Global Perfume Market Size, Share, Growth Analysis By Product (Mass, Premium), By Ingredient (Natural, Synthetic), By End Use (Women, Men, Unisex), By Distribution Channel (Offline, Online), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179550

- Number of Pages: 348

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

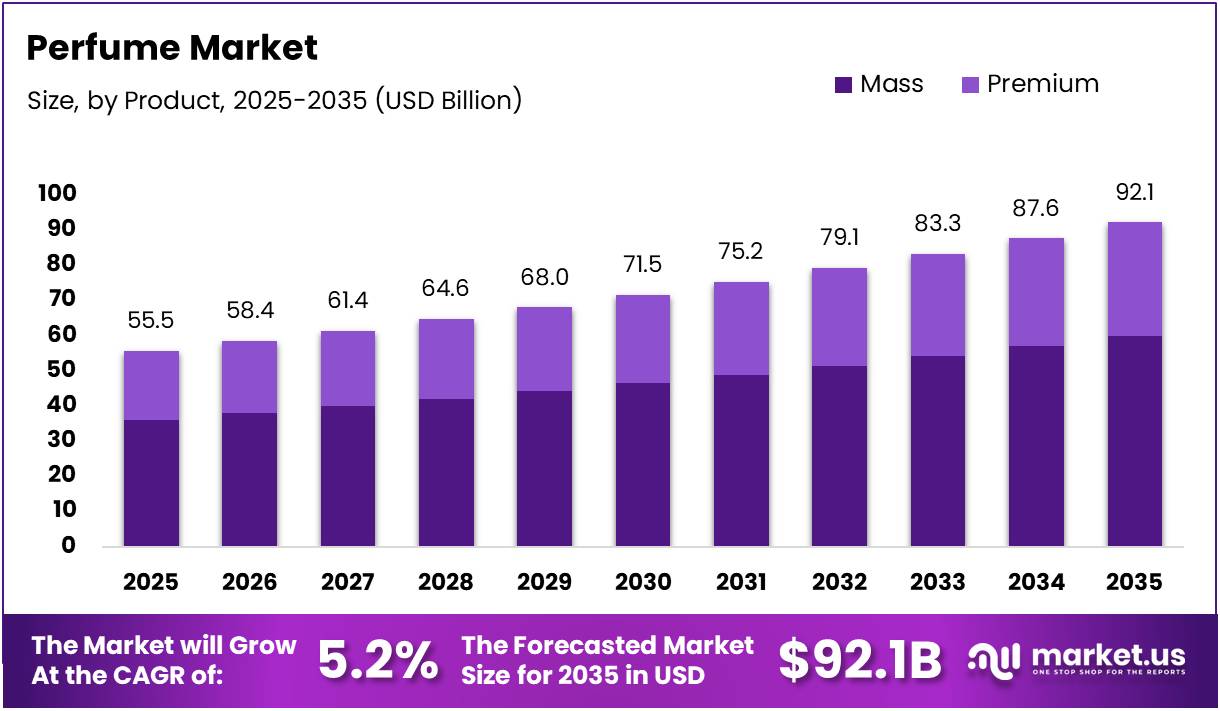

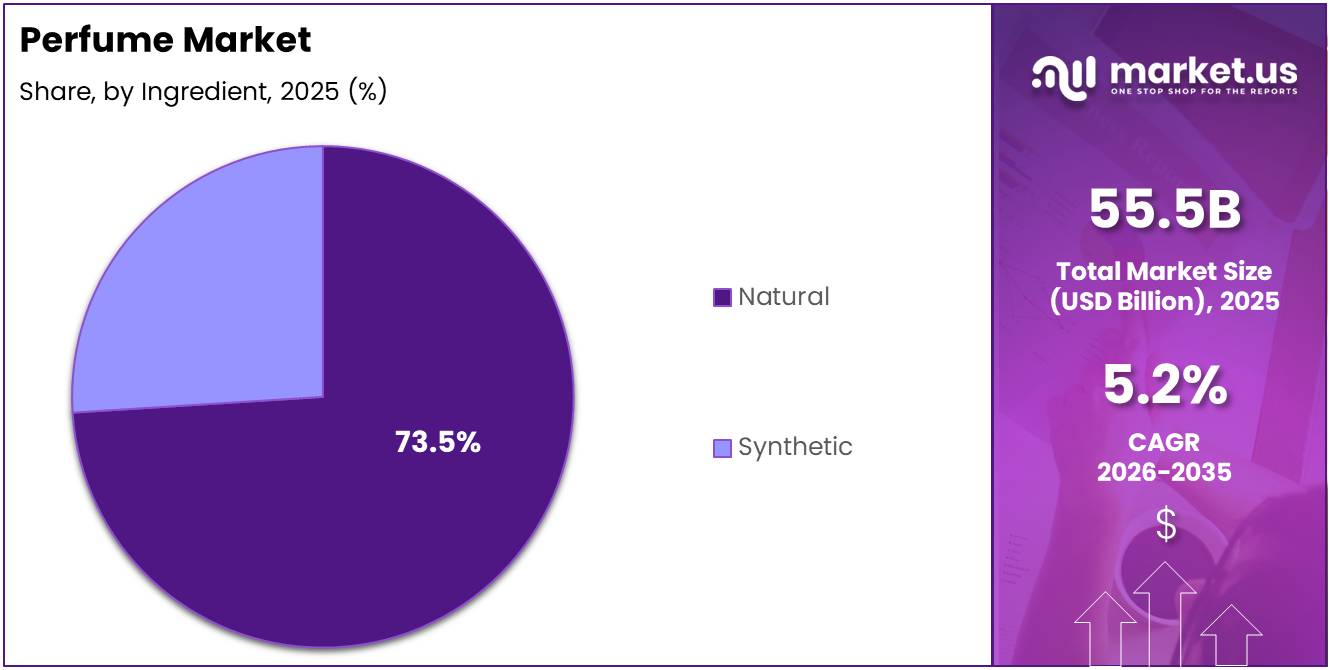

The Global Perfume Market size is expected to be worth around USD 92.1 Billion by 2035 from USD 55.5 Billion in 2025, growing at a CAGR of 5.2% during the forecast period 2026 to 2035.

The perfume market encompasses a broad range of scented products including eau de parfum, eau de toilette, and cologne formulations. These products are sold across mass and premium segments, catering to diverse consumer needs globally. The industry spans both natural and synthetic ingredient sources, supporting a wide spectrum of fragrances profiles.

Consumer demand for perfumes has shifted significantly over the last decade. Rising disposable incomes, growing urbanization, and evolving personal grooming habits are all accelerating market participation. Moreover, the influence of luxury branding and aspirational lifestyles has made fragrance a daily essential rather than an occasional luxury product.

Government regulations and ingredient safety standards continue to shape product formulations. Regulatory bodies in Europe and North America enforce strict allergen disclosure norms. Additionally, sustainability mandates are pushing brands to adopt eco-friendly packaging and responsibly sourced natural ingredients, creating new compliance-driven opportunities.

Premium and niche fragrance segments are witnessing accelerated expansion globally. Retail channels including departmental stores, specialty boutiques, and e-commerce platforms are broadening access to luxury fragrances. Consequently, brands are investing heavily in omnichannel strategies to reach both urban and emerging market consumers effectively.

According to Harper’s Bazaar, approximately 50% of U.S. adults now apply perfume daily, with that figure rising to 79% among consumers aged 18 to 34 in 2025. Additionally, according to In-Cosmetics, floral scents are the most preferred globally, with 30% of consumers choosing them, followed by fresh scents at 24%, fruity at 23%, and citrus at 22%.

According to YouGov, 45% of American perfume users repurchase one or two favorite scents, indicating strong brand loyalty. Furthermore, according to The Essence Vault, women (81%) are more likely than men (56%) to wear perfume on a daily basis, highlighting a key gender-driven usage gap.

Key Takeaways

- The global Perfume Market was valued at USD 55.5 Billion in 2025 and is projected to reach USD 92.1 Billion by 2035.

- The market is expected to grow at a CAGR of 5.2% during the forecast period 2026 to 2035.

- By Product, Mass segment dominated with a share of 65.3% in 2025.

- By Ingredient, Natural segment led the market with a share of 73.5% in 2025.

- By End Use, Women segment held the largest share at 62.8% in 2025.

- By Distribution Channel, Offline segment accounted for 69.1% of market share in 2025.

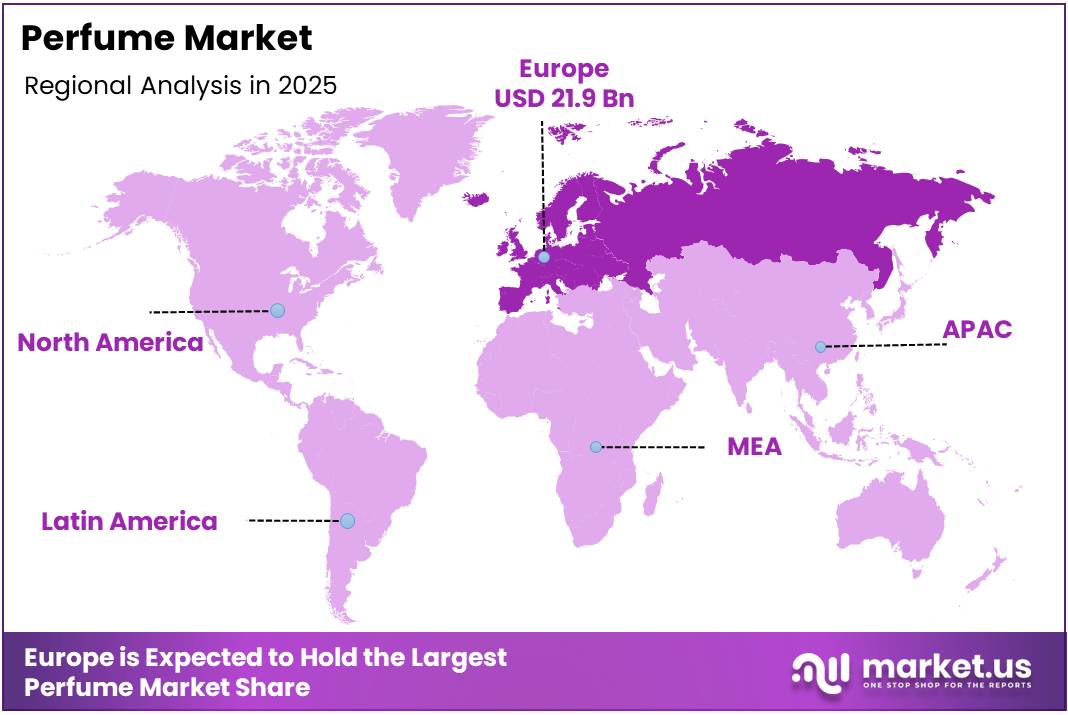

- Europe dominated the global Perfume Market with a share of 39.6%, valued at USD 21.9 Billion in 2025.

By Product Analysis

Mass dominates with 65.3% due to wide accessibility and affordable price points across global retail channels.

In 2025, Mass held a dominant market position in the By Product segment of the Perfume Market, with a 65.3% share. Mass fragrances are widely distributed through supermarkets, drugstores, and e-commerce platforms. Their affordability makes them accessible to a broad consumer base across both developed and emerging economies.

The Premium segment, while smaller in volume, contributes significantly to overall market revenue. Consumers increasingly associate premium fragrances with luxury, identity, and status. Moreover, the growing middle class in Asia Pacific and Latin America is shifting aspirational spending toward premium and designer scent categories.

By Ingredient Analysis

Natural dominates with 73.5% due to rising consumer preference for clean, sustainable, and skin-friendly fragrance formulations.

In 2025, Natural held a dominant market position in the By Ingredient segment of the Perfume Market, with a 73.5% share. Consumers are increasingly drawn to fragrances made from botanical extracts, essential oils, and plant-based ingredients. This preference is driven by growing awareness around skin safety and environmental sustainability.

The Synthetic ingredient segment continues to play a critical role in fragrance development. Synthetic molecules offer consistent quality, cost efficiency, and the ability to replicate rare or endangered natural materials. Consequently, many brands blend synthetic and natural ingredients to achieve both performance and sustainability goals.

By End Use Analysis

Women dominates with 62.8% due to higher daily usage frequency and broader product variety within female-targeted fragrance lines.

In 2025, Women held a dominant market position in the By End Use segment of the Perfume Market, with a 62.8% share. Women consistently demonstrate higher fragrance purchase frequency and brand loyalty. Additionally, floral, fruity, and oriental scent families have driven strong repeat purchases within this demographic globally.

The Men segment is growing steadily, supported by evolving grooming habits and increased male interest in personal care products. Fragrance is becoming a key component of everyday male grooming routines. Moreover, brands are expanding their men’s fragrance lines with bold, modern scent profiles designed to appeal to a younger and more style-conscious male audience.

The Unisex segment is gaining strong momentum as consumers increasingly embrace gender-neutral identities and inclusive personal care choices. Younger demographics, particularly millennials and Gen Z, are driving demand for fragrances that transcend traditional gender boundaries. Consequently, brands are actively launching gender-fluid collections to meet this growing and commercially significant consumer preference.

By Distribution Channel Analysis

Offline dominates with 69.1% due to the sensory nature of fragrance shopping, which favors in-store testing and trial experiences.

In 2025, Offline held a dominant market position in the By Distribution Channel segment of the Perfume Market, with a 69.1% share. Physical retail stores, including department stores and specialty fragrance boutiques, remain the preferred purchase point. Consumers value the ability to test scents directly before making a buying decision.

The Online distribution channel is growing rapidly, driven by digital convenience and expanding e-commerce infrastructure. Social media discovery and influencer recommendations are converting online browsers into buyers. Moreover, subscription fragrance services and virtual scent-matching tools are enhancing digital purchase confidence for new consumers.

Key Market Segments

By Product

- Mass

- Premium

By Ingredient

- Natural

- Synthetic

By End Use

- Women

- Men

- Unisex

By Distribution Channel

- Offline

- Online

Drivers

Rising Urbanization and Aspirational Lifestyles Drive Global Perfume Market Growth

Rapid urbanization across emerging economies is significantly expanding the consumer base for perfumes. As more people migrate to cities and adopt aspirational lifestyles, fragrance becomes an integral part of daily grooming routines. This shift is particularly visible in markets across Asia Pacific, Latin America, and the Middle East.

Celebrity and designer fragrance endorsements play a powerful role in shaping consumer purchase decisions. When high-profile personalities promote a scent, it creates immediate aspirational demand. Consequently, brands are investing heavily in licensing agreements and limited-edition celebrity collaborations to capture attention and drive retail traffic.

The expansion of premium and niche fragrance retail channels is further supporting market growth. Specialty boutiques, luxury department stores, and curated online platforms are increasing product visibility. Moreover, growing consumer interest in exclusive and artisanal scents is fueling demand for specialized retail formats beyond mainstream outlets.

Restraints

Stringent Regulatory Requirements and Product Substitution Limit Perfume Market Expansion

Regulatory compliance is a significant challenge for perfume manufacturers operating globally. Strict rules on fragrance ingredient safety, allergen labeling, and chemical disclosure add complexity to product development and market entry. These requirements increase R&D costs and can delay product launches, particularly for smaller and emerging fragrance brands.

The International Fragrance Association and regional regulatory bodies continuously update restricted ingredient lists. Brands must regularly reformulate existing products to maintain compliance. Therefore, manufacturers face ongoing operational costs related to testing, documentation, and ingredient substitution, which can reduce profit margins significantly.

High product substitution from deodorants, body mists, and alternative fragrance formats presents another key restraint. Many consumers, particularly in price-sensitive markets, opt for these lower-cost alternatives instead of traditional perfumes. Additionally, the growing variety of substitute products makes it harder for perfume brands to retain casual or infrequent fragrance users.

Growth Factors

Personalization, Inclusivity, and Sustainability Create New Perfume Market Growth Opportunities

Personalized and custom-blended fragrance solutions are emerging as a high-growth opportunity within the perfume market. Consumers increasingly seek scents that reflect their individual personalities and preferences. Brands offering bespoke fragrance experiences, both in-store and online, are attracting premium customers willing to pay more for exclusivity.

Growing demand for gender-neutral and inclusive fragrance portfolios is reshaping product development strategies. Younger consumers, particularly millennials and Gen Z, are rejecting traditional gender binaries in scent categorization. Consequently, brands launching unisex and fluid fragrance lines are gaining strong traction across key global markets.

Development of sustainable, refillable, and eco-friendly packaging formats presents a significant opportunity for market differentiation. Environmentally conscious consumers are actively choosing brands that align with their values. Moreover, refillable perfume systems reduce packaging waste and offer long-term cost savings, making them attractive to both consumers and sustainability-focused retailers.

Emerging Trends

Digital Discovery, Concentration Preferences, and Layering Trends Reshape the Perfume Market

Social media platforms are transforming how consumers discover and engage with fragrance brands. Influencer-led reviews, TikTok fragrance content, and YouTube tutorials are driving rapid brand awareness among younger audiences. Consequently, brands are shifting marketing budgets toward digital channels to capitalize on this growing fragrance discovery ecosystem.

Increasing consumer preference for long-lasting Eau de Parfum concentrations is influencing product development strategies. Shoppers are prioritizing value and performance, seeking fragrances that stay throughout the day. Therefore, brands are expanding their EDP offerings and reformulating existing lines to deliver higher concentration and improved longevity.

The rising popularity of fragrance layering is creating new cross-sell and upsell opportunities. Consumers are combining multiple scent products, such as body lotions, hair mists, and perfumes, to build unique personal fragrance profiles. Moreover, brands are launching curated layering sets to encourage multi-product purchases and deepen customer engagement.

Regional Analysis

Europe Dominates the Perfume Market with a Market Share of 39.6%, Valued at USD 21.9 Billion

Europe holds a commanding position in the global perfume market, accounting for 39.6% of total market share and valued at USD 21.9 Billion in 2025. The region’s dominance is rooted in its deep fragrance heritage, home to iconic luxury houses in France, Italy, and the UK. Strong consumer spending on premium and niche fragrances continues to reinforce Europe’s leadership position.

North America Perfume Market Trends

North America represents one of the largest and fastest-evolving fragrance markets globally. The United States leads consumption, supported by high daily usage rates and a growing appetite for premium and indie fragrance brands. Additionally, robust e-commerce infrastructure and strong influencer marketing activity are accelerating online fragrance sales across the region.

Asia Pacific Perfume Market Trends

Asia Pacific is the fastest-growing regional market, driven by rising disposable incomes and urbanization across China, India, and Southeast Asia. Growing exposure to global fragrance brands through digital channels is elevating consumer awareness. Moreover, local fragrance culture, particularly in the Middle East-influenced markets within APAC, is supporting premium product adoption.

Middle East and Africa Perfume Market Trends

The Middle East holds a uniquely strong fragrance culture, with oud, musk, and oriental blends deeply embedded in regional traditions. High consumer spending on luxury perfumes drives a premium-heavy market across GCC countries. Furthermore, rising tourism and duty-free retail channels are contributing to sustained fragrance demand across the broader MEA region.

Latin America Perfume Market Trends

Latin America presents solid growth potential for perfume brands, particularly in Brazil and Mexico. Increasing brand awareness, a growing middle class, and rising female workforce participation are expanding fragrance consumption. However, economic volatility and currency fluctuations in key markets remain factors that brands must navigate when developing regional pricing strategies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Avon has maintained a broad global presence through its direct-selling model, which gives it unmatched reach in emerging markets. The company’s fragrance portfolio spans affordable mass-market options to mid-tier products. Moreover, Avon’s established distributor network continues to drive fragrance penetration in regions where traditional retail infrastructure remains limited.

CHANEL remains one of the most recognizable luxury fragrance houses globally, with iconic products that command premium pricing and exceptional brand loyalty. The company invests significantly in heritage-driven marketing and in-store experiences. Additionally, CHANEL’s selective distribution strategy reinforces its exclusivity positioning, making its fragrances aspirational across both mature and emerging markets.

Coty Inc. operates across both mass and prestige fragrance segments, giving it strategic flexibility in responding to shifting consumer demand. The company manages a diverse portfolio of licensed celebrity and designer fragrances. Consequently, Coty’s ability to leverage high-profile brand partnerships has strengthened its competitive standing in department store and specialty retail channels.

LVMH Moet Hennessy-Louis Vuitton is a dominant force in the global luxury fragrance space, with a portfolio that includes Dior and Givenchy among other prestige brands. LVMH’s vertical integration across production, distribution, and retail provides a significant competitive advantage. Furthermore, the group’s continued investment in brand storytelling and immersive retail experiences drives sustained consumer engagement and premium pricing power.

Key Players

- Avon

- CHANEL

- Coty Inc.

- LVMH Moet Hennessy-Louis Vuitton

- The Estée Lauder Companies

- Revlon

- Puig

- L’Oréal

- Shiseido Company, Ltd.

- Givaudan

- Hermès

- KERING

Recent Developments

- December 2025 – Givaudan completed its acquisition of fragrance player Belle Aire Creations, strengthening its reach with local and regional customers in the US market. This strategic move expands Givaudan’s North American footprint and broadens its customer base across the independent and regional fragrance manufacturing segment.

- November 2025 – Fragrance manufacturer Mäurer & Wirtz GmbH & Co. KG announced its acquisition of Herbert Stricker Classic Parfums GmbH and The Nose Behind GmbH. This dual acquisition is expected to broaden Mäurer & Wirtz’s fragrance development capabilities and deepen its presence in the European specialty fragrance sector.

- October 2025 – L’Oréal agreed to acquire the luxury beauty and fragrance business of French luxury group Kering in a major strategic deal valued at approximately €4 Billion. This transaction significantly strengthens L’Oréal’s position in the global prestige fragrance and luxury beauty market.

- July 2025 – Turpaz Industries Ltd. announced the completion of its acquisition of a controlling stake of 68.6% in French fragrance company Attractive Scent SAS, for EUR 27.4 Million (USD 32.3 Million). This deal expands Turpaz’s European fragrance manufacturing presence and adds a new premium French brand to its portfolio.

- July 2025 – Phlur was acquired by TSG Consumer Partners amid rising consumer demand for indie and direct-to-consumer fragrance brands. This acquisition reflects growing investor confidence in the independent fragrance segment as a high-growth opportunity within the broader perfume market.

Report Scope

Report Features Description Market Value (2025) USD 55.5 Billion Forecast Revenue (2035) USD 92.1 Billion CAGR (2026-2035) 5.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Mass, Premium), By Ingredient (Natural, Synthetic), By End Use (Women, Men, Unisex), By Distribution Channel (Offline, Online) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Avon, CHANEL, Coty Inc., LVMH Moet Hennessy-Louis Vuitton, The Estée Lauder Companies, Revlon, Puig, L’Oréal, Shiseido Company Ltd., Givaudan, Hermès, KERING Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Avon

- CHANEL

- Coty Inc.

- LVMH Moet Hennessy-Louis Vuitton

- The Estée Lauder Companies

- Revlon

- Puig

- L'Oréal

- Shiseido Company, Ltd.

- Givaudan

- Hermès

- KERING

Our Clients

- 179550

- Feb 2026