Quick Navigation

Report Overview

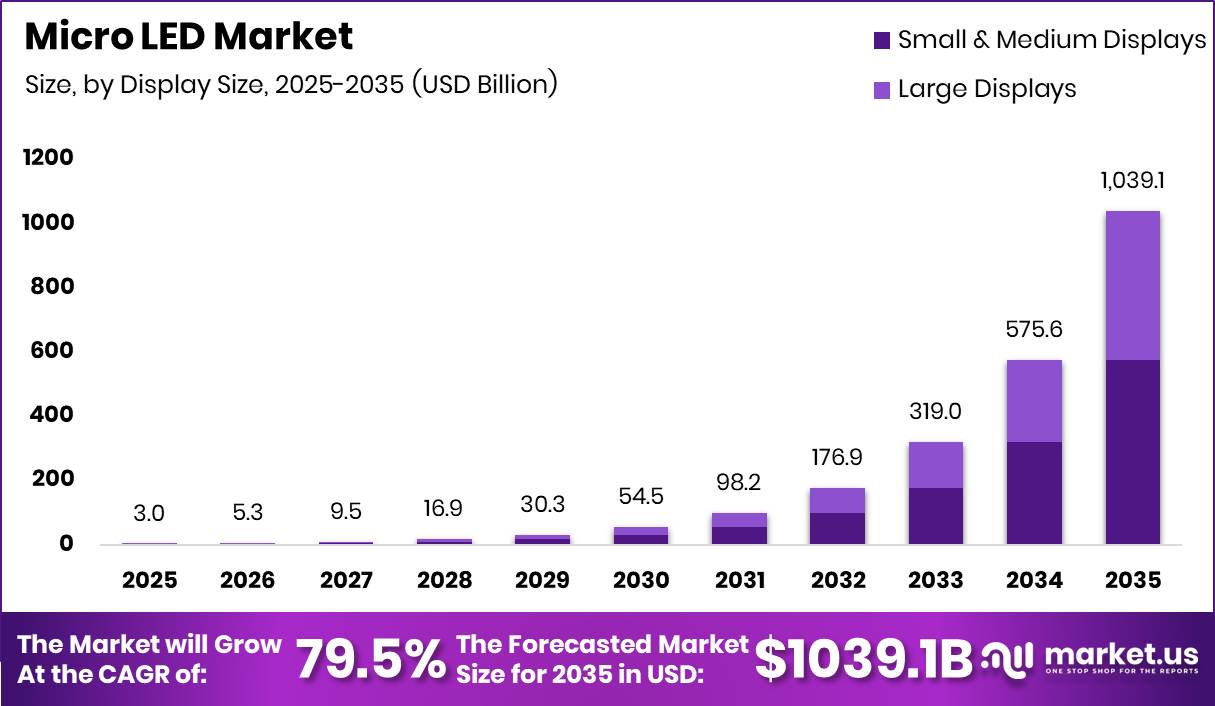

Global Micro LED Market size is expected to be worth around USD 1,039.1 Billion by 2035 from USD 3.0 Billion in 2025, growing at a CAGR of 79.5% during the forecast period 2026 to 2035.

The Micro LED market covers self-emissive display technology built on microscale inorganic LED chips transferred onto backplane substrates. This market spans display size segments from small wearables to large commercial panels, panel types including rigid, flexible, and transparent formats, and applications across consumer electronics, automotive, healthcare, BFSI, and aerospace and defense.

Key Takeaways

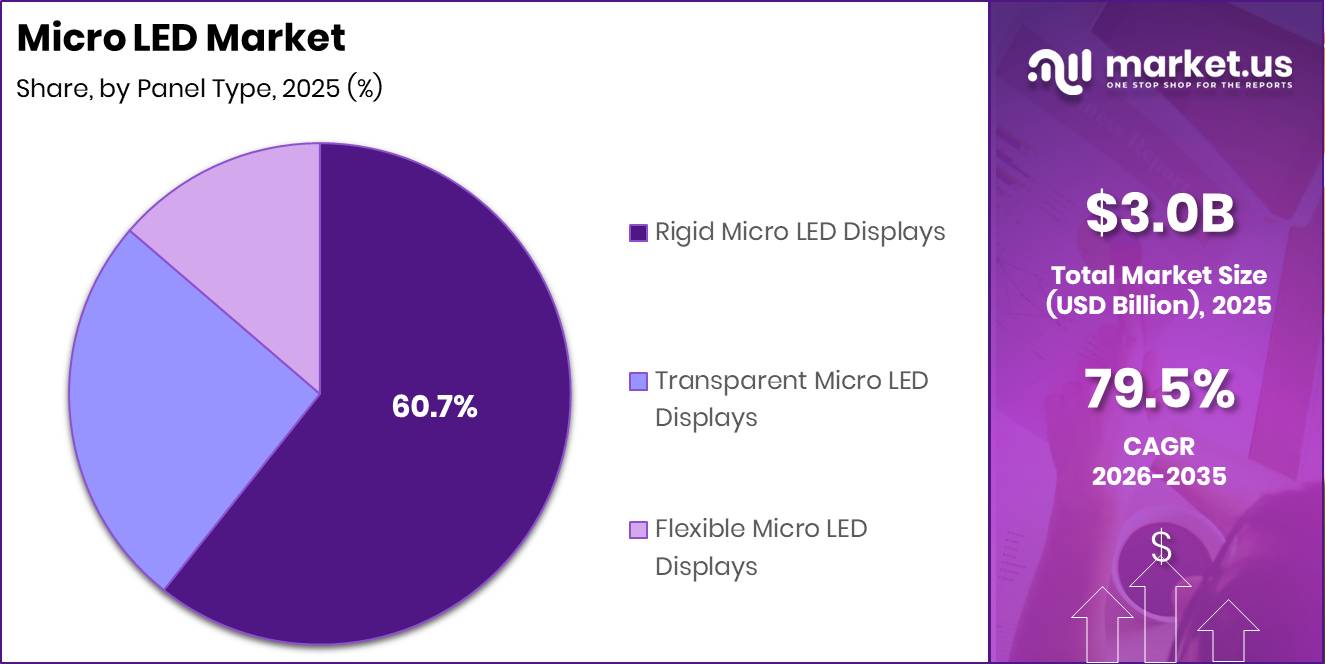

- Micro LED Market size in 2025 stands at USD 3.0 Billion, reaching USD 1,039.1 Billion by 2035.

- The market grows at a CAGR of 79.5% between 2026 and 2035.

- Small and Medium Displays dominate the Display Size segment with a 55.4% share.

- Rigid Micro LED Displays lead the Panel Type segment with a 60.7% share.

- Consumer Electronics dominates the Application segment with a 65.7% share.

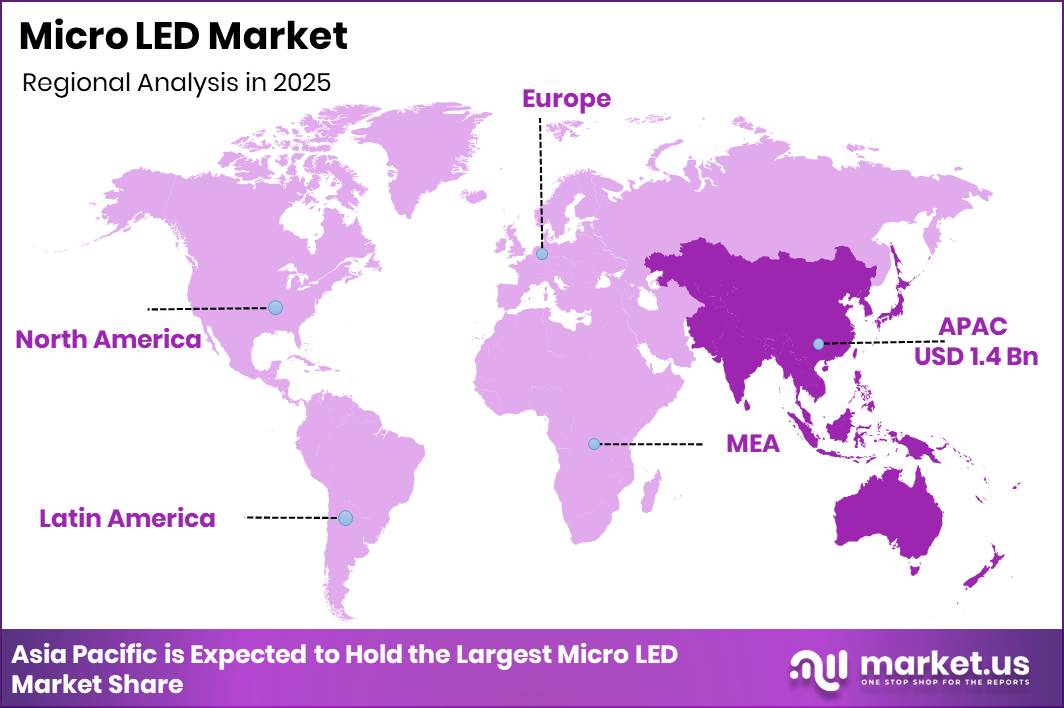

- Asia Pacific leads all regions with a 45.6% market share, valued at USD 1.4 Billion in 2025.

Government bodies and industrial consortia across East Asia and North America treat Micro LED as a strategic technology asset. Taiwan’s display supply chain, China’s panel manufacturing clusters, and South Korea’s semiconductor-display crossover programs all support development funding and fab incentives. This public-private investment signals a structural commitment to Micro LED beyond standard commercial R&D cycles.

As per our research, VueReal secured USD 40 million in funding to accelerate commercialization of its MicroSolid Printing platform. This capital injection targets the mass transfer bottleneck that constrains production scale. Investors entering this market now are effectively betting on process innovation, not just product demand, which means manufacturing IP will define competitive moats more than panel specifications alone.

Transfer yield improvements, sub-pixel architecture advances, and wearable launch validations are converging to shift Micro LED from prototype to production economics. This convergence compresses the timeline for cost curve declines across display sizes. Early-stage suppliers that secure wearable or automotive design wins before 2027 will gain process learning advantages that are difficult to replicate at scale.

Display Size Analysis

Small and Medium Displays dominate with 55.4% due to wearable and mobile premium adoption.

In 2025, Small and Medium Displays held a dominant market position in the By Display Size segment of the Micro LED Market, with a 55.4% share. Wearable devices and smartphones carry higher display cost tolerance per square inch than large-panel formats. This pricing dynamic makes small panels the most commercially viable entry path for Micro LED suppliers seeking to build volume and process experience before targeting larger screen categories.

Smartphones represent a high-volume target for Micro LED as manufacturers pursue brightness and power efficiency gains over current OLED panels. The density requirements of smartphone displays, however, push sub-pixel placement precision to its limits. Suppliers that solve pixel pitch challenges at smartphone scale will hold transferable manufacturing advantages across all other small-panel categories.

Smartwatches and Wearables are the earliest validated commercial segment for Micro LED deployment. According to Coherent Market Insights, a 2025 smartwatch implementation achieved 326 pixels per inch on a 1.4-inch circular panel. This deployment confirms that wearable display economics can absorb Micro LED cost premiums, giving contract manufacturers a repeatable purchase model to build production volume against.

Large Displays, including televisions, digital signage, and video walls, represent the long-term volume upside for the Micro LED market. As reported by Samsung News, Samsung launched the world’s first Micro RGB display in a 115-inch screen format. This launch establishes a commercial reference point for large-format Micro LED and signals that flagship consumer electronics brands are prepared to price-test premium segments ahead of broad cost reduction.

Panel Type Analysis

Rigid Micro LED Displays dominate with 60.7% due to process maturity and structural reliability.

In 2025, Rigid Micro LED Displays held a dominant market position in the By Panel Type segment of the Micro LED Market, with a 60.7% share. Rigid substrates offer the most stable backplane environment for high-density LED transfer at current yield levels. Buyers in consumer electronics and commercial signage favor rigid formats because performance consistency is more predictable than in flexible alternatives, reducing deployment risk.

Transparent Micro LED Displays occupy a high-value niche in retail, automotive, and architectural applications where see-through functionality commands premium pricing. This format benefits from the same brightness and self-emissive properties as rigid panels while enabling new spatial design formats. Vendors that secure early transparent display projects in automotive head-up displays or retail environments gain reference accounts that justify higher ASPs.

Flexible Micro LED Displays represent the longest development runway among panel types due to the added complexity of transferring chips onto non-rigid substrates without yield loss. This category targets curved automotive surfaces, wearable bands, and foldable consumer devices. Suppliers that crack flexible transfer yields before 2028 will unlock a structurally differentiated product category that rigid-only competitors cannot address.

Application Analysis

Consumer Electronics dominates with 65.7% due to premium device upgrade cycles and brightness demand.

In 2025, Consumer Electronics held a dominant market position in the By Application segment of the Micro LED Market, with a 65.7% share. Smartphones, smartwatches, tablets, and AR/VR devices all benefit from Micro LED’s superior brightness-to-power ratio. This performance advantage over OLED creates a clear upgrade proposition for premium device OEMs, accelerating Micro LED’s penetration into the consumer device refresh cycle.

Automotive applications represent the second most commercially advanced category after consumer electronics. Instrument clusters, center stack displays, and head-up display systems in premium vehicles are transitioning toward Micro LED formats for their outdoor readability and durability. OEMs that integrate Micro LED cockpit platforms before 2028 will differentiate on interior experience at a time when software-defined vehicle interiors are redefining premium positioning.

Healthcare, BFSI, and Aerospace and Defense applications collectively expand the addressable market beyond consumer cycles. Healthcare imaging and BFSI data visualization require high-brightness, always-on displays with low failure rates. Aerospace and defense procurement timelines are long but offer non-commoditized pricing, making these segments attractive for suppliers with certified manufacturing processes seeking to diversify from consumer-driven volatility.

Key Market Segments

By Display Size

- Small and Medium Displays

- Smartphones

- Smartwatches and Wearables

- Tablets

- AR/VR Devices

- Others

- Large Displays

- Televisions

- Digital Signage

- Video Walls

- Others

By Panel Type

- Rigid Micro LED Displays

- Transparent Micro LED Displays

- Flexible Micro LED Displays

By Application

- Automotive

- Consumer Electronics

- Healthcare

- BFSI

- Aerospace and Defense

- Others

Drivers

The strongest near-term demand catalyst is the fact that Micro LED has crossed from demonstration into branded wearable launch activity. AUO’s partnership with Garmin produced the fēnix 8 Pro MicroLED smartwatch using a 1.4-inch display at 326 PPI. Wearables can absorb a higher display cost per square inch than smartphones or TVs while monetizing brightness, battery efficiency, and outdoor readability more effectively.

This commercial wearable launch changes the market structure by giving suppliers a realistic entry segment where panel area is small, average selling prices are premium, and defect exposure is lower than in large panels. Wearable programs improve factory utilization and accelerate process learning. This creates repeatable purchase logic for Micro LED modules, making wearables the most immediate shipment-validating driver for the 2026 baseline.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wearable launch cycle validating micro LED commercialization | +2.3% | Taiwan core, North America premium device brands, Japan wearable channels | Short term (≤ 2 years) |

| Automotive display integration moving from concept to SOP | +2.0% | North America core, Japan, EU premium EV corridors | Medium term (2-4 years) |

| Transfer yield and pilot-line scaling improving cost viability | +2.8% | Taiwan core, China, South Korea, U.S. engineering nodes | Short term (≤ 2 years) |

| Premium brightness and transparent format demand in commercial display | +1.5% | North America, Japan, South Korea, Gulf project markets | Medium term (2-4 years) |

| Ecosystem consolidation around Taiwan-led supply partnerships | +1.6% | Taiwan core, China manufacturing belt, APAC spill-over | Medium term (2-4 years) |

| Solution-stack expansion beyond panels into HMI and mobility systems | +1.2% | North America, EU, Taiwan, India | Long term (≥ 4 years) |

Restraints

A core structural restraint on the 2026 to 2030 Micro LED trajectory is persistently low yield for sub-5 µm chips. Functional device yields for full-color displays often struggle to move beyond 60 to 70% at pilot lines versus the 95 to 98% threshold required to support mainstream smartphone or TV economics. This gap delivers a modeled 2.4 percentage-point drag on the high-baseline CAGR forecast.

At current defect densities, scrap and rework inflate effective die cost per square centimeter by 1.5 to 2.0 times. Repair-centric architectures add 10 to 15% extra backplane and control IC cost, compressing gross margins by 300 to 500 basis points for early adopters. Tier-1 display makers in Korea, Taiwan, and China are deferring aggressive capital expenditure ramps by 12 to 24 months as a direct consequence, slowing ecosystem learning curves across all major manufacturing hubs.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-5 µm chip yield failures | -2.4% | East Asia hubs, North America, EU | Medium term (2–4 years) |

| Mass-transfer throughput bottlenecks | -1.9% | APAC corridors, North America core | Medium term (2–4 years) |

| CapEx intensity and financing risk | -1.7% | North America, EU, China, Taiwan | Long term (≥ 4 years) |

| Equipment and IP export controls | -1.5% | China, East Asia, US, EU | Short–Medium term (≤ 4 years) |

| Wafer, sapphire, and epi cost spikes | -1.3% | Global, with focus on Korea, Taiwan, Japan | Short term (≤ 2 years) |

| Brand and OEM adoption hesitancy | -1.1% | North America, EU, premium APAC | Medium–Long term (≥ 3 years) |

Challenges

Micro LED economics in 2026 remain structurally constrained by mass transfer and repair yields. Assembling 8 to 30 million sub-100 µm chips for a 4K television or large signage wall produces effective line yields often below 70%, versus the 95 to 98% yield achieved in mature LCD and OLED lines. Per-panel scrap rates can add 20 to 40% to unit manufacturing cost, which directly suppresses margin for any producer attempting commercial-scale shipments today.

Chip placement must occur at rates above 10 million units per hour with positional accuracy in the 1 to 2 µm range. Even a 0.001% defect probability per die aggregates into tens of thousands of failures per panel. These yield penalties cap short-run capacity utilization at 60 to 75%, preventing price curves from falling at the 20 times reduction required for true mass markets in monitors and televisions.

Leading players must invest in semiconductor-style fully automated lines combining wafer-level testing, binning, and AI-driven defect prediction to push aggregate yields up by 10 to 20 percentage points over the next five to eight years. Pixel architectures must also be redesigned to tolerate small defect densities via redundant emitters. This investment trajectory can recover approximately 2 percentage points of CAGR otherwise sacrificed to yield-driven production throttling.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Mass transfer yield bottlenecks | -2.0% | APAC fabs, NA/EU R&D hubs | Long term (≥ 4 years) |

| Capex- and tooling-intensive scale-up | -1.5% | APAC manufacturing clusters, NA/EU entrants | Medium term (2-4 years) |

| Epitaxy and wafer supply stress | -1.2% | APAC core, EU specialty suppliers | Medium term (2-4 years) |

| Talent and process integration gap | -1.0% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Ecosystem / standards fragmentation | -0.8% | Global OEM and OS ecosystems | Medium term (2-4 years) |

| Competitive display price pressure | -0.7% | North America, Europe, APAC consumer markets | Short term (≤ 2 years) |

Opportunities

Automotive represents the clearest structural opportunity for Micro LED suppliers willing to commit to multi-display cockpit platform design. Suppliers that lock in instrument cluster, center stack, passenger display, and adaptive ambient interface programs before platform standardization occurs can raise display content value per vehicle by an estimated USD 250 to USD 900. This shifts the revenue model from one-time panel shipments to long-cycle program income across five to seven year vehicle architectures.

Premium EV adoption rates can expand by 10 to 20 percentage points where Micro LED cockpit integration is paired with software-defined interior personalization and OTA-enabled interface upgrades. This creates an incremental service and software revenue layer beyond hardware margin. Suppliers that enter automotive Micro LED programs before 2028 gain certification and integration experience that becomes a structural barrier to late entrants.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| XR optics stack integration | +3.2% | North America, East Asia, EU | Short term (≤ 2 years) |

| Auto premium cockpit scale-up | +2.4% | China, EU, Japan, South Korea, North America | Medium term (2-4 years) |

| Display-as-a-service for virtual production | +1.7% | North America core, EU, Middle East, East Asia | Short term (≤ 2 years) |

| Defense-to-commercial manufacturing spillover | +1.5% | U.S. core, allied EU markets, Taiwan | Medium term (2-4 years) |

| IP licensing and transfer-tool monetization | +1.9% | Taiwan, China, South Korea, EU | Medium term (2-4 years) |

| Regional fab-light assembly hubs | +2.1% | EU, U.S., India, Southeast Asia | Long term (≥ 4 years) |

Regional Analysis

Asia Pacific Dominates the Micro LED Market with a Market Share of 45.6%, Valued at USD 1.4 Billion

Asia Pacific commands the Micro LED market through its concentration of panel manufacturers, semiconductor fabs, and display supply chain infrastructure across Taiwan, China, South Korea, and Japan. Taiwan anchors the supply ecosystem through wafer-level LED production and mass transfer tool development. This structural depth gives Asia Pacific manufacturers first-mover cost and learning curve advantages over Western entrants across every display category.

North America drives the Micro LED market through its concentration of high-value device OEMs, defense procurement programs, and university-linked R&D hubs. Premium wearable and smartphone brands headquartered in the region pull advanced display specifications from Asia Pacific supply partners. In July 2025, MicroLumin signed a joint development partnership with Anhui Yuanchen covering an initial order of 20,000 AR smart glasses, reflecting the cross-regional sourcing logic shaping North American AR demand.

Europe’s Micro LED market is defined by automotive OEM demand from Germany and France, industrial display procurement, and publicly funded pilot production programs in the semiconductor corridor. Regulatory alignment on energy efficiency standards accelerates the case for Micro LED in commercial and architectural formats. EU industrial policy backing for display sovereignty creates a policy tailwind that distinguishes European market conditions from purely market-driven adoption elsewhere.

Latin America and the Middle East and Africa represent early-stage markets where commercial digital signage, luxury retail installations, and government-funded smart infrastructure programs create localized demand pockets. Procurement in Gulf project markets prioritizes premium brightness and large-format visual impact. This positions Micro LED video wall and digital signage formats as the primary entry vectors for suppliers looking to establish a commercial footprint in these regions ahead of broader consumer adoption.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AUO Corporation holds a strategic position at the intersection of display manufacturing scale and Micro LED process development, with its 2026 smart-mobility platform targeting automotive cockpit integration. This automotive focus creates a medium-term revenue anchor that is less price-sensitive than consumer display volumes. However, program timelines of five to seven years create cash flow exposure if wearable and AR volumes do not bridge near-term factory utilization.

In September 2025, Mojo Vision closed a USD 75 million Series B Prime funding round to accelerate its high-performance Micro LED platform for AI and AR applications. Samsung Electronics Co. Ltd. leads the large-format Micro LED commercialization race with its 115-inch Micro RGB launch, establishing a flagship reference that competitor OEMs must respond to. This product leadership in premium TV creates brand authority but also concentrates Samsung’s Micro LED revenue in a segment where unit volumes remain limited by pricing until cost curves fall further.

Key Players

- AUO Corporation

- Samsung Electronics Co. Ltd.

- Sony Corporation

- LG Display Co. Ltd.

- BOE Technology Group Co. Ltd.

- PlayNitride Inc.

- Innolux Corporation

- Tianma Microelectronics Co. Ltd.

- Nichia Corporation

- Sharp Corporation

- VueReal Inc.

- Plessey Semiconductors Ltd.

- Aledia SA

- JBD (Jade Bird Display)

- Leyard Optoelectronics Co. Ltd.

- Other Key Players

Recent Developments

- January 2025 – VueReal secured USD 40.5 million in Series C funding led by Export Development Canada to scale MicroLED production capacity and expand commercialization of its MicroSolid Printing technology.

- January 2025 – Aledia unveiled a USD 200 million MicroLED production line in Grenoble, France, targeting mass production of MicroLED displays for augmented-reality smart glasses and vision applications.

- December 2025 – PlayNitride announced the acquisition of Lumiode Inc. for USD 2 million, strengthening its MicroLED intellectual-property portfolio and expanding near-eye display capabilities for AR applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.0 Billion |

| Forecast Revenue (2035) | USD 1,039.1 Billion |

| CAGR (2026-2035) | 79.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Display Size (Small and Medium Displays: Smartphones, Smartwatches and Wearables, Tablets, AR/VR Devices, Others; Large Displays: Televisions, Digital Signage, Video Walls, Others), By Panel Type (Rigid Micro LED Displays, Transparent Micro LED Displays, Flexible Micro LED Displays), By Application (Automotive, Consumer Electronics, Healthcare, BFSI, Aerospace and Defense, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AUO Corporation, Samsung Electronics Co. Ltd., Sony Corporation, LG Display Co. Ltd., BOE Technology Group Co. Ltd., PlayNitride Inc., Innolux Corporation, Tianma Microelectronics Co. Ltd., Nichia Corporation, Sharp Corporation, VueReal Inc., Plessey Semiconductors Ltd., Aledia SA, JBD (Jade Bird Display), Leyard Optoelectronics Co. Ltd., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |