Quick Navigation

Report Overview

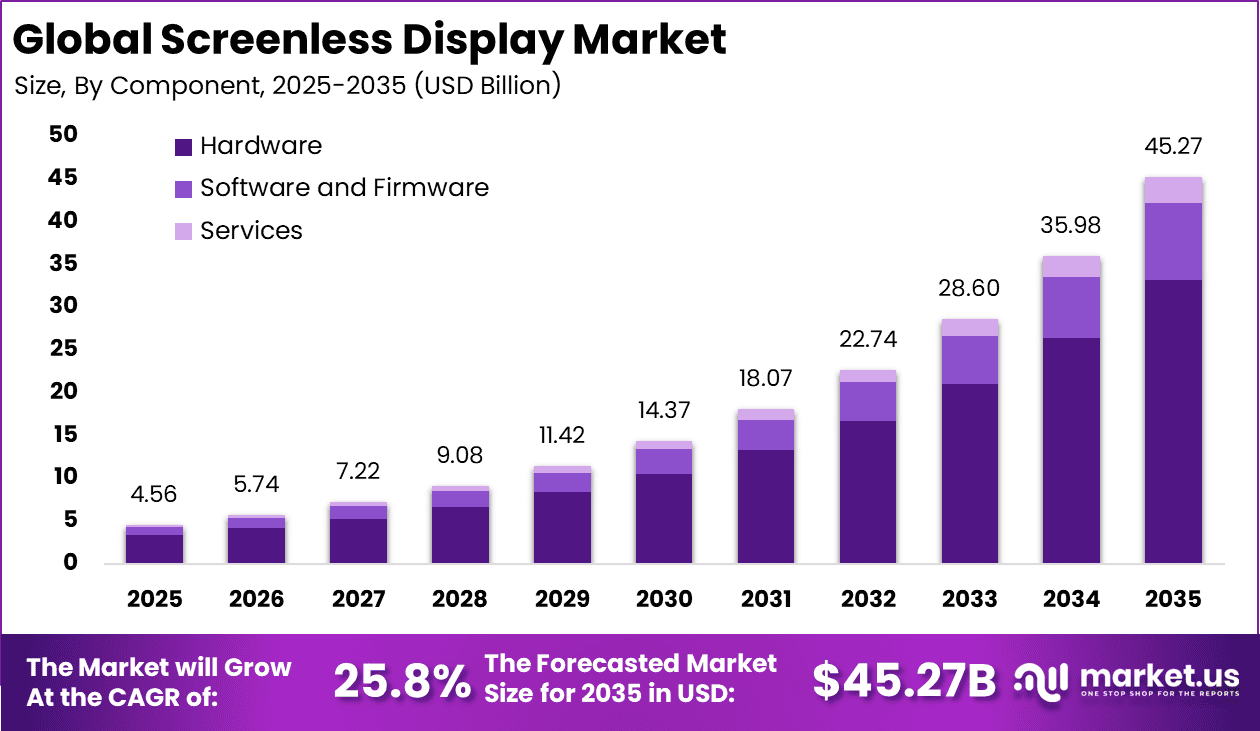

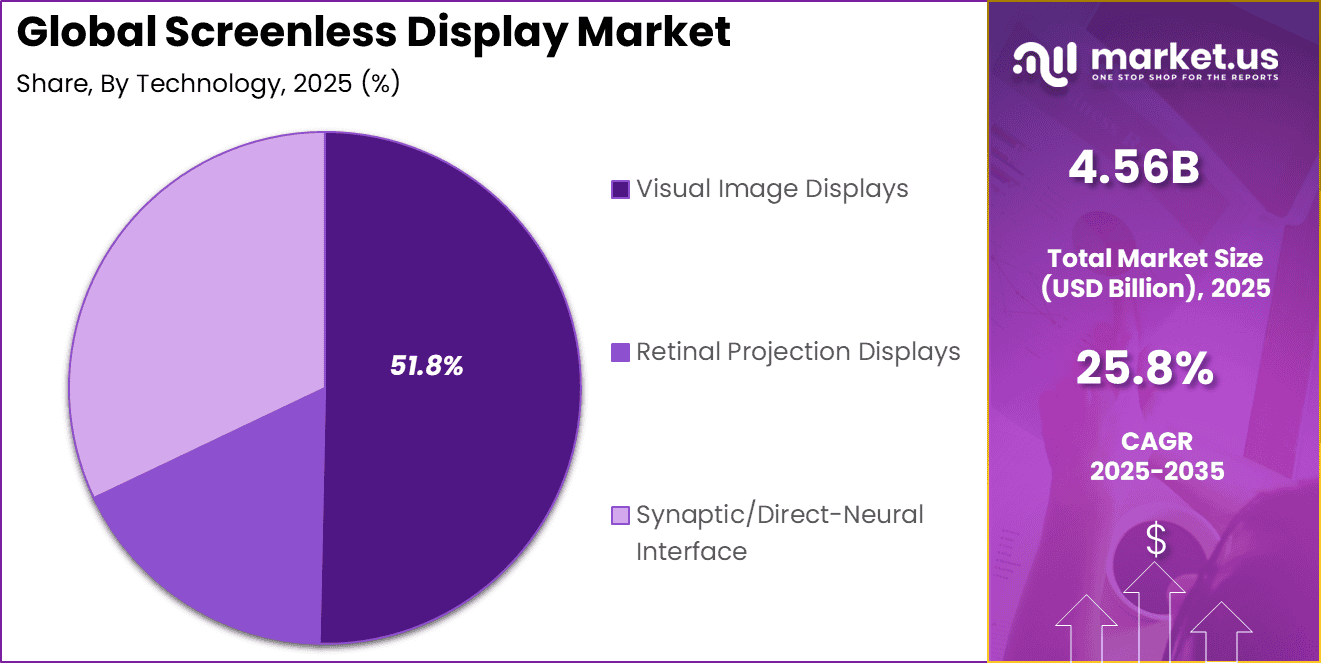

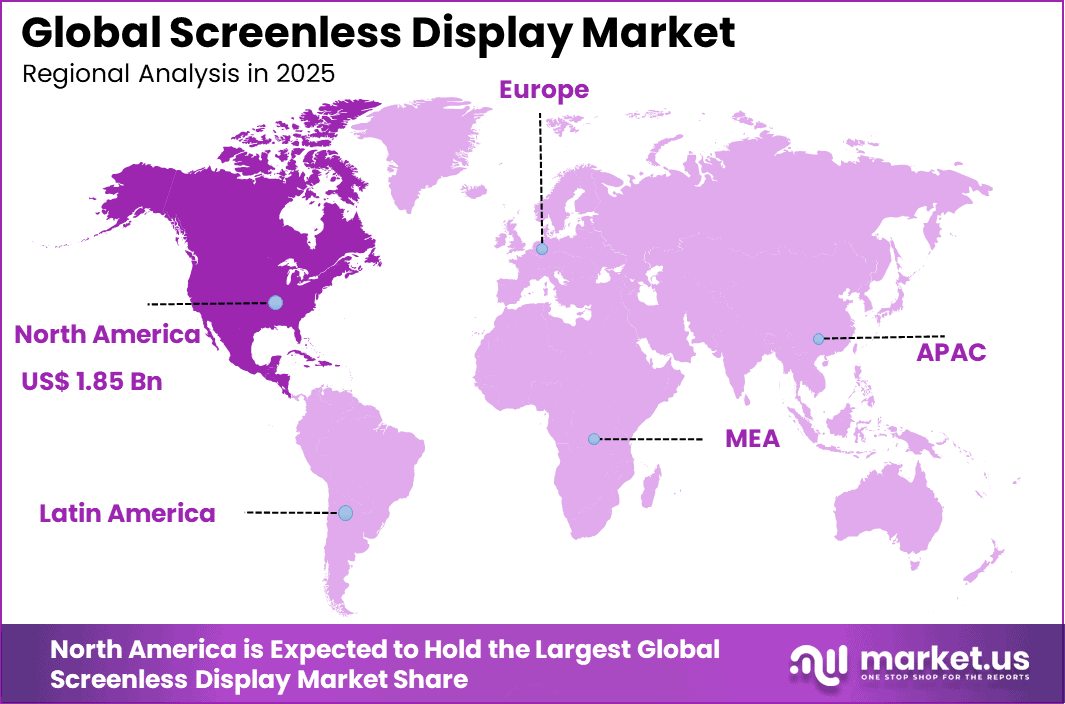

The Global Screenless Display Market size is expected to be worth around USD 45.27 billion by 2035, from USD 4.56 billion in 2025, growing at a CAGR of 25.8% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 40.6% share, holding USD 1.85 billion in revenue.

The screenless display market refers to technologies that project or transmit visual information without the use of a traditional physical screen. These systems include holographic displays, retinal projection devices, and spatial projection technologies that display images directly onto surfaces or into the human eye. Screenless displays are designed to provide immersive visual experiences while reducing reliance on conventional display hardware such as monitors, televisions, and mobile screens.

The market is gaining attention as industries explore new ways to deliver digital content in more interactive and space-efficient formats. Screenless display technologies are being applied in areas such as augmented reality, virtual reality, automotive interfaces, healthcare visualization, and consumer electronics. These systems enable users to access digital information in real time without the need for bulky display devices.

Demand for screenless displays is rising as users seek immersive experiences without the strain of prolonged screen exposure. Nearly 64% of recent technology upgrades include eye-tracking and voice-control features, making these systems more intuitive and practical. Healthcare and automotive settings show especially strong demand, where fast access to clear information improves efficiency, reduces distraction, and supports safer outcomes.

For instance, in March 2026, WaveOptics Ltd. (Snap‑linked ecosystem) broadened its licensing model, enabling more OEMs to integrate its holographic waveguide technology into fashion‑style AR glasses. The shift supports the trend of embedding screenless‑style optics into everyday eyewear, rather than bulky headsets, especially for social and lifestyle applications.

Key Takeaway

- In 2025, the hardware segment dominated the screenless display market, accounting for 73.4% share.

- In 2025, visual image display technology led the market with a 51.8% share.

- In 2025, head-up displays (HUD) held the largest share at 50.3%.

- In 2025, the aerospace and defense sector led end-user adoption with 34.4% share.

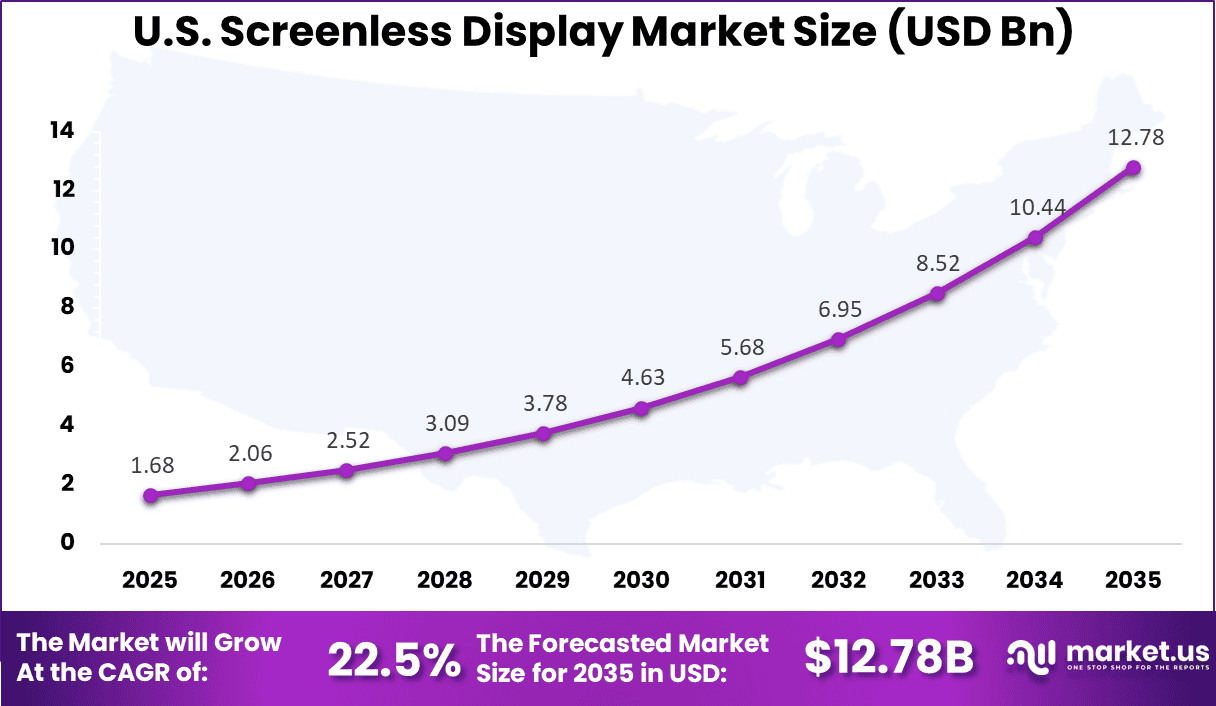

- In 2025, North America dominated the market with a 40.6% share, while the U.S. market reached USD 1.68 billion and is expanding at a CAGR of 22.5%.

Component Analysis

In 2025, The Hardware segment held a dominant market position, capturing a 73.4% share of the Global Screenless Display Market. This dominance is due to the essential role hardware plays in enabling accurate and reliable screenless display performance. Components like sensors and projection units form the core of these systems, ensuring clarity and stability in output. Growing use of wearables and vehicles strengthens demand for durable and high-quality hardware integration.

Hardware continues to gain importance as industries focus on improving real-time interaction and system efficiency. Strong reliance on physical components supports seamless operation in complex environments. As applications expand, the need for advanced optical and sensing technologies increases, reinforcing hardware as a foundational element in screenless display solutions.

For Instance, in January 2026, Google pushed forward with lightweight hardware modules for screenless projection in smart eyewear prototypes. These compact sensors and optics aim to blend seamlessly into daily glasses, letting users see overlays without bulky gear. Teams focused on durability for real-world knocks, sparking interest from wearable fans.

Technology Analysis

In 2025, the Visual Image Displays segment held a dominant market position, capturing a 51.8% share of the Global Screenless Display Market. This dominance is due to the strong preference for technologies that deliver clear and immediate visual output without physical screens. Visual image displays provide effective communication of information, making them suitable for environments where quick understanding is required. Their adaptability across industries supports wider acceptance and consistent usage.

Visual image displays continue to evolve with improvements in projection and clarity. Users benefit from enhanced viewing experiences that feel natural and intuitive. As industries demand better interaction without traditional screens, this technology remains a preferred choice for delivering visual content efficiently in both personal and professional settings.

For instance, in February 2026, Leia advanced its lightfield tech for sharper visual image rendering without screens. This update creates natural depth in holograms, ideal for medical visuals or gaming. Growth stems from users craving vivid, eyesafe projections that pop in any light, fueling quick uptake in creative fields hungry for immersive tools.

Display Type Analysis

In 2025, The Head-Up Display (HUD) segment held a dominant market position, capturing a 50.3% share of the Global Screenless Display Market. This dominance is due to the ability of head-up displays to present information directly within the user’s field of vision. This reduces the need to look away from tasks, improving focus and safety. Strong adoption in vehicles and aircraft highlights its value in situations where attention and timing are critical.

Head-up displays support better decision-making by delivering real-time data in a simple and accessible format. Their use enhances user awareness without adding complexity. As safety and efficiency become more important across industries, HUD systems continue to expand in both advanced mobility and operational environments.

For Instance, in January 2026, DigiLens unveiled thinner holographic gratings for HUDs in vehicle windshields. This lets drivers view alerts without shifting gaze, built tough for vibrations. The segment grows as auto builders seek distraction-free info overlays, making roads safer and pulling in fleet operators who value clear, hands-free updates.

End-User Industry Analysis

In 2025, The Aerospace and Defense segment held a dominant market position, capturing a 34.4% share of the Global Screenless Display Market. This dominance is due to the high demand for precise and reliable visualization tools in critical operations. Aerospace and defense environments require quick access to real-time data, where screenless displays improve situational awareness and response time. These systems support better coordination and accuracy in challenging conditions.

Adoption continues to grow as defense and aviation sectors prioritize advanced technologies for mission efficiency. Screenless displays enable seamless data access without physical limitations, supporting complex tasks. Their role in enhancing performance and reducing operational risk makes them valuable in high-pressure and sensitive environments.

For Instance, in January 2026, RealView rolled out 3D holographic sims for aerospace training cockpits. Trainees interact with floating models sans screens, boosting retention. Growth hits from ops needing precise visuals in tight spaces, as forces invest to cut errors and speed up readiness for real missions.

By Region

North America holds 40.6% of the market share due to strong adoption of advanced visualization technologies and significant investment in aerospace, defense, and automotive sectors. Organizations in the region actively implement screenless display systems to improve operational efficiency and user experience. The presence of leading technology companies further supports regional market growth.

For instance, in February 2026, Synaptics introduced touchless gesture interfaces combined with holographic projection for automotive HUDs. Partnerships with Detroit automakers showcase California’s semiconductor expertise, driving North America’s screenless display commercialization leadership.

Within North America, the United States contributes USD 1.68 billion with a growth rate of 22.5%. The country’s advanced aerospace and defense industry and increasing adoption of innovative display technologies have strengthened demand for screenless display solutions. Continued investment in immersive and augmented visualization technologies is expected to sustain market expansion.

For instance, in January 2026, Google strengthened U.S. dominance in screenless displays by unveiling advanced AR prototypes using retinal projection at CES 2026. The technology promises seamless integration with Android devices, targeting enterprise and consumer markets with hands-free visual overlays. This innovation reinforces North America’s lead in immersive display solutions.

Growth Factors

One of the primary growth factors driving the screenless display market is the increasing demand for immersive and interactive user experiences. Consumers and businesses are seeking advanced visualization technologies that provide more engaging ways to interact with digital content. Screenless displays offer three-dimensional and projection-based experiences that enhance user engagement.

Another growth factor is the expansion of augmented reality and virtual reality applications. AR and VR technologies rely on advanced display systems to deliver immersive environments. Screenless display solutions enable more natural interaction with digital content by projecting visuals into real-world environments or directly into the user’s field of view.

Emerging Trends

One emerging trend in the screenless display market is the development of retinal projection technology. These systems project images directly onto the retina, allowing users to view high-resolution visuals without external screens. This approach improves portability and enables personalized viewing experiences.

Another trend is the integration of screenless displays into wearable devices. Smart glasses and head-mounted devices are incorporating projection-based display technologies to deliver information directly to users. This trend supports hands-free interaction and enhances productivity in various applications.

Key Market Segments

By Component

- Hardware

- Light Engine and Lasers

- Waveguides and Optical Combiners

- ICs and Controllers

- Software and Firmware

- Services

- Design

- Integration

- Maintenance

By Technology

- Visual Image Displays

- Retinal Projection Displays

- Synaptic/Direct-Neural Interface

By Display Type

- Head-Up Display (HUD)

- Head-Mounted Display (HMD)

- Holographic Projection Kiosks

- Implantable and Wearable Micro-Projectors

By End-user Industry

- Consumer Electronics

- Automotive

- Aerospace and Defense

- Healthcare and Life-Sciences

- Industrial and Logistics

- Retail and Advertising

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Rising Demand for Hands-Free Interaction

The growing need for hands-free interaction is encouraging the adoption of screenless display technologies across various industries. Users prefer solutions that allow quick access to information without relying on physical screens. This improves convenience and helps maintain focus, especially in environments where attention and efficiency are important.

Screenless displays enable natural interaction through voice commands and gesture-based controls. This reduces dependency on traditional devices and supports smoother workflows. As industries move toward more connected and responsive systems, demand for such intuitive technologies continues to increase, supporting better user experiences and improved operational performance.

For instance, in January 2026, Alphabet Inc. (Google) pushed forward with Android XR glasses that bring hands-free controls to everyday use. Users can now gesture or speak to navigate apps while on the move, like checking directions during a walk. This builds on their long interest in smart eyewear, making interactions feel natural without pulling out a phone.

Restraint

High Development Costs

High development costs remain a key restraint for screenless display technologies. Advanced components such as sensors, projection systems, and optical modules require significant investment. This increases the overall cost of production, making it difficult for companies to offer affordable solutions, especially in price-sensitive markets and early adoption stages.

Research and testing also add to expenses, as these technologies require precision and reliability. Continuous improvements in design and performance demand ongoing investment. Smaller companies may struggle to enter the market, which slows innovation and limits widespread adoption despite growing interest in screenless display solutions.

For instance, in March 2025, Magic Leap faced funding hurdles while refining its AR headset prototypes, as custom optics and sensors drove up expenses. The team had to scale back some features to manage budgets, showing how pricey R&D can slow even established players. They focused on core elements to keep projects alive.

Opportunities

Expansion in Healthcare Applications

Healthcare offers strong opportunities for screenless display technologies, especially in areas that require precision and real-time data access. Medical professionals benefit from hands-free visualization, which allows them to focus on procedures without interruption. This improves workflow efficiency and supports better patient care outcomes.

The use of projection-based and wearable display solutions enhances accuracy in surgeries and diagnostics. These technologies help reduce reliance on external screens and simplify information access. As healthcare systems continue to adopt advanced tools, screenless displays are becoming an important part of modern medical environments.

For instance, in June 2025, Microsoft updated HoloLens for medical training, letting surgeons project 3D organ models mid-procedure without screens. Doctors practiced complex operations hands-free, improving focus and precision in busy ORs. This move highlights healthcare as a key growth area for such tech.

Challenges

Technical Complexity and Integration Issues

Technical complexity is a major challenge in the development of screenless display systems. These technologies require precise coordination between hardware and software to deliver clear and stable visuals. Any inconsistency can affect performance, making it difficult to ensure reliability across different operating conditions.

Integration with existing infrastructure also presents difficulties for organizations. Many systems require customization to function properly with current technologies. This increases implementation time and effort, creating barriers for adoption. Overcoming these challenges is essential for achieving seamless deployment and long-term usability.

For instance, in October 2025, Samsung Electronics Co. Ltd. ran into glitches blending their AR glasses with existing phone apps, as gesture tracking clashed with older software. Early testers noted lag and setup hassles, forcing extra tweaks for smoother compatibility. It underscores the hurdles in making screenless tech work seamlessly across devices.

Key Players Analysis

The Screenless Display Market is driven by global technology companies that are advancing augmented reality, holographic projection, and virtual display technologies. Alphabet Inc., Microsoft Corporation, Sony Group Corporation, and Samsung Electronics are investing in next generation display solutions that eliminate the need for physical screens.

Augmented reality and holographic display specialists play a significant role in shaping market innovation. Magic Leap, Avegant, RealView Imaging, and Holoxica develop advanced visual technologies that enable 3D visualization without traditional screens. Their platforms are widely used in medical imaging, training simulations, and immersive visualization applications.

Component manufacturers and emerging innovators further strengthen the competitive landscape. Synaptics, Vuzix, MicroVision, DigiLens, Dispelix, and Lumus provide core components such as waveguides, micro displays, and projection systems. Additional players including Apple Inc., Panasonic Corporation, Leia Inc., EON Reality, and Mojo Vision focus on immersive computing and next generation display ecosystems.

Top Key Players in the Market

- Alphabet Inc. (Google)

- Microsoft Corp.

- Sony Group Corp.

- Samsung Electronics Co. Ltd.

- Magic Leap Inc.

- Avegant Corp.

- RealView Imaging Ltd.

- Synaptics Inc.

- Holoxica Ltd.

- EON Reality Inc.

- Leia Inc.

- Vuzix Corp.

- MicroVision Inc.

- DigiLens Inc.

- Dispelix Oy

- Lumus Ltd.

- Panasonic Corp.

- Apple Inc.

- Jade Bird Display

- WaveOptics Ltd.

- Mojo Vision

- Others

Recent Developments

- In March 2026, Synaptics Inc. rolled out a new sensor‑fusion platform optimized for screenless AR and AI‑glasses, combining eye‑tracking, hand‑gesture recognition, and low‑latency audio processing. The platform is being integrated into several third‑party glasses designs, accelerating the time‑to‑market for screenless‑style consumer and enterprise wearables.

- In January 2026, Alphabet Inc. (Google) deepened its indirect footprint in screenless displays by investing in a startup ecosystem working on retinal projection and holographic optics, via its Google Ventures‑linked funds. The focus is on enabling smaller, low‑power screenless interfaces for future AR‑style wearables, positioning Google to influence the core software and AI layers of the screenless stack.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.5 Bn |

| Forecast Revenue (2035) | USD 45.2 Bn |

| CAGR (2026-2035) | 25.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Hardware, Software, and Firmware, Services), By Technology (Visual Image Displays, Retinal Projection Displays, Synaptic/Direct-Neural Interface), By Display Type (Head-Up Display (HUD), Head-Mounted Display (HMD), Holographic Projection Kiosks, Implantable and Wearable Micro-Projectors), By End-user Industry (Consumer Electronics, Automotive, Aerospace and Defense, Healthcare and Life-Sciences, Industrial and Logistics, Retail and Advertisement, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Alphabet Inc. (Google), Microsoft Corp., Sony Group Corp., Samsung Electronics Co. Ltd., Magic Leap Inc., Avegant Corp., RealView Imaging Ltd., Synaptics Inc., Holoxica Ltd., EON Reality Inc., Leia Inc., Vuzix Corp., MicroVision Inc., DigiLens Inc., Dispelix Oy, Lumus Ltd., Panasonic Corp., Apple Inc., Jade Bird Display, WaveOptics Ltd., Mojo Vision, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |