Global Lutein Market Size, Share, And Business Benefits By Source (Natural, Synthetic), By Form (Powder, Oil Suspension, Emulsion, Beadlet), By Application (Dietary Supplements, Food and Beverage, Pharmaceuticals, Animal Feed, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: August 2025

- Report ID: 156097

- Number of Pages: 368

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

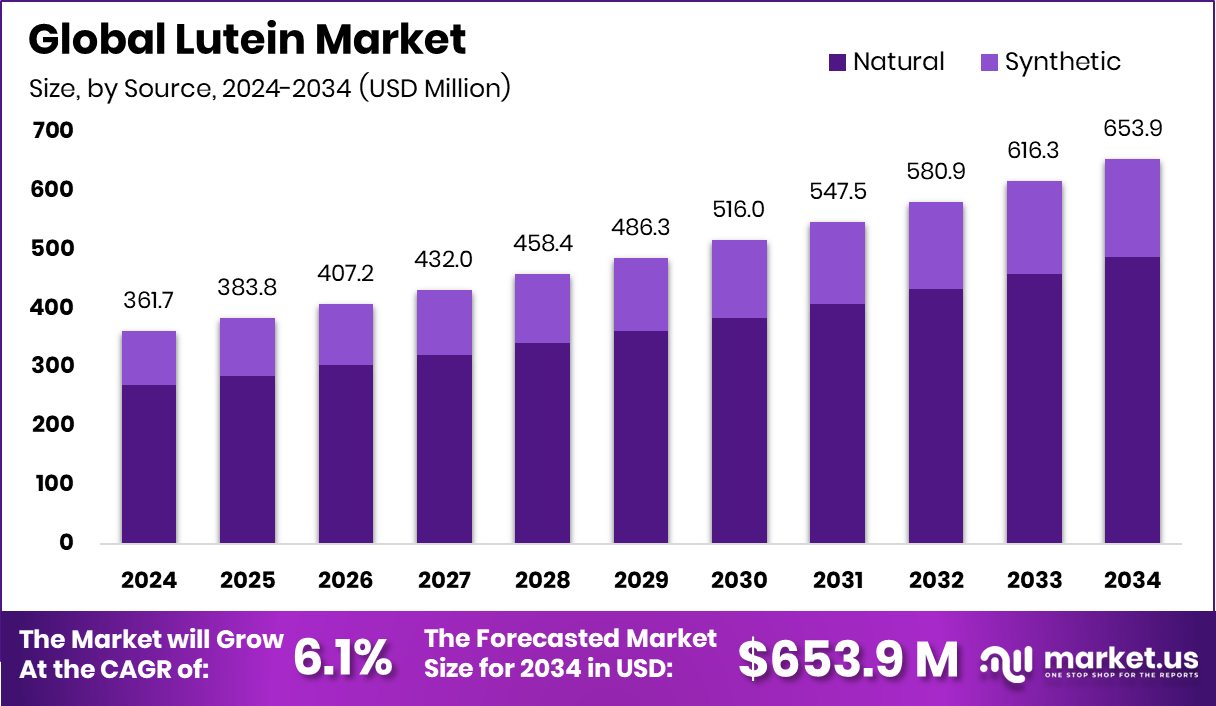

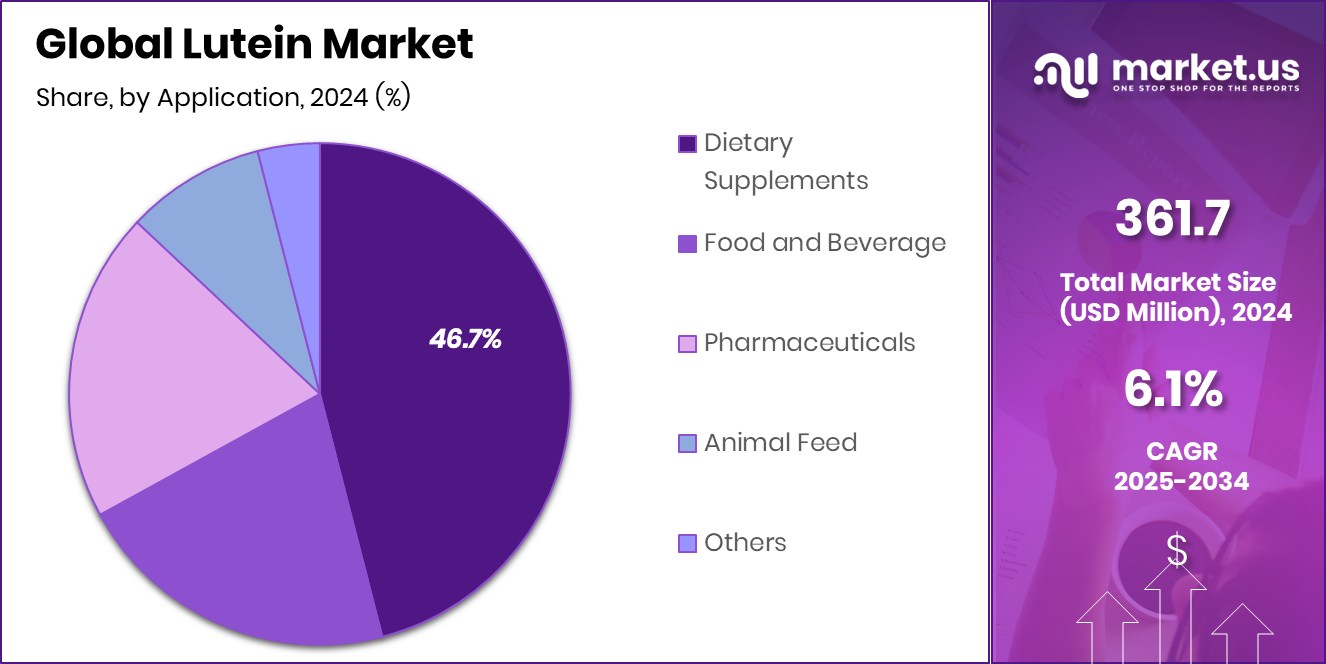

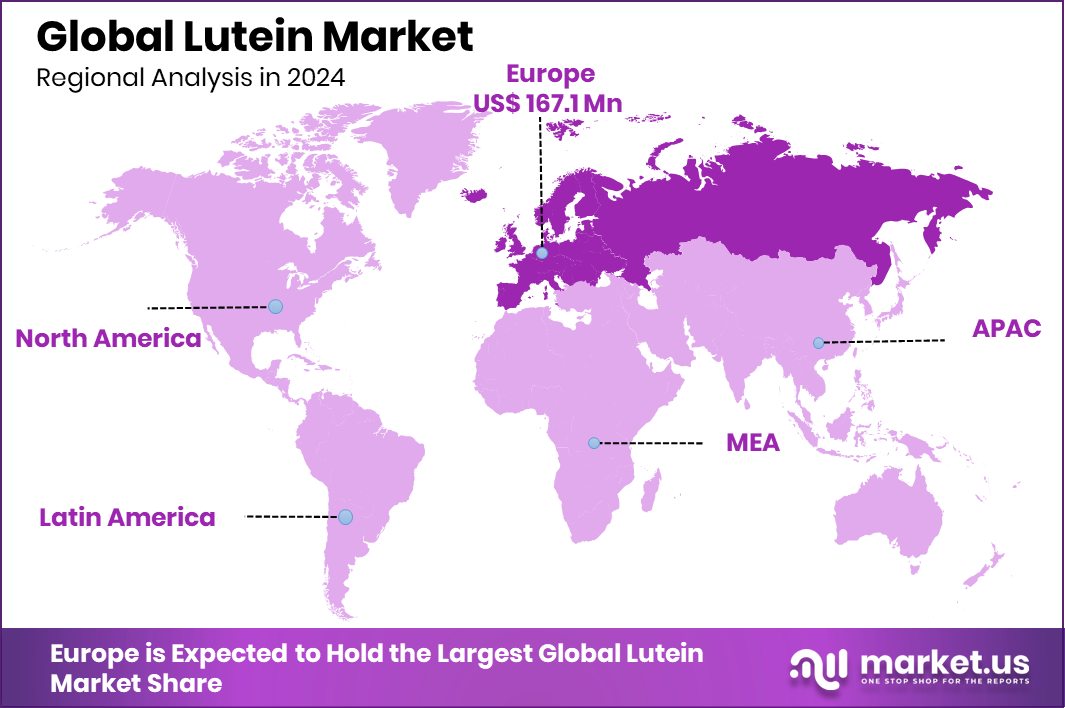

The Global Lutein Market is expected to be worth around USD 653.9 million by 2034, up from USD 361.7 million in 2024, and is projected to grow at a CAGR of 6.1% from 2025 to 2034. Rising preventive healthcare demand drives Europe’s 46.2% lutein market, valued at USD 167.1 Mn.

Lutein is a natural carotenoid pigment found in high amounts in leafy green vegetables, egg yolks, and some fruits. It plays an essential role in human eye health by acting as an antioxidant that protects the retina from damage caused by blue light and oxidative stress. Lutein is also linked to improved cognitive function and skin health, making it an important nutrient in both dietary supplements and fortified food products. ARTAH Nutrition secures £2.85M investment to expand its dietary supplement business.

The lutein market refers to the global trade, production, and application of lutein in supplements, food and beverages, pharmaceuticals, and cosmetics. Its demand is steadily growing as consumers become more aware of the health benefits of natural antioxidants. Rising interest in preventive healthcare and nutrition-focused lifestyles has strengthened the market’s position across both developed and developing regions. HealthKart obtains $153M in a fresh round of funding.

A key growth factor for the lutein market is the increasing prevalence of eye-related disorders, including age-related macular degeneration and cataracts. With aging populations worldwide, the need for natural eye health solutions is rising, pushing lutein-based products into mainstream healthcare and wellness practices. MDARD provides nearly $400K in funding through its new Farm to Family Program.

On the demand side, there is a strong push from consumers for natural and plant-derived ingredients. Lutein fits into this trend, as it is sourced from marigold flowers and other natural origins, aligning with the clean-label movement and the rising shift toward organic nutritional products. Cano-ela secures €1.6M to speed up the development of seed-based ingredients. BinSentry raises $50M to modernize animal feed supply chains using AI-powered sensor solutions.

Key Takeaways

- The Global Lutein Market is expected to be worth around USD 653.9 million by 2034, up from USD 361.7 million in 2024, and is projected to grow at a CAGR of 6.1% from 2025 to 2034.

- Natural lutein held a 74.5% share, driven by preference for plant-based health products.

- Powder accounted for 38.4% and was favored for easy blending in supplements and food formulations.

- Dietary supplements led with 46.7%, supported by rising consumer focus on preventive eye health.

- Europe’s 46.2% market share, worth USD 167.1 Mn, highlights strong consumer health awareness.

By Source Analysis

Natural held a 74.5% share, reflecting consumer preference for plant-based lutein.

In 2024, Natural held a dominant market position in the By Source segment of the Lutein Market, with a 74.5% share. This strong presence is largely attributed to the growing preference for naturally derived ingredients among consumers who are increasingly prioritizing clean-label and plant-based products. Natural lutein, commonly extracted from marigold flowers and other botanical sources, is perceived as safer and more effective compared to synthetic alternatives, which has significantly boosted its acceptance across dietary supplements, fortified foods, and pharmaceutical applications.

The dominance of natural lutein is also supported by its alignment with the global shift toward sustainable and eco-friendly production practices. With rising health awareness, consumers are actively seeking products that carry natural origins, particularly for eye health, cognitive support, and skin benefits. This trend has encouraged manufacturers to expand their natural lutein portfolios to meet the demand for premium, plant-based nutrition solutions.

Moreover, regulatory bodies and health organizations have been increasingly supportive of natural formulations, further encouraging their widespread use. The strong consumer trust in naturally sourced lutein ensures its continued leadership within the segment. As awareness of preventive healthcare expands, natural lutein is expected to maintain its growth trajectory, solidifying its market dominance in the years ahead.

By Form Analysis

Powder captured 38.4% share, offering stability and versatile product applications.

In 2024, Powder held a dominant market position in the By Form segment of the Lutein Market, with a 38.4% share. The popularity of powdered lutein stems from its versatility and stability, making it suitable for a wide range of applications across dietary supplements, functional foods, and nutraceuticals. Powder form is easier to transport, store, and blend with other ingredients compared to liquid or beadlet forms, which enhances its appeal for both manufacturers and end-users.

The dominance of the powder form is also driven by the rising consumer preference for convenient dosage formats. Powdered lutein can be easily mixed into smoothies, beverages, and food preparations, supporting the trend toward functional foods enriched with natural antioxidants. Its adaptability to various product formulations allows companies to cater to diverse consumer needs, ranging from eye health supplements to general wellness products.

Additionally, advancements in extraction and drying technologies have improved the bioavailability and quality of powdered lutein, making it more effective in delivering health benefits. With growing awareness of preventive healthcare, the powdered form is expected to maintain its strong position, reinforcing its role as the preferred choice in the lutein market.

By Application Analysis

Dietary supplements led with a 46.7% share, driven by rising health awareness.

In 2024, Dietary Supplements held a dominant market position in the By Application segment of the Lutein Market, with a 46.7% share. This strong position is primarily driven by the growing consumer focus on preventive healthcare and the increasing awareness of eye health benefits associated with lutein consumption. As cases of age-related macular degeneration, cataracts, and general vision problems continue to rise, especially among aging populations, dietary supplements fortified with lutein have become a preferred solution for maintaining long-term eye health.

The demand for lutein in supplement form is further boosted by its convenience and accessibility. Capsules, tablets, and soft gels are widely available through pharmacies, health stores, and online platforms, making it easy for consumers to incorporate lutein into their daily routines. This accessibility has significantly contributed to the segment’s leadership, particularly in developed markets where nutritional supplementation is part of regular health practices.

In addition to eye care, dietary supplements containing lutein are also being marketed for broader benefits such as cognitive function support and skin protection against oxidative stress. With increasing consumer trust in natural antioxidants and rising disposable incomes, the dietary supplements segment is expected to sustain its growth momentum, reinforcing its leading role within the lutein market.

Key Market Segments

By Source

- Natural

- Synthetic

By Form

- Powder

- Oil Suspension

- Emulsion

- Beadlet

By Application

- Dietary Supplements

- Food and Beverage

- Pharmaceuticals

- Animal Feed

- Others

Driving Factors

Rising Eye Health Awareness Boosts Lutein Demand

One of the biggest driving factors for the lutein market is the rising awareness about eye health among people of all age groups. With increasing exposure to digital screens, smartphones, and artificial lighting, concerns about vision problems have grown sharply. Lutein, being a natural antioxidant that protects the eyes from harmful blue light and oxidative stress, has gained strong consumer interest.

The growing number of cases related to age-related macular degeneration and cataracts, especially among the elderly population, has further increased demand. Governments and health organizations are also spreading awareness about preventive nutrition, encouraging people to include lutein supplements in their daily lives.

Restraining Factors

Limited Awareness in Developing Regions Restrains Growth

A major restraining factor for the lutein market is the lack of awareness about its health benefits in many developing regions. While consumers in advanced economies are familiar with lutein’s role in protecting eye health and preventing age-related vision problems, large parts of Asia, Africa, and Latin America still view it as a niche product. Limited knowledge, combined with lower purchasing power, restricts widespread adoption of lutein-based supplements and fortified foods.

In rural areas, traditional diets and limited access to nutritional products further slow down growth. Without strong educational campaigns or government-driven nutrition programs, consumer demand remains concentrated in urban centers, creating an uneven market landscape. This knowledge gap continues to challenge the global expansion of lutein products.

Growth Opportunity

Expanding Applications Beyond Eye Health Creates Opportunities

A major growth opportunity for the lutein market lies in expanding its applications beyond eye health into areas such as brain function, skin care, and cardiovascular wellness. Research studies increasingly highlight lutein’s antioxidant and anti-inflammatory properties, which make it valuable for protecting brain cells, supporting memory, and improving overall cognitive performance.

In the skincare industry, lutein is being recognized for its ability to protect skin from oxidative damage and UV stress, making it attractive for use in beauty and personal care products. Similarly, its potential in heart health opens doors to functional foods and nutraceuticals. By diversifying into these new areas, lutein can reach wider consumer segments and secure long-term growth across multiple industries.

Latest Trends

Rising Demand for Plant-Based and Natural Lutein

One of the latest trends shaping the lutein market is the growing demand for plant-based and naturally sourced ingredients. Consumers today are becoming more careful about what they eat and prefer clean-label products that come from natural origins. Lutein, commonly extracted from marigold flowers and leafy greens, fits perfectly into this trend as it is plant-derived and free from synthetic chemicals.

The clean-label movement, along with the rise of vegan and vegetarian lifestyles, is encouraging companies to highlight the natural sourcing of lutein in their supplements and fortified foods. This shift not only increases consumer trust but also strengthens market opportunities, as natural lutein is seen as safer, healthier, and more sustainable compared to synthetic alternatives.

Regional Analysis

In 2024, Europe dominated the Lutein Market with a 46.2% share, reaching /USD 167.1 Mn.

The lutein market shows varied regional dynamics, with Europe emerging as the leading region in 2024. Europe held a dominant share of 46.2%, valued at USD 167.1 million, making it the largest contributor to global market revenues. The region’s leadership is supported by a high level of consumer awareness about preventive healthcare, particularly eye health, as aging populations continue to face risks of vision-related conditions such as macular degeneration and cataracts. Strong regulatory support for natural and plant-derived supplements further enhances the adoption of lutein across dietary products and fortified foods.

In North America, the market is driven by rising consumer preference for dietary supplements and the growing focus on eye health due to increasing screen exposure. Asia Pacific is witnessing robust growth as urban populations become more health-conscious and demand for functional foods accelerates.

Meanwhile, the Middle East & Africa and Latin America show steady uptake, supported by gradual improvements in healthcare awareness and rising disposable incomes. However, Europe’s strong position, backed by well-established supplement markets and supportive healthcare initiatives, ensures its dominance in the global lutein landscape, with its 46.2% share setting the benchmark for other regions to follow.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE continues to demonstrate its strong expertise in nutritional ingredients by expanding its lutein-based offerings with a focus on sustainability and natural sourcing. The company’s emphasis on research-driven formulations ensures that its lutein products maintain high bioavailability, which appeals to health-conscious consumers seeking preventive eye care and wellness solutions.

Kemin Industries, Inc. has established itself as a trusted supplier of naturally sourced lutein, particularly from marigold flowers. Its focus on high-quality extraction and purification processes has reinforced consumer confidence in natural lutein, while its broad portfolio caters to both human nutrition and animal health sectors.

Allied Biotech Corporation stands out for its specialization in carotenoid production, where lutein is a core product. With expertise in producing stable formulations suitable for various food and beverage applications, Allied Biotech is expanding the reach of lutein beyond supplements, strengthening its role in the functional food space.

Koninklijke DSM N.V., with its strong global presence, is advancing innovation in lutein through science-based nutrition. The company’s investment in research and technology allows it to position lutein not only for eye health but also for emerging areas such as cognitive wellness and skin protection.

Top Key Players in the Market

- BASF SE

- Kemin Industries, Inc.

- Allied Biotech Corporation

- Koninklijke DSM N.V.

- Xi’an Green Spring Technology Co., Ltd

- Synthite Industries Ltd.

- Bio Actives Japan Corporation

- Santen Pharmaceutical Co., Ltd.

- Xi’an Healthful Biotechnology Co., Ltd

Recent Developments

- In April 2025, BASF introduced three natural-based ingredients tailored for personal care, under its “Longevity Ecosystem” showcased at in‑cosmetics Global: Verdessence® Maize, Lamesoft® OP Plus, and Dehyton® PK45 GA/RA. These innovations emphasize biodegradable, plant‑derived alternatives—but none reference lutein directly—highlighting BASF’s shift toward sustainable personal care ingredients rather than carotenoids.

- In March 2025, at SupplySide Connect in New Jersey, Kemin showcased its science-backed nutritional solutions—including its lutein-based products like FloraGLO®, OPTISHARP®, and Macu‑LZ™—emphasizing their benefits for eye, brain, and skin health across all stages of life.

Report Scope

Report Features Description Market Value (2024) USD 361.7 Million Forecast Revenue (2034) USD 653.9 Million CAGR (2025-2034) 6.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Natural, Synthetic), By Form (Powder, Oil Suspension, Emulsion, Beadlet), By Application (Dietary Supplements, Food and Beverage, Pharmaceuticals, Animal Feed, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF SE, Kemin Industries, Inc., Allied Biotech Corporation, Koninklijke DSM N.V., Xi’an Green Spring Technology Co., Ltd, Synthite Industries Ltd., Bio Actives Japan Corporation, Santen Pharmaceutical Co., Ltd., Xi’an Healthful Biotechnology Co., Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- BASF SE

- Kemin Industries, Inc.

- Allied Biotech Corporation

- Koninklijke DSM N.V.

- Xi'an Green Spring Technology Co., Ltd

- Synthite Industries Ltd.

- Bio Actives Japan Corporation

- Santen Pharmaceutical Co., Ltd.

- Xi'an Healthful Biotechnology Co., Ltd

Our Clients

- 156097

- August 2025