Global Lipstick Market Size, Share, Growth Analysis By Form (Stick, Liquid, Palette), By Product Type (Matte, Glossy, Lip Powder, Others), By Distribution Channel (Hypermarkets and Supermarkets, Specialty Stores, Online Retail, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182293

- Number of Pages: 385

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

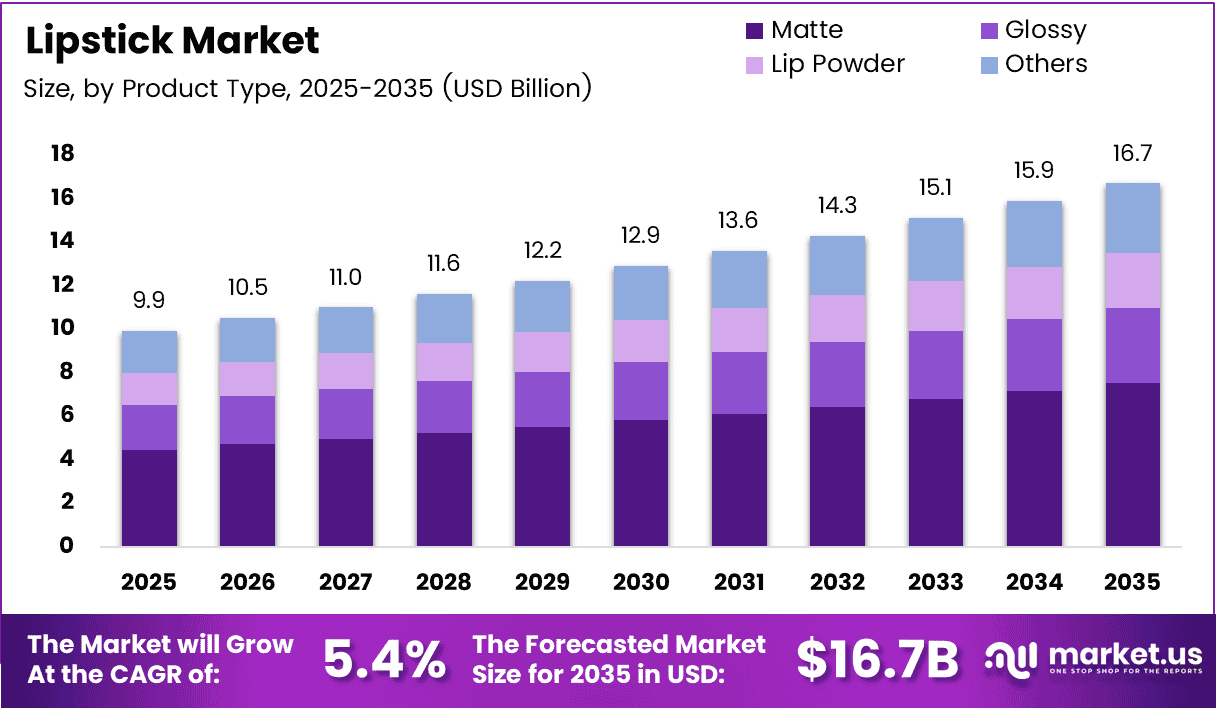

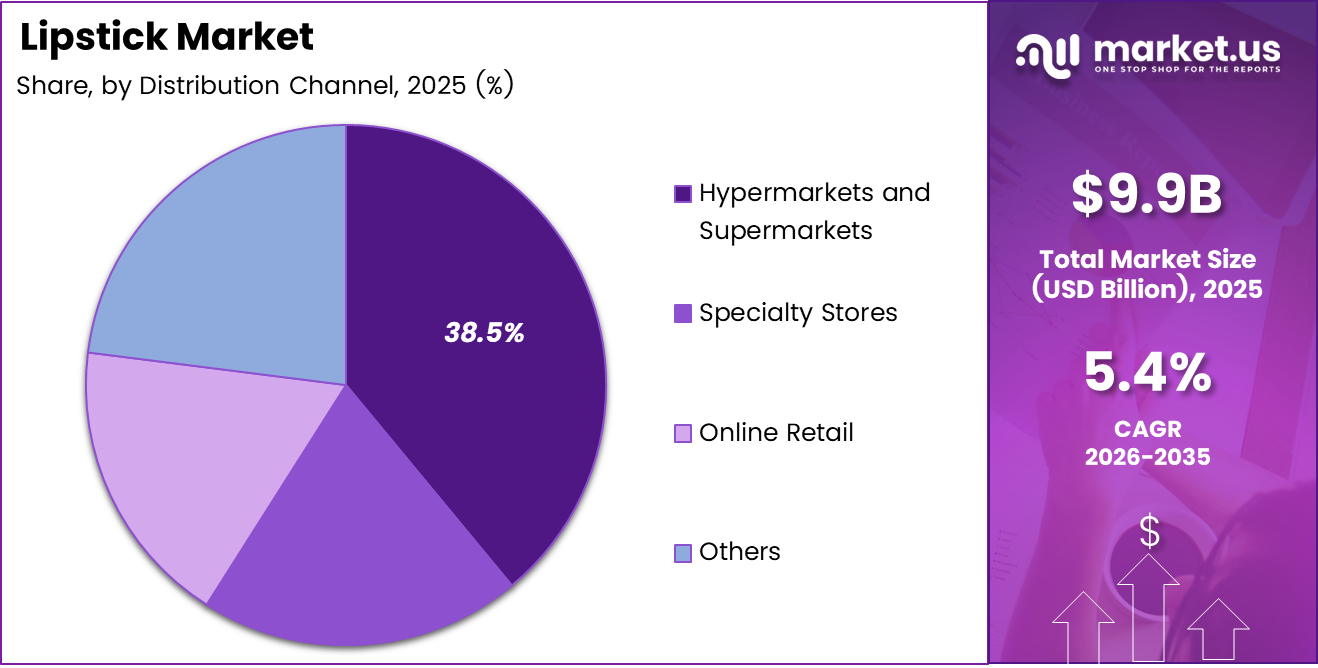

Global Lipstick Market size is expected to be worth around USD 16.7 Billion by 2035 from USD 9.9 Billion in 2025, growing at a CAGR of 5.4% during the forecast period 2026 to 2035.

The lipstick market covers a broad category of color cosmetics designed for lip coloration, care, and enhancement. Products range from traditional stick formats to liquid lipsticks, lip powders, and hybrid lip care treatments. This market sits at the intersection of beauty, personal care, and self-expression — three consumer motivations that prove resilient across economic cycles.

Social media platforms have structurally rewired how consumers discover and trial lip color products. Beauty influencers drive product launches from niche to mainstream within days. This compresses the traditional product adoption curve and forces brands to operate with shorter innovation windows and faster go-to-market cycles.

Female workforce participation in urban emerging economies continues to lift daily makeup usage rates. As professional and social contexts overlap, lipstick moves from occasional to habitual purchase — which structurally supports repeat buying and brand loyalty in ways that benefit both mass and prestige segments.

Premium and luxury cosmetic brands have accelerated their lipstick portfolio expansions. In August 2025, Louis Vuitton launched La Beauté Louis Vuitton featuring LV Rouge lipsticks, signaling that ultra-luxury houses now view lip color as a core entry-point product — not a secondary category. This raises the competitive floor for established beauty players.

Clean beauty and ingredient transparency have become purchase criteria, not just marketing claims. Consumers in North America and Western Europe actively scrutinize formulations for synthetic compounds. This shift forces reformulation investment across mid-tier brands, adding cost pressure while simultaneously opening space for natural-ingredient-led product lines.

According to a study published in the IJPS Journal, an epazote-based biolipstick formulation achieved 100% color consistency as measured by colorimeter using the L*a*b* system. This level of performance from a plant-derived formula indicates that natural ingredient substitution no longer requires a quality trade-off — a signal that will accelerate clean-label adoption across mainstream lipstick manufacturing.

Additionally, biolipstick formulations demonstrated statistically significant antimicrobial performance against Staphylococcus epidermidis and Candida albicans compared to commercial controls (p < 0.05 via ANOVA), per SARSEF research. This matters for the market because antimicrobial efficacy adds a functional health dimension to what was previously a purely aesthetic product category — expanding the addressable consumer base.

Key Takeaways

- The global lipstick market is valued at USD 9.9 Billion in 2025 and forecast to reach USD 16.7 Billion by 2035.

- The market grows at a CAGR of 5.4% during the forecast period 2026 to 2035.

- By Form, Stick leads the market with a 67.1% share in 2025.

- By Product Type, Matte holds the dominant position with a 44.6% share.

- By Distribution Channel, Hypermarkets and Supermarkets account for 38.5% of sales.

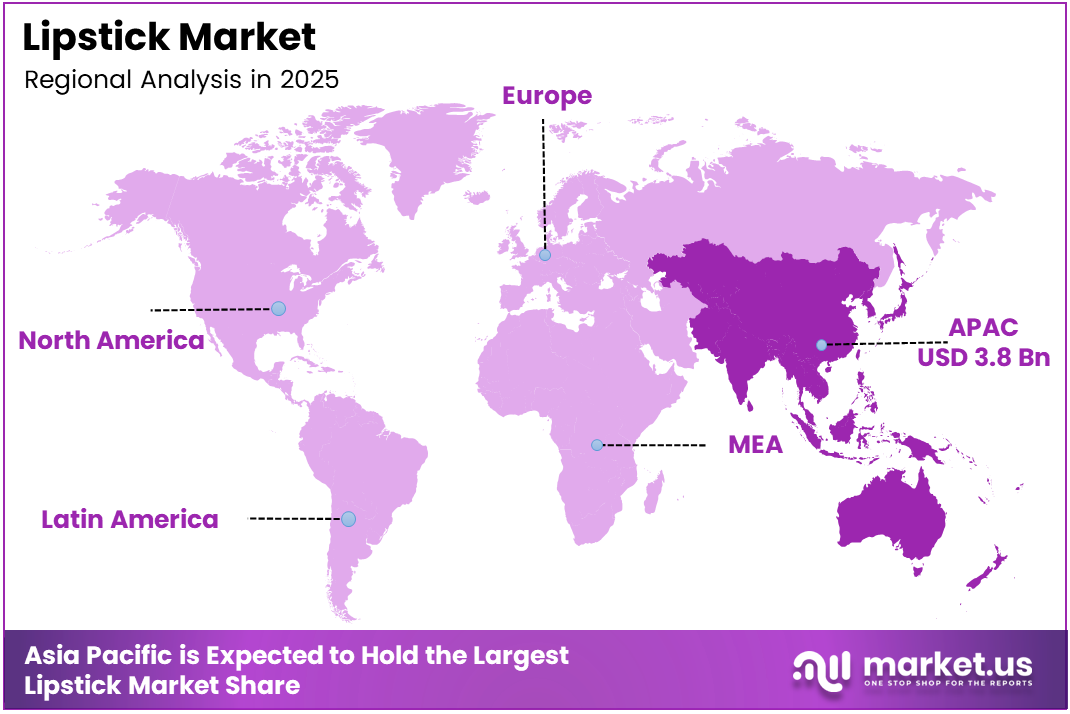

- Asia Pacific dominates the regional landscape with a 38.5% share, valued at USD 3.8 Billion.

- Key players include Unilever, L’Oréal Group, Coty Inc., Amorepacific Corporation, Shiseido Company, and others.

Form Analysis

Stick dominates with 67.1% due to established consumer habit and universal retail availability.

In 2025, Stick held a dominant market position in the By Form segment of the Lipstick Market, with a 67.1% share. This dominance reflects decades of consumer familiarity and the format’s unmatched shelf presence across all retail channels. Stick lipstick requires no applicator, delivers precise application, and carries strong repurchase rates — structural advantages that competing formats have yet to displace.

Liquid lipstick carries the highest innovation intensity within the By Form segment. Its ability to deliver full-pigment matte or glossy finishes in a single application has made it the preferred format for social-media-driven product launches. Liquid formats attract younger buyers who prioritize longevity and photogenic color payoff over the tactile familiarity of traditional stick formats.

Palette differentiates through versatility and multi-shade access in a single purchase. Palettes appeal to professional makeup artists and enthusiasts who require color mixing and customization. However, their higher price point and lower repurchase frequency position them as a specialty format — commanding strong margins but limited volume contribution relative to stick and liquid formats.

Product Type Analysis

Matte dominates with 44.6% due to social media-driven demand for high-pigmentation, long-wear formulas.

In 2025, Matte held a dominant market position in the By Product Type segment of the Lipstick Market, with a 44.6% share. Social media beauty culture has firmly embedded matte finishes as the benchmark for professional-looking lip color. Its transfer-resistant performance and all-day wear reduce touch-up frequency — a practical benefit that reinforces consumer preference across professional and lifestyle contexts.

Glossy lipstick serves as the entry-point format for first-time and younger lip color buyers. Its lower pigmentation barrier and forgiving application process make it accessible for daily casual use. Glossy formats also benefit from the ongoing hybrid trend — brands increasingly infuse gloss with skincare actives, repositioning it as a lip treatment product rather than a pure color cosmetic.

Lip Powder occupies an emerging and differentiating niche within the product type spectrum. Its ultra-long-wear positioning and unique application ritual attract experimentally-minded consumers seeking alternatives to standard formats. However, limited consumer familiarity and a steeper learning curve restrict its penetration to specialist channels and digitally engaged beauty segments.

Others within product type include tinted balms, sheer formulas, and multi-functional lip treatments. In May 2025, Glow Recipe launched its first tinted Glass Balm Lip Treatment, illustrating how brands embed color payoff within skincare-positioned products. This sub-segment captures crossover buyers who prioritize ingredient benefits alongside aesthetics.

Distribution Channel Analysis

Hypermarkets and Supermarkets dominate with 38.5% due to high foot traffic and accessible price-point product mix.

In 2025, Hypermarkets and Supermarkets held a dominant market position in the By Distribution Channel segment of the Lipstick Market, with a 38.5% share. Mass retail channels provide the broadest geographic reach and attract value-conscious shoppers who prefer to physically evaluate color and texture before purchase. This channel disproportionately serves mid-tier and mass-market lipstick brands with high repurchase velocity.

Specialty Stores serve as the primary channel for premium and prestige lipstick brands. Dedicated beauty retailers provide trained staff, brand storytelling environments, and curated assortments — conditions that convert trial into loyalty for higher price-point products. This channel commands lower volume but higher basket values and stronger brand equity outcomes.

Online Retail has restructured the competitive dynamics for direct-to-consumer lipstick brands. E-commerce enables smaller indie brands to compete nationally without the capital requirement of shelf space. Virtual shade-matching tools and augmented reality try-on technology are actively reducing the color selection barrier — historically online retail’s largest conversion hurdle in color cosmetics.

Others includes direct selling, salon retail, and duty-free channels. Direct selling remains structurally relevant in markets where brands such as Avon maintain strong independent representative networks. These channels sustain personalized selling models that generate above-average order values and strong customer retention in developing market contexts.

Key Market Segments

By Form

- Stick

- Liquid

- Palette

By Product Type

- Matte

- Glossy

- Lip Powder

- Others

By Distribution Channel

- Hypermarkets and Supermarkets

- Specialty Stores

- Online Retail

- Others

Drivers

Social Media Beauty Culture and Rising Female Workforce Participation Accelerate Lipstick Consumption Across Urban Markets

Social media platforms have fundamentally changed how consumers engage with lip color. Beauty influencers can turn an unknown lipstick shade into a sell-out product within hours of posting. This compresses product lifecycles, increases trial frequency, and sustains consumer spending on color cosmetics well beyond seasonal purchase patterns.

Rising female workforce participation in urban emerging economies directly lifts daily makeup usage rates. As women spend more time in professional environments, lipstick transitions from an occasional purchase to a routine product. This behavioral shift builds habitual repurchase cycles — which structurally benefit brands with strong retail availability and consistent shade portfolios.

Continuous formulation innovation also sustains consumer interest and repeat purchasing. Long-lasting, smudge-proof, and transfer-resistant formulas address real functional needs — particularly for working professionals and consumers in humid climates. In August 2025, Louis Vuitton launched LV Rouge lipsticks within its La Beauté collection, signaling that even ultra-luxury houses recognize performance attributes as essential purchase drivers, not just aesthetics.

Restraints

Minimal Makeup Trends and Ingredient Regulation Complexity Limit Lipstick Market Expansion

A measurable shift toward natural beauty aesthetics and “no-makeup makeup” looks reduces lipstick’s frequency of use among specific consumer segments. As skin-first beauty routines displace color-first habits, brands face declining usage occasions per buyer — compressing per-capita category spending in Western markets where this trend is most pronounced.

Stringent cosmetic ingredient regulations across the US, EU, and key Asian markets create compliance cost burdens that disproportionately affect mid-tier and indie brands. Reformulation requirements triggered by ingredient bans add development timelines and cost. According to research published in Storage.googleapis/ejpmr, plant-based lipstick formulations show perfume stability decline after 3 days — indicating that natural ingredient substitution requires further stabilization investment before it can fully replace conventional formulations at scale.

The regulatory fragmentation across global markets forces multinational brands to maintain multiple regional formulations for the same product. This raises SKU management complexity, increases inventory costs, and slows speed-to-market for new launches. Smaller brands without dedicated regulatory teams face the highest barriers — limiting their ability to compete in high-growth international markets despite strong product innovation.

Growth Factors

Clean Beauty Demand, E-Commerce Expansion, and AI-Powered Personalization Open New Revenue Channels for Lipstick Brands

Consumer demand for vegan, cruelty-free, and clean-label lipstick products is creating a structurally distinct sub-market with premium pricing power. According to research published via Storage.googleapis/ejpmr, plant-based lipstick formulations using turmeric, beetroot, and papaya achieve melting points of 60–63°C — matching conventional lipstick performance benchmarks. This confirms that clean-label formulations can deliver equivalent product quality, removing the performance trade-off that previously limited their mainstream appeal.

Expanding e-commerce beauty retail channels allow brands to reach consumers directly, bypassing traditional retail margin structures. Direct-to-consumer models improve data capture, enable personalization, and support faster product iteration. Brands that invest in digital-first distribution now build structural advantages in consumer relationships that offline-dependent competitors cannot quickly replicate.

Gender-neutral and inclusive beauty positioning expands the total addressable market beyond the traditionally female-skewed lipstick buyer base. AI-powered shade matching tools reduce the risk of wrong color purchase — historically one of the highest barriers to online lipstick conversion. Brands that deploy these tools measurably improve digital conversion rates and reduce return rates, improving unit economics across their e-commerce operations.

Emerging Trends

Skincare-Infused Lip Color, Sustainable Packaging, and Celebrity Brand Collaborations Reshape the Lipstick Category

Hydrating lipsticks formulated with hyaluronic acid, vitamin E, and other skincare actives are dissolving the boundary between lip care and lip color. According to research published in the IJPS Journal, herbal lipstick formulations maintain a pH of approximately 6 — closely aligned with natural skin pH. This compatibility supports consumer confidence in ingredient safety and positions functional lip color as a daily skincare step rather than a purely cosmetic choice.

Sustainable and refillable lipstick packaging is shifting from a niche positioning to a mainstream brand expectation. As environmental regulations tighten and consumer scrutiny of cosmetic packaging waste intensifies, brands that offer refillable systems protect both their margin structure and their brand reputation. In January 2025, Celine released the full Le Rouge Celine collection with 15 satin-finish shades, reflecting luxury brands’ integration of quality formulation with refined packaging as a combined value proposition.

Celebrity beauty brands and limited-edition collaborations generate outsized consumer attention relative to their product volume. These launches create urgency-driven purchasing behavior and compress decision timelines. For established brands, co-creation with celebrity names provides renewed relevance in competitive retail environments — particularly in the specialty and online channels where discovery-driven purchases are highest.

Regional Analysis

Asia Pacific Dominates the Lipstick Market with a Market Share of 38.5%, Valued at USD 3.8 Billion

Asia Pacific leads global lipstick consumption with a 38.5% market share valued at USD 3.8 Billion in 2025. China, Japan, South Korea, and India collectively drive this position through high beauty product spending, deeply embedded cosmetics culture, and the influence of K-beauty and J-beauty trends. South Korea’s export-driven beauty ecosystem continues to set global formulation and packaging standards, pulling regional consumer expectations higher.

North America Lipstick Market Trends

North America holds a structurally mature lipstick market underpinned by high per-capita beauty spending and established prestige retail infrastructure. Premium and clean beauty sub-categories drive above-average growth within the region. The US market specifically benefits from strong influencer marketing ecosystems and a retail environment that supports both mass and luxury lipstick distribution at scale.

Europe Lipstick Market Trends

Europe’s lipstick market operates under the world’s most stringent cosmetic ingredient regulations, which simultaneously constrain conventional formulations and accelerate clean-label innovation. Western European consumers show above-average preference for sustainable packaging and natural ingredients. French and Italian heritage brands maintain strong regional equity, while regulatory compliance requirements create barriers for non-European market entrants.

Latin America Lipstick Market Trends

Latin America presents a high-potential lipstick market driven by young demographic profiles, strong beauty culture particularly in Brazil and Mexico, and expanding middle-class purchasing power. Direct selling channels retain significant structural importance in the region, sustaining brands that operate through independent representative networks. E-commerce penetration is rising but remains below North American and Asian levels.

Middle East and Africa Lipstick Market Trends

The Middle East and Africa region combines two distinct market structures. Gulf Cooperation Council countries show high demand for luxury and prestige lip color products driven by high disposable incomes and strong brand awareness. Sub-Saharan African markets offer longer-term volume growth potential as urbanization increases and modern retail infrastructure expands across major metropolitan centers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Unilever approaches the lipstick market through its mass-market personal care infrastructure, leveraging global distribution reach across more than 190 countries. Its strategic advantage lies in scaling accessible price-point lip color products through hypermarket and supermarket channels — the dominant distribution format at 38.5% share. However, its portfolio breadth also creates brand dilution risk as prestige competitors sharpen their positioning.

L’Oréal Group operates the most diversified lipstick portfolio across mass, mid-tier, and luxury segments simultaneously. This multi-tier architecture allows L’Oréal to capture consumer spend at every price point and reduces exposure to any single market segment’s fluctuation. Its R&D investment in long-wear, transfer-resistant formulations directly addresses the functional demands that social media beauty culture has made non-negotiable for mainstream buyers.

Coty Inc. has strategically repositioned from a broad cosmetics conglomerate toward focused prestige and color cosmetics growth. Its lipstick portfolio benefits from strong brand heritage in color categories and a distribution network that spans both specialty retail and e-commerce. Coty’s ability to support celebrity and licensed brand collaborations provides a competitive mechanism to generate high-frequency consumer engagement around new launches.

Amorepacific Corporation holds a structurally advantaged position as a native player in Asia Pacific — the market’s dominant region at 38.5% share. Its deep integration within South Korean beauty culture enables faster trend identification and shorter product development cycles than Western multinationals operating in the region. Amorepacific’s K-beauty heritage translates directly into premium pricing power in export markets across Southeast Asia and beyond.

Key Players

- Unilever

- L’Oréal Group

- Coty Inc.

- Amorepacific Corporation

- Shiseido Company

- Revlon Inc.

- Hermès

- Procter & Gamble

- Beiersdorf AG

- Chanel

- Mary Kay Inc.

- Dior

- Avon Products Inc.

- Estée Lauder Companies

- Kakao Corporation

Recent Developments

- January 2024 — Yellow Wood Partners portfolio company Suave Brands Company signed an agreement to acquire ChapStick from Haleon, marking a significant ownership transition for one of the world’s most recognized lip care brands and signaling private equity confidence in the lip treatment and care segment.

- May 2025 — Dior launched Addict Lip Glow Butter, expanding its lip care-meets-color portfolio with a formulation designed to deliver both hydration and tinted color payoff — directly targeting the hybrid skincare-cosmetic buyer segment that has driven lip balm-to-lipstick crossover purchases.

- August 2025 — Louis Vuitton launched La Beauté Louis Vuitton collection featuring LV Rouge lipsticks, representing the brand’s formal entry into prestige lip color and reinforcing the ultra-luxury segment’s commitment to color cosmetics as a core revenue category alongside fragrance and skincare.

Report Scope

Report Features Description Market Value (2025) USD 9.9 Billion Forecast Revenue (2035) USD 16.7 Billion CAGR (2026-2035) 5.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Stick, Liquid, Palette), By Product Type (Matte, Glossy, Lip Powder, Others), By Distribution Channel (Hypermarkets and Supermarkets, Specialty Stores, Online Retail, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Unilever, L’Oréal Group, Coty Inc., Amorepacific Corporation, Shiseido Company, Revlon Inc., Hermès, Procter & Gamble, Beiersdorf AG, Chanel, Mary Kay Inc., Dior, Avon Products Inc., Estée Lauder Companies, Kakao Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Unilever

- L'Oréal Group

- Coty Inc.

- Amorepacific Corporation

- Shiseido Company

- Revlon Inc.

- Hermès

- Procter & Gamble

- Beiersdorf AG

- Chanel

- Mary Kay Inc.

- Dior

- Avon Products Inc.

- Estée Lauder Companies

- Kakao Corporation

Our Clients

- 182293

- Mar 2026