Quick Navigation

Report Overview

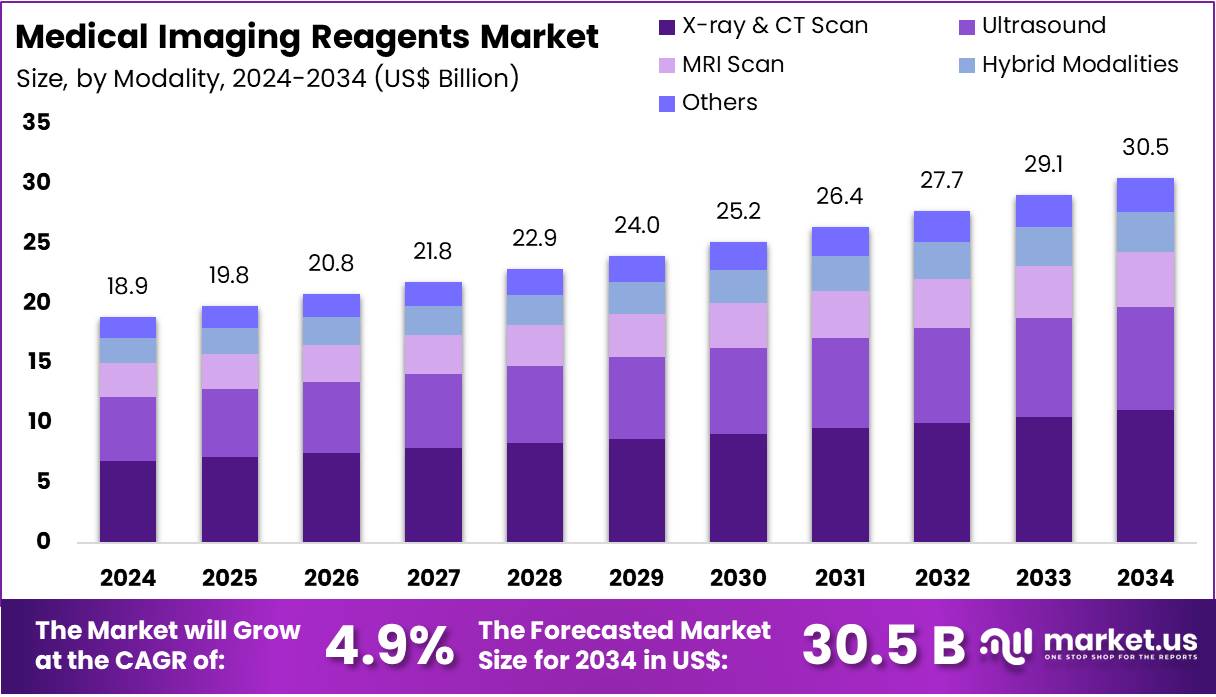

The Global Medical Imaging Reagents Market Size is expected to be worth around US$ 30.5 Billion by 2034, from US$ 18.9 Billion in 2024, growing at a CAGR of 4.9% during the forecast period from 2025 to 2034.

The Global Medical Imaging Reagents Market is expanding steadily, driven by advancements in imaging technologies and growing clinical needs. According to the World Health Organization (WHO), nearly 47% of the global population still lacks access to essential diagnostic services, including imaging. This unmet demand, especially in low- and middle-income countries where only 30% of health facilities are adequately equipped, is prompting urgent reforms and investments in diagnostic infrastructure.

Advancements in imaging technologies such as MRI, CT, PET, and SPECT have significantly boosted the demand for specialized reagents. These reagents enhance image clarity, improve disease visualization, and support accurate diagnosis. For instance, imaging reagents now enable visualization of disease mechanisms at the cellular and molecular levels, playing a vital role in academic and pharmaceutical research. According to WHO efforts, initiatives in remote and underserved areas are improving access to imaging through technical training and infrastructure support.

The rising global prevalence of chronic diseases such as cancer and cardiovascular conditions further fuels market demand. Medical imaging reagents facilitate early detection and monitoring of these conditions. For example, the integration of PET imaging with radiolabeled peptides allows real-time tumor detection and monitoring. A study has shown that augmented reality (AR)-guided thoracolumbar pedicle screw placement achieved 96% accuracy, with angular and distance errors of just 2.4° and 1.9 mm respectively, reflecting the clinical precision enabled by advanced visualization tools.

Government initiatives are reinforcing growth through investments in healthcare infrastructure and early disease detection programs. WHO’s WHA76.5 resolution on “Strengthening Diagnostics Capacity” emphasizes integrating diagnostics into national strategies. The WHO’s Model List of Essential In Vitro Diagnostics (EDL) also guides countries in prioritizing essential tests. For instance, NHS England’s “Cancer 360” digital tool centralizes patient data, enabling faster cancer diagnosis and improved treatment timelines.

The market is also benefiting from the shift towards personalized medicine. Molecular imaging reagents are crucial for identifying biomarkers and tailoring therapies to individual patients. This trend is exemplified in oncology, where theranostics—agents that combine diagnostic and therapeutic capabilities—are gaining traction. For example, ^177Lu-DOTATATE used in peptide receptor radionuclide therapy (PRRT) has shown efficacy in treating neuroendocrine tumors by targeting somatostatin receptors. Similarly, prostate-specific membrane antigen (PSMA)-targeted radiotherapies are advancing treatment outcomes in metastatic prostate cancer.

Technological innovation in reagent development continues to improve specificity, safety, and application scope. These advancements support applications in surgical navigation and intraoperative imaging. For example, AR and electromagnetic tracking technologies now enable real-time surgical guidance, improving precision and reducing risks. These improvements, supported by WHO collaborations and ongoing research, are expanding the role of imaging reagents in modern healthcare delivery.

Key Takeaways

- The global medical imaging reagents market is projected to reach approximately US$ 30.5 billion by 2034, up from US$ 18.9 billion in 2024.

- The market is expected to grow at a steady compound annual growth rate (CAGR) of 4.9% between 2025 and 2034.

- In 2024, contrast reagents dominated the class segment, accounting for over 43.2% of the global medical imaging reagents market share.

- The neurological disorder segment led the application category in 2024, holding more than a 28.7% share of the overall market.

- X-ray and CT scan modalities were the largest contributors in 2024, capturing more than 36.3% of the modality-based segment.

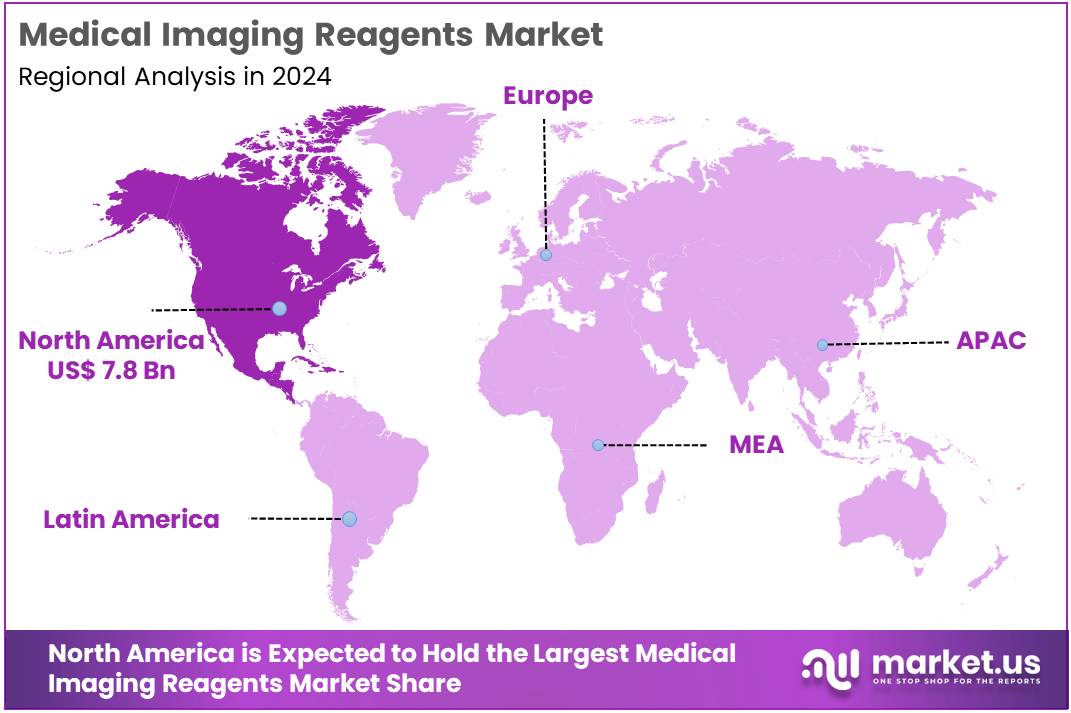

- North America emerged as the leading regional market in 2024, generating US$ 7.8 billion and accounting for over 41.7% of the global share.

Class Analysis

In 2024, the Contrast Reagents section held a dominant market position in the class segment of the Medical Imaging Reagents Market, and captured more than a 43.2% share. This leadership is driven by their frequent use in imaging techniques like MRI, CT scans, and X-rays. These reagents enhance image clarity, helping doctors detect diseases early. The increasing cases of cancer and heart disease are key contributors. The availability of different types of contrast agents supports their wide use across diagnostic platforms.

Optical Reagents stood as the second-largest segment in 2024. These reagents are mainly used in fluorescence and near-infrared imaging. They are favored for their role in identifying molecular and cellular changes. Their growing use in research and targeted diagnostics has boosted demand. These reagents help in early-stage detection and are popular in personalized medicine. Their precision and sensitivity make them useful in identifying disease markers at a microscopic level. Their role in innovation continues to grow.

Nuclear Reagents accounted for a smaller but steadily expanding portion of the market. These are essential in PET and SPECT scans. They help trace metabolic and biochemical processes inside the body. Their use is especially high in oncology, cardiology, and neurology. New developments in radiopharmaceuticals are supporting growth in this segment. Their ability to visualize internal body functions makes them vital in modern diagnostics. The demand for these reagents is expected to rise with advanced disease detection needs.

Application Analysis

In 2024, the Neurological Disorder section held a dominant market position in the application segment of the medical imaging reagents market and captured more than a 28.7% share. This segment’s growth was driven by the rising cases of Alzheimer’s disease, epilepsy, and stroke. Experts believe the demand for precise brain imaging has grown significantly. Advanced techniques like PET and MRI are often used for early diagnosis. These methods rely heavily on specialized imaging reagents to detect neurological abnormalities.

The Cardiovascular Disorder segment held the second-largest share. Its expansion is linked to the global rise in heart diseases. Conditions like coronary artery disease and hypertension are now more common. Healthcare providers are using imaging reagents to improve non-invasive scans. These agents enhance visibility during CT and MRI procedures. As a result, doctors can better assess heart structure and blood flow. This helps in planning early treatments and reducing complications.

Cancer imaging applications also showed notable progress. A high number of breast, lung, and prostate cancer cases led to increased use of imaging agents. These reagents support early tumor detection and monitor treatment responses. In gastrointestinal disorders, contrast agents are used to detect inflammation and lesions. Musculoskeletal applications are growing too. They help in diagnosing arthritis and bone injuries. Meanwhile, nephrological imaging and other minor categories are slowly gaining traction due to expanding diagnostic needs.

Modality Analysis

In 2024, the X-ray & CT Scan section held a dominant market position in the modality segment of the medical imaging reagents market, and captured more than a 36.3% share. The growth of this segment can be attributed to its wide use in disease screening and trauma assessment. X-ray and CT scans are preferred due to their speed, affordability, and detailed imaging capabilities. These modalities are often used in emergency care and routine diagnostics.

The MRI scan segment followed closely, supported by increasing demand for soft tissue imaging. MRI reagents are essential in neurological and musculoskeletal examinations. Their non-invasive nature and superior image clarity drive usage in chronic disease diagnosis. Government healthcare initiatives and the adoption of advanced imaging technologies are expected to further strengthen this segment’s growth.

The hybrid modalities segment is also witnessing notable expansion. This includes PET-CT and SPECT-CT technologies, which combine functional and structural imaging. Their use is growing in cancer diagnostics and cardiology. The need for accurate staging and treatment planning supports this growth. Additionally, ultrasound imaging reagents are gaining traction due to their safety and portability. These are often used in prenatal care and organ assessments, especially in developing healthcare settings.

Key Market Segments

By Class

- Contrast Reagents

- Optical Reagents

- Nuclear Reagents

By Application

- Neurological Disorder

- Cardiovascular Disorder

- Cancer

- Gastrointestinal Disorder

- Musculoskeletal Disorder

- Nephrological Disorder

- Others

By Modality

- X-ray & CT Scan

- Ultrasound

- MRI Scan

- Hybrid Modalities

- Others

Drivers

Rising Burden of Chronic Diseases Fuels Imaging Reagent Demand

The global rise in chronic diseases such as cancer, cardiovascular disorders, and neurological conditions is significantly increasing the demand for medical imaging reagents. These health issues require accurate diagnostic imaging for early-stage identification and effective clinical management. As a result, there is growing reliance on enhanced imaging solutions to support timely medical decisions. Medical imaging reagents play a vital role by improving contrast and visualization in diagnostic scans. This trend is driving continuous adoption across both developed and developing healthcare systems.

Medical imaging reagents are especially critical in modalities such as MRI, CT, and PET scans, which are widely used in chronic disease diagnostics. These reagents help in highlighting internal structures and biological activities, enabling clinicians to detect abnormalities with higher precision. The need for early and accurate detection in cancer screening, cardiovascular evaluations, and brain disorder assessments is accelerating the adoption of these reagents. This growing dependency is directly contributing to market expansion globally.

As healthcare systems increasingly shift toward preventive care and personalized treatment, the demand for high-quality diagnostic imaging is expected to grow. Governments and healthcare providers are investing in advanced imaging infrastructure to support chronic disease management. Consequently, the market for imaging reagents is poised for steady growth, driven by the urgent need for clarity and accuracy in chronic disease diagnostics.

Restraints

Limited Access to Imaging Reagents in Emerging Markets

The limited availability of imaging reagents in developing regions is a major barrier to the growth of the medical imaging market. Many countries in Asia, Africa, and Latin America face infrastructure limitations that prevent the integration of advanced diagnostic tools. Poorly equipped hospitals and insufficient trained personnel make it difficult to support complex imaging technologies. As a result, the penetration of reagents used in modalities like PET, SPECT, and CT remains significantly lower than in high-income regions, restricting diagnostic capabilities.

In addition to weak infrastructure, these regions often lack the domestic capacity to manufacture imaging reagents. This leads to dependence on imports, which increases costs and causes frequent supply chain disruptions. Without localized production, imaging centers face delays and inconsistencies in reagent availability. Governments in these areas may also struggle to fund expensive equipment and radioactive isotopes, making the use of advanced reagents financially unviable for many public health systems. This scenario severely limits access to timely and accurate diagnosis.

Furthermore, there is a notable shortage of essential isotopes such as molybdenum-99 and technetium-99m in these countries. These isotopes are critical for various imaging procedures, including nuclear medicine applications. Global supply constraints and the lack of local nuclear reactors capable of isotope production compound the issue. Consequently, patients in developing countries are deprived of accurate and early-stage diagnostic interventions, further widening healthcare disparities.

Opportunities

Rising Demand from Diagnostic Imaging Center Expansion

The global rise in diagnostic imaging centers creates a major opportunity for the medical imaging reagents market. As the need for early and accurate disease detection grows, healthcare systems are investing in advanced imaging infrastructure. This includes the establishment of new centers in urban and semi-urban areas. These facilities rely on a consistent supply of imaging reagents for procedures such as MRI, CT scans, and ultrasound. This growth is expected to increase the consumption rate of reagents across both developed and emerging markets.

Healthcare providers are focusing on expanding diagnostic capacity to meet growing patient volumes. As chronic diseases and age-related conditions rise, imaging plays a key role in treatment planning. The expansion of imaging centers improves access to diagnostic services, particularly in underserved regions. Consequently, the demand for safe and high-quality reagents increases, especially contrast agents used for enhanced imaging clarity. This trend supports market growth and opens opportunities for new product development and localization strategies.

Furthermore, private investments and government initiatives are fueling the establishment of state-of-the-art diagnostic facilities. These developments promote the integration of imaging technologies in outpatient and specialty clinics. Each new facility contributes to consistent reagent procurement for daily operations. This sustained demand cycle enhances revenue prospects for manufacturers. It also encourages innovations in reagent formulations aimed at improving patient safety and diagnostic precision.

Trends

Shift Towards Personalized and Precision Imaging

The medical imaging reagents market is witnessing a significant transformation due to the rising emphasis on personalized and precision imaging. This trend is being driven by advancements in molecular imaging technologies that allow reagents to specifically target disease biomarkers. These specialized reagents enable physicians to visualize biological processes at the cellular level, improving early detection. The precision offered by these agents supports better diagnostic outcomes. This shift is gaining momentum, especially in fields such as oncology, where tumor-specific imaging is crucial for treatment planning.

In neurology, precision imaging reagents are enabling better visualization of complex brain disorders. These reagents can highlight subtle molecular changes in neural tissues, which assists in diagnosing conditions like Alzheimer’s and Parkinson’s disease. The targeted nature of these imaging agents reduces the chances of misdiagnosis and helps customize patient treatment. As imaging becomes more personalized, clinicians can make data-driven decisions that align with a patient’s unique physiological profile. This has the potential to improve therapeutic efficacy significantly.

The growing adoption of personalized imaging also reflects broader healthcare goals of precision medicine. Medical imaging reagents that work at a molecular level are increasingly integrated into diagnostic workflows. This integration allows for accurate disease monitoring, response assessment, and optimized treatment strategies. As regulatory bodies and healthcare systems support such innovations, the market is expected to expand. This trend is likely to remain a primary growth driver in the coming years.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 41.7% share and holds US$ 7.8 billion market value for the year. This regional leadership is driven by strong healthcare infrastructure and advanced imaging technologies. The United States, in particular, benefits from a high number of diagnostic procedures. Increased demand for early disease detection has further supported market growth.

The presence of leading pharmaceutical and biotech firms contributes significantly. These companies continue to invest in the development of novel imaging agents. Supportive regulatory policies from the U.S. FDA also play a key role in accelerating product approvals. Public and private funding for research in molecular imaging has increased, enabling innovation.

Additionally, the growing elderly population is fueling the demand for diagnostic imaging. Higher awareness of chronic disease management in North America further supports the use of imaging reagents. Widespread availability of PET, MRI, and CT scanners across hospitals and diagnostic centers has created a favorable environment. Combined, these factors are reinforcing the region’s leading position in the global medical imaging reagents market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global medical imaging reagents market includes several key players actively pursuing innovation, regulatory compliance, and global expansion. Siemens AG holds a leading position by integrating advanced reagents with its imaging modalities, particularly in MRI and CT. The company’s strategic focus on AI-powered diagnostics has enhanced its product utility. Bayer AG is also prominent, with a strong portfolio in iodine- and gadolinium-based contrast agents. Its ongoing research aims to improve safety and usability for broader patient segments, including those with renal impairments.

CMC Contrast AB stands out by developing gadolinium-free contrast media. The company emphasizes sustainable chemistry and patient safety. Its products are gaining traction across Europe and select emerging markets. Thermo Fisher Scientific supports the market by offering high-purity reagents for clinical and research applications. Its collaborations with academic and healthcare institutions help it serve the precision imaging segment. The company also benefits from a broad distribution network and deep R&D expertise that supports innovation in diagnostic reagents.

Merck & Co., Inc. provides a wide range of reagents suited for diverse imaging applications. Its focus on biocompatibility and reagent efficiency supports adoption in both clinical and pre-clinical settings. Strategic alliances help Merck expand its diagnostic footprint globally. Shimadzu Corporation offers imaging systems with associated reagents, focusing on efficiency and integration. Its growth is driven by a strong regional presence in Asia-Pacific and adherence to local regulatory standards.

Other significant players include Bracco Imaging S.p.A., GE HealthCare, Guerbet Group, and Lantheus Holdings, Inc. These companies invest heavily in expanding their contrast media offerings. They also prioritize securing regulatory approvals and forming device partnerships to enhance compatibility. Innovation is centered on safer, low-toxicity, and high-contrast reagents. These efforts reflect the industry’s continuous shift toward precision imaging and patient-centric diagnostic solutions, ensuring ongoing competition and market advancement.

Market Key Players

- Siemens AG

- Bayer AG

- CMC Contrast AB

- Thermo Fisher Scientific Inc

- Merck & Co. Inc

- Shimadzu Corporation

- Koninklijke Philips N.V.

- Bracco Spa

- Lantheus Holdings Inc

- General Electric Company

Recent Developments

- In March 2024: Bayer reported the first Phase 3 results for gadoquatrane, a novel gadolinium-based contrast agent (GBCA) developed under its QUANTI program. The findings indicated that gadoquatrane could reduce the gadolinium dose by approximately 60% during MRI scans compared to existing macrocyclic GBCAs. Despite the reduced dosage, gadoquatrane demonstrated comparable effectiveness in tissue visualization and lesion detection, aligning with current standards in diagnostic accuracy.

- In April 2025: Shimadzu released the MobileDaRt Evolution MX9 Premium Version, a mobile X-ray system designed to improve clinical workflow and imaging accuracy. This system features a second monitor on the X-ray emitter unit and incorporates the industry’s first optional 3D camera. The additional monitor displays patient information and imaging conditions, while the 3D camera enhances positioning accuracy. These innovations aim to streamline operations during clinical rounds and reduce the frequency of re-imaging, thereby improving efficiency and patient outcomes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 18.9 Billion |

| Forecast Revenue (2034) | US$ 30.5 Billion |

| CAGR (2025-2034) | 4.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Class (Contrast Reagents, Optical Reagents, Nuclear Reagents), By Application (Neurological Disorder, Cardiovascular Disorder, Cancer, Gastrointestinal Disorder, Musculoskeletal Disorder, Nephrological Disorder, Others), By Modality (X-ray & CT Scan, Ultrasound, MRI Scan, Hybrid Modalities, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Siemens AG, Bayer AG, CMC Contrast AB, Thermo Fisher Scientific Inc, Merck & Co. Inc, Shimadzu Corporation, Koninklijke Philips N.V., Bracco Spa, Lantheus Holdings Inc, General Electric Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |