Quick Navigation

Report Overview

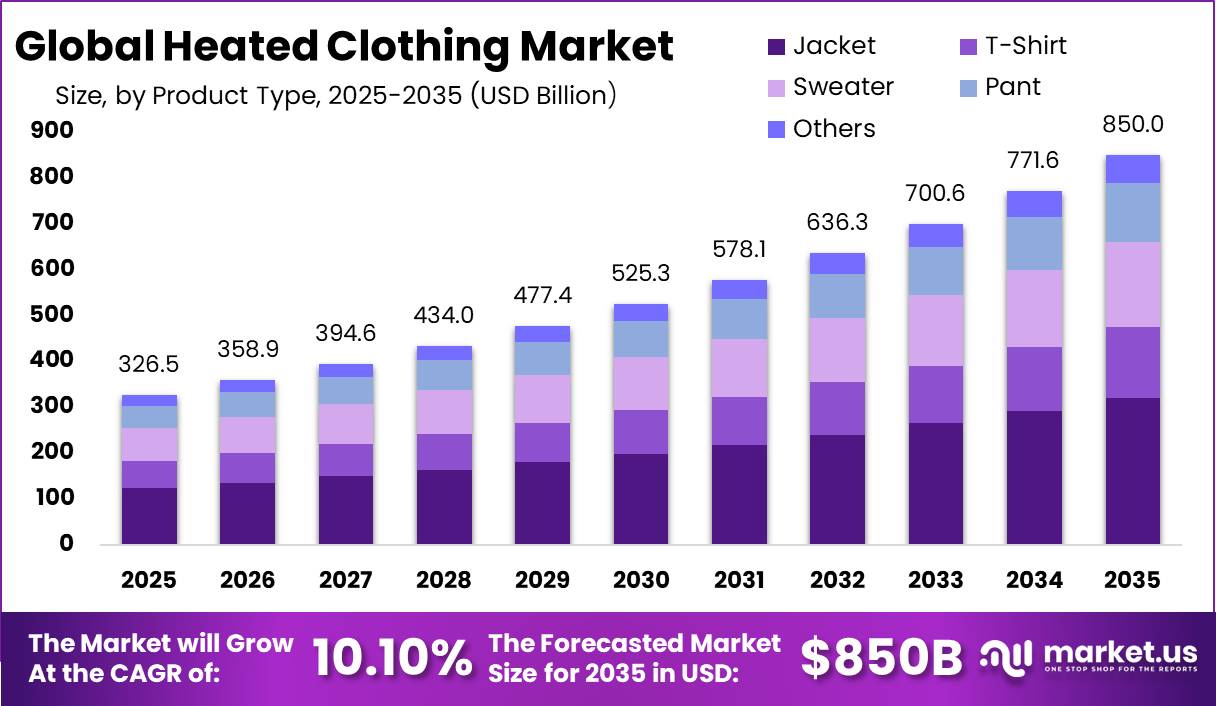

Global Heated Clothing Market size is expected to be worth around USD 850 Billion by 2035 from USD 171.739 Billion in 2025, growing at a CAGR of 10.10% during the forecast period 2026 to 2035.

The heated clothing market covers battery-powered and electrically heated garments worn to regulate body temperature in cold or extreme environments. This includes jackets, sweaters, pants, t-shirts, and other apparel categories. Products serve recreational, occupational, military, and therapeutic end-uses. The market spans direct-to-consumer retail, e-commerce, and business-to-business procurement channels.

Key Takeaways

- Global Heated Clothing Market was valued at USD 171.739 Billion in 2025 and is forecast to reach USD 850 Billion by 2035.

- The market is growing at a CAGR of 10.10% during the forecast period 2026 to 2035.

- By Product Type, Jacket dominates with a 37.80% share in 2025.

- By Power Rating, the 7–20 Volts segment holds the largest share at 44.90%.

