Quick Navigation

Report Overview

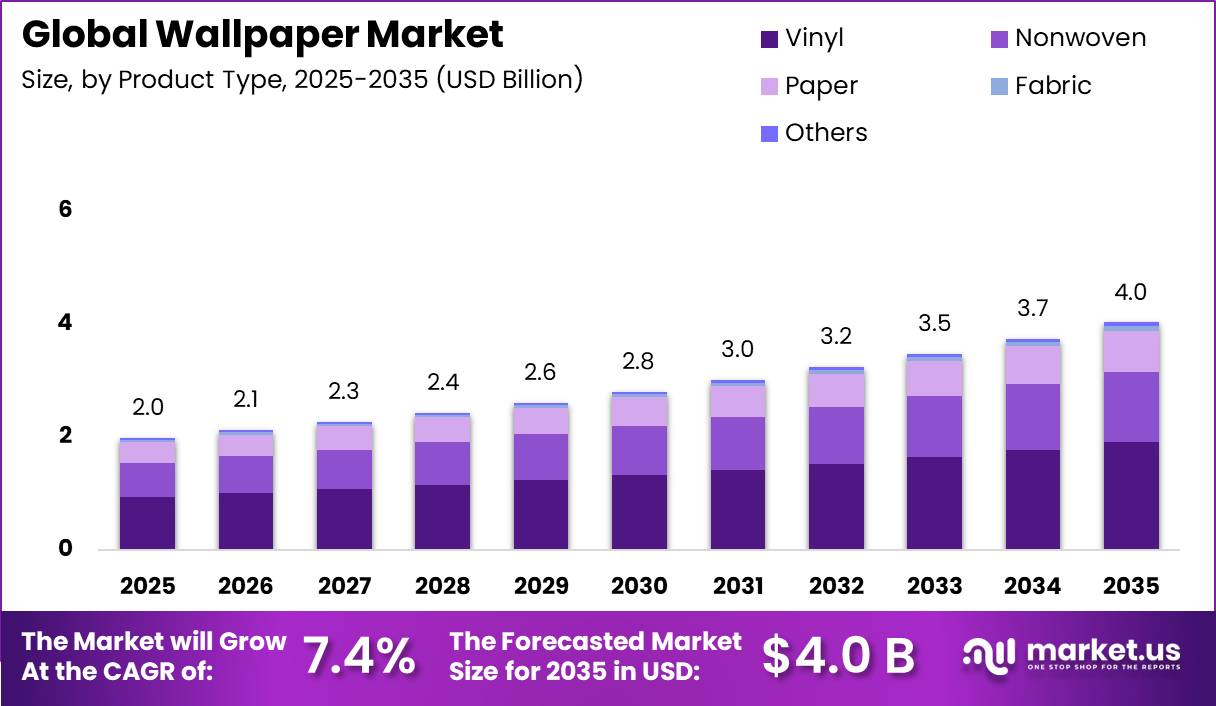

Global Wallpaper Market size is expected to be worth around USD 4.0 Billion by 2035 from USD 2.0 Billion in 2025, growing at a CAGR of 7.40% during the forecast period 2026 to 2035. This trajectory signals a market that doubles in value within a decade, making timing of entry and segment selection critical for investors.

The wallpaper market covers decorative and functional wall coverings sold across residential and commercial end-use channels. Products span nonwoven, vinyl, paper, fabric, and other substrate types. Demand flows through interior designers, contractors, retail chains, and e-commerce platforms. This structural diversity creates both fragmentation risks and consolidation opportunities for participants at every level of the value chain.

Key Takeaways

- Global Wallpaper Market was valued at USD 2.0 Billion in 2025.

- The market is forecast to reach USD 4.0 Billion by 2035.

- The market will grow at a CAGR of 7.40% from 2026 to 2035.

- By Product, Nonwoven is the dominant sub-segment.

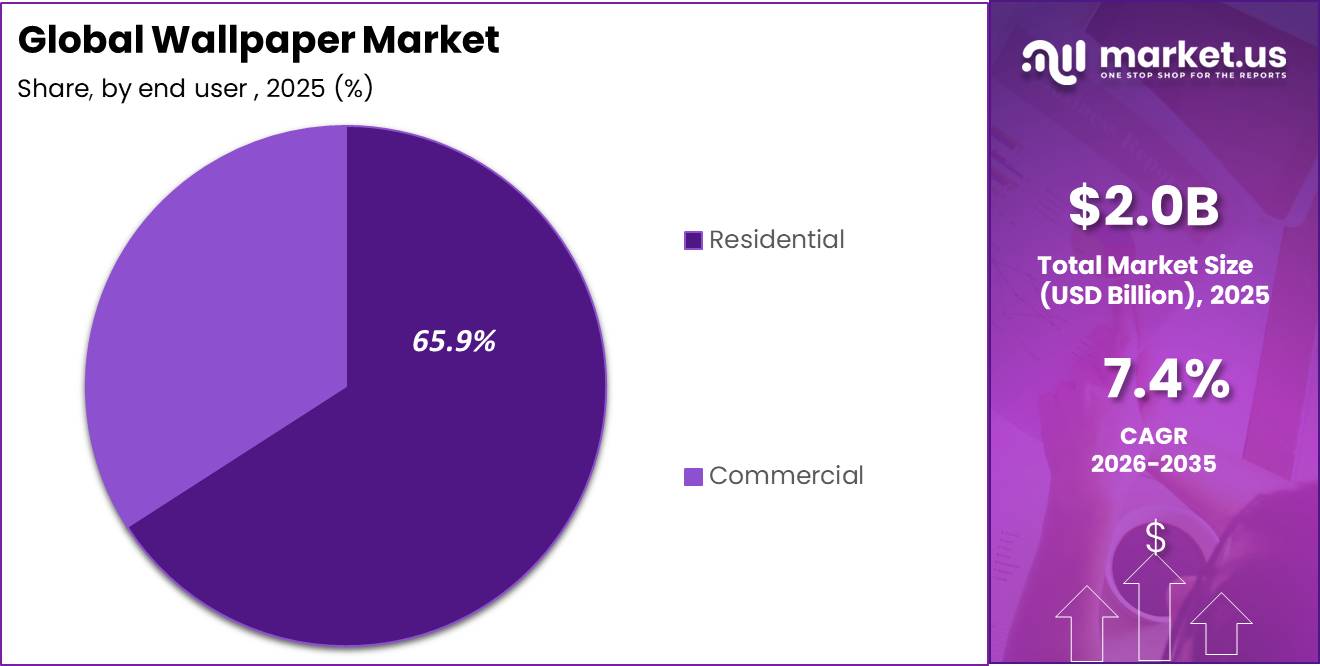

- By End Use, Residential holds the dominant position.

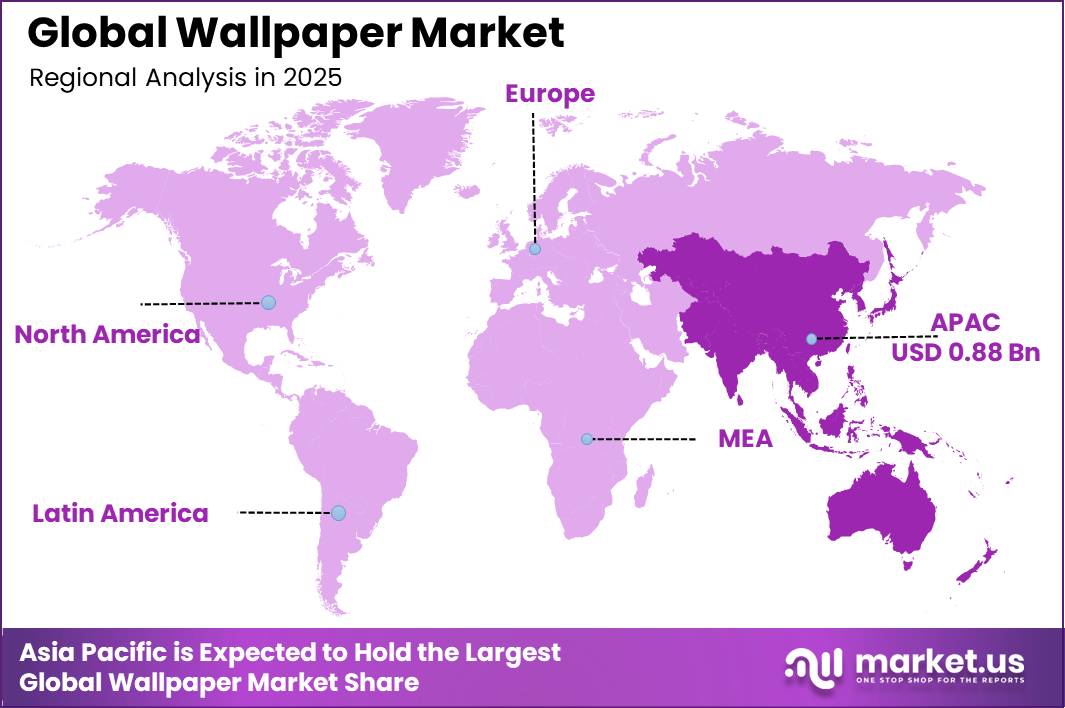

- Asia-Pacific is the dominant region with a 44.6% market share, valued at USD 0.88 Billion in 2025.

Houzz surveyed more than 1,700 U.S. and Canadian homeowners on decorating behavior, providing measurable evidence of recurring renovation cycles. This scale of data validates the frequency of wallpaper replacement demand as a structural feature rather than a cyclical anomaly. Vendors who build for repeat purchasers will outperform those targeting first-time buyers only.

Data from the Architectural Digest consumer survey shows 71% of Americans planned to redecorate their homes in the year following the survey. This signals a pipeline of wall-surface upgrade activity that extends well beyond a single season. Brands that maintain consistent product refresh cycles will capture a larger share of this active, recurring buyer base. In January 2025, Antalis launched its new ID Wallcovering range, adding five customizable wallcovering finishes sourced from European suppliers, demonstrating how established distributors are responding to this sustained consumer demand.

As per surveyed more than 1,200 homeowners on behalf of Sherwin-Williams regarding home improvement and wall-finishing preferences. This dataset highlights that wall-surface decisions extend beyond paint into adjacent categories like wallpaper. Brands that position wallpaper alongside paint as an interior finishing alternative can capture budget share from homeowners already committed to renovation spending.

Product Analysis

Nonwoven dominates with the leading share due to durability, ease of installation, and sustainability credentials.

In 2025, Nonwoven held a dominant market position in the By Product segment of the Wallpaper Market, with the leading share. Nonwoven wallpapers offer tear resistance, dimensional stability, and compatibility with low-VOC adhesives, making them the preferred choice for both professional installers and DIY consumers. This performance profile positions nonwoven as the default substrate for brands targeting renovation-active homeowner segments.

Vinyl wallpapers maintain strong demand in commercial applications due to their durability, moisture resistance, and ease of cleaning. Hotels, healthcare facilities, and retail environments favor vinyl for high-traffic wall surfaces where longevity outweighs aesthetic flexibility. This commercial dependency creates stable baseline volume but limits vinyl’s growth ceiling as sustainability regulations tighten across EU markets.

Paper wallpapers serve a distinct premium and heritage design segment, particularly in European residential markets where traditional aesthetics command higher price points. According to Houzz data, 56% of homeowners planned wall-surface renovation activity within 12 months, indicating an active buyer pool that paper wallpaper suppliers can address with curated, trend-led collections. In February 2026, WallPops launched the Morris & Co. x WallPops Collection, introducing eight iconic archive designs as peel-and-stick products, directly targeting this heritage-conscious residential segment.

End Use Analysis

Residential dominates with the leading share due to frequent home décor refresh cycles and rising interior renovation activity.

In 2025, Residential held a dominant market position in the By End Use segment of the Wallpaper Market, with the leading share. Figures from the NY Post renovation survey show 59% of planned renovation projects in 2025 focused on interior upgrades rather than exterior work, directing a majority of renovation spend toward wall-surface categories. This structural interior bias reinforces residential as the primary demand engine for wallpaper suppliers and distributors.

Commercial end use captures demand from hospitality, retail, healthcare, and corporate interior segments. Sherwin-Williams data indicates 74% of millennial homeowners planned interior painting projects within one year, reflecting broader generational investment in interior surfaces. As this cohort ages into higher income brackets, their spending on premium commercial and residential interior products will expand, creating long-term volume growth for wallpaper brands positioned in the mid-to-premium tier.

Key Market Segments

By Product

- Nonwoven

- Vinyl

- Paper

- Fabric

- Others

By End Use

- Residential

- Commercial

Drivers

EU Eco-Design and VOC compliance mandates are accelerating the shift toward sustainable wallpaper substrates across European markets. The EU’s Ecodesign for Sustainable Products Regulation came into force in 2024, establishing product durability, recyclability, and lower environmental impact as baseline compliance requirements. Manufacturers that align product portfolios with these standards now will gain first-mover advantage as enforcement tightens through the decade.

As reported by Houzz survey data, 66% of homeowners had recently decorated the same room they were currently decorating again, confirming that wallpaper replacement demand is a recurring event rather than a one-time purchase decision. This repeat-purchase behavior compresses the typical sales cycle and creates predictable reorder volume for brands with strong loyalty programs and consistent product availability. By 2025, sustainable wallpapers with recycled fiber content had reached 28% penetration in EU retail channels, showing that eco-certified products are no longer a niche offering but a mainstream demand category.

Houzz data also shows 21% of homeowners redecorated a room within just two years of a previous project, and 45% did so within five years. These compressed refresh cycles increase annual addressable demand beyond what single-purchase models predict. Suppliers who build replenishment-ready distribution and sampling programs will convert these repeat-cycle buyers at higher rates than competitors relying on one-time transaction models.

NY Post renovation survey data shows 43% of U.S. homeowners completed renovation projects in 2025, with 32% already planning projects for 2026, and 65% expecting 2026 to be their biggest renovation year yet. This pipeline of committed renovation activity translates directly into wall-surface upgrade demand. Public-sector procurement in Europe adds further institutional volume, with environmental criteria accounting for 20 to 30% of tender evaluation scores across school, hospital, and government building projects.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential Renovation & Remodeling Boom Fueled by Mid-Income Urbanization | +1.2% | APAC core (India, Vietnam, Indonesia), North America spill-over | Long term (≥ 4 years) |

| Digital Printing & On-Demand Customization Reshaping Make-to-Order Economics | +1.0% | North America, Western Europe, APAC corridors | Medium term (2–4 years) |

| Biophilic & Nature-Inspired Interior Design Creating Premium SKU Pull | +0.8% | North America, EU, GCC, emerging APAC | Medium term (2–4 years) |

| E-Commerce AR Visualization Tools Reducing Purchase Friction & Returns | +0.6% | North America, EU, East Asia | Short term (≤ 2 years) |

| Hospitality Construction & Refresh Cycles Driving Commercial Wallcovering Demand | +0.7% | GCC, ASEAN, North America | Medium term (2–4 years) |

| EU Eco-Design & VOC Compliance Mandates Accelerating Sustainable Substrate Adoption | +0.5% | European Union primary; North America & APAC regulatory spill-over | Long term (≥ 4 years) |

Restraints

Trade tensions and elevated tariff regimes continue to disrupt procurement cycles for wallpaper manufacturers reliant on Chinese sourcing. U.S. imports from China declined by 28% in 2025 and remain approximately 40% below pre-2018 levels, reflecting the sustained impact of trade restrictions and supply chain restructuring on the broader interior finishes category. This persistent sourcing disruption forces distributors to either absorb margin compression or pass cost increases to end consumers.

As per our research many Chinese imports now carry a cumulative tariff burden of approximately 55%, increasing landed costs for imported wallpaper substrates, PVC films, and specialty adhesives. These higher costs have extended lead times and reduced product variety in cost-sensitive segments. Houzz data shows 84% of homeowners base decorating decisions on personal taste rather than price trends, but sustained cost increases will eventually constrain purchase frequency among mid-income buyers who dominate the residential segment.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material (Vinyl/PVC) Cost Volatility | -1.2% | Global; APAC, North America core | Short term (≤ 2 years) |

| Regulatory Compliance Burden (EU REACH / EN 15102 / Formaldehyde Limits) | -0.9% | EU, UK; spillover to APAC exporters | Medium term (2–4 years) |

| Substitution Threat from Alternative Wall Coverings | -0.8% | EU, North America, APAC corridors | Long term (≥ 4 years) |

| Trade Tariff Escalation & Supply Chain Disruption | -0.7% | North America, EU (China-sourced goods) | Short term (≤ 2 years) |

| Skilled Labor Shortage in Installation Trades | -0.6% | North America, EU, India | Medium term (2–4 years) |

| Cyclical Housing Market Sensitivity | -0.5% | EU, North America, China | Medium term (2–4 years) |

Challenges

The shift toward omnichannel purchasing has created significant operational friction for wallpaper manufacturers and distributors managing simultaneous e-commerce, showroom, and marketplace channels. Our research indicates 79% of logistics decision-makers cite documentation burdens, 76% report administrative workload challenges, and 70% experience customs clearance delays in cross-border wallpaper trade. These friction points increase cost per order and compress delivery timelines that consumers now treat as a baseline expectation.

Wallpaper products present unique last-mile challenges due to bulky dimensions, transit damage risk, and the requirement for same-batch fulfillment to maintain pattern consistency. Return rates for damaged or incorrectly ordered wallpaper rolls in online channels are estimated at 18 to 24%, exceeding typical home décor category benchmarks. Only 15% of homeowners prioritize following the latest design trends, meaning return drivers are more likely operational than aesthetic, making logistics investment the more productive intervention.

Maintaining competitive omnichannel capabilities requires annual technology investment of USD 200,000 to USD 600,000 per business unit. This cost threshold excludes most small and mid-sized market participants from offering unified inventory systems and augmented reality visualization tools that reduce purchase friction and returns. This creates a structural bifurcation in the market where well-capitalized brands extend their distribution advantage while smaller players lose share to platform-native competitors.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| PVC/Vinyl Raw Material Price Volatility | -0.9% | Global; acute in EU, South Asia, APAC import corridors | Medium term (2–4 years) |

| Escalating Regulatory & VOC Compliance Burden | -0.7% | EU regulatory hubs; APAC export corridors; North America tier-1 markets | Long term (≥ 4 years) |

| Skilled Installer Workforce Attrition | -0.6% | North America core; EU construction markets; Tier-1 APAC urban centres | Long term (≥ 4 years) |

| Digital Printing Adoption Gap Among SME Manufacturers | -0.8% | APAC SME clusters (India, Vietnam, Indonesia); LATAM; Middle East | Medium term (2–4 years) |

| Omnichannel Distribution Complexity & Last-Mile Friction | -0.5% | North America e-commerce hubs; EU retail corridors; South & Southeast Asia | Short–Medium term (≤ 3 years) |

| Consumer Education Deficit & Paint Substitution Pressure | -0.6% | Emerging markets (India, SEA, Africa); cost-sensitive North American & European segments | Long term (≥ 4 years) |

Opportunities

The EU’s proposed Circular Economy Act, targeted for adoption by end of 2026, will strengthen sustainability requirements in public-sector purchasing across government buildings, schools, and hospitals. European innovation funding allocated EUR 101 Million to circular economy and bioeconomy initiatives in 2026, directly reducing certification and product development costs for compliant manufacturers. This regulatory tailwind concentrates contract value among a small pool of early-certified suppliers.

As reported by the Opportunities data, in regulatory-driven procurement markets, 30 to 50% of contract value concentrates among the small number of vendors that achieve compliance ahead of implementation deadlines. This winner-take-most dynamic rewards early investment in bio-based material certification, Digital Product Passport compliance, and recyclability credentials. Houzz data shows 75% of homeowners say comfort influences their decorating decisions, reinforcing that functional product attributes create genuine pull demand beyond purely aesthetic motivations.

Peer influence in home décor is measurably strong, with 27% of homeowners reporting inspiration from neighbors’ home improvement projects and 23% noticing neighbors copying their own projects. This social contagion effect in residential decorating shortens adoption cycles for new wallpaper designs. Brands that seed aspirational product launches through design-forward communities and real-home showcases can accelerate organic discovery without relying solely on paid acquisition.

Consumer motivation data shows 28% of homeowners redecorate to create a sense of luxury, signaling that premium and textured wallpaper collections address a distinct emotional purchase driver. This motivation segment is value-insensitive relative to average buyers, making it the most defensible margin pool for premium brands. The DACH region, Nordic countries, and Benelux markets are positioned as the primary EU adoption centers given their advanced sustainability procurement frameworks.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| AI-Powered Generative Design + DTC Print-on-Demand Platform | +1.8% | North America, Western Europe, APAC (urban) | Short term (≤ 2 years) |

| Peel-and-Stick / Subscription “Décor-as-a-Service” for Rental Housing | +1.5% | North America, Western Europe, APAC metro clusters | Short term (≤ 2 years) |

| Antimicrobial & Functional Wallcovering Vertical in Healthcare & Hospitality | +1.2% | North America, EU, GCC (Saudi, UAE) | Medium term (2–4 years) |

| ASEAN Urbanisation TAM Capture via Affordable Digital-Print Local Manufacturing | +1.4% | Southeast Asia (Indonesia, Vietnam, Philippines, Thailand) | Medium term (2–4 years) |

| PE-Backed M&A Roll-Up to Consolidate Fragmented Global Independents | +1.6% | Global — DACH, Southern Europe, South/Southeast Asia | Medium–Long term (3–5 years) |

| Circular / Bio-Based Wallpaper Certification Arbitrage in EU Public Procurement | +0.8% | European Union (DACH, Nordics, Benelux core) | Long term (≥ 4 years) |

Regional Analysis

Asia-Pacific Dominates the Wallpaper Market with a Market Share of 44.6%, Valued at USD 0.88 Billion

Asia-Pacific commands 44.6% of the global wallpaper market, driven by mid-income urbanization, rising residential construction activity across China, India, and Southeast Asia, and expanding middle-class spending on interior finishes. This concentration of demand makes APAC the single most important region for wallpaper manufacturers targeting volume growth, and early manufacturing or distribution presence here creates a structural cost advantage.

North America represents a mature but renovation-active market where consumer spending on home interiors remains consistent. NY Post data shows 77% of homeowners consider curb appeal important when evaluating home improvements, reflecting a broader commitment to property investment that includes interior wall surfaces. This behavioral profile supports steady wallpaper demand in mid-to-premium price tiers across the US and Canada.

Europe benefits from strong sustainability regulations and an established design culture that supports premium wallpaper adoption. The EU’s Ecodesign for Sustainable Products Regulation is accelerating a shift toward nonwoven and bio-based substrates, reshaping procurement criteria across residential, hospitality, and public-sector channels. Manufacturers with certified, low-VOC product portfolios hold a structural advantage in this regulatory environment.

Latin America and the Middle East and Africa remain earlier-stage markets where construction activity and a rising urban population are the primary demand catalysts. These regions represent smaller current revenue pools but offer above-average growth potential as household incomes rise and interior finishing standards increase. Wallpaper brands entering these markets now can establish distribution networks ahead of peak demand cycles.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Sangetsu Corporation commands a strong position in the APAC wallpaper market through its broad product portfolio and consistent collection refresh cycles. In June 2026, the company launched its 2026–2029 FINE collection with 771 wallpaper designs, including HARLEQUIN-branded products and expanded non-combustible wallcoverings. This scale of launch signals disciplined SKU investment and positions Sangetsu ahead of competitors in fire-safety-regulated commercial segments.

York Wall Coverings Inc. operates as a key North American player with a heritage brand identity that supports premium residential and commercial sales. As reported by Architectural Digest survey data, 55% of Americans redecorated their homes in 2020, highlighting the depth of consumer renovation activity that North American incumbents like York are positioned to capture. However, their reliance on traditional retail channels creates exposure as e-commerce and DTC models gain share in the residential segment.

Key Players

- Sangetsu Corporation

- York Wall Coverings Inc.

- Brewster Wallpaper Corporation

- F. Schumacher & Co.

- AS Creation Tapeten AG

- Osborne & Little

- The Romo Group

- Grandeco

- 4walls

- Asian Paints

Recent Developments

- May 2026 – Leftbank Art launched its Bespoke Art-Driven Wallcoverings collection, expanding from wall art into custom wallcovering products for hospitality, commercial, and residential applications.

- March 2025 – Feathr launched an eco-friendly wallcovering collection featuring two new products, Grasscloth and Recycled Material wallcoverings, made from natural and recycled fibers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.0 Billion |

| Forecast Revenue (2035) | USD 4.0 Billion |

| CAGR (2026-2035) | 7.40% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Nonwoven, Vinyl, Paper, Fabric, Others), By End Use (Residential, Commercial) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Sangetsu Corporation, York Wall Coverings Inc., Brewster Wallpaper Corporation, F. Schumacher & Co., AS Creation Tapeten AG, Osborne & Little, The Romo Group, Grandeco, 4walls, Asian Paints |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |