Global Lactulose Market Size, Share, And Business Benefits By Form (Syrup/Liquid, Powder, Crystalline, Others), By Function (Sweetening Agent, Laxative, Hepatic Encephalopathy, Others), By Applications (Pharmaceutical, Food and Beverage, Animal Feed, Veterinary, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: September 2025

- Report ID: 158747

- Number of Pages: 372

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

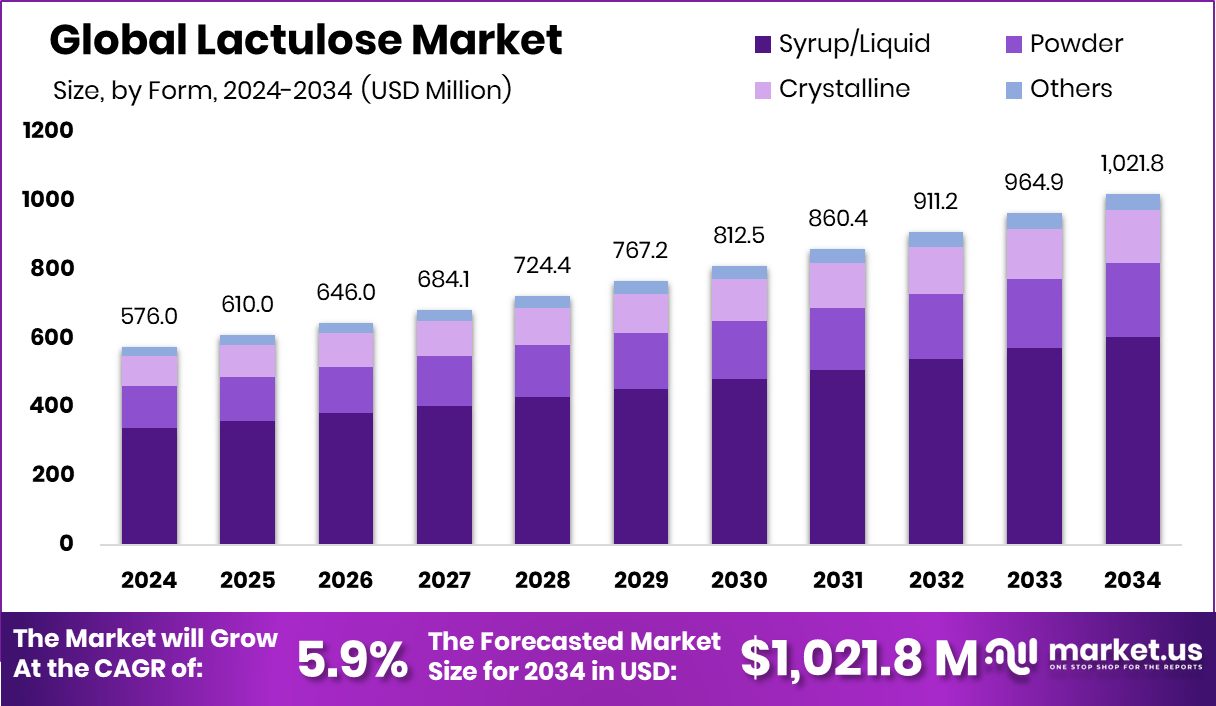

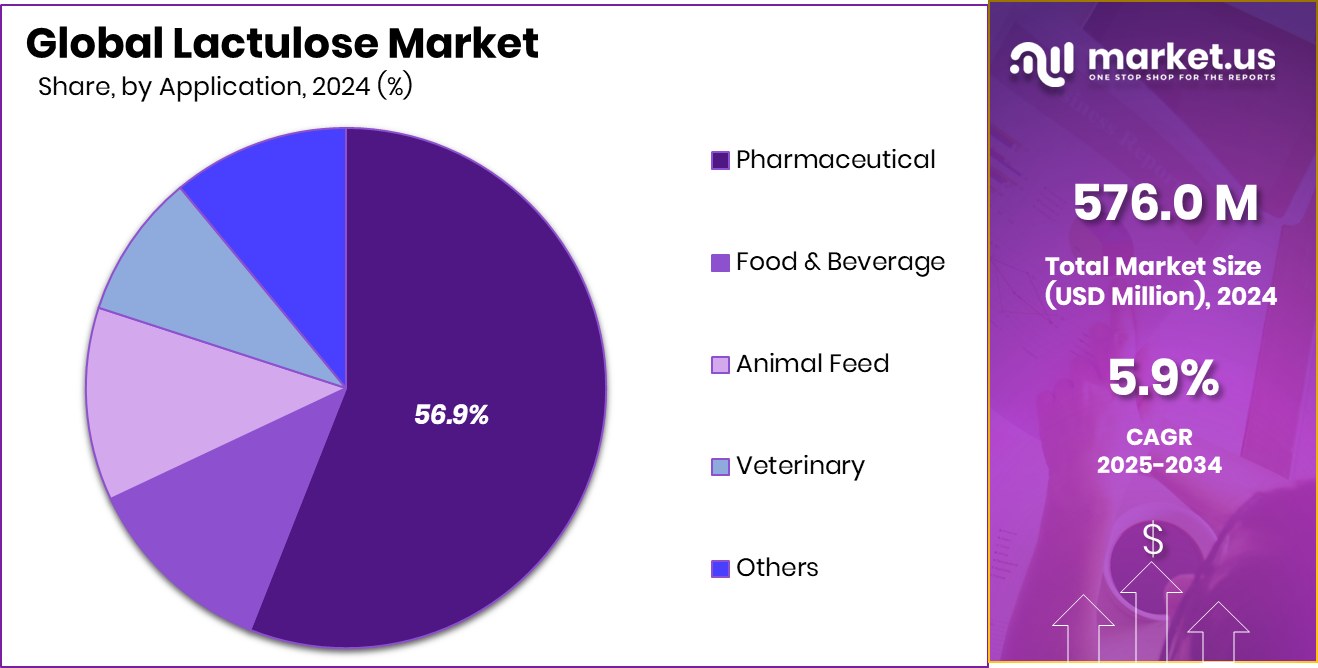

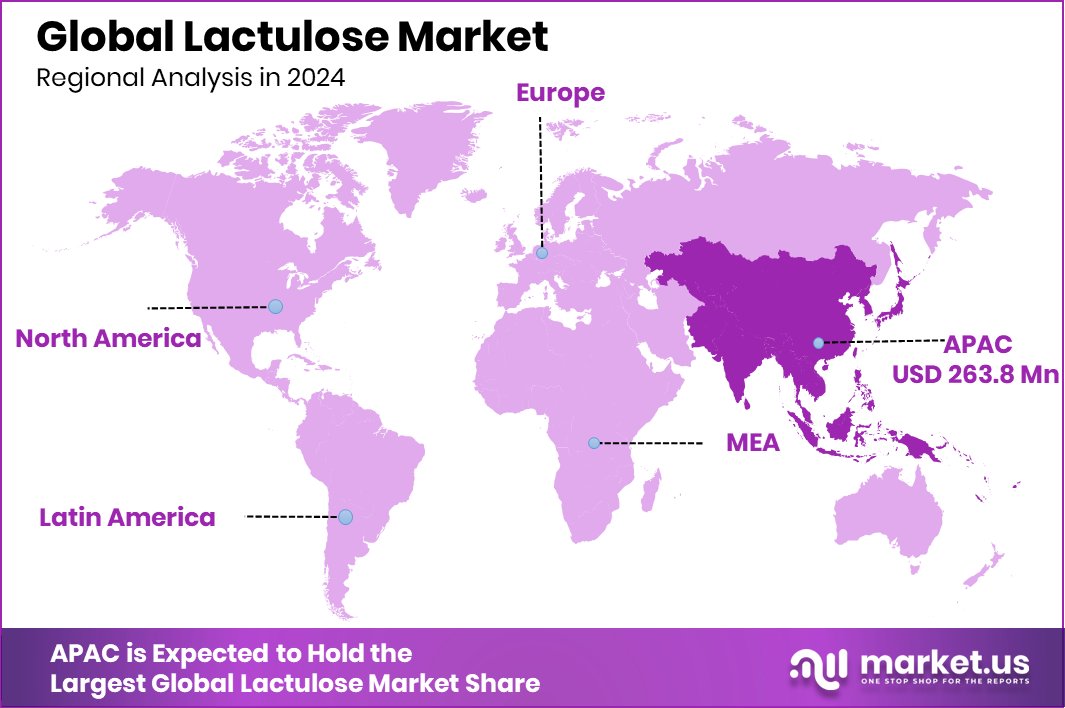

The Global Lactulose Market is expected to be worth around USD 1,021.8 million by 2034, up from USD 576.0 million in 2024, and is projected to grow at a CAGR of 5.9% from 2025 to 2034. With a 45.80% share, the Asia Pacific Lactulose Market generated USD 263.8 Mn revenue in 2024.

Lactulose is a synthetic sugar made from galactose and fructose. It is not absorbed in the small intestine and passes into the colon, where it is broken down by bacteria into acids that draw water into the bowel. This action softens stools and helps in treating constipation. Beyond this, lactulose is widely prescribed to manage hepatic encephalopathy, as it reduces the absorption of ammonia in the gut and lowers toxin levels in patients with liver disease.

The lactulose market refers to the global demand and supply of this therapeutic sugar, used primarily in pharmaceuticals for gastrointestinal health and liver disease management. The market is shaped by rising cases of chronic constipation, increasing liver disorders, and the growing focus on digestive health. In recent years, governments and medical foundations have supported liver research, boosting awareness and accessibility of lactulose-based treatments.

For instance, the AASLD Foundation in the United States has specific grant programs for hepatic encephalopathy research, including one-year awards of around USD 50,000. In 2023, the foundation committed USD 2 million to liver disease and hepatology research, supporting nearly 150 recipients.

The primary growth driver for the lactulose market is the rising prevalence of liver-related disorders and gastrointestinal diseases. With lifestyle changes and growing alcohol consumption, the incidence of cirrhosis and hepatic encephalopathy has increased worldwide. This, in turn, fuels the clinical use of lactulose as a first-line therapy in managing these complications.

Another strong factor is the growing awareness of digestive health, especially in aging populations where constipation is common. Lactulose, being non-addictive and safe for long-term use, is increasingly favored by doctors and patients alike. The rising healthcare spending across developed and emerging economies further adds to the product’s growing demand.

There is a significant opportunity in the expansion of lactulose applications beyond traditional therapies. Ongoing clinical studies are exploring its benefits in broader metabolic and gut-related disorders. Funding initiatives, such as those from the AASLD Foundation, highlight the increasing investment in liver health, which is expected to create fresh pathways for lactulose adoption in new treatment areas.

Key Takeaways

- The Global Lactulose Market is expected to be worth around USD 1,021.8 million by 2034, up from USD 576.0 million in 2024, and is projected to grow at a CAGR of 5.9% from 2025 to 2034.

- In the Lactulose Market, syrup and liquid form dominate with 59.2% market share.

- Laxative function leads the Lactulose Market, contributing 49.1% to overall segment growth globally.

- Pharmaceutical applications account for a 56.9% share, making them the largest driver in the Lactulose Market.

- The Asia Pacific Lactulose Market, valued at USD 263.8 Mn, accounted for a 45.80% share.

By Form Analysis

In the lactulose market, syrup and liquid form dominate with 59.2%.

In 2024, Syrup/Liquid held a dominant market position in the By Form segment of the Lactulose Market, accounting for a 59.2% share. This strong presence is driven by the preference of healthcare providers and patients for liquid formulations, as they offer easier dosing, faster absorption, and greater suitability for pediatric and geriatric use compared to other forms.

Syrup-based lactulose is widely prescribed in hospitals, clinics, and home care settings for the management of constipation and hepatic encephalopathy, making it the most trusted format in therapeutic use. The convenience of oral administration, coupled with growing demand in both developed and emerging markets, further reinforces syrup/liquid as the leading form of lactulose in the global marketplace.

By Function Analysis

As a laxative, lactulose accounts for 49.1% market share globally.

In 2024, Laxative held a dominant market position in the By Function segment of the Lactulose Market, capturing a 49.1% share. This leadership is largely due to the widespread use of lactulose as a safe and effective treatment for chronic constipation, particularly among elderly populations and individuals with sedentary lifestyles. The non-addictive nature of lactulose, along with its suitability for long-term use, has strengthened its adoption across hospitals, retail pharmacies, and home care.

Increasing awareness about digestive health and the growing prevalence of constipation-related disorders have further boosted the reliance on lactulose-based laxatives. This strong demand underlines its position as the primary therapeutic application within the global market.

By Applications Analysis

Pharmaceutical applications lead the lactulose market, holding 56.9% overall usage share.

In 2024, Pharmaceutical held a dominant market position in the By Applications segment of the Lactulose Market, accounting for a 56.9% share. The dominance of this segment is linked to the extensive use of lactulose in treating chronic constipation and managing hepatic encephalopathy, where it is considered a first-line therapy. The increasing incidence of liver diseases, coupled with rising healthcare awareness, has fueled demand for pharmaceutical-grade lactulose.

Its proven efficacy, safety profile, and inclusion in clinical guidelines have further cemented its adoption across hospitals, specialty clinics, and retail pharmacies. This consistent demand underscores the pharmaceutical segment as the core driver of market growth, making it the most influential application area for lactulose worldwide.

Key Market Segments

By Form

- Syrup/Liquid

- Powder

- Crystalline

- Others

By Function

- Sweetening Agent

- Laxative

- Hepatic Encephalopathy

- Others

By Applications

- Pharmaceutical

- Food and Beverage

- Animal Feed

- Veterinary

- Others

Driving Factors

Rising Digestive Disorders Boosting Lactulose Demand

One of the top driving factors for the Lactulose Market is the increasing number of people suffering from digestive disorders, especially chronic constipation. With changing diets, sedentary lifestyles, and aging populations, constipation has become a common health problem worldwide. Lactulose is widely used as a gentle and effective laxative that is safe for long-term use, making it a trusted option for both doctors and patients.

Its ability to improve bowel movements without addictive side effects has increased its preference in medical treatments. Additionally, elderly individuals and patients with limited mobility are frequent users of lactulose, which strengthens its demand. This rising patient base continues to push the growth of the lactulose market significantly.

Restraining Factors

High Treatment Costs Limiting Wider Lactulose Adoption

A key restraining factor for the Lactulose Market is the high cost of treatment in certain regions, which limits accessibility for many patients. While lactulose is an effective therapy for constipation and liver-related conditions, its pricing and recurring need for use can become a financial burden, particularly in low- and middle-income countries.

Limited insurance coverage for digestive health treatments further adds to the challenge, making patients opt for cheaper alternatives. In some healthcare systems, the lack of subsidies or reimbursement policies also slows down their adoption. As a result, despite its proven medical benefits, the higher costs associated with consistent lactulose use restrict its reach to a broader population.

Growth Opportunity

Expanding Use in Liver Disease Treatment Worldwide

A major growth opportunity for the Lactulose Market lies in its expanding use for managing liver-related conditions, particularly hepatic encephalopathy. As liver diseases continue to rise globally due to alcohol consumption, obesity, and viral infections, the need for effective therapies is growing rapidly. Lactulose plays a vital role in reducing toxin levels in the blood by lowering ammonia absorption, making it a first-choice treatment recommended by healthcare professionals.

The rising number of hospital admissions for liver complications and the focus on improving patient quality of life are creating strong demand for lactulose. With more emphasis on early diagnosis and treatment of liver diseases, this therapeutic sugar has a wide scope for future growth.

Latest Trends

Growing Preference for Liquid Lactulose Formulations

One of the latest trends in the Lactulose Market is the growing preference for liquid or syrup-based formulations. Patients and healthcare providers increasingly favor this form because it is easy to swallow, allows flexible dosing, and is well-suited for children and elderly patients. Unlike tablets or powders, liquid lactulose offers a faster onset of action and better patient compliance, making it the most trusted form in hospitals and clinics.

The convenience of adjusting doses for different age groups has also added to its popularity. With rising awareness of digestive health and the need for user-friendly medications, the shift toward liquid lactulose formulations is becoming a defining trend in shaping the future of the market.

Regional Analysis

In 2024, the Asia Pacific captured a 45.80% share of the Lactulose Market, worth USD 263.8 Mn.

The Lactulose Market shows varied regional dynamics across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, with Asia Pacific emerging as the dominant region in 2024. Asia Pacific accounted for 45.80% of the global market, generating USD 263.8 million in revenue. This strong position is supported by the rising prevalence of digestive health disorders, an increasing number of patients with liver diseases, and growing awareness about safe laxative use across densely populated countries.

Expanding healthcare infrastructure and higher accessibility to pharmaceutical products are further enhancing the adoption of lactulose in this region. North America and Europe also contribute significantly, backed by advanced healthcare systems and rising demand for therapies addressing chronic constipation and hepatic encephalopathy.

Meanwhile, Latin America and the Middle East & Africa are gradually expanding due to improving medical access and growing awareness of gastrointestinal care. However, Asia Pacific’s large patient base, coupled with increasing healthcare spending, positions it as the leading growth driver globally.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Fresenius Kabi maintained its strong role in the lactulose market through its focus on high-quality pharmaceutical formulations. The company’s broad presence in healthcare systems worldwide gives it an advantage in supplying lactulose as both a laxative and a therapeutic solution for hepatic encephalopathy. Its well-established hospital network and distribution reach continue to support its stable growth.

Orion Lifescience has positioned itself as a notable participant in the lactulose segment, with a clear focus on providing reliable and affordable formulations. Its strength lies in addressing the rising demand for digestive health solutions, particularly in emerging economies where cost-effective therapies are gaining traction. Orion’s strategic focus on expanding accessibility aligns with the rising need for safe and effective laxative treatments.

Morinaga Milk Industry Co., Ltd., known primarily for its dairy and nutrition expertise, has extended its capabilities into functional ingredients such as lactulose. Its diversified portfolio provides a unique edge, as the company integrates lactulose production into its broader nutrition and health offerings. This positions Morinaga not just as a supplier to the pharmaceutical industry, but also as a key contributor to health-focused product development.

Top Key Players in the Market

- Fresenius Kabi

- Orion Lifescience

- Morinaga Milk Industry Co., Ltd.

- Illovo

- Biofac

- Daiichi Sankyo

- Inalco SpA

- Casca Remedies

- Enrich Pharma

Recent Developments

- In June 2024, Rodney Rogan was appointed as Lactulose MD (Managing Director) at Illovo. This is a personnel leadership appointment, possibly tied to oversight of their lactulose-related business and ensuring strong governance.

- In October 2021, Biofac supplied lactulose liquid as an API (active pharmaceutical ingredient) in bulk, compliant with EP (European Pharmacopoeia) and USP standards. They also offer OEM finished lactulose products in various packaging.

Report Scope

Report Features Description Market Value (2024) USD 576.0 Million Forecast Revenue (2034) USD 1,021.8 Million CAGR (2025-2034) 5.9% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Syrup/Liquid, Powder, Crystalline, Others), By Function (Sweetening Agent, Laxative, Hepatic Encephalopathy, Others), By Applications (Pharmaceutical, Food and Beverage, Animal Feed, Veterinary, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Fresenius Kabi, Orion Lifescience, Morinaga Milk Industry Co., Ltd., Illovo, Biofac, Daiichi Sankyo, Inalco SpA, Casca Remedies, Enrich Pharma Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Fresenius Kabi

- Orion Lifescience

- Morinaga Milk Industry Co., Ltd.

- Illovo

- Biofac

- Daiichi Sankyo

- Inalco SpA

- Casca Remedies

- Enrich Pharma

Our Clients

- 158747

- September 2025