GPU Orchestration Platform Market By Component (Software, Hardware, Services), By Deployment Mode (On-Premises, Cloud-based), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By Application (AI and Machine Learning, High-Performance Computing, Other Applications), By End-User (BFSI, Healthcare, Other End-Users), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

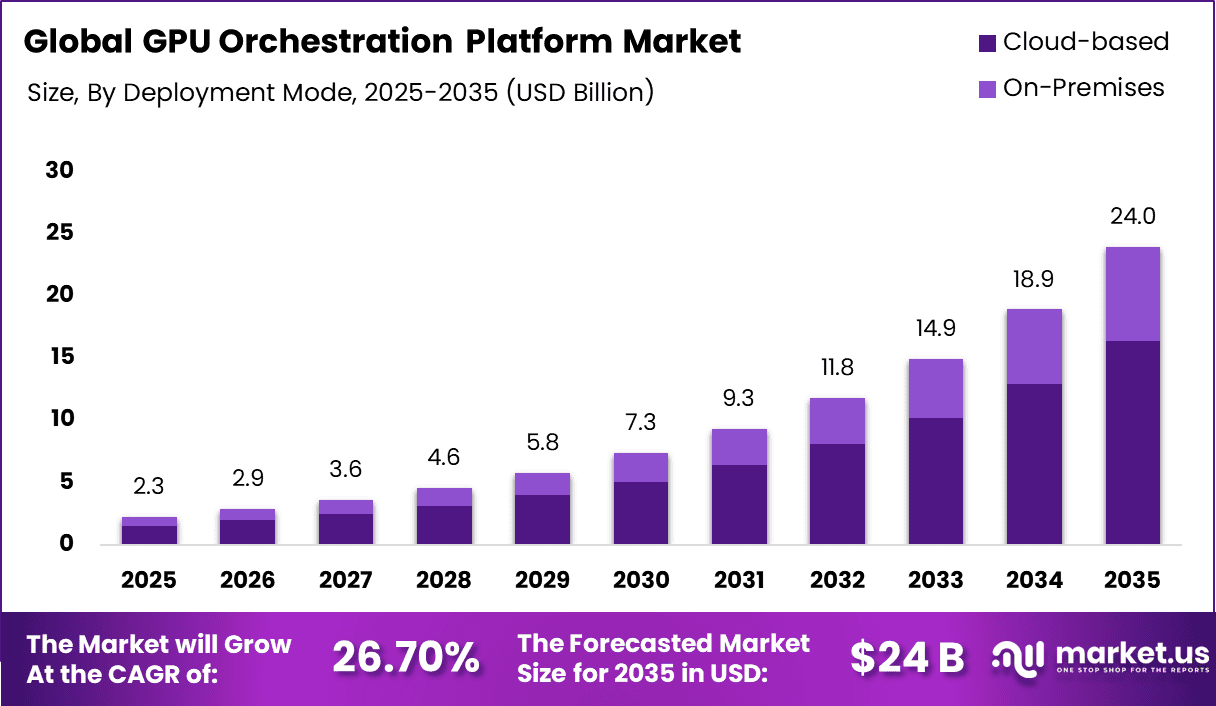

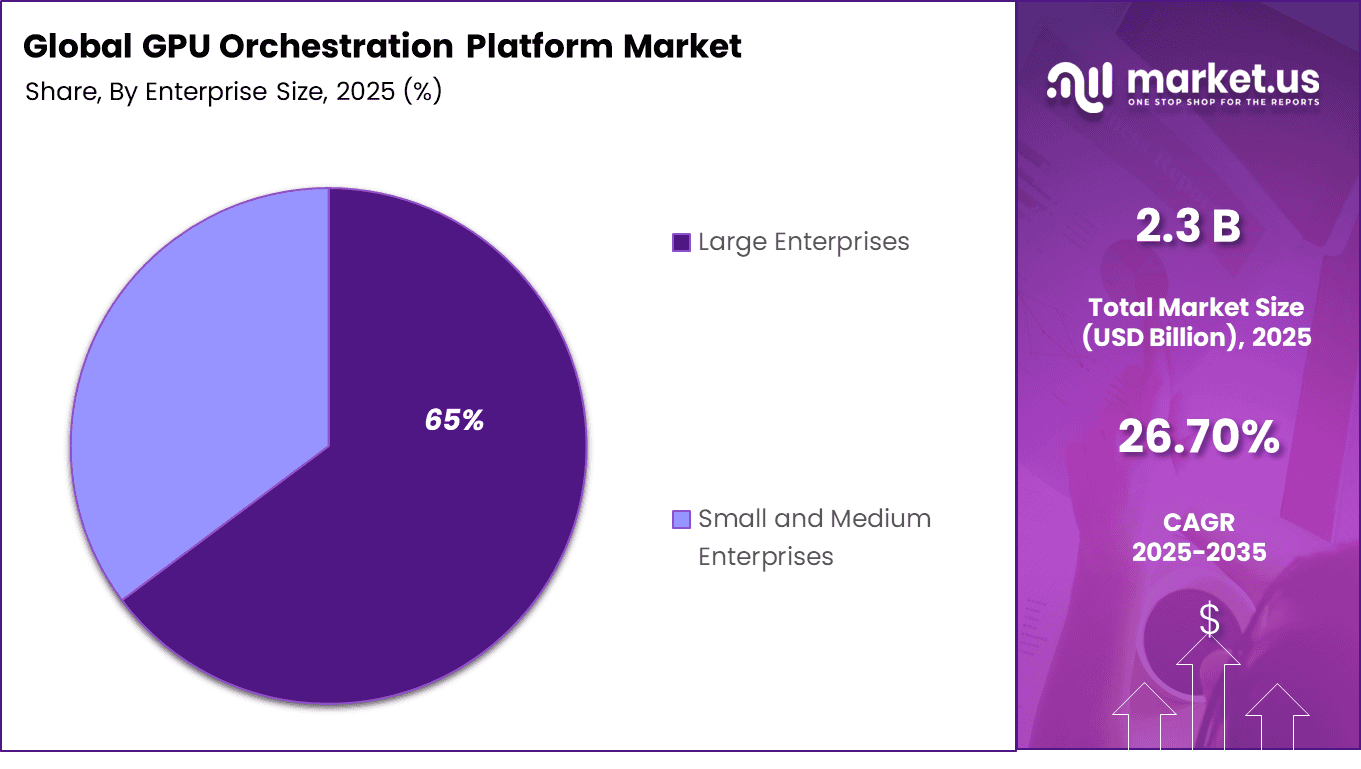

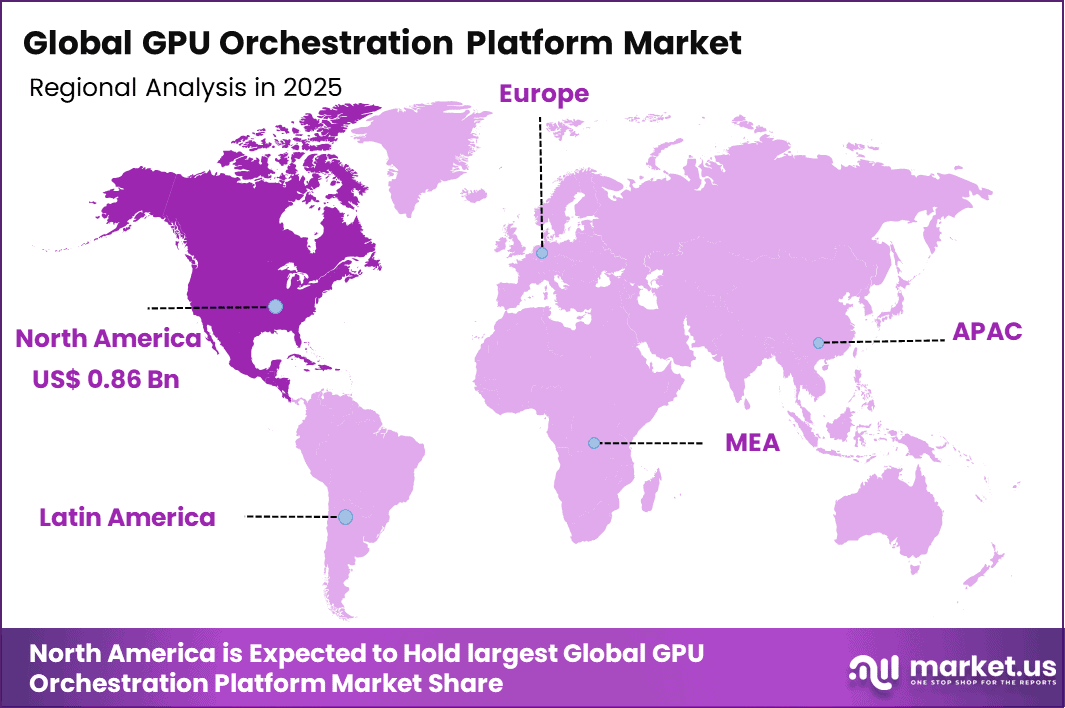

The Global GPU Orchestration Platform Market generated USD 2.3 billion in 2025 and is predicted to register growth from USD 2.9 billion in 2026 to about USD 24 billion by 2035, recording a CAGR of 26.70% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 38.3% share, holding USD 0.86 Billion revenue.

Top Market Takeaways

Software commands 54.2% market share, delivering dynamic workload scheduling, multi-GPU resource pooling, and containerized inference orchestration across hybrid environments.

Cloud-based deployment captures 68.5%, enabling elastic scaling, pay-per-GPU economics, and seamless integration with hyperscaler AI platforms like AWS SageMaker and Azure ML.

Large enterprises hold 64.8%, leveraging enterprise-grade platforms for training LLMs, distributed deep learning, and real-time inference at petabyte scale.

AI and machine learning applications claim 35.4%, powering transformer model training, computer vision pipelines, and recommendation engine optimization with automated hyperparameter tuning.

IT & telecom sectors represent 25.9%, deploying GPU orchestration for 5G RAN analytics, network anomaly detection, and telco cloud AI services.

North America drives 38.3% global value, with U.S. market at USD 0.78 billion and 24.8% CAGR, fueled by NVIDIA DGX clusters and hyperscaler GPU-as-a-Service expansions.

GPU orchestration platforms are becoming important as organizations scale their use of high performance computing for artificial intelligence, machine learning, and data intensive workloads. These platforms help manage and allocate GPU resources across multiple users, applications, and environments, ensuring efficient utilization and smooth workload execution.

As GPUs are expensive and limited resources, companies are focusing on systems that can schedule workloads, balance demand, and avoid idle capacity. This is making orchestration platforms a key layer in modern computing infrastructure, especially in cloud and hybrid environments.

One of the main driving factors is the rapid growth of artificial intelligence and deep learning workloads, which require large amounts of GPU power for training and inference. Organizations are increasingly running multiple models and experiments at the same time, creating the need for better resource coordination. In addition, the shift toward containerized and distributed computing environments is pushing the demand for platforms that can manage GPUs across clusters efficiently.

Companies are also aiming to reduce infrastructure costs by improving utilization rates, and orchestration tools help achieve this by allocating resources based on priority and workload needs. The increasing adoption of cloud based computing is further supporting this trend, as users require flexible and scalable GPU access.

Demand for GPU orchestration platforms is rising as enterprises look for ways to simplify complex computing environments. There is a strong need for solutions that can provide visibility into resource usage, automate workload scheduling, and support multiple users without performance conflicts. Organizations are also seeking platforms that can integrate with existing tools for data science, development, and operations.

The demand is particularly strong in sectors such as technology, healthcare, finance, and research, where large scale data processing and model development are common. As computing workloads continue to grow in complexity, the need for efficient and intelligent GPU management solutions is expected to increase steadily.

Drivers Impact Analysis

Key Driver

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

Rapid growth in AI and machine learning workloads

+5.6%

North America, China, Europe

Short to long term

AI demand drives GPU utilization

Increasing adoption of cloud-based GPU infrastructure

+5.1%

Global

Medium to long term

Cloud platforms enable scalable GPU access

Rising need for efficient GPU resource utilization

+4.4%

Global

Medium term

Orchestration improves workload efficiency

Expansion of data centers and hyperscale computing

+4.8%

US, China, Europe

Medium to long term

Data center growth supports GPU demand

Growth in high-performance computing applications

+3.9%

Developed markets

Medium to long term

HPC workloads require optimized GPU management

Restraints Impact Analysis

Key Restraint

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

High cost of GPU infrastructure and deployment

-4.2%

Emerging markets

Short to medium term

High costs limit adoption

Complexity in managing distributed GPU environments

-3.6%

Global

Medium term

Technical challenges slow deployment

Limited availability of skilled professionals

-2.9%

Global

Medium to long term

Skill gaps affect implementation

Vendor lock-in concerns in cloud ecosystems

-2.5%

North America and Europe

Medium term

Dependency risks reduce flexibility

Power consumption and cooling challenges

-2.2%

Global

Long term

High energy needs impact scalability

By Component Analysis

The software segment accounted for 54.2% of the market share, reflecting its critical role in managing and optimizing GPU resources across complex computing environments. This dominance is supported by the increasing need for platforms that can allocate workloads efficiently, monitor performance, and ensure maximum utilization of GPU infrastructure. Software solutions enable better control over distributed systems, helping organizations improve processing efficiency and reduce idle capacity.

Another factor driving this segment is the growing complexity of high-performance computing workloads, which require advanced orchestration tools. These platforms allow seamless integration with existing systems and support dynamic workload scheduling, making them essential for organizations handling intensive computing tasks across multiple environments.

By Deployment Mode Analysis

The cloud-based segment held 68.5% share, driven by the rising adoption of scalable and flexible computing infrastructure. Cloud deployment allows organizations to access GPU resources on demand without investing heavily in physical hardware. This approach supports faster deployment, easier scalability, and remote accessibility, which are becoming increasingly important for modern workloads.

In addition, cloud-based platforms enable better collaboration and centralized management of resources across different locations. Organizations prefer cloud solutions as they simplify infrastructure management and support rapid expansion based on workload requirements. This flexibility has made cloud deployment the preferred choice for GPU orchestration.

By Enterprise Size Analysis

The large enterprises segment captured 65% of the market, reflecting their strong demand for advanced computing capabilities and resource management tools. These organizations operate large-scale data environments and require efficient orchestration to handle complex workloads. GPU orchestration platforms help them optimize performance and maintain operational efficiency across multiple departments.

Moreover, large enterprises have the financial and technical capacity to adopt sophisticated platforms that offer automation, monitoring, and integration features. Their focus on improving productivity and reducing operational inefficiencies has led to higher adoption of GPU orchestration solutions, especially in data-intensive industries.

By Application Analysis

The AI and machine learning segment held 35.4% share, driven by the increasing use of GPU-intensive workloads in training and deploying advanced models. These applications require high computational power and efficient resource allocation, which makes orchestration platforms essential. The ability to manage multiple workloads and ensure optimal GPU usage supports faster processing and improved outcomes.

Additionally, the growing adoption of intelligent systems across industries has increased the demand for scalable and efficient computing solutions. GPU orchestration platforms enable better workload distribution and reduce processing delays, which is crucial for maintaining performance in AI and machine learning applications.

By End-User Analysis

The IT and telecom segment accounted for 25.9% of the market share, driven by the need to manage large-scale data processing and network operations. Organizations in this sector rely on GPU orchestration platforms to handle complex workloads, support data analytics, and improve service delivery. Efficient resource management is essential for maintaining performance and ensuring seamless operations.

Furthermore, the increasing demand for high-speed connectivity and data-driven services has encouraged IT and telecom companies to invest in advanced computing infrastructure. GPU orchestration platforms help them optimize resource usage, reduce operational complexity, and enhance overall system performance, supporting continued growth in this segment.

Investor Type Impact Analysis

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture capital firms

Very high

High

US, China

Investing in AI infrastructure startups

Private equity firms

High

Moderate

North America and Europe

Scaling GPU and cloud infrastructure providers

Corporate investors

Very high

Moderate

Global

Strategic investments in AI and cloud ecosystems

Institutional investors

Moderate to high

Moderate

Developed markets

Focus on established tech and semiconductor firms

Government and public funding bodies

High

Low

US, EU, Asia Pacific

Supporting AI infrastructure and computing capacity expansion

Technology Enablement Analysis

Technology

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

Kubernetes-based GPU orchestration

+5.3%

Global

Medium to long term

Enables efficient containerized GPU management

AI-driven workload scheduling

+4.7%

US, Europe, China

Medium term

Optimizes GPU allocation dynamically

Multi-cloud and hybrid cloud orchestration

+4.2%

Global

Medium to long term

Enhances flexibility across environments

GPU virtualization and partitioning technologies

+3.8%

Developed markets

Medium term

Improves resource sharing efficiency

Edge AI and distributed computing integration

+3.5%

Global

Long term

Expands GPU usage beyond centralized data centers

Key Challenges

High cost of GPU infrastructure makes it expensive for many organizations to adopt.

Complex setup and configuration require skilled technical teams.

Difficulty in managing workloads across multiple GPUs and environments.

Integration challenges with existing IT systems and cloud platforms.

Limited availability of skilled professionals for GPU management and optimization.

Performance issues due to improper resource allocation and scheduling.

Data security and privacy concerns in shared or cloud environments.

Lack of standardization across different platforms and vendors.

High energy consumption increases operational costs.

Dependence on continuous updates and maintenance for smooth operations.

Emerging Trends

The GPU orchestration platform market is moving toward more intelligent and flexible resource management as demand for high performance computing continues to rise. One of the key emerging trends is the shift toward automated workload scheduling that dynamically allocates GPU resources based on real time demand and priority levels. This helps organizations maximize utilization and avoid idle capacity. Another important trend is the integration of orchestration platforms with containerization and cloud native environments, allowing seamless deployment of AI and data intensive workloads across distributed systems.

There is also growing focus on multi tenant environments where multiple users or teams can share GPU infrastructure securely without performance conflicts. In addition, platforms are increasingly offering visibility tools that provide detailed insights into GPU usage, workload performance, and bottlenecks, helping teams optimize operations more effectively. Edge computing is also influencing this market, as orchestration capabilities are being extended beyond centralized data centers to support real time processing closer to data sources.

Growth Factors

The growth of this market is driven by the rapid expansion of AI, machine learning, and data analytics applications that require significant computing power. Organizations are looking for efficient ways to manage GPU infrastructure without overinvesting in hardware, which is increasing the need for orchestration solutions. The growing complexity of workloads and the need to scale computing resources quickly are also supporting adoption, especially in environments where demand fluctuates frequently.

Another major factor is the rising importance of cost optimization, as GPU resources are expensive and require careful allocation to ensure maximum return on investment. Enterprises are also focusing on improving productivity by reducing manual intervention in resource management, which is pushing the use of automated orchestration platforms. Furthermore, the increasing use of hybrid and multi cloud strategies is creating a need for unified platforms that can manage GPU resources across different environments, ensuring consistent performance and operational efficiency.

Key Market Segments

By Component

Software

Hardware

Services

By Deployment Mode

On-Premises

Cloud-based

By Enterprise Size

Small and Medium Enterprises

Large Enterprises

By Application

AI and Machine Learning

High-Performance Computing

Data Analytics

Graphics Rendering

Other Applications

By End-User

BFSI

Healthcare

IT and Telecommunications

Media and Entertainment

Automotive

Manufacturing

Other End-Users

Regional Analysis

North America accounted for 38.3% of the GPU Orchestration Platform market, supported by strong demand for high-performance computing and rapid adoption of artificial intelligence workloads. The region has a well-established cloud ecosystem and advanced data center infrastructure, which enables efficient deployment and scaling of GPU resources.

Enterprises are increasingly using orchestration platforms to manage complex GPU workloads across hybrid and multi-cloud environments, improving utilization and reducing operational inefficiencies. The growing need for faster model training, real-time analytics, and large-scale data processing has further strengthened the adoption of GPU orchestration solutions across industries such as technology, healthcare, and finance.

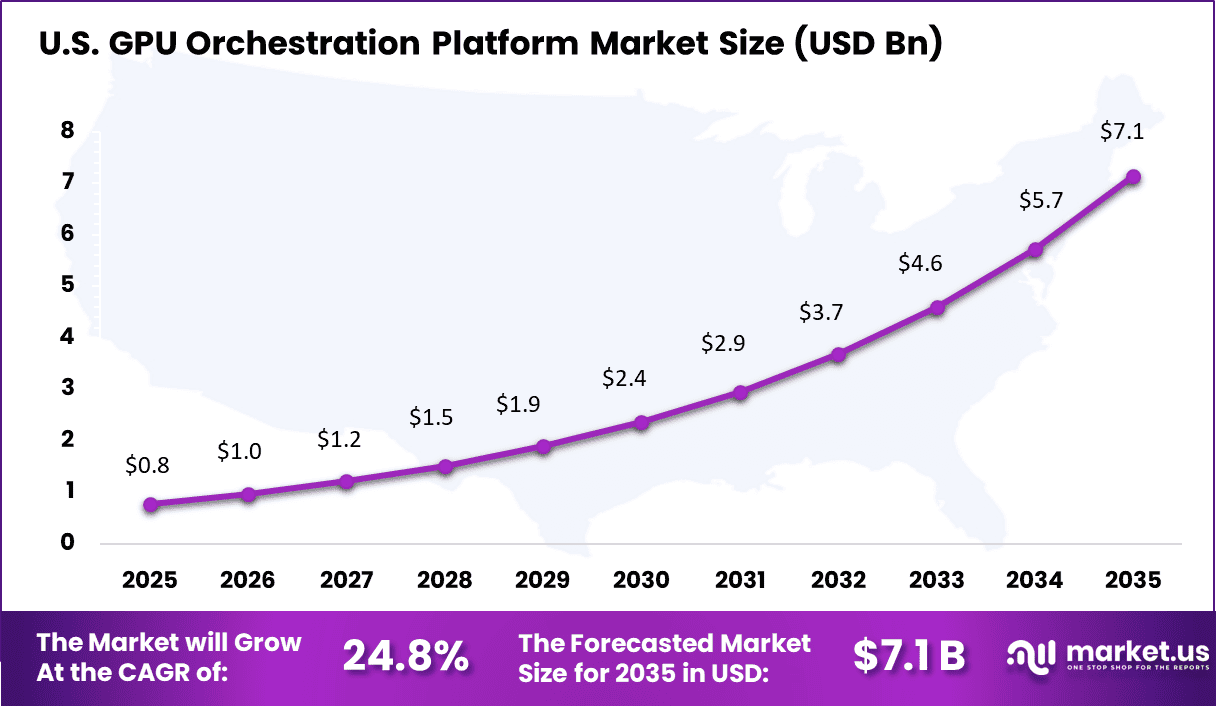

The U.S. market reached USD 0.78 Billion and is projected to grow at a CAGR of 24.8%, driven by expanding investments in AI, machine learning, and deep learning applications. Organizations are focusing on optimizing GPU usage to handle increasing computational demands while controlling infrastructure costs.

The rise of generative AI, autonomous systems, and advanced simulation workloads is encouraging companies to adopt orchestration platforms that provide better workload scheduling and resource allocation. In addition, strong presence of hyperscale data centers and continuous innovation in cloud-based GPU services are expected to support sustained growth in the US market over the coming years.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The competitive landscape of the GPU Orchestration Platform Market is developing quickly, supported by strong participation from global cloud providers and AI infrastructure companies. Organizations such as Amazon Web Services Inc., Alibaba Group Holding Ltd, IBM Corporation, Hewlett Packard Enterprise Company, and Red Hat Inc. focus on integrating GPU orchestration into their cloud and hybrid platforms.

These players provide scalable environments for AI and machine learning workloads, with emphasis on automation, container-based deployment, and enterprise-level security. NVIDIA Corporation also holds a strong position by offering software that improves GPU utilization and enables efficient workload management across distributed systems.

At the same time, emerging players such as CoreWeave Inc., Crusoe Cloud Inc., RunPod Inc., Vast AI Inc., and DigitalOcean LLC are gaining attention by offering GPU-focused cloud platforms designed for high-performance computing needs. These companies focus on flexible infrastructure, faster deployment, and cost efficiency for AI workloads.

In addition, firms like Rafay Systems Inc., Anyscale Inc., OctoML Inc., Modal Labs Inc., Exostellar Inc., and Civo Limited are building developer-friendly orchestration tools that simplify scaling and workload optimization. Competition in this market is driven by innovation in GPU resource management, ease of integration, and the ability to support large-scale AI applications efficiently.

The future outlook for the GPU Orchestration Platform Market looks very strong as demand for AI, machine learning, and high-performance computing continues to rise across industries. Companies are expected to increasingly rely on these platforms to manage complex GPU workloads, improve resource utilization, and reduce operational costs. The shift toward cloud-based and GPU-as-a-service models is also anticipated to make advanced computing more accessible and scalable for businesses of all sizes.

Recent Developments

March, 2026 – Alibaba Cloud PAI adds GPU cluster federation across APAC regions and auto-scales Llama3 training. Serves e-commerce AI with cost-per-token billing model. Tongyi Qianwen integration boosts regional LLMs.

February, 2026 – AWS ParallelCluster 3.8 boosts multi-region GPU bursting and EC2 P5 instances with InfiniBand. Trainium2 integration with SageMaker Pipelines native support. Project Amelia agentic orchestration live.

Report Scope

Report Features

Description

Market Value (2025)

USD 2.3 Billion

Forecast Revenue (2035)

USD 24 Billion

CAGR(2025-2035)

26.70%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2025-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Component (Software, Hardware, Services), By Deployment Mode (On-Premises, Cloud-based), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By Application (AI and Machine Learning, High-Performance Computing, Other Applications), By End-User (BFSI, Healthcare, Other End-Users)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA

Competitive Landscape

Alibaba Group Holding Ltd, Amazon Web Services Inc., IBM Corporation, NVIDIA Corporation, Hewlett Packard Enterprise Company, Red Hat Inc., Scale AI Inc., DigitalOcean LLC, CoreWeave Inc., Crusoe Cloud Inc., RunPod Inc., Rafay Systems Inc., Anyscale Inc., OctoML Inc., Modal Labs Inc., Exostellar Inc., Vast AI Inc., Civo Limited, Others

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Purchase Options

We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)