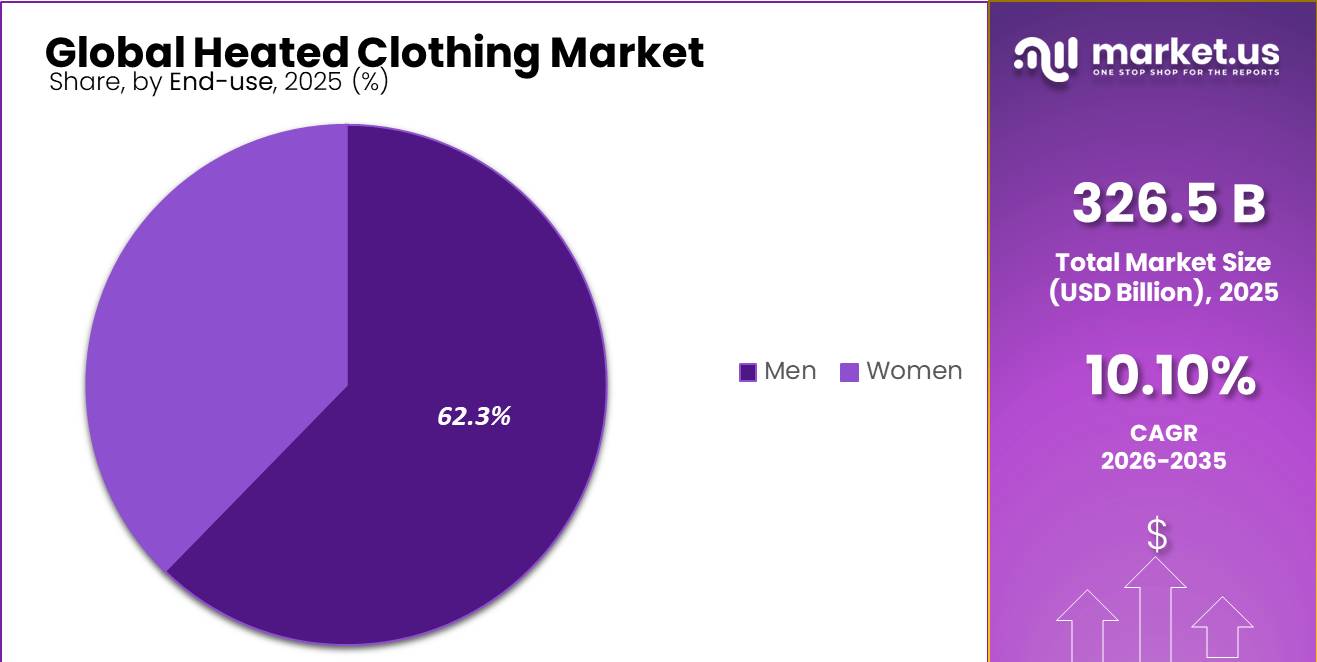

- By End-Use, Men account for the dominant share at 62.30%.

- North America leads all regions with a 52.60% market share.

Government and institutional data support the scale of this market’s addressable base. According to the Outdoor Industry Association, outdoor recreation participation in the United States reached 175.8 million people in 2023, representing 57.3% of the U.S. population aged 6 and older. This scale of participation creates a structural demand base that vendors cannot ignore when sizing product volume and retail distribution capacity.

Occupational exposure to outdoor conditions adds another demand layer. Data from the U.S. Bureau of Labor Statistics shows 33.0% of U.S. workers faced outdoor conditions regularly in 2023. This means heated workwear is not a niche purchase. Employers in construction, utility, and field service sectors face direct incentives to equip workers with performance protective apparel.

Product Type Analysis

Jacket dominates with 37.80% due to full-torso coverage and core body warming.

In 2025, Jacket held a dominant market position in the By Product Type segment of the Heated Clothing Market, with a 37.80% share. Jackets cover the torso and core, which is the most critical thermal zone for sustained outdoor performance. Buyers across recreational and workwear segments prioritize jackets first. This makes the jacket category the default entry point for new heated clothing purchasers, supporting premium pricing and repeat upgrade cycles.

Sweater holds a 22.00% share and serves as a mid-layer performance option for buyers seeking lighter heated solutions. The sweater segment attracts consumers who already own outerwear and want a versatile heated layer beneath it. This positions sweaters as an accessible entry product for first-time heated clothing buyers, and creates cross-sell opportunities for brands with jacket-first product lines.

T-Shirt accounts for 18.00% of the product type segment and targets base-layer buyers in workwear and athletic contexts. The U.S. National Park System recorded more than 331.8 million recreation visits in 2024, expanding the pool of outdoor participants who may layer heated base garments under standard outerwear. This volume signals strong unit potential for lower-priced heated base-layer products distributed through outdoor retail chains.

In February 2026, Adidas unveiled the CLIMAWARM SYSTEM heated pre-race jacket and trouser platform for winter sports athletes, integrating Clim8 smart heating technology to maintain muscle temperature before competition. This signals that performance-oriented heated base and mid-layer categories are moving toward mainstream sport brands, raising the competitive stakes for specialist heated clothing manufacturers.

Power Rating Analysis

7–20 Volts dominates with 44.90% due to extended battery runtime for full-day outdoor use.

In 2025, the 7–20 Volts segment held a dominant market position in the By Power Rating segment of the Heated Clothing Market, with a 44.90% share. Higher voltage systems deliver longer heating duration, which directly addresses the most common consumer complaint about heated clothing performance. Buyers in cold-environment occupations and winter sports choose higher-voltage systems to ensure consistent warmth across multi-hour sessions. This segment commands a pricing premium that supports stronger revenue margins for manufacturers.

The 5–7 Volts segment targets mid-range buyers who balance heat output with garment weight and battery portability. This voltage band suits recreational day users and commuters who need moderate heat for shorter durations. As USB-C power formats standardize across consumer electronics, 5–7 volt garments compatible with portable power banks will attract a broader consumer audience beyond dedicated heated clothing buyers.

The 3–5 Volts segment captures entry-level buyers and gift purchasers seeking lower-cost options with basic heat function. Products in this range often use USB power inputs and appeal to price-sensitive consumers. This sub-segment is a volume driver rather than a margin driver and supports market penetration in emerging regions where premium heated clothing pricing remains a barrier

End-Use Analysis

Men dominates with 62.30% due to higher outdoor occupational and recreational exposure rates.

In 2025, Men held a dominant market position in the By End-Use segment of the Heated Clothing Market, with a 62.30% share. Male consumers represent the largest share of outdoor recreation participants and cold-environment occupational workers. New motorcycle registrations in Europe’s five largest markets reached 1,155,640 units in 2024, a 10.1% increase from 2023. Male motorcyclists represent a core buyer group for heated riding jackets, gloves, and base layers, directly expanding this segment’s addressable volume.

Women account for 37.70% of the end-use segment, representing a structurally underserved growth area. Female participation in outdoor recreation, motorcycling, and cold-environment workplaces is rising across North America and Europe. Brands that invest in women-specific heated garment design, including fit, power pack placement, and style, have an opportunity to grow share in this segment ahead of competitors who continue treating it as secondary.

Key Market Segments

By Product Type

- Jacket

- T-Shirt

- Sweater

- Pant

- Others

By Power Rating

- 7–20 Volts

- 5–7 Volts

- 3–5 Volts

By End-Use

- Men

- Women

Drivers

The outdoor recreation economy generated USD 696.7 billion in value added and USD 1.3 trillion in gross output in 2024, supporting 5.2 million jobs across the United States. This scale confirms that heated clothing sits within one of the largest and most active consumer spending ecosystems in North America. Brands that position heated garments as performance tools for outdoor participation, rather than seasonal accessories, can access this full spending base.

As reported by the National Ski Areas Association, U.S. ski areas recorded 61.5 million skier visits in the 2024–25 season, the second-highest visitation level on record. This concentrated volume of cold-weather sports activity drives direct demand for heated jackets, base layers, and accessories. Vendors with retail presence in mountain resort towns and ski specialty channels hold a structural distribution advantage during peak winter months.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outdoor recreation spending and winter activity extension | +2.1% | North America core, EU alpine belt, Japan, South Korea, ANZ | Short term (≤ 2 years) |

| Industrial cold-exposure and utility/workwear adoption | +1.7% | North America core, Nordics, DACH, Canada, North Asia | Medium term (2-4 years) |

| Better batteries, USB power formats, and lighter heating systems | +1.5% | Global, with faster uptake in North America, EU, East Asia | Short term (≤ 2 years) |

| DTC e-commerce expansion and premium product mix | +1.3% | North America core, Western Europe, urban APAC | Short term (≤ 2 years) |

| Colder regional winter episodes and weather volatility | +1.0% | Northern U.S., Canada, Northern Europe, Northeast Asia | Medium term (2-4 years) |

| Compliance-led market formalization under GPSR and battery scrutiny | +0.8% | EU core, UK-linked sellers, North America spill-over | Medium term (2-4 years) |

Restraints

Tariff escalation creates a direct cost burden for heated clothing manufacturers because these products combine apparel construction with battery-powered electronics, drawing duties from multiple import categories simultaneously. Industry estimates indicate that a 12–18% increase in landed costs translates into 8–14% retail price inflation. This inflation forces manufacturers to choose between absorbing margin loss or passing higher costs to price-sensitive buyers, both of which slow purchasing volume.

Tariff uncertainty also suppresses brand investment in inventory expansion and channel development. Brands that cannot forecast landed costs accurately will reduce forward purchasing commitments, limiting shelf availability during peak winter selling windows. This dynamic is most acute in the U.S. market, which depends heavily on APAC-sourced heated garment production and component supply chains.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithium battery air-shipping limits | -1.4% | North America core, EU, cross-border APAC | Short term (≤ 2 years) |

| Safety incidents and recall risk | -1.2% | North America core, EU, Canada | Short term (≤ 2 years) |

| Tariff-led retail inflation | -1.6% | U.S. core, North America imports, APAC export corridors | Medium term (2-4 years) |

| Premium pricing vs casual demand | -1.1% | EU, North America, Japan, South Korea | Medium term (2-4 years) |

| New compliance and certification burden | -0.9% | India, EU, North America | Medium term (2-4 years) |

| Battery degradation and charging friction | -0.8% | Global, especially winter sports and workwear markets | Long term (≥ 4 years) |

Challenges

Current e-textile architectures face a critical durability gap that undermines consumer confidence in heated clothing products. Industry testing shows many e-textile systems begin experiencing electrical performance degradation within 10–50 wash cycles, far short of the 50–100 wash cycles consumers expect from premium apparel. Some surface-printed conductive materials deteriorate in as few as 1–5 wash cycles. This mismatch between performance and expectation drives returns, negative reviews, and reduced repeat purchasing.

Durability failures carry direct financial consequences for manufacturers. Warranty claim rates reach 6–9% of annual unit volume for products using less robust heating-element integration methods. Product development and certification timelines extend to approximately 18–24 months as a result. These costs limit how aggressively brands can invest in new product launches, channel expansion, and price reductions needed to broaden market access.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Li-ion Battery Supply Chain Concentration | -1.8% | North America, EU, APAC import-dependent markets | Long term (≥ 4 years) |

| E-Textile Washability & Durability Attrition | -1.4% | Global; most acute in North America & EU premium retail | Medium term (2–4 years) |

| Escalating Multi-Jurisdiction Regulatory Compliance | -1.1% | EU regulatory hubs, North America, Southeast Asia exports | Medium term (2–4 years) |

| Geopolitical Tariff-Driven Cost Inflation | -1.3% | North America core; APAC-to-US/EU logistics corridors | Short–Medium term (1–3 years) |

| Extreme Seasonality & Demand Volatility | -0.9% | Temperate-zone markets: North America, Northern/Central EU | Medium term (2–4 years) |

| Cross-Disciplinary Talent Deficit | -0.7% | North America, EU R&D clusters; nascent APAC smart-textile hubs | Long term (≥ 4 years) |

Opportunities

Circular economy regulation creates a structural design opportunity for heated clothing manufacturers, particularly in Europe. Emerging requirements around textile waste management, battery removability, and lifecycle transparency are reshaping product standards. Manufacturers who develop modular garments with user-replaceable batteries and recyclable textile materials will gain lower compliance costs and access to sustainability-driven procurement channels before competitors adapt.

Early movers in circular heated textile platforms can also capture a revenue premium from sustainability-conscious buyers. Figures from the provided data show that such products could command a 10–20% price premium in compliance-focused markets. Circular designs may also reduce end-of-life management and compliance costs by 10–15% compared with conventional products. This means sustainability investment pays back through both pricing power and operational savings.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Smart industrial heated PPE | +2.0% | North America, Europe, Northeast Asia | Medium term (2-4 years) |

| Defense and tactical systems integration | +1.5% | North America, Europe, Israel, East Asia | Medium term (2-4 years) |

| Subscription, rental and B2B service models | +1.2% | North America, Europe, APAC urban | Short term (≤ 2 years) |

| Outdoor sports and performance co-brands | +1.0% | North America, Europe, Japan, ANZ | Short term (≤ 2 years) |

| Healthcare, elder-care and rehab garments | +1.3% | Europe, Japan, North America, China coastal | Long term (≥ 4 years) |

| Sustainable, circular heated textiles platform | +0.8% | Europe, North America, Nordics, Japan | Long term (≥ 4 years) |

Regional Analysis

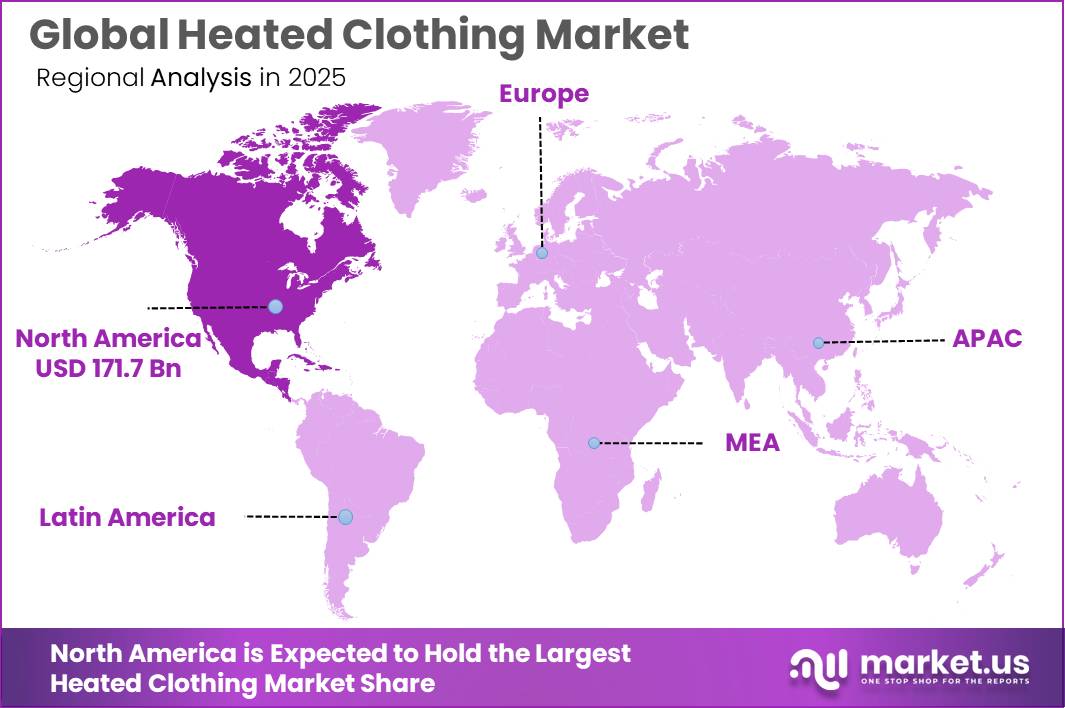

North America Dominates the Heated Clothing Market with a Market Share of 52.60%, Valued at USD 90.395 Billion

North America holds a 52.60% share of the global heated clothing market, driven by high outdoor recreation participation, large cold-environment workforces, and strong direct-to-consumer purchasing behavior. The U.S. ski industry recorded 61.5 million skier visits in the 2024–25 season, the second-highest visitation level on record. This volume of cold-weather recreational activity creates recurring seasonal demand for heated jackets, base layers, and accessories.

Europe is the second largest regional market, underpinned by strong winter sports cultures, occupational safety regulations, and growing motorcycling activity. Germany recorded 248,618 new motorcycle registrations in 2024, a 16.3% rise from 2023. As reported by the European Agency for Safety and Health at Work, outdoor workers are among the occupational groups most exposed to cold weather risks, creating regulatory incentive for employer procurement of heated workwear across the EU.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Company Insights

S&THONG operates as a specialist heated apparel brand with a product range spanning jackets, vests, and gloves positioned across mid-market price bands. Its competitive position rests on accessible pricing and broad online retail availability, which reduces distribution cost relative to physical retail-dependent competitors. However, brand differentiation in a market moving toward smart heating controls and premium materials remains a structural risk for the company.

Warmthru focuses on heated base layers and therapeutic apparel targeting users with circulatory conditions and chronic pain, a segment with limited direct competition from outdoor and workwear-focused brands. The U.S. Army’s Cold Weather Clothing System signals continued institutional demand for layered thermal protection technologies. Warmthru’s therapeutic positioning allows it to pursue healthcare and elder-care procurement channels that mainstream heated clothing brands have not yet prioritized, creating a defensible niche.

Key Players

- S&THONG

- Warmthru

- Milwaukee Tool

- Volt Resistance

- Warm & Safe

- Venture Heat

- EXO²

- Ravean

- Gerbing

- Blaze Wear

- Gears Canada

- ewool

Recent Developments

- July 2025 – ORORO launched the ZenFlow Power Cooling Jacket, its first cooling apparel product, expanding beyond heated clothing with a battery-powered wearable cooling solution for outdoor workers and recreational users.

- February 2026 – Adidas unveiled the CLIMAWARM SYSTEM heated pre-race jacket and trouser platform for winter sports athletes, integrating Clim8 smart heating technology to maintain muscle temperature before competition.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 171.739 Billion |

| Forecast Revenue (2035) | USD 850 Billion |

| CAGR (2026-2035) | 10.10% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Jacket, T-Shirt, Sweater, Pant, Others), By Power Rating (7–20 Volts, 5–7 Volts, 3–5 Volts), By End-Use (Men, Women) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | S&THONG, Warmthru, Milwaukee Tool, Volt Resistance, Warm & Safe, Venture Heat, EXO², Ravean, Gerbing, Blaze Wear, Gears Canada, ewool |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |