Global Polyethylene Wax Market Size, Share, And Enhanced Productivity By Product Type (Low Density Polyethylene, High Density Polyethylene, Oxidized Polyethylene, Others), By Processing Method (Polymerization, Chemical Modification, Physical Blending), By Application (Coating (Powder Coating, Pastile Coating), Plastics and Polymer, Hot Melt Adhesive, Candles, Rubber, Cosmetics and Pharmaceuticals, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179361

- Number of Pages: 334

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

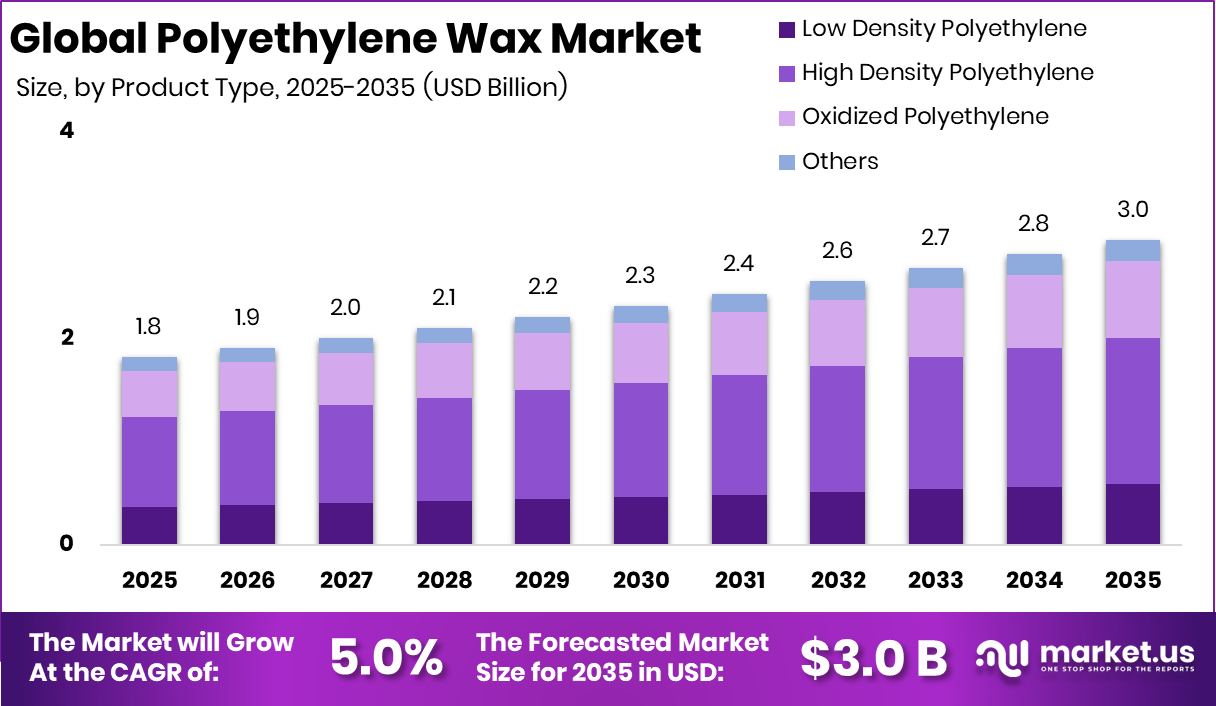

The Global Polyethylene Wax Market is expected to be worth around USD 3.0 billion by 2035, up from USD 1.8 billion in 2025, and is projected to grow at a CAGR of 5.0% from 2026 to 2035. The Asia Pacific region commands 56.6% market share valued at USD 1.0 Bn.

Polyethylene wax is a lightweight, fine-textured synthetic wax produced from polyethylene through polymerization, chemical modification, or physical blending. It is valued for its hardness, lubricity, thermal stability, and compatibility with a wide range of industrial materials. The material functions as a processing aid and performance enhancer across coatings, plastics, hot-melt adhesives, rubber goods, and candle formulations, with additional relevance in cosmetics and pharmaceutical applications.

The Polyethylene Wax Market represents the commercial ecosystem that supplies, processes, and distributes these wax grades across industries. It is shaped by the performance needs of plastics and polymer processors, the demand for stable coating formulations, and the requirement for clean-burning waxes in industrial and consumer products. Market structure is aligned with your taxonomy—product type, processing method, and application—reflecting how buyers choose wax grades for specific end-uses.

Growth factors in this market relate to rising polymer production, expanding adhesive consumption, and broader use of processing aids that improve output efficiency. Demand is also influenced by global plastic volumes, which exceed 400 million tonnes annually, with only about 10% recycled. This challenge has created opportunities for better materials management and improved processing technologies.

Funding activity further shapes opportunities. Investments such as Catalyst raising $400m for its IOS fund, General Atlantic acquiring European Wax Center for $330m, and Magpet Polymers securing ₹205 crore for a major recycling facility indicate strong financial interest in polymer-linked sectors. Additional developments like Akron’s polymer cluster competing for a $160 million NSF grant and BacAlt Biosciences raising ₹18 crore for biopolymers reflect the potential for innovation in materials that complement or compete with polyethylene wax.

Key Takeaways

- The Global Polyethylene Wax Market is expected to be worth around USD 3.0 billion by 2035, up from USD 1.8 billion in 2025, and is projected to grow at a CAGR of 5.0% from 2026 to 2035.

- The Polyethylene Wax Market grows steadily as high-density polyethylene usage reaches nearly 47.8% worldwide.

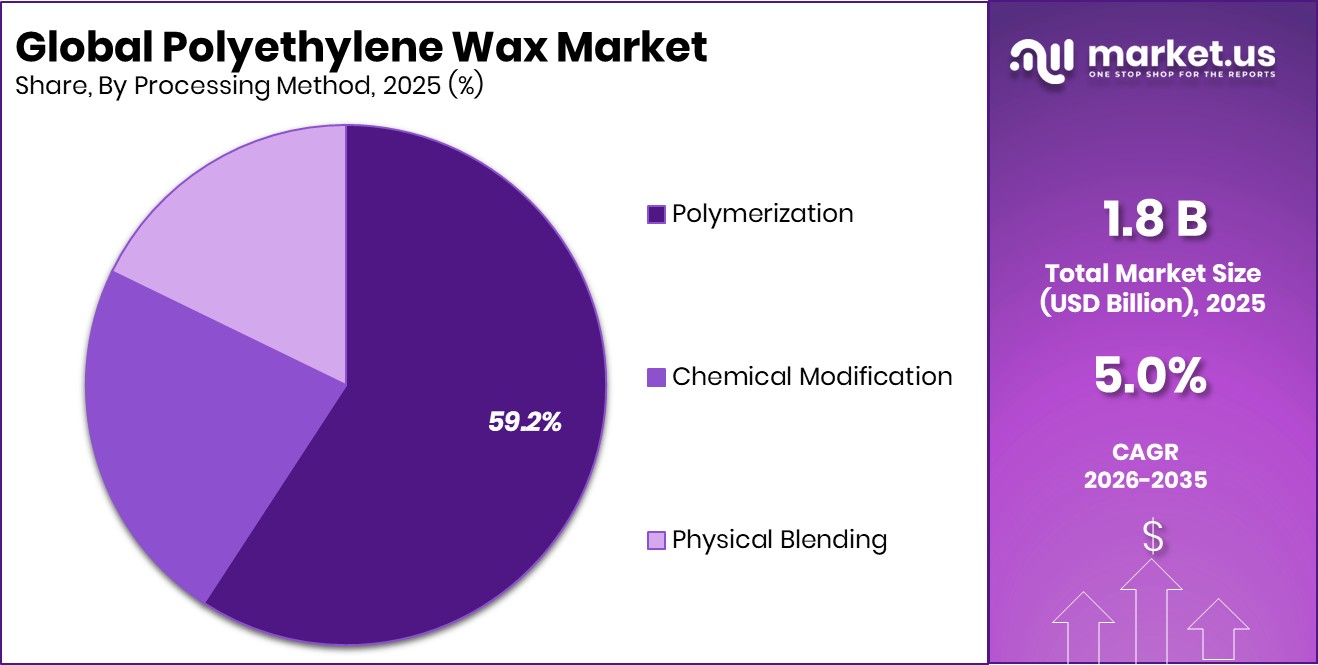

- Polymerization dominates the Polyethylene Wax Market, contributing 59.2% share and strengthening overall global demand.

