Quick Navigation

- Report Overview

- Key Takeaway

- Analysts’ Viewpoint

- US Market Revenue

- North America Market Valuation

- Device Type Analysis

- Technology Analysis

- End-User Analysis

- Distribution Channel Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

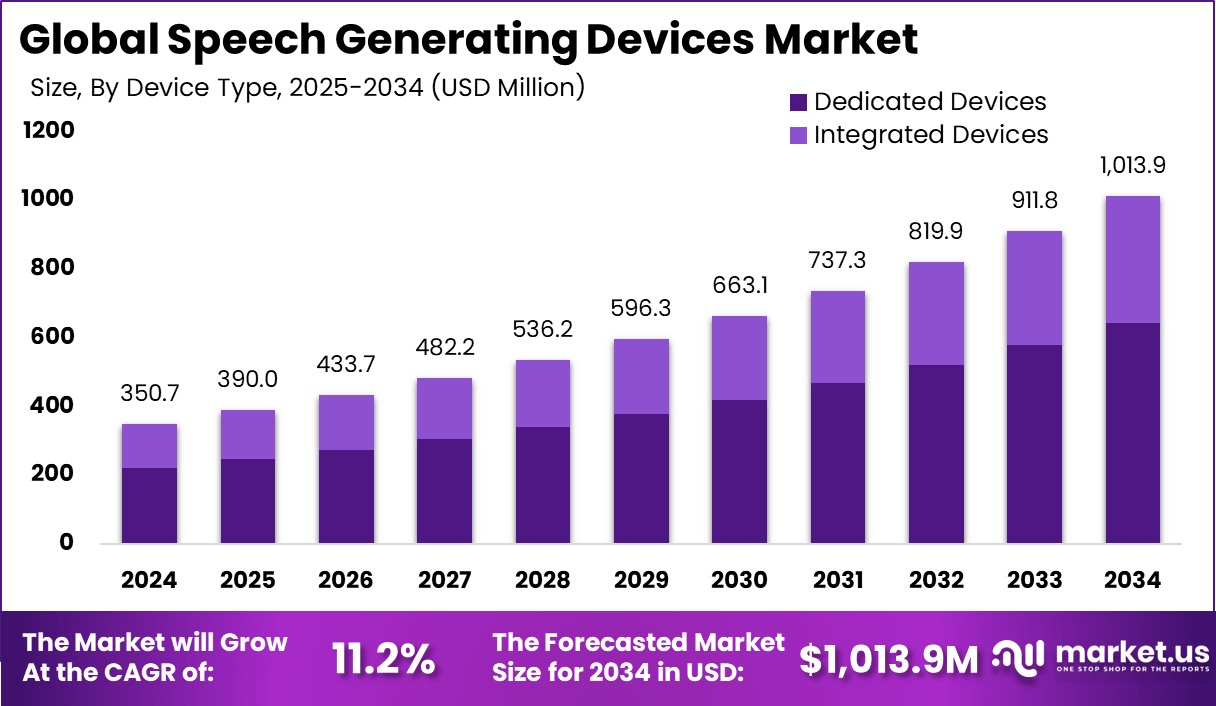

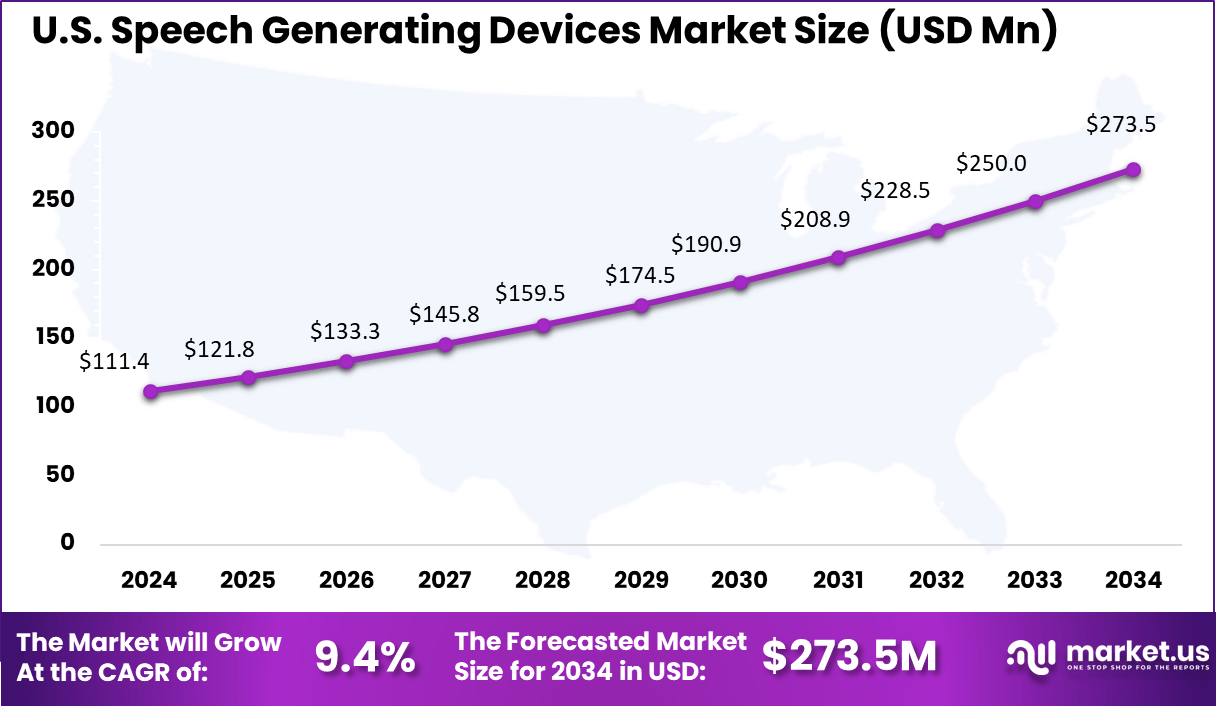

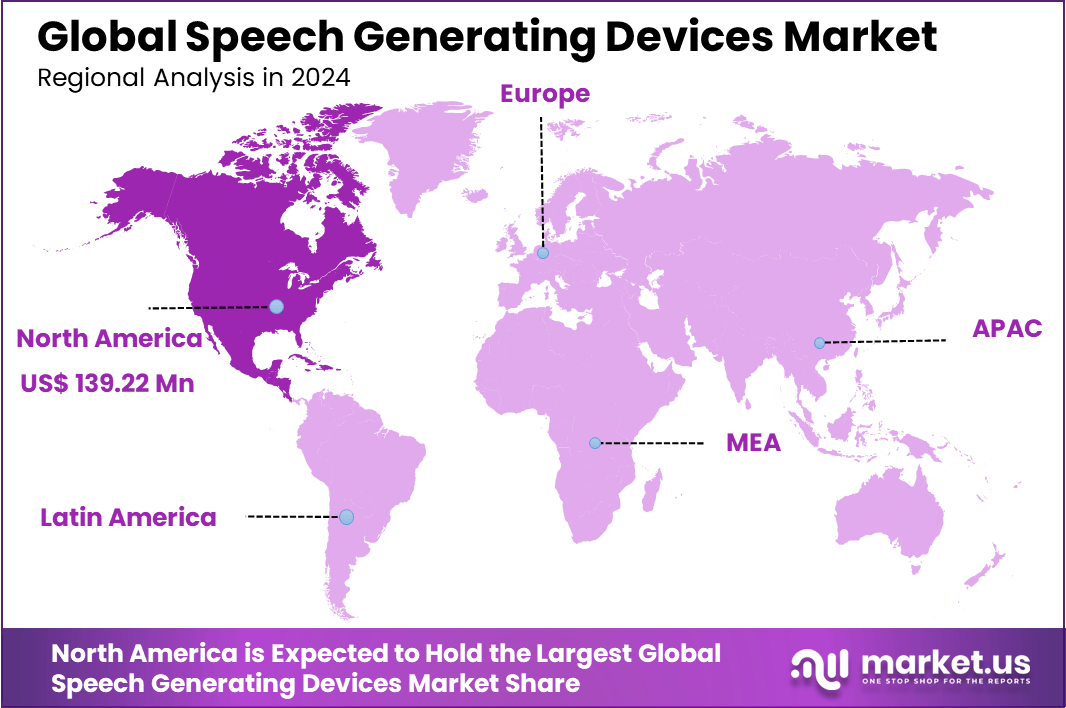

The Global Speech Generating Devices Market size is expected to be worth around USD 1,013.9 Million By 2034, from USD 350.7 Million in 2024, growing at a CAGR of 11.2% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 39.7% share, holding USD 139.22 Million revenue. The U.S. market size was estimated at USD 111.38 Million in 2024 and is expected to grow at a CAGR of 9.4% from 2025 to 2034.

Speech Generating Devices (SGDs), also known as augmentative and alternative communication (AAC) devices, are electronic tools designed to aid communication for individuals who are unable to speak naturally. These devices can range from simple machines that play recorded phrases to complex systems that synthesize speech from text entered via keyboards or touchscreens.

The market for SGDs is experiencing significant growth, driven by technological advancements and increasing awareness of the needs of individuals with speech impairments. This growth is supported by both the rising incidence of medical conditions that necessitate the use of SGDs and the advancements in technology that make these devices more accessible and effective.

Key factors propelling the market growth include the rising prevalence of speech and communication disorders and the continuous technological enhancements in SGDs. The integration of virtual and augmented reality technologies is also playing a crucial role, providing more immersive and effective communication aids for users.

Recent developments in SGD technology involve AI-powered speech recognition and language processing, which significantly improve the interaction quality for users. Moreover, the advent of implantable SGDs and the use of VR/AR technologies are setting new standards in the field, making these devices more accessible and effective.

The primary reasons for adopting SGDs include the need for enhanced communication aids in educational and healthcare settings, particularly for individuals with severe speech impairments. These devices are also crucial in improving the quality of life for many users, enabling them to engage more fully with their communities and environments.

Demand for SGDs is particularly high in regions with robust healthcare infrastructure and awareness of speech and communication disabilities. North America leads in market adoption, followed by Europe and the Asia-Pacific region, which shows promising growth potential due to increasing healthcare investments and awareness.

Key Takeaway

- The Speech Generating Devices (SGD) market is poised for substantial growth, with the market size projected to reach approximately USD 1,013.9 Million by 2034 from USD 350.7 Million in 2024, growing at a CAGR of 11.2% throughout the forecast period from 2025 to 2034.

- North America emerged as the dominant regional market in 2024, accounting for more than 39.7% of the global revenue share, valued at around USD 139.22 Million. Within this region, the United States maintained a significant position, with an estimated market size of USD 111.38 Million in 2024.

- The U.S. market is projected to grow at a CAGR of 9.4% from 2025 to 2034, driven by increasing healthcare investments and the presence of leading market players.

- The Dedicated Devices segment dominated the market in 2024, holding an impressive market share of over 63.4%. These devices, designed specifically for speech generation, continue to gain traction due to their robust performance and user-friendly interfaces.

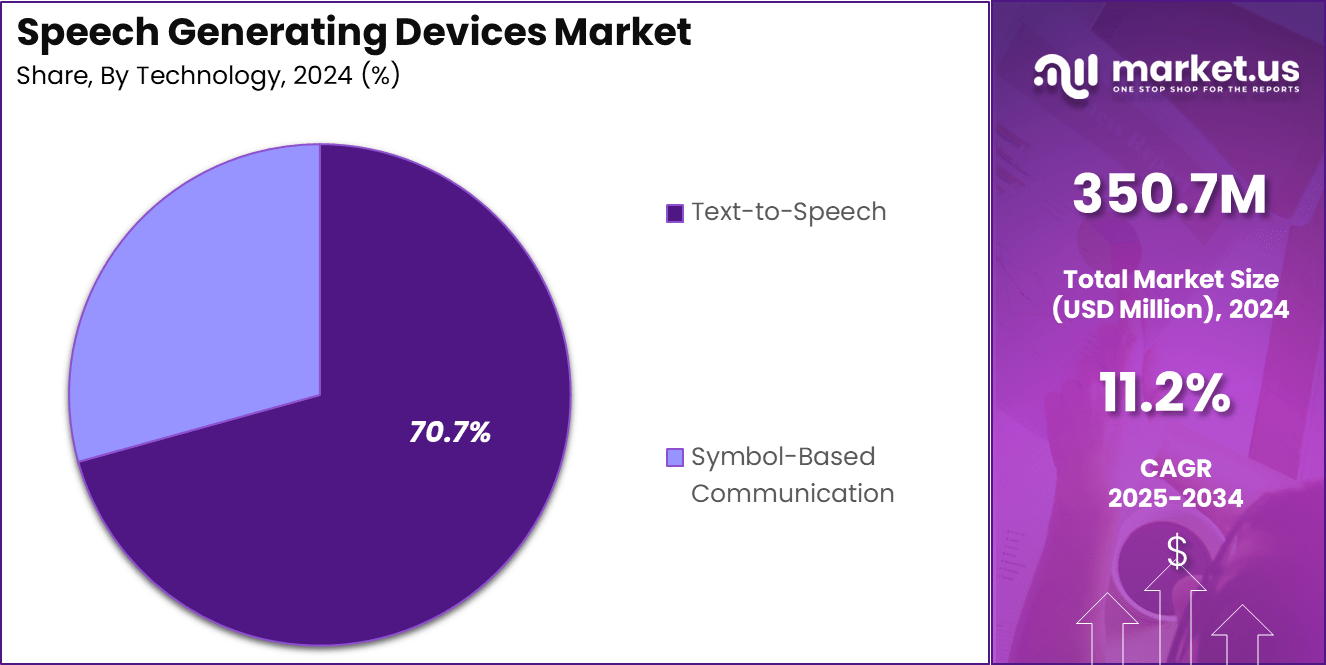

- The Text-to-Speech (TTS) technology segment took the lead in 2024, capturing more than 70.7% of the market share. The widespread adoption of TTS solutions can be attributed to their ability to convert written text into natural-sounding speech, offering a practical solution for individuals with speech impairments.

- Hospitals remained the primary end-users of speech generating devices in 2024, securing over 45.2% of the market share. The increasing focus on improving patient care and the integration of advanced communication aids in healthcare settings have significantly driven the segment’s growth.

- The Medical Supply Stores segment held a commanding position in the distribution landscape, capturing more than 52.8% of the market share in 2024.

Analysts’ Viewpoint

The expanding scope of applications for SGDs in healthcare, education, and home care settings offers numerous investment opportunities. Additionally, the growing demand in emerging markets presents a significant chance for market expansion and the introduction of cost-effective solutions.

Recent trends in the SGD market include the integration of natural language processing technologies to improve the fluidity and naturalness of synthesized speech. The market is also seeing a rise in the use of cloud-based solutions for data storage and management, which enhances the flexibility and capability of SGDs.

Businesses involved in the production and distribution of SGDs benefit from a growing customer base and the opportunity to lead in innovation within the assistive technology market. The increasing integration of advanced technologies in SGDs offers competitive advantages and potential for market leadership.

The regulatory environment for SGDs is primarily focused on ensuring the safety and effectiveness of these devices. Regulations govern everything from manufacturing standards to marketing practices, ensuring that the devices meet strict quality standards before they reach consumers.

US Market Revenue

The US Speech Generating Devices Market is valued at approximately USD 111.4 Million in 2024 and is predicted to increase from USD 121.8 Million in 2025 to approximately USD 273.5 Million by 2034, projected at a CAGR of 9.4% from 2025 to 2034.

This dominance is primarily due to the high prevalence of speech and language disorders within the country. According to the National Institute on Deafness and Other Communication Disorders (NIDCD), approximately 7.5 million individuals in the U.S. experience difficulties using their voices, necessitating the adoption of assistive communication technologies like SGDs.

Government initiatives have further propelled market growth. The Individuals with Disabilities Education Act (IDEA) provides funding for assistive technologies, ensuring that students with speech impairments have access to necessary communication devices. This support not only enhances educational outcomes but also contributes to the expansion of the SGD market.

North America Market Valuation

In 2024, North America held a dominant market position in the Speech Generating Devices sector, capturing more than a 39.7% share with revenues amounting to USD 139.22 Million. This prominent standing can be attributed to several key factors.

First, the region benefits from advanced healthcare infrastructure and a high level of awareness regarding speech and communication disabilities. These factors collectively facilitate the widespread adoption and integration of speech-generating technologies, particularly in educational and healthcare settings.

Moreover, North America’s leadership in the market is bolstered by strong governmental support and favorable regulatory policies. For instance, the Individuals with Disabilities Education Act (IDEA) in the United States mandates the provision of assistive technology, including speech generating devices, to eligible students at no cost.

Additionally, the presence of leading companies that specialize in advanced technology for SGDs contributes to the region’s market strength. These firms are often at the forefront of research and development, introducing innovations such as AI-enhanced speech recognition and language processing technologies. This not only enhances the functionality of SGDs but also improves user satisfaction by providing more natural and effective communication solutions.

Device Type Analysis

In 2024, the Dedicated Devices segment of the Speech Generating Devices market held a dominant position, capturing a significant market share of over 63.4%. This prominence can be primarily attributed to the specific advantages that dedicated devices offer over their integrated counterparts.

Dedicated speech generating devices are typically designed with a singular focus on communication enhancement, which allows for greater specialization in features tailored to the needs of individuals with speech impairments. These devices often incorporate high-quality, user-friendly interfaces that are customized for various disabilities, thereby facilitating easier communication for users with specific requirements.

The leading position of the Dedicated Devices segment is also bolstered by their robust construction and the ability to withstand frequent use, which is essential for individuals relying heavily on these devices for daily communication. Furthermore, dedicated devices usually feature extensive customization options that can be adapted to a wide range of communication disorders, making them highly versatile for users with complex needs.

Technological advancements have significantly enhanced the functionality of these devices, integrating sophisticated technologies such as touch screens and customizable software that supports a variety of languages and speech outputs. This technological integration not only improves user interaction but also enhances the effectiveness of communication aids, thereby increasing the adoption rate of dedicated devices.

Technology Analysis

In 2024, the Text-to-Speech (TTS) technology segment of the Speech Generating Devices market held a commanding lead, securing over 70.7% of the market share. This dominant position can be largely attributed to the critical role TTS technology plays in enhancing accessibility and user interaction across various applications.

Text-to-Speech systems convert written text into spoken word, allowing for significant improvements in accessibility for individuals with visual impairments, reading difficulties, or those who prefer auditory learning methods. The substantial market share of the Text-to-Speech segment is further supported by technological advancements that have enhanced the naturalness and intelligibility of synthesized speech.

Innovations in artificial intelligence and machine learning have propelled TTS technology forward, enabling more dynamic and context-aware voice responses. This evolution has expanded the use of TTS in sectors such as education, healthcare, customer service, and consumer electronics, where interactive and user-friendly communication tools are essential.

Moreover, the integration of TTS technology into mobile devices and cloud-based platforms has increased its accessibility and affordability, making it a preferred option in both developed and emerging markets. The cloud-based deployment models offer scalability and ease of integration with existing technologies, which further drives the adoption of TTS solutions across various industries.

End-User Analysis

In 2024, the Hospitals segment commanded the Speech Generating Devices market, capturing more than a 45.2% share. This leadership can largely be attributed to the essential role these devices play within hospital settings, particularly in specialized departments like neurology and speech therapy.

Hospitals utilize speech generating devices to enhance communication for patients experiencing speech impairments due to various medical conditions. These devices are integral in improving patient care by facilitating clearer communication between patients and healthcare professionals, which is crucial during treatment and recovery.

The dominant market position of the Hospitals segment is also reinforced by the integration of advanced speech technologies that cater specifically to the complex needs of hospital environments. The growing focus on patient-centered care in healthcare settings further drives the demand for such innovative communication solutions, which help in delivering effective care and improving health outcomes.

Furthermore, the push for technological integration in hospitals, including the adoption of AI-enhanced speech generating devices, supports the high adoption rates seen in this segment. These advancements not only enhance the functionality of speech devices but also ensure their adaptability to various patient needs, thereby solidifying the Hospitals segment’s lead in the market.

Distribution Channel Analysis

In 2024, the Medical Supply Stores segment held a commanding position in the distribution of Speech Generating Devices, securing more than a 52.8% market share. This leading role can be attributed to the specialized services that medical supply stores offer, which are crucial for the effective selection and utilization of these devices.

Medical supply stores typically provide expert guidance and personalized customer service, which is essential for healthcare professionals and patients alike to choose the most appropriate speech generating device that meets specific medical needs.

Moreover, the dominance of this segment is reinforced by the trust and reliability associated with purchasing from established medical supply outlets. These stores not only offer a wide range of products but also ensure that the devices comply with medical standards and regulations, which is a critical factor for medical equipment.

The physical presence of these stores allows for immediate access to products and the ability to receive hands-on support and training, which is particularly valued in the medical field. The extensive network and established relationships that medical supply stores have with healthcare institutions further strengthen their market position.

These connections facilitate streamlined procurement processes and integration of speech generating devices into healthcare practices, enhancing the operational efficiency of medical settings. This integrated approach helps in maintaining the Medical Supply Stores segment’s leadership in the market.

Key Market Segments

By Device Type

- Dedicated Devices

- Integrated Devices

By Technology

- Text-to-Speech

- Symbol-Based Communication

By End-User

- Hospitals

- Home Care Settings

- Rehabilitation Centers

- Others

By Distribution Channel

- Online Stores

- Medical Supply Stores

- Others

Driver

Integration of Advanced Technologies

The growth of the speech generating devices market is significantly driven by the integration of advanced technologies. These devices, particularly dynamic display devices, have evolved to include customizable touch screens and extensive vocabulary options, which cater to a wide range of speech impairments such as ALS and cerebral palsy.

The adoption of AI-driven features like real-time predictive text and voice customization enhances the functionality of these devices, making them more intuitive and effective for users. This technological advancement not only improves user interaction but also broadens the scope of applications for speech generating devices, thereby driving market expansion.

Restraint

High Costs and Lack of Skilled Professionals

One of the primary restraints in the speech generating devices market is the high cost associated with their development and implementation. The advanced technology and the materials required for these devices entail significant investments, which can be prohibitive for many healthcare providers and users.

Additionally, there is a notable shortage of skilled professionals who are trained to operate these sophisticated devices. This lack of expertise limits the effective utilization of speech generating devices, hindering their adoption across potential new markets and impacting the overall growth of the industry.

Opportunity

Increasing Global Prevalence of Speech Impairments

The rising global incidence of speech and language impairments presents a substantial opportunity for the expansion of the speech generating devices market. With conditions like autism, cerebral palsy, and aphasia becoming more prevalent, the demand for effective communication aids is on the rise.

Speech generating devices are increasingly being recognized as essential tools in speech therapy and rehabilitation, especially in educational and healthcare settings. The growing awareness and advocacy for inclusive communication solutions further propel the market’s growth, as more institutions and individuals seek out these technologies.

Challenge

Regulatory and Compliance Hurdles

Market players in the speech generating devices sector face significant challenges related to regulatory compliance and the continuously evolving legal landscape. Manufacturers must navigate complex certification processes to ensure their devices meet stringent safety and effectiveness standards set by healthcare regulators.

Additionally, as technology advances, so too do the regulatory requirements, which can vary widely between regions. Keeping up with these changes requires constant vigilance and adaptability, which can strain resources and slow down the pace of innovation and market entry for new players.

Growth Factors

The speech generating devices market is experiencing robust growth, driven by several key factors. The integration of advanced technologies such as dynamic displays, AI-driven predictive text, and voice customization features significantly enhances the functionality and user-friendliness of these devices.

This technological evolution is crucial in meeting the diverse needs of individuals with speech and language impairments. Moreover, the market is benefiting from increased governmental support and funding in regions like North America, where policies such as the Individuals with Disabilities Education Act (IDEA) play a pivotal role.

The global increase in the prevalence of speech and language disorders also fuels the demand for these devices. Conditions such as autism, cerebral palsy, and aphasia are becoming more recognized and diagnosed, leading to a greater need for effective communication aids across healthcare and educational settings.

Emerging Trends

Emerging trends in the speech generating devices market include the growing adoption of mobile and software-based applications, which offer portability and ease of use. These apps are becoming an integral part of the assistive technology landscape, providing flexibility and convenience for users on the go.

Additionally, there is a noticeable shift towards devices that support multimodal communication, combining text-to-speech, symbol-based communication, and other interactive methods. This trend highlights the market’s move towards more comprehensive and versatile communication solutions that cater to a broader range of communication disabilities.

The geographical expansion of the market into emerging economies in the Asia-Pacific region is another significant trend. Countries like India and China are witnessing a rapid increase in awareness and infrastructure development, which is creating new opportunities for market growth. Government initiatives in these regions to subsidize the cost of speech generating devices further bolster the market’s expansion.

Business Benefits

The advancements in speech generating devices offer numerous business benefits, including the ability to tap into new market segments and expand the customer base. With the broadening scope of applications for these devices, companies can explore untapped opportunities in various healthcare and educational sectors.

Furthermore, the continuous innovation in device features and capabilities allows companies to differentiate their products in a competitive market. Offering cutting-edge technology such as eye-tracking devices or AI-enhanced speech recognition can provide a significant competitive advantage.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Speech Generating Devices (SGD) market has seen significant activity among leading companies, particularly in acquisitions and new product launches.

Tobii Dynavox, a prominent player in the SGD market, has focused on expanding its product portfolio and global reach. The company has been involved in strategic partnerships and product innovations to enhance communication solutions for individuals with speech impairments.

Prentke Romich Company (PRC) has a longstanding history of developing AAC devices. The company continues to innovate by introducing new products designed to improve user experience and accessibility. PRC’s commitment to research and development ensures that their devices meet the evolving needs of individuals with communication challenges.

Lingraphica, specializes in AAC devices tailored for individuals with aphasia and other speech disorders. The company has recently focused on expanding its product line and enhancing device functionality to better serve its users. Lingraphica’s efforts underscore its dedication to improving communication solutions for those with speech impairments.

Top Key Players in the Market

- Tobii Dynavox

- Prentke Romich Company (PRC)

- Saltillo Corporation

- Lingraphica

- Zygo-USA

- Jabbla

- Smartbox Assistive Technology

- Forbes AAC

- Inclusive Technology Ltd.

- Attainment Company

- AMDi (Advanced Multimedia Devices, Inc.)

- Speech Generating Devices, Inc.

- Techcess Communications

- DynaVox Mayer-Johnson

- Liberator Ltd.

- Control Bionics

- Voice4u

- CoughDrop

- Grid 3

- LoganTech

- Others

Recent Developments

- In January 2025, Lingraphica, a prominent provider of augmentative and alternative communication (AAC) devices, announced that Chief Operating Officer Kevin Self would assume the role of Chief Executive Officer, succeeding Andrew Gomory.

- In August 2024, SoundHound, a voice AI company, acquired Amelia AI for $85 million. This acquisition aimed to enhance SoundHound’s presence in sectors such as financial services, insurance, healthcare, retail, and hospitality.

- In February 2023, Forbes AAC, a U.S.-based provider of dedicated communication devices, acquired CoughDrop Inc., a company known for its augmentative and alternative communication (AAC) applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 350.7 Mn |

| Forecast Revenue (2034) | USD 1,013.9 Mn |

| CAGR (2025-2034) | 11.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Device Type (Dedicated Devices, Integrated Devices), By Technology (Text-to-Speech, Symbol-Based Communication), By End-User (Hospitals, Home Care Settings, Rehabilitation Centers, Others), By Distribution Channel (Online Stores, Medical Supply Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Tobii Dynavox, Prentke Romich Company (PRC), Saltillo Corporation, Lingraphica, Zygo-USA, Jabbla, Smartbox Assistive Technology, Forbes AAC, Inclusive Technology Ltd., Attainment Company, AMDi (Advanced Multimedia Devices, Inc.), Speech Generating Devices, Inc., Techcess Communications, DynaVox Mayer-Johnson, Liberator Ltd., Control Bionics, Voice4u, CoughDrop, Grid 3, LoganTech, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |