Global Polyester Polyol Market Size, Share, And Enhanced Productivity By Product Type (Aliphatic Polyester Polyols, Aromatic Polyester Polyols), By Type (Flexible Polyol, Rigid Polyol, Thermoplastic Polyol), By Physical State (Liquid, Solid), By Production Process (Batch Process, Continuous Process), By Source (Petroleum-Based, Bio-Based), By Application (Flexible Foam, Rigid Foam, Coatings, Adhesives, Sealants, Elastomers, Packaging, Others), By End-User (Furniture, Automotive, Construction, Electronics, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179469

- Number of Pages: 242

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- By Product Type Analysis

- By Type Analysis

- By Physical State Analysis

- By Production Process Analysis

- By Source Analysis

- By Application Analysis

- By End-User Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

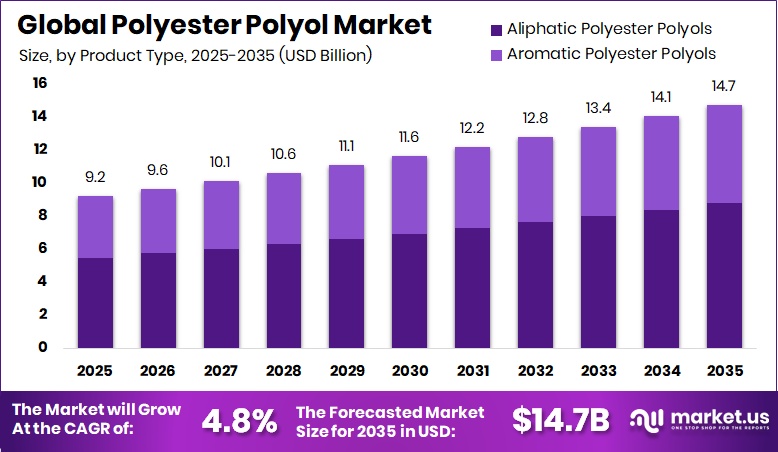

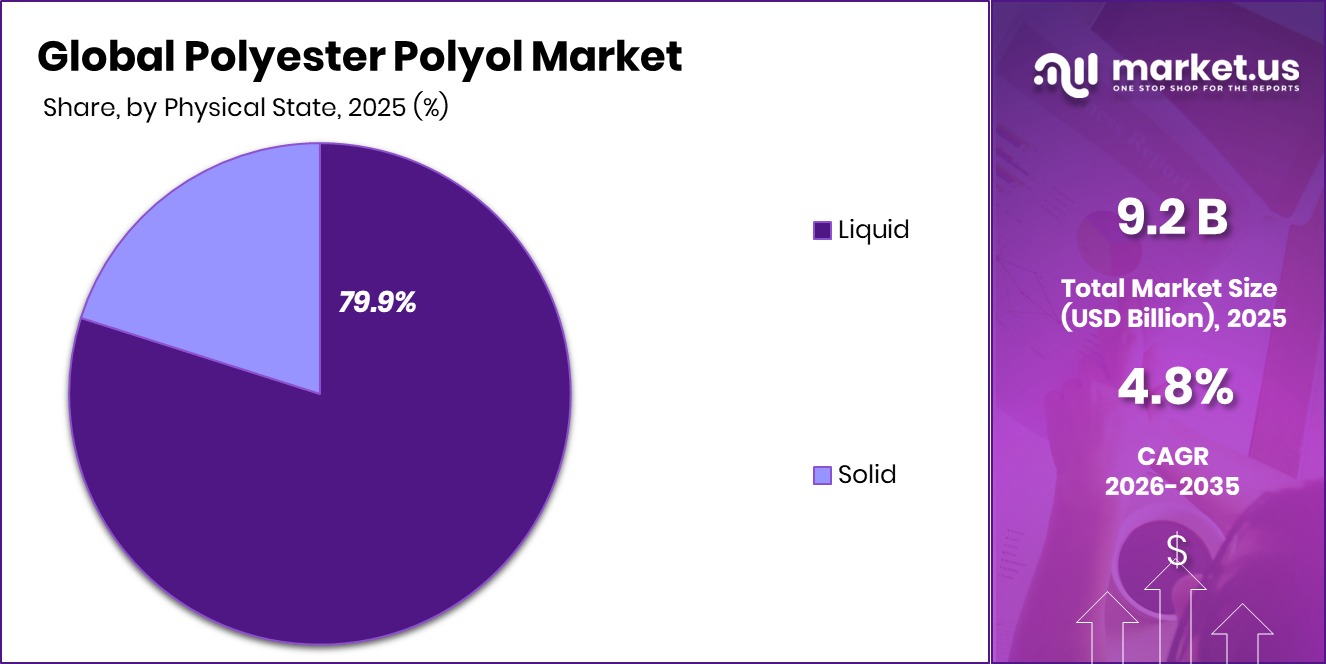

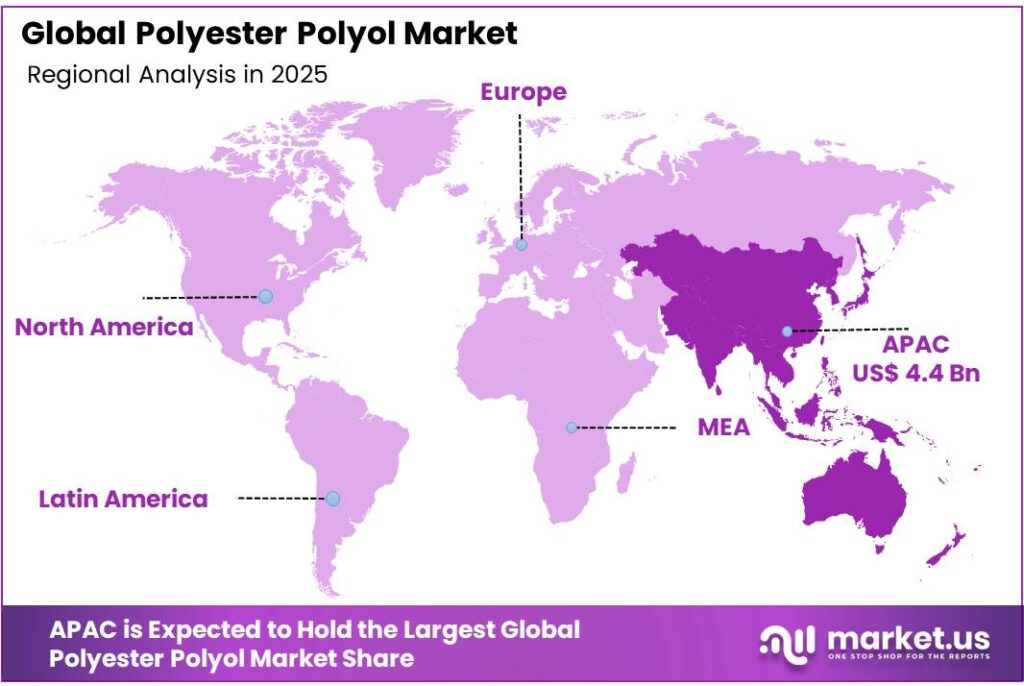

The Global Polyester Polyol Market is expected to be worth around USD 14.7 billion by 2035, up from USD 9.2 billion in 2025, and is projected to grow at a CAGR of 4.8% from 2026 to 2035. The region Asia Pacific dominated with 48.6% valued at USD 4.4 Bn.

The global Polyester Polyol Market is structured across multiple product and application layers, including aliphatic and aromatic grades, flexible and rigid polyols, liquid and solid forms, and production routes such as batch and continuous processes. These polyols support a wide range of applications—flexible and rigid foams, coatings, adhesives, sealants, elastomers, and packaging—serving end-use sectors like furniture, automotive, construction, and electronics. Their role in polyurethane systems makes them essential materials for comfort products, insulation, protective surfaces, and performance-driven industrial components.

Polyester polyol is a chemical building block made by reacting diacids with diols, creating a versatile polymer used to produce polyurethane foams, coatings, and industrial materials. It offers durability, chemical resistance, and mechanical strength, making it valuable for flexible cushioning, rigid insulation boards, and protective coatings.

The Polyester Polyol Market represents the global demand, production, and application adoption of these specialty polymers across industries. It reflects how manufacturers rely on polyester polyols to enhance product performance, extend material life, and support engineering requirements in both consumer and industrial environments.

Growth in this market is supported by stronger demand for high-performance coatings, insulation materials, and durable foams. Funding activities such as Ecot securing €21 million, NxLite raising $9.2 million, and EU support of €4 million for natural coatings highlight rising innovation. Additional momentum comes from Flō Optics’ $35 million funding and Graphite Innovation & Technologies receiving $10 million to advance surface-improving coatings.

Opportunities expand as industries explore better material efficiency and new coating technologies. Investments like Anaphite’s £1.4 million funding for dry-coating advancements and AssetCool’s £10 million round reflect strong interest in next-generation engineered surfaces that align with polyester polyol-based application growth.

Key Takeaways

- The Global Polyester Polyol Market is expected to be worth around USD 14.7 billion by 2035, up from USD 9.2 billion in 2025, and is projected to grow at a CAGR of 4.8% from 2026 to 2035.

- Polyester Polyol Market sees strong momentum as aliphatic polyester polyols dominate with a 59.7% share.

- Growing demand boosts the Polyester Polyol Market, where flexible polyol leads applications with 51.3% dominance today.

- Liquid polyols strengthen the Polyester Polyol Market, maintaining an impressive 79.9% share across global industries.

- Batch processing drives the Polyester Polyol Market, securing 81.2% usage due to efficiency and consistent quality.

- Petroleum-based inputs remain essential, giving the Polyester Polyol Market a commanding 82.5% sourcing share globally.

- Flexible foam applications support the Polyester Polyol Market, contributing 44.4% share within major manufacturing sectors.

- Furniture end-users continue shaping the Polyester Polyol Market, holding 39.2% share through steady product demand.

- In the Asia Pacific, the Polyester Polyol Market reached USD 4.4 Bn, capturing 48.6%.

By Product Type Analysis

Polyester Polyol Market sees Aliphatic Polyester Polyols leading strongly with 59.7% share.

In 2025, the Polyester Polyol Market continues to see strong demand for aliphatic polyester polyols, which hold a 59.7% share, making them the leading product segment. Their popularity grows as industries prefer materials that offer better UV stability, low yellowing, and long outdoor durability. Manufacturers in coatings, adhesives, and elastomers rely heavily on aliphatic grades because they help improve final product performance.

Automotive and construction sectors also boost usage as the need for weather-resistant surfaces rises. With global industries moving toward higher-quality polyurethane production, aliphatic polyols remain essential due to their strong balance between performance and processing ease. This segment’s leadership reflects consistent industrial adoption and the shift toward premium polyurethane materials.

By Type Analysis

Flexible Polyol dominates the Polyester Polyol Market, accounting for a major 51.3% portion.

In 2025, flexible polyols dominate the Polyester Polyol Market with a 51.3% share, driven by rising consumption in cushioning, furniture materials, and automotive interiors. Their softness, resilience, and lightweight performance make them important for foam production across several consumer and industrial applications. The comfort-related industries—mattresses, sofas, seating systems—continue expanding, pushing manufacturers to increase output of flexible-grade polyols. They also support large-scale production of flexible polyurethane foams used in packaging and insulation.

As consumers become more quality-focused, flexible polyols benefit from the rising preference for durable and comfortable foam products. This segment’s stronghold highlights the ongoing shift toward materials that enhance comfort while maintaining reliability and affordability.

By Physical State Analysis

Liquid form holds 79.9% share, shaping trends in the Polyester Polyol Market.

In 2025, liquid polyester polyols hold a commanding 79.9% share, reflecting their widespread adoption across manufacturing processes. Liquid polyols simplify blending, allow better reaction control, and support consistent foam and coating production. Manufacturers prefer them because they provide efficient mixing with isocyanates, reduce processing time, and maintain uniform quality in polyurethane systems.

The growing use of liquid polyols in adhesives, flexible foams, and specialty coatings reinforces their dominance. Industries in construction and automotive continue to shift toward liquid grades due to their clear processing advantages. With production lines prioritizing smooth operation and reduced waste, liquid polyester polyols remain the preferred choice for large-scale and high-quality polyurethane applications.

By Production Process Analysis

Batch Process production steers the Polyester Polyol Market with its notable 81.2% share.

In 2025, the batch process accounts for 81.2% of polyester polyol production, reflecting its reliability and flexibility for different formulations. Manufacturers rely on batch systems because they support precise control over reaction conditions, allowing tailored polyol properties for specialized polyurethane applications. This process suits industries that require consistent batches with specific performance parameters, such as automotive interior materials, high-grade coatings, and foam systems.

Batch production also helps producers manage diverse product portfolios without compromising quality. Its strong share indicates that despite advancements in continuous processing, industries still favor the customizability and lower production risk offered by batch systems. This preference ensures stable output, repeatability, and versatility for varied polyester polyol requirements.

By Source Analysis

Petroleum-Based sources lead the Polyester Polyol Market, capturing a significant 82.5% share.

In 2025, petroleum-based polyester polyols continue to command an 82.5% market share, supported by their widespread availability, cost advantages, and well-established production infrastructure. These polyols offer predictable performance and are deeply integrated into manufacturing lines for foams, coatings, adhesives, and elastomers. While bio-based options are emerging, petroleum-derived grades remain the industry standard due to their processing familiarity and consistent chemical properties.

Industries such as automotive, furniture, and construction rely heavily on these polyols to maintain stable supply chains. Although sustainability initiatives are gradually promoting greener alternatives, petroleum-based polyols still dominate because they meet large-scale industrial needs without high cost or formulation changes. Their strong presence reflects entrenched manufacturing ecosystems.

By Application Analysis

Flexible Foam applications represent 44.4% demand within the Polyester Polyol Market landscape.

In 2025, flexible foam applications represent 44.4% of polyester polyol consumption, driven by strong demand from furniture, bedding, transportation seating, and packaging materials. These foams provide comfort, cushioning, and lightweight structural support, making them widely used in consumer and industrial goods. With rising living standards and rapid urban development, the need for comfortable interiors and durable foam components continues to rise.

Flexible foams benefit from advancements in polyurethane chemistry, allowing better elasticity, durability, and long-term performance. Their broad applicability—from sofas and mattresses to vehicle seats and protective packaging—keeps this segment at the forefront of market demand. The segment’s strong share highlights flexible foam’s essential role across daily-use products.

By End-User Analysis

Furniture end-users contribute 39.2% demand, anchoring growth in the Polyester Polyol Market.

In 2025, the furniture industry holds a 39.2% share in the Polyester Polyol Market, reflecting rising demand for high-quality cushioning materials, durable foam components, and long-lasting surface coatings. Modern furniture manufacturers rely on polyester polyols to create comfortable, resilient polyurethane foams used in sofas, chairs, mattresses, and ergonomic seating. The global expansion of residential and commercial real estate development further increases furniture demand.

Growing consumer expectations for comfort and durability support the steady use of polyols in upholstered furniture and bedding products. As home décor spending increases and lifestyle upgrades continue worldwide, the furniture segment remains a major driver of polyester polyol consumption, sustaining its strong position in the market.

Key Market Segments

By Product Type

- Aliphatic Polyester Polyols

- Aromatic Polyester Polyols

By Type

- Flexible Polyol

- Rigid Polyol

- Thermoplastic Polyol

By Physical State

- Liquid

- Solid

By Production Process

- Batch Process

- Continuous Process

By Source

- Petroleum-Based

- Bio-Based

By Application

- Flexible Foam

- Rigid Foam

- Coatings

- Adhesives

- Sealants

- Elastomers

- Packaging

- Others

By End-User

- Furniture

- Automotive

- Construction

- Electronics

- Others

Driving Factors

Rising forestry activities boost chainsaw adoption

The Polyester Polyol Market continues to benefit from rising demand for durable polyurethane materials used in foams, coatings, sealants, and industrial products. Industries prefer polyester polyols because they enhance strength, flexibility, and long-term performance. This growing need aligns with advancements in material science, where better bonding, resilience, and wear resistance are becoming essential.

Supporting this momentum, new funding developments like Sealonix securing $20 million to develop advanced hemostatic sealants show how performance-driven polymer technologies are attracting investment. Such funding highlights the broader push toward stronger and more efficient engineered materials, indirectly reinforcing the market’s interest in reliable polyol formulations across multiple application areas.

Restraining Factors

Volatile raw material prices are impacting production.

Volatile raw material prices remain a major challenge for polyester polyol producers, as fluctuations in petrochemical feedstocks disrupt cost planning and impact product availability. This instability makes it harder for manufacturers to maintain steady pricing and long-term supply commitments, especially when end-use sectors depend on predictable material costs.

The landscape is further influenced by healthcare material innovations, such as a VCU startup winning an $800k grant to advance infection-fighting surgical gel technologies. These external advancements show how investment is flowing toward alternative material systems, signaling competition for resources and innovation focus that may indirectly restrain attention on traditional polyester polyol routes.

Growth Opportunity

Increasing adoption in advanced insulation applications.

Opportunities emerge as advanced insulation applications grow in demand across construction, refrigeration, and industrial systems requiring efficient thermal control. Polyester polyols play an important role in enabling rigid and flexible insulation foams with enhanced durability.

Market momentum aligns with significant funding events such as Cohera Medical raising $26.3 million to expand surgical adhesive technologies and Tissium securing €50 million to develop next-generation glue for nerve and hernia repair. These investments reflect wider industry interest in high-performance polymer chemistry, creating indirect spillover benefits for polyester polyol producers positioned to support specialized material innovation.

Latest Trends

Shift toward sustainable polyester polyol formulations.

A major trend in the market is the shift toward sustainable polyester polyol formulations, as industries increasingly seek environmentally conscious materials with strong performance. This push includes interest in low-impact chemicals, circular materials, and advanced processing methods.

Recent funding developments underscore this transition, including Veltist winning CHF 150,000 to rethink surgical sealing and Aeroseal raising $67 million to scale sealing technologies globally. These investments show how innovation in material sealing, efficiency, and environmental performance is accelerating, encouraging broader adoption of progressive polyester polyol solutions that align with sustainability-focused advancements.

Regional Analysis

Asia Pacific leads the Polyester Polyol Market with a strong 48.6% share worth USD 4.4 Bn.

The Polyester Polyol Market shows varied regional performance across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, with Asia Pacific standing out as the clear leader. Asia Pacific dominates the market with a 48.6% share valued at USD 4.4 Bn, supported by strong manufacturing activity, expanding construction needs, and consistent growth in furniture and automotive production.

North America maintains steady demand, driven by polyurethane usage in insulation, cushioning, and industrial applications, while Europe continues to benefit from its well-established automotive and consumer goods sectors.

The Middle East & Africa region reflects gradual adoption as industrial infrastructure strengthens, and Latin America shows moderate progress supported by rising consumption of foams and coatings. Together, these regions form a balanced global landscape, with Asia Pacific’s scale and production depth securing its dominant position.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, BASF SE continues to play a central role in the global Polyester Polyol Market, backed by its broad chemical expertise and strong global manufacturing base. The company’s strategic focus on delivering consistent quality and scalable production supports widespread adoption across foam, coatings, and elastomer applications. BASF’s diversified product portfolio allows it to serve both high-performance industries and large-volume end users, reinforcing its position as a dependable supplier. With stable downstream demand from automotive, furniture, and construction sectors, BASF remains a key contributor to market stability and long-term growth.

Covestro AG maintains a strong competitive edge in 2025 due to its specialized material technologies and commitment to improving performance characteristics across polyester polyol grades. Its deep presence in polyurethane value chains enables it to serve customers seeking reliability, technical support, and efficient product integration. Covestro’s operational scale and material science capabilities make it influential in shaping product trends, particularly where durability and processing efficiency matter. Its focus on consistent output keeps it well-positioned in markets that depend on high-quality polyol systems.

Dow Inc. remains a significant force by leveraging its extensive chemical production network and long-standing experience in polyol technologies. The company’s ability to deliver stable supply, formulation flexibility, and well-engineered products strengthens its relationship with end-use industries. Dow’s broad customer footprint across insulation, foam comfort products, and industrial materials supports its sustained demand in 2025. Its operational efficiency and deep integration across chemical value chains help ensure resilience in shifting market conditions, reinforcing Dow’s role as a key global player.

Top Key Players in the Market

- BASF SE

- Covestro AG

- Dow Inc.

- Huntsman Corporation

- Mitsui Chemicals, Inc.

- LG Chem Ltd.

- Shell Chemicals

- Wanhua Chemical Group Co., Ltd.

- Sinopec Shanghai Petrochemical Co., Ltd.

- Kumho P&B Chemicals, Inc.

- Mitsubishi Chemical Corporation

- Evonik Industries AG

- Arkema S.A.

Recent Developments

- In July 2025, Covestro India partnered with CSIR-NCL to explore new ways to upcycle polyurethane waste into valuable chemicals. This initiative supports recycling of end-of-life polyurethane materials, potentially feeding back into polyol and related raw materials production, improving material circularity.

- In March 2025, BASF increased production capacity for polyester and polyurethane resin at its Caojing plant in Shanghai, more than doubling annual capacity from 8,000 to 18,800 metric tons. This expansion strengthens BASF’s ability to deliver core materials used in coatings and potentially polyester polyol-related systems for industrial uses.

Report Scope

Report Features Description Market Value (2025) USD 9.2 Billion Forecast Revenue (2035) USD 14.7 Billion CAGR (2026-2035) 4.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Aliphatic Polyester Polyols, Aromatic Polyester Polyols), By Type (Flexible Polyol, Rigid Polyol, Thermoplastic Polyol), By Physical State (Liquid, Solid), By Production Process (Batch Process, Continuous Process), By Source (Petroleum-Based, Bio-Based), By Application (Flexible Foam, Rigid Foam, Coatings, Adhesives, Sealants, Elastomers, Packaging, Others), By End-User (Furniture, Automotive, Construction, Electronics, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF SE, Covestro AG, Dow Inc., Huntsman Corporation, Mitsui Chemicals, Inc., LG Chem Ltd., Shell Chemicals, Wanhua Chemical Group Co., Ltd., Sinopec Shanghai Petrochemical Co., Ltd., Kumho P&B Chemicals, Inc., Mitsubishi Chemical Corporation, Evonik Industries AG, Arkema S.A. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Polyester Polyol MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Polyester Polyol MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- Covestro AG

- Dow Inc.

- Huntsman Corporation

- Mitsui Chemicals, Inc.

- LG Chem Ltd.

- Shell Chemicals

- Wanhua Chemical Group Co., Ltd.

- Sinopec Shanghai Petrochemical Co., Ltd.

- Kumho P&B Chemicals, Inc.

- Mitsubishi Chemical Corporation

- Evonik Industries AG

- Arkema S.A.

Our Clients

- 179469

- February 2026