Global Paraffin Wax And Emulsions Market Size, Share, And Enhanced Productivity By Type(Natural, Synthetic), By Product Type (Paraffin Wax, Paraffin Emulsion), By Grade (Fully Refined, Semi-Refined, Unrefined), By Application (Leather, Construction, Agriculture, Paper, Paints and Coatings, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180002

- Number of Pages: 302

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

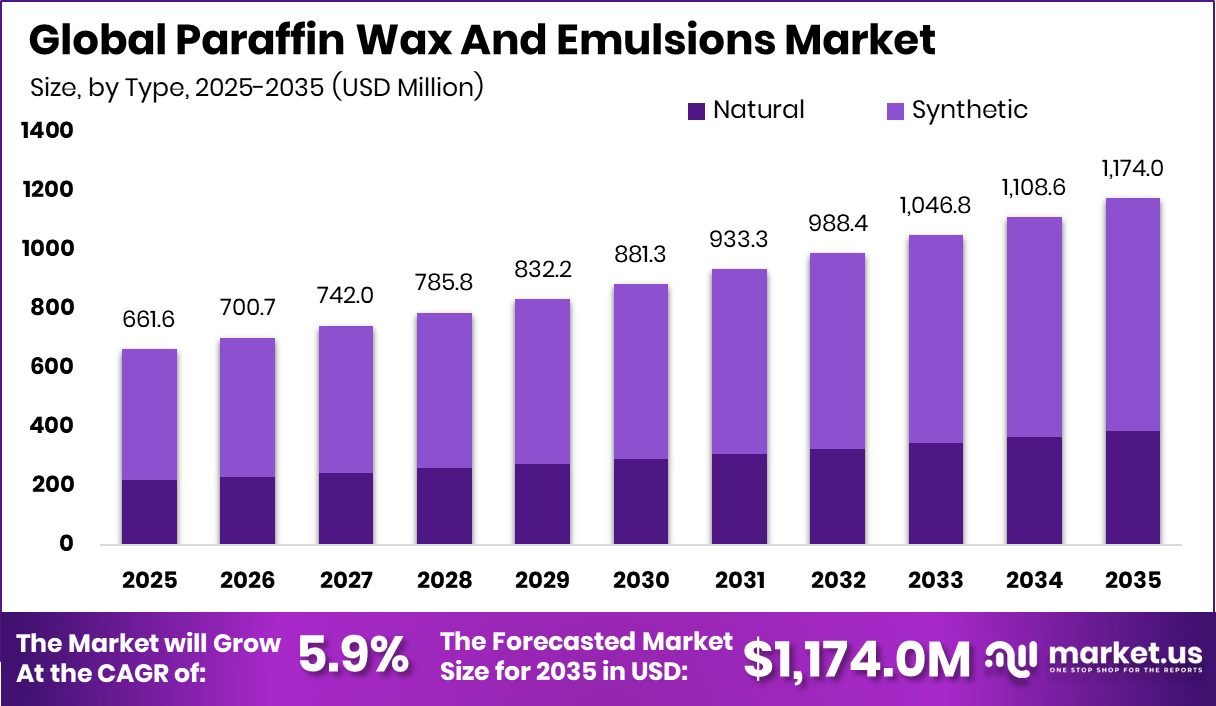

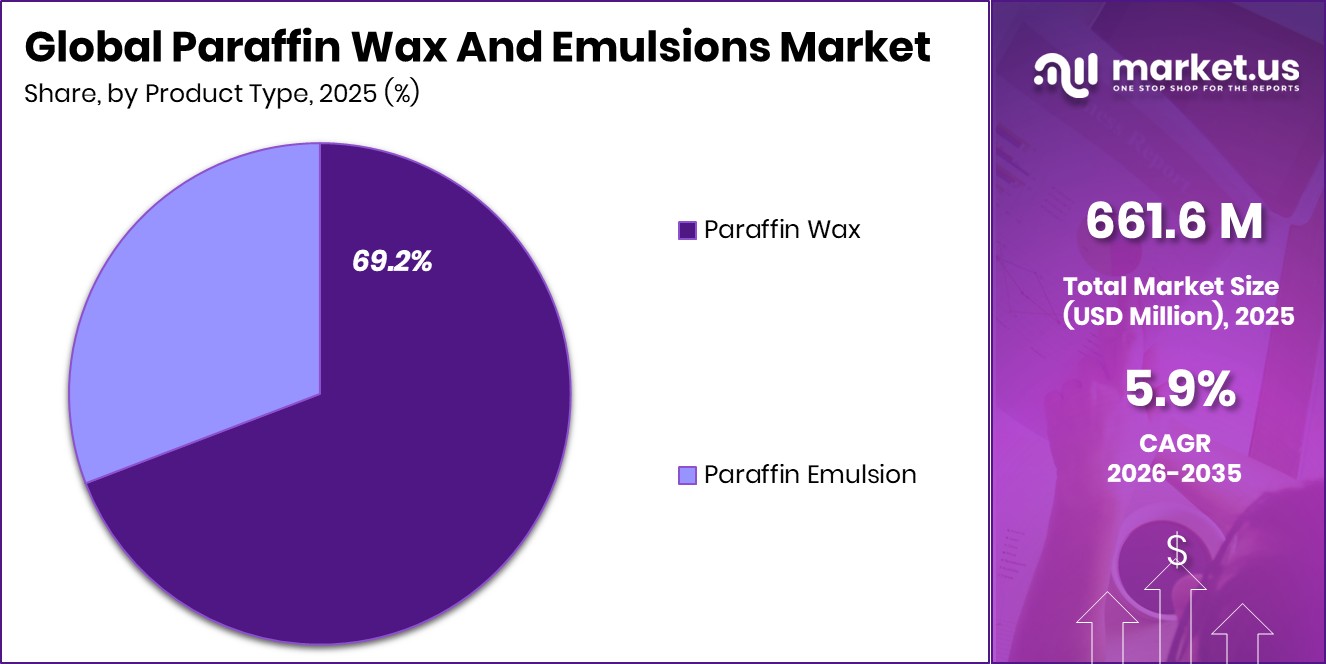

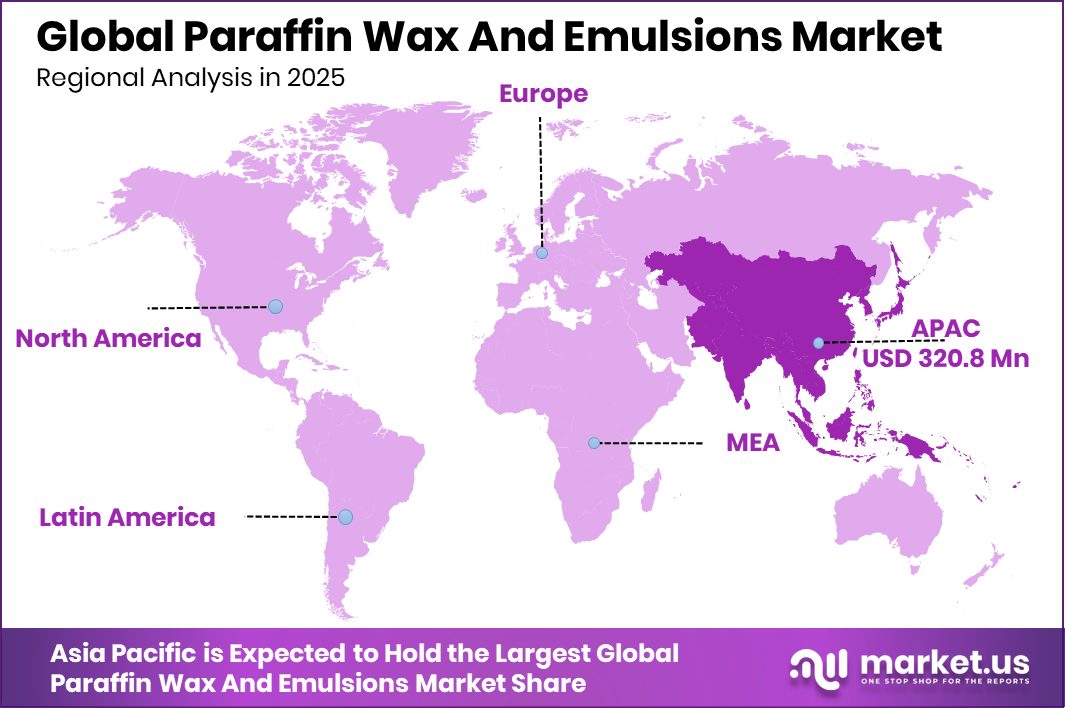

The Global Paraffin Wax And Emulsions Market is expected to be worth around USD 1,174.0 million by 2035, up from USD 661.6 million in 2025, and is projected to grow at a CAGR of 5.9% from 2026 to 2035. Asia Pacific recorded 48.5%, valued at USD 320.8 Mn, driving strong market expansion.

Paraffin wax and emulsions are material systems made from natural or synthetic waxes that are blended or dispersed to create products used in coatings, leather finishing, paper treatment, construction chemicals, and agricultural formulations. These materials offer water resistance, smooth film properties, and protective performance, making them reliable for many industrial and commercial applications.

The Paraffin Wax and Emulsions Market covers the production and use of natural and synthetic grades, including fully refined, semi-refined, and unrefined types supplied across industries such as leather, construction, agriculture, paper, and paints and coatings.

One of the main growth factors comes from rising interest in improved coating performance and protective layers. This is reinforced by funding activity across the broader materials and chemical space, such as the $20M raised by a decarbonization tech startup from United and Microsoft, which signals ongoing investment flow that indirectly supports innovation in formulation ingredients.

Demand continues to build in paper, construction, and paints, where paraffin emulsions help improve durability and resistance. Developments such as Ecoat securing €21 million to reinvent paint sustainably show how the coatings ecosystem remains active and open to performance-enhancing ingredients.

Opportunities also come from restructuring and portfolio shifts across chemicals, highlighted by moves such as Univar Solutions being acquired by Apollo Funds for $8.1B, BASF considering a €7 billion coatings unit sale, and AkzoNobel selling its Specialty Chemicals unit for €10.1 billion, all creating openings for suppliers of wax and emulsion technologies to strengthen customer reach and product positioning.

Key Takeaways

- The Global Paraffin Wax And Emulsions Market is expected to be worth around USD 1,174.0 million by 2035, up from USD 661.6 million in 2025, and is projected to grow at a CAGR of 5.9% from 2026 to 2035.

- The Paraffin Wax and Emulsions Market grows steadily as synthetic types dominate with 67.3% share.

- Strong demand continues as paraffin wax products lead the market landscape with a 69.2% contribution.

- Fully refined grades strengthen market structure, holding 58.1% preference across industrial and commercial applications.

- Paints and coatings drive key usage, accounting for 38.8% of total application demand.

- In the Asia Pacific, the market achieved USD 320.8 Mn with 48.5% dominance.

By Type Analysis

Paraffin Wax and Emulsions Market shows the synthetic segment dominating with 67.3%.

In 2025, the Paraffin Wax and Emulsions Market is expected to continue shifting toward synthetic types, which already account for 67.3%, reflecting stronger demand for controlled performance and purity in industrial formulations. The dominance of synthetic material is supported by steady consumption in packaging, rubber processing, cosmetics, and building materials, where consistent melting behavior and stability matter.

Many manufacturers are also focusing on improving supply chains to avoid fluctuations seen in crude-derived paraffin sources. As industries move toward higher efficiency, synthetic grades are favored for better emulsification stability and improved compatibility with additives. This makes synthetic paraffin a central element for companies aiming to maintain quality, especially in sectors seeking reliable thermal and moisture-barrier properties.

By Product Type Analysis

Paraffin Wax and Emulsions Market highlights paraffin wax as the leading product at 69.2%.

In 2025, Paraffin Wax holds a strong 69.2% share in the overall product type category, highlighting its deep integration across consumer goods, candles, paper coating, packaging boards, and textile finishing. The material’s versatility and cost-effectiveness continue to strengthen its presence despite emerging alternatives. Manufacturers are expected to increase output to support growing downstream demand, particularly in regions with expanding packaging and construction activity.

Paraffin Wax remains preferred for applications requiring smooth finishing, water resistance, and controlled melting ranges. Its high adoption also reflects steady usage among medium-scale industries that rely on predictable supply and consistent performance. With steady demand in both industrial and consumer segments, Paraffin Wax maintains its role as the market’s anchor product.

By Grade Analysis

Paraffin Wax and Emulsions Market records fully refined grade holding strong 58.1% share.

In 2025, Fully Refined grades continue to lead the Paraffin Wax and Emulsions Market with 58.1%, driven by applications where purity and clarity matter the most. This grade is widely used in cosmetics, pharmaceuticals, polymer processing, and premium candle production due to its low oil content and stable structure.

As manufacturers aim to enhance product quality, fully refined wax becomes crucial for improving surface finish, odor control, and thermal consistency. Industries that require precise formulation—such as specialty coatings and adhesives—depend on this grade for reliability. With increasing consumer focus on clean ingredients and high-performance materials, fully refined paraffin gains more traction, ensuring steady growth for producers aligned with purity-focused markets.

By Application Analysis

Paraffin Wax and Emulsions Market sees paints and coatings application reaching 38.8%.

In 2025, Paints and Coatings represent 38.8% of the application share, confirming their role as a major driver in the Paraffin Wax and Emulsions Market. The sector uses paraffin emulsions to achieve better water resistance, anti-settling behavior, and enhanced surface protection across architectural, automotive, and industrial coatings. As infrastructure activities grow and protective coating standards tighten, demand for stable wax-emulsion additives rises.

Coating manufacturers increasingly incorporate paraffin emulsions to improve film smoothness and durability, especially in regions experiencing high humidity and temperature variations. With ongoing innovation in decorative and protective coatings, the use of paraffin emulsions remains essential for achieving uniform finishes and long-term performance in diverse environmental conditions.

Key Market Segments

By Type

- Natural

- Synthetic

By Product Type

- Paraffin Wax

- Paraffin Emulsion

By Grade

- Fully Refined

- Semi-Refined

- Unrefined

By Application

- Leather

- Construction

- Agriculture

- Paper

- Paints and Coatings

- Others

Driving Factors

Rising industrial demand supports wax consumption

Rising industrial demand supports wax consumption, which continues to shape the Paraffin Wax and Emulsions Market as more sectors rely on protective coatings, moisture barriers, and smooth finishing layers. Industries such as construction, packaging, leather processing, and paper treatment consistently use paraffin-based formulations to maintain durability and performance. This growing industrial activity aligns with broader momentum in the construction and logistics environment, highlighted when Veyor raised $10.5 million in Series A funding to grow its construction logistics platform.

Investment directed toward material movement, site coordination, and project expansion indirectly strengthens demand for wax emulsions used across surface preparation, coating protection, and processing improvements. As these industries scale, the need for stable, refined paraffin grades remains an essential driver.

Restraining Factors

Raw material volatility pressures overall pricing

Raw material volatility pressures overall pricing, especially as feedstocks linked to refining output and energy markets fluctuate based on global supply cycles. Variability in crude-derived inputs can create uncertainty for producers of natural and synthetic paraffin wax, making cost planning more complex for downstream users in coatings, paper, and construction chemicals. These challenges sit against a backdrop of rising energy-linked project financing, such as the

Construction Financing Complete for the 347-MW Texas Solar Power Project, which shows how capital movement in energy infrastructure can influence supply dynamics. When large-scale energy projects shift consumption patterns or compete for resources, the paraffin wax and emulsions segment experiences tighter margins and cautious purchasing behavior.

Growth Opportunity

Emerging markets are increasing the adoption of wax application

Emerging markets increasing wax application adoption offer strong openings as construction, agriculture, and packaging sectors expand their use of paraffin emulsions for moisture protection, surface enhancement, and processing efficiency. These regions often upgrade infrastructure, expand manufacturing, and invest in climate-resilient projects, supported by funding such as the record £85m flood investment announced during the Cardiff coastal defence initiative.

Similar momentum is seen in financial modernization efforts, including Pillar securing €3.2M pre-seed to digitize Europe’s construction finance, which supports smoother project execution. As emerging markets improve planning and expand industrial activity, paraffin wax and emulsions gain more room for application growth, from coatings and paper treatments to construction additives and agricultural formulations.

Latest Trends

Shift toward cleaner refined wax grades

Shift toward cleaner refined wax grades reflects a broader move toward higher-purity materials with improved stability and controlled performance in coatings, paper finishing, and construction chemicals. Customers increasingly prioritize refined paraffin and stable emulsion systems that offer smoother films, better compatibility, and reduced impurities. This trend connects with ongoing digital and financial innovation in the construction ecosystem, illustrated by Construction FinTech Billd raising $7.3m in funding, which highlights modernization across project workflows.

As industries modernize operations and seek consistency in material quality, refined wax grades and cleaner emulsions become more appealing. This preference encourages suppliers to focus on purity improvements and tighter production standards while supporting downstream users seeking reliable performance.

Regional Analysis

Asia Pacific holds 48.5%, reaching USD 320.8 Mn, strengthening Paraffin Wax and Emulsions growth.

The Paraffin Wax and Emulsions Market shows varied regional performance across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, with demand influenced by industrial maturity and application diversity.

Asia Pacific leads the global landscape with a dominant 48.5% share valued at USD 320.8 Mn, supported by its strong manufacturing base and extensive usage in coatings, packaging, and refining-linked industries.

North America reflects stable demand due to established applications in consumer products, paper coating, and industrial processing, while Europe continues to rely on structured manufacturing and regulatory-driven use of refined wax grades. Latin America exhibits moderate growth, driven by rising consumption in packaging and emerging coating applications.

The Middle East & Africa maintain gradual expansion supported by industrial development and increasing local production capabilities. Across all regions, application-linked consumption patterns create a balanced market structure, but the clear leadership of Asia Pacific—both in share and value—positions it as the primary contributor to global market movement.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Sasol continues to stand out for its reliable supply capabilities and long-standing expertise in wax production. The company’s strong integration with its chemical operations allows it to maintain consistent material quality, which remains important for industries requiring stable melting profiles and uniform performance. Its position supports downstream users in coatings, packaging materials, and process industries, where dependable paraffin output remains essential for operational continuity.

Meanwhile, Altana AG plays a meaningful role from the specialty chemicals side, particularly in emulsions used in coatings and surface applications. The company’s emphasis on formulation improvement and application-specific development helps customers achieve better dispersion, film quality, and surface performance. In 2025, its contribution is largely reflected in the consistent demand from coating manufacturers who rely on stable emulsion systems to enhance finish and durability across architectural and industrial segments.

For PMC Crystal, its relevance continues to grow as it strengthens its position in refined paraffin and related emulsions. The company’s focus on product purity and tailored material performance supports sectors that require cleaner grades and application flexibility. Across all three players, 2025 showcases a market shaped by dependable supply, consistency in product behavior, and industry-specific alignment rather than aggressive shifts or structural volatility.

Top Key Players in the Market

- PMC Crystal

- Sasol

- Altana AG

- Lubrizol Corporation

- Nippon Seiro Co., Ltd

- Michelman, Inc.

- TIANSHI WAX

- BASF SE

- Repsol

Recent Developments

- In October 2025, PMC Crystal, a specialty chemicals maker known for wax emulsions and additives, announced a new distribution partnership with ChemPoint. Through this agreement, ChemPoint will help distribute PMC Crystal’s ADVALUBE® PVC lubricant products across North America. These lubricants support PVC applications like rigid pipe making, film and sheet extrusion, and other rigid PVC processing. This partnership expands the sales reach of PMC Crystal’s product range beyond its direct customers.

- In February 2025, Sasol Chemicals expanded its wax product range with new micronised waxes called SASOLWAX LC Spray 30 G and LC Spray 30 G-EF, which have about 32% lower product carbon footprint compared to earlier spray wax products. These micronised waxes are designed for use in inks, paints, coatings, and other formulations, offering performance while reducing environmental impact.

Report Scope

Report Features Description Market Value (2025) USD 661.6 Million Forecast Revenue (2035) USD 1,174.0 Million CAGR (2026-2035) 5.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Natural, Synthetic), By Product Type (Paraffin Wax, Paraffin Emulsion), By Grade (Fully Refined, Semi-Refined, Unrefined), By Application (Leather, Construction, Agriculture, Paper, Paints and Coatings, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape PMC Crystal, Sasol, Altana AG, Lubrizol Corporation, Nippon Seiro Co., Ltd, Michelman, Inc., TIANSHI WAX, BASF SE, Repsol Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Paraffin Wax And Emulsions MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Paraffin Wax And Emulsions MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- PMC Crystal

- Sasol

- Altana AG

- Lubrizol Corporation

- Nippon Seiro Co., Ltd

- Michelman, Inc.

- TIANSHI WAX

- BASF SE

- Repsol

Our Clients

- 180002

- March 2026