- Plastics and polymer applications drive the Polyethylene Wax Market, accounting for 49.1% of total consumption.

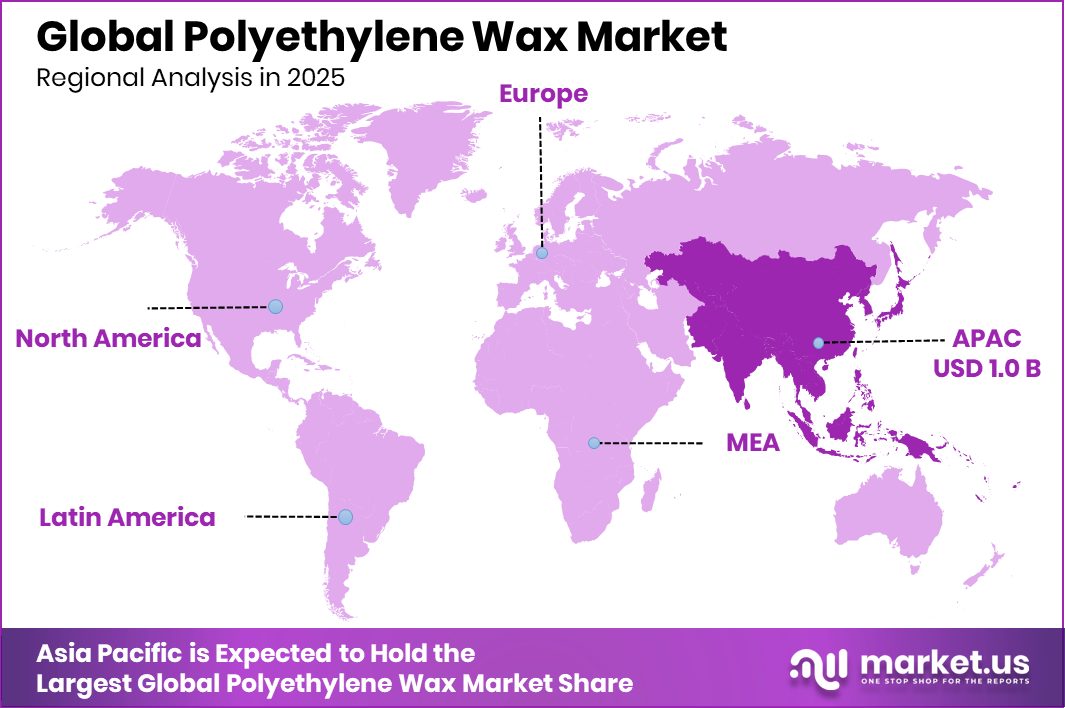

- In the Asia Pacific, Polyethylene Wax demand totals USD 1.0 Bn with 56.6% dominance.

By Product Type Analysis

The Polyethylene Wax Market grows steadily as high-density polyethylene captures 47.8%.

In 2025, the Polyethylene Wax Market is expected to see strong momentum as High-Density Polyethylene (HDPE) grades maintain a leading 47.8% share due to their superior hardness, thermal stability, and compatibility with multiple industrial formulations. Manufacturers continue to rely on HDPE-based waxes for consistent performance in plastics, coatings, and adhesives, especially where higher melting points and enhanced abrasion resistance are required.

Growth is further supported by expanding packaging activity and demand for durable plastic compounds across Asia and North America. As industries prioritize materials that offer cost efficiency and better processing behavior, HDPE-derived polyethylene wax remains a core choice, helping producers strengthen both product quality and operational reliability in 2025.

By Processing Method Analysis

Strong polymerization dominance drives the Polyethylene Wax Market with a notable 59.2%.

In 2025, polymerization-derived polyethylene wax holds a commanding 59.2% share in the market, driven by industries’ preference for controlled molecular structure, higher purity, and reliable performance across varied applications.

Producers continue shifting toward polymerization technology because it allows them to customize melting points and hardness levels, meeting the specifications of modern plastics and coating formulations. This method also supports consistent large-scale production, which is essential for fast-growing sectors such as masterbatches, rubber processing, and inks.

With manufacturers demanding predictable dispersion and better thermal behavior, polymerization remains the most trusted method in 2025, helping companies deliver stable, high-quality PE wax grades tailored to advanced industrial requirements.

By Application Analysis

Expanding plastics demand boosts the Polyethylene Wax Market through its leading 49.1% application.

In 2025, the plastics and polymer segment holds a substantial 49.1% share of the Polyethylene Wax Market, reflecting its deep integration in compounding, molding, and extrusion activities worldwide. PE wax continues to be valued for improving melt flow, enhancing surface finish, and ensuring smoother processing in PVC, masterbatch production, engineered plastics, and color concentrates.

With packaging, construction materials, and consumer goods manufacturing expanding across Asia-Pacific and the Middle East, demand for processing aids remains strong. Companies increasingly use PE wax to reduce energy consumption during extrusion and to achieve consistent product quality. As polymer producers scale up output in 2025, the role of PE wax as an essential industrial additive remains firmly established.

Key Market Segments

By Product Type

- Low-Density Polyethylene

- High-Density Polyethylene

- Oxidized Polyethylene

- Others

By Processing Method

- Polymerization

- Chemical Modification

- Physical Blending

By Application

- Coating

- Powder Coating

- Pastile Coating

- Plastics and Polymer

- Hot Melt Adhesive

- Candles

- Rubber

- Cosmetics and Pharmaceuticals

- Others

Driving Factors

Rising polymer production boosts wax demand

Rising polymer production boosts wax demand, especially as global plastic output continues to grow and manufacturers seek materials that enhance processing efficiency, surface quality, and product durability. The market also gains momentum from increasing attention to recycling and circular material flows, supported by significant funding events shaping the broader polymer ecosystem.

Magpet Polymers securing ₹205 crore for India’s largest bottle-to-bottle recycling facility signals a strong push toward improved plastic handling, indirectly supporting demand for processing aids like polyethylene wax. Additionally, Prism Worldwide is raising $40 million in Series A and A1 funding highlights growing investment in polymer-related material innovation. These developments reinforce industrial activity, driving consistent uptake of polyethylene wax across major applications.

Restraining Factors

Volatile polyethylene prices affect wax stability

Volatile polyethylene prices affect wax stability, making cost planning difficult for producers and end-users who depend on predictable raw material inputs. Price fluctuations often lead to inconsistent margins for processors and can reduce the willingness of buyers to commit to large-scale output or long-term supply contracts. The broader plastic-related funding landscape reflects both challenges and attempts to tackle environmental concerns.

Planet Smart, raising $1 million in pre-seed funding, shows efforts to innovate around waste reduction, while Breaking, securing $10.5 million in seed funding to develop naturally derived plastic-degradation solutions, points to a rising market shift toward alternative materials. These developments may gradually influence long-term demand patterns and restrain certain polyethylene wax consumption segments.

Growth Opportunity

Expanding adhesive applications create new openings

Expanding adhesive applications create new openings for polyethylene wax, as industries increasingly require materials that improve melt flow, bonding behavior, and long-term product durability. Hot melt adhesives, packaging tapes, bookbinding materials, and industrial assembly lines all rely on wax-based modifiers to achieve smoother processing. Growth potential is further supported by innovations in waste-handling and material recovery.

Planet Smart raising $1 million to address plastic waste in nappies and pads highlights continued activity in polymer-related sustainability fields. Such investments indicate long-term market transitions that can create fresh opportunities for specialty additives like polyethylene wax, particularly in applications where performance improvements and material efficiency are essential for manufacturers.

Latest Trends

Shift toward cleaner high-purity wax grades

The shift toward cleaner, high-purity polyethylene wax grades is becoming more pronounced as manufacturers prioritize better processing behavior, reduced residue, and improved compatibility with advanced polymer systems. Industries are increasingly adopting refined waxes to meet stricter performance expectations in coatings, masterbatches, rubber compounds, and sophisticated adhesive formulations. Broader trends in the plastics sector also influence this direction.

The U.S. Department of Energy’s $13.4 million funding to combat plastic waste and reduce emissions underscores a clear push toward improved material efficiency and cleaner industrial practices. This momentum supports interest in advanced wax technologies that align with higher sustainability expectations and evolving regulatory landscapes across global markets.

Regional Analysis

Asia Pacific leads the Polyethylene Wax Market with 56.6% share reaching USD 1.0 Bn.

In the Polyethylene Wax Market, regional performance varies across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, with Asia Pacific holding the dominant position.

Asia Pacific accounts for 56.6% of the total market and reaches USD 1.0 Bn, driven by expanding plastics manufacturing, stronger polymer processing activity, and higher consumption of PE wax in compounding and packaging industries. North America shows steady demand supported by established industrial production and the presence of major plastic processors, while Europe benefits from mature polymer applications and consistent usage across coatings and adhesives.

The Middle East & Africa region reflects gradual growth tied to rising industrialization and polymer-related developments, and Latin America continues to gain traction through increasing plastic production and compounding activities. With Asia Pacific clearly holding the largest share at 56.6%, the region remains the key growth engine of the Polyethylene Wax Market, outpacing all other regions in both value and application-level penetration.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE is positioned to play a solid role in the global Polyethylene Wax Market in 2025 due to its wide industrial polymer portfolio and long-standing presence in specialty materials. The company’s ability to integrate PE wax production with broader chemical chains gives it flexibility in cost management and product reliability. BASF’s portfolio strength supports applications in plastics processing, coatings, and adhesives—sectors that continue to rely on consistent, high-purity wax grades. With the company’s established global distribution capabilities, it remains one of the more stable suppliers in a market where quality consistency and scalable production matter heavily for converters and compounders.

For Clariant International, the 2025 outlook remains centered on value-added specialty wax solutions. Clariant’s expertise in creating tailored additives positions it well in applications requiring improved dispersion, lubrication, and processing efficiency. The company’s long-term focus on performance materials helps it meet customer needs for controlled melting points and optimized polymer interaction. Its strong foothold in color concentrates, masterbatches, and coatings further supports demand, as these sectors consistently adopt PE wax for smooth processing and improved end-product finish.

Meanwhile, Honeywell International Inc. maintains a competitive advantage through engineered wax technologies aligned with industrial-scale applications. Honeywell’s history in producing precision-grade materials supports sectors that depend on predictable thermal behavior and stable molecular properties. In 2025, its capability to supply consistent technical-grade polyethylene wax makes it relevant for processors seeking dependable additives across plastics, inks, and adhesives. Honeywell’s technical orientation keeps it a credible player in a market increasingly driven by performance and reliability.

Top Key Players in the Market

- BASF SE

- Clariant International

- Honeywell International Inc.

- Innospec Inc.

- Mitsui Chemicals America, Inc.

- Westlake Chemical Corporation

- Trecora Resources

- The Lubrizol Corporation

- EUROCERAS

- Qingdao Haihao Chemical Co., Ltd.

Recent Developments

- In April 2025, Clariant introduced Ceridust 1310, a new wax solution aimed at helping formulators who face supply issues with carnauba wax. This product provides a more consistent and reliable wax alternative for applications such as printing inks, addressing raw material volatility, and supporting smoother production planning.

- In March 2025, Honeywell named David Sewell as CEO of its Advanced Materials unit ahead of the planned spin-off. This unit is expected to become Solstice Advanced Materials, a business focused on sustainable specialty materials and chemicals, which connects closely with the chemicals and industrial materials segments.

Report Scope

Report Features Description Market Value (2025) USD 1.8 Billion Forecast Revenue (2035) USD 3.0 Billion CAGR (2026-2035) 5.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Low Density Polyethylene, High Density Polyethylene, Oxidized Polyethylene, Others), By Processing Method (Polymerization, Chemical Modification, Physical Blending), By Application (Coating (Powder Coating, Pastile Coating), Plastics and Polymer, Hot Melt Adhesive, Candles, Rubber, Cosmetics and Pharmaceuticals, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF SE, Clariant International, Honeywell International Inc., Innospec Inc., Mitsui Chemicals America, Inc., Westlake Chemical Corporation, Trecora Resources, The Lubrizol Corporation, EUROCERAS, Qingdao Haihao Chemical Co., Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Polyethylene Wax MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Polyethylene Wax MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- Clariant International

- Honeywell International Inc.

- Innospec Inc.

- Mitsui Chemicals America, Inc.

- Westlake Chemical Corporation

- Trecora Resources

- The Lubrizol Corporation

- EUROCERAS

- Qingdao Haihao Chemical Co., Ltd.

Our Clients

- 179361

- February 2026