple specialties. These hospitals manage diverse patient populations, which increases the need for efficient bed allocation and flow management.

General hospitals are expected to lead adoption as they face continuous demand for emergency, inpatient, and outpatient services. The segment benefits from the need to coordinate multiple departments and ensure timely patient care. Increasing hospital admissions and healthcare utilization are likely to support demand for bed management systems.

General hospitals are projected to invest in digital solutions to improve operational efficiency and patient experience. As healthcare systems continue to expand, general hospitals are estimated to retain their leading position in this market.

Key Market Segments

By Component

- Software

- Hardware

- Services

By Deployment Mode

- Cloud-based

- On-premises

By Type

- Real-Time Bed Tracking Systems

- Patient Flow Management Systems

- Bed Capacity Planning Systems

- Integrated Bed Management Platforms

By Hospital Size

- Small Hospitals

- Medium-sized Hospitals

- Large Hospitals

By End User

- General Hospitals

- Specialty Hospitals

- Ambulatory Surgical Centers

- Others

Drivers

Rising hospital admissions and bed occupancy rates are driving the Hospital Bed Management Systems market.

Increasing patient volumes and higher bed utilization necessitate efficient real-time tracking and allocation tools to optimize capacity and reduce bottlenecks. According to the American Hospital Association, total annual admissions in all U.S. hospitals exceeded 34 million in 2025.

The OECD reported an average hospital bed occupancy rate of 72% in 2023 across member countries, with rates surpassing 85% in select nations such as Ireland. In the United States, the number of staffed beds in all hospitals reached 907,216 as per the 2024 AHA Annual Survey data. These metrics reflect sustained pressure on inpatient resources stemming from chronic disease prevalence, aging populations, and post-pandemic recovery demands.

Bed management systems provide color-coded visibility, patient flow analytics, and automated alerts that enhance throughput and minimize emergency department boarding. Hospitals increasingly adopt these platforms to address overcrowding and improve discharge planning coordination. Public health initiatives, including the CDC’s Hospital Bed Capacity Project initiated in 2022 with expansions in 2024, underscore the value of automated data feeds for operational resilience.

Integration with electronic health records further supports data-driven decision-making for admissions and transfers. Professional guidelines emphasize capacity management as essential for maintaining care quality amid fluctuating demand. Consequently, these operational and epidemiological pressures constitute a primary driver propelling market expansion during the 2022–2025 period.

Restraints

High implementation and integration costs are restraining the Hospital Bed Management Systems market.

Deployment of sophisticated bed management platforms requires substantial upfront investment in software licensing, hardware infrastructure, and staff training, which burdens smaller or resource-constrained facilities. Ongoing expenses for system maintenance, cybersecurity compliance, and interoperability upgrades with legacy electronic health records add to total ownership costs.

Many hospitals operate under tight budgets amid rising overall hospital care expenditures, which reached 1.5 trillion U.S. dollars in 2023 according to KFF analyses. Integration challenges with diverse vendor systems prolong rollout timelines and increase project risks. Limited reimbursement mechanisms for digital operational tools discourage rapid adoption in public health systems.

Rural and critical access hospitals face additional barriers due to constrained information technology resources and personnel. These financial and technical hurdles result in deferred purchases or reliance on manual processes despite evident inefficiencies. Persistent concerns over return on investment slow broader market penetration across facility types. Consequently, such cost-related and integration constraints impose measurable restraint on accelerated growth throughout the 2022–2025 timeframe.

Opportunities

Adoption of real-time data analytics and predictive capabilities is creating growth opportunities in the Hospital Bed Management Systems market.

Advanced platforms incorporating predictive modeling enable hospitals to forecast admissions, discharges, and bed turnover with greater accuracy, supporting proactive capacity planning. Opportunities arise for seamless linkage with Internet of Things sensors and wearable devices that monitor patient status and environmental factors in real time.

Health systems can leverage these tools to optimize staffing allocation, reduce length of stay, and enhance surge preparedness during seasonal or emergency demands. Integration with broader hospital information systems facilitates enterprise-wide visibility and collaborative decision-making across departments. Potential exists for subscription-based models and cloud deployments that lower capital barriers while providing continuous updates and scalability.

Partnerships with technology vendors allow customization for specialty units such as intensive care or emergency services. Value-based care initiatives reward demonstrated improvements in throughput and reduced boarding times, creating incentives for investment.

Expansion into outpatient and ambulatory settings broadens applicability beyond traditional inpatient environments. These technological synergies unlock diversified revenue streams and improved clinical outcomes. Overall, predictive and real-time functionalities generate substantial prospects for market differentiation and sustained adoption.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical developments are influencing investment decisions, system upgrades, and adoption rates in the hospital bed management systems market. Rising patient volumes and pressure on hospital efficiency are driving demand for digital bed tracking and workflow optimization, while inflation is increasing the cost of software deployment, integration, and IT infrastructure.

Budget constraints in public healthcare systems can delay modernization projects, especially in developing regions. Geopolitical tensions affect the supply of hardware components and create uncertainty around cross-border technology partnerships. Current US tariffs on imported electronic components and hospital equipment increase capital expenditure for healthcare providers, which may slow system upgrades in cost-sensitive environments.

These cost pressures can impact vendor pricing strategies and extend procurement cycles. At the same time, hospitals are prioritizing operational efficiency and patient flow management to reduce costs and improve care delivery. Overall, despite financial and supply-related challenges, the growing need for real-time hospital resource management is expected to support steady market growth.

Latest Trends

Integration of artificial intelligence and predictive analytics for capacity optimization represents a recent trend in the Hospital Bed Management Systems market.

In 2024 and 2025, hospitals have accelerated incorporation of predictive artificial intelligence tools within bed management workflows to forecast patient flow and automate allocation decisions. Data from the Office of the National Coordinator for Health Information Technology indicate that 71% of non-federal acute-care hospitals utilized predictive AI integrated with electronic health records in 2024, rising from 66 percent in 2023.

This trend supports dynamic dashboards that visualize bed status, predict bottlenecks, and recommend optimal patient placements in real time. Implementations combine Lean methodologies with AI algorithms to minimize idle capacity while preserving surge buffers. Cloud-based platforms enable remote monitoring and cross-facility coordination, aligning with CDC efforts to enhance automated bed capacity reporting.

The approach reduces administrative burden on staff and improves response to fluctuating demand patterns. Publications and operational case studies from 2025 highlight measurable gains in throughput and reduced emergency department wait times through these intelligent systems.

This evolution prioritizes proactive rather than reactive management, fostering resilience in high-occupancy environments. Prominent in 2024–2025, artificial intelligence integration continues to redefine standards for efficient hospital resource utilization.

Regional Analysis

North America is leading the Hospital Bed Management Systems Market

North America accounted for 41.5% of the hospital bed management systems market in 2025 as healthcare providers intensified efforts to optimize patient flow and reduce overcrowding across emergency and inpatient departments. Hospitals across the United States are deploying digital bed tracking platforms that provide real-time visibility into bed availability, discharge status, and patient movement across departments.

According to the American Hospital Association, the United States had about 919000 staffed hospital beds in 2022, highlighting the scale of infrastructure that requires efficient coordination and utilization. Rising patient volumes, particularly in emergency care and aging populations, have increased pressure on hospitals to manage bed occupancy more effectively.

Healthcare systems are integrating bed management software with electronic health records and admission-discharge-transfer systems to streamline operations. Predictive analytics tools are helping administrators forecast patient inflow and optimize bed allocation in advance.

Hospitals are also adopting centralized command centers that monitor bed usage and coordinate patient transfers in real time. Digital transformation initiatives and government support for healthcare IT are further accelerating adoption of operational management systems. These developments collectively supported strong growth of hospital bed management solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong expansion during the forecast period as healthcare infrastructure improves and hospitals adopt digital systems to manage growing patient demand. Countries such as China, India, Japan, and Southeast Asian nations are expanding hospital capacity while also facing challenges related to high patient volumes and limited bed availability in urban centers.

The World Health Organization reported that many countries in the region have lower hospital bed density compared to developed nations, encouraging healthcare providers to improve efficiency through digital management tools. Hospitals across the region are implementing bed tracking systems that enhance coordination between departments and reduce patient waiting times.

Governments are promoting smart hospital initiatives that integrate digital technologies into healthcare operations. Private healthcare providers are also investing in centralized monitoring platforms that optimize patient flow and resource utilization. Increasing adoption of electronic health records is enabling seamless integration with bed management systems.

Technology vendors are introducing scalable and cost-effective solutions tailored for high-volume hospitals. These developments are expected to accelerate adoption of hospital bed management technologies across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Hospital Bed Management Systems Market expand growth by deploying real-time capacity management platforms, integrating patient flow analytics, and collaborating with hospitals to optimize bed allocation and reduce admission delays. Companies invest in cloud-based dashboards, interoperability with electronic health records, and predictive algorithms that forecast occupancy and streamline discharge planning.

They also strengthen implementation services and training programs that help healthcare facilities improve operational efficiency and patient throughput. TeleTracking Technologies represents a prominent participant in the Hospital Bed Management Systems Market and operates as a U.S.-based healthcare technology company that develops patient flow automation, capacity management software, and clinical operations solutions for hospitals.

The company focuses on data-driven workflow optimization and real-time visibility tools that enhance hospital resource utilization. Industry competitors continue to introduce advanced analytics platforms, expand digital health integrations, and strengthen hospital partnerships to improve patient flow management and support sustained market growth.

Top Key Players

- Epic Systems Corporation

- Cerner Corporation (Oracle Health)

- Allscripts Healthcare Solutions, Inc. (Alivio Health)

- McKesson Corporation

- Siemens Healthineers AG

- GE HealthCare

- Philips Healthcare

- Oracle Corporation

- Central Logic (LeanTaaS)

- TeleTracking Technologies, Inc.

- Awarepoint Corporation

- Stanley Healthcare

Recent Developments

- Entering 2026, Epic expanded the use of artificial intelligence across its electronic health record ecosystem, embedding a wide range of AI-enabled tools to support clinical workflows. Among these is an AI assistant that helps automate routine documentation tasks, allowing nurses to complete shift notes more efficiently and maintain more accurate, real-time bed management data.

- In early 2026, Oracle Health advanced its strategy around autonomous, task-oriented artificial intelligence within hospital operations. The company is developing tools to automate administrative processes, including bed allocation and identification of underutilized capacity, helping healthcare systems improve patient throughput in high-demand environments.

- At CES 2026, GE HealthCare announced a collaboration with NXP Semiconductors to integrate edge-based artificial intelligence into acute care settings. By processing patient data directly at the bedside, the technology enables immediate clinical insights, supporting faster decision-making around discharge readiness and overall bed utilization.

Report Scope

Report Features Description Market Value (2025) US$ 2.5 Billion Forecast Revenue (2035) US$ 5.9 Billion CAGR (2026-2035) 8.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Component (Software, Hardware and Services), By Deployment Mode (Cloud-based and On-premises), By Type (Real-Time Bed Tracking Systems, Patient Flow Management Systems, Bed Capacity Planning Systems and Integrated Bed Management Platforms), By Hospital Size (Small Hospitals, Medium-sized Hospitals and Large Hospitals), By End User (General Hospitals, Specialty Hospitals, Ambulatory Surgical Centers and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Epic Systems Corporation, Cerner Corporation, Allscripts Healthcare Solutions, Inc., McKesson Corporation, Siemens Healthineers AG, GE HealthCare, Philips Healthcare, Oracle Corporation, Central Logic, TeleTracking Technologies, Inc., Awarepoint Corporation, Stanley Healthcare. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Hospital Bed Management Systems MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Hospital Bed Management Systems MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Epic Systems Corporation

- Cerner Corporation (Oracle Health)

- Allscripts Healthcare Solutions, Inc. (Alivio Health)

- McKesson Corporation

- Siemens Healthineers AG

- GE HealthCare

- Philips Healthcare

- Oracle Corporation

- Central Logic (LeanTaaS)

- TeleTracking Technologies, Inc.

- Awarepoint Corporation

- Stanley Healthcare

Our Clients

- 183089

- March 2026