Global Greenhouse Film Market Size, Share, And Enhanced Productivity By Resin Type (Low-density polyethylene (LDPE), Linear low-density polyethylene (LLDPE), Ethylene-vinyl acetate (EVA), Polyvinyl Chloride (PVC)), By Width (4.5, 5.5, 7, 9, Others (9 to 20-meter)), By Thickness (80 to 150 Micron, 150 to 200 Micron, More than 200 Micron), By Application (Vegetables, Fruits, Flower and Ornaments, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: February 2026

- Report ID: 179264

- Number of Pages: 294

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

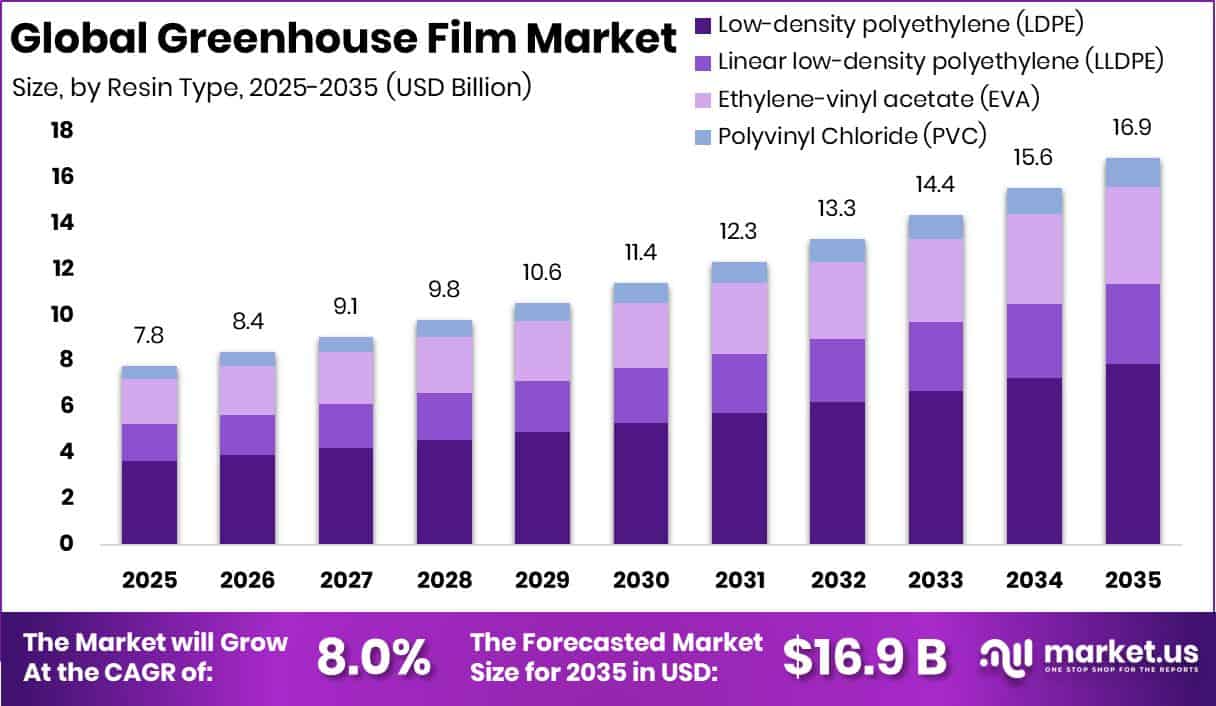

The Global Greenhouse Film Market is expected to be worth around USD 16.9 billion by 2035, up from USD 7.8 billion in 2025, and is projected to grow at a CAGR of 8.0% from 2026 to 2035. Asia Pacific maintains growth leadership with 44.8% share and a USD 3.4 Bn valuation.

Greenhouse films are protective plastic coverings designed to regulate temperature, humidity, and light inside greenhouse structures. These films help growers create a controlled environment that supports healthy plant development, protects crops from rain and pests, and extends the growing season. They are made in different resin types such as LDPE, LLDPE, EVA, and PVC to match varied strength and light-diffusion needs. The Greenhouse Film Market covers the production and use of these films across widths ranging from small 4.5–7-meter setups to larger 9–20-meter structures, as well as thickness options from 80 microns to above 200 microns used across vegetables, fruits, flowers, and ornamental plants.

Growth in this market is influenced by stronger demand for protected cultivation, especially as regions expand their agricultural networks. Many countries are increasing infrastructure spending, such as Dong Thap’s 242 billion VND investment in road and waterway maintenance, improving access for farming communities. Demand rises further as growers shift to higher-value produce, supported by initiatives like Moldovan farmers receiving $1M in grants for vegetable and herb processing.

Opportunities continue to widen as technology in agriculture advances. Developments such as Hudson River Biotechnology raising $5.9M for crop-focused CRISPR innovation and Idaho schools gaining $3M in fruit and vegetable grants push growers to adopt better environmental control. Consumer-driven sectors also support expansion, seen in food producers like Actual Veggies securing $7M Series A while expecting strong revenue growth, further encouraging investment in reliable greenhouse systems.

Key Takeaways

- The Global Greenhouse Film Market is expected to be worth around USD 16.9 billion by 2035, up from USD 7.8 billion in 2025, and is projected to grow at a CAGR of 8.0% from 2026 to 2035.

- Greenhouse Film Market growth is driven by low-density polyethylene, which leads with a strong 46.7% share.

- With 36.4% share for nine-meter width, the Greenhouse Film Market shows expanding structural preferences.

- Greenhouse Film Market demand rises as 150–200 micron thickness dominates applications with 52.6% adoption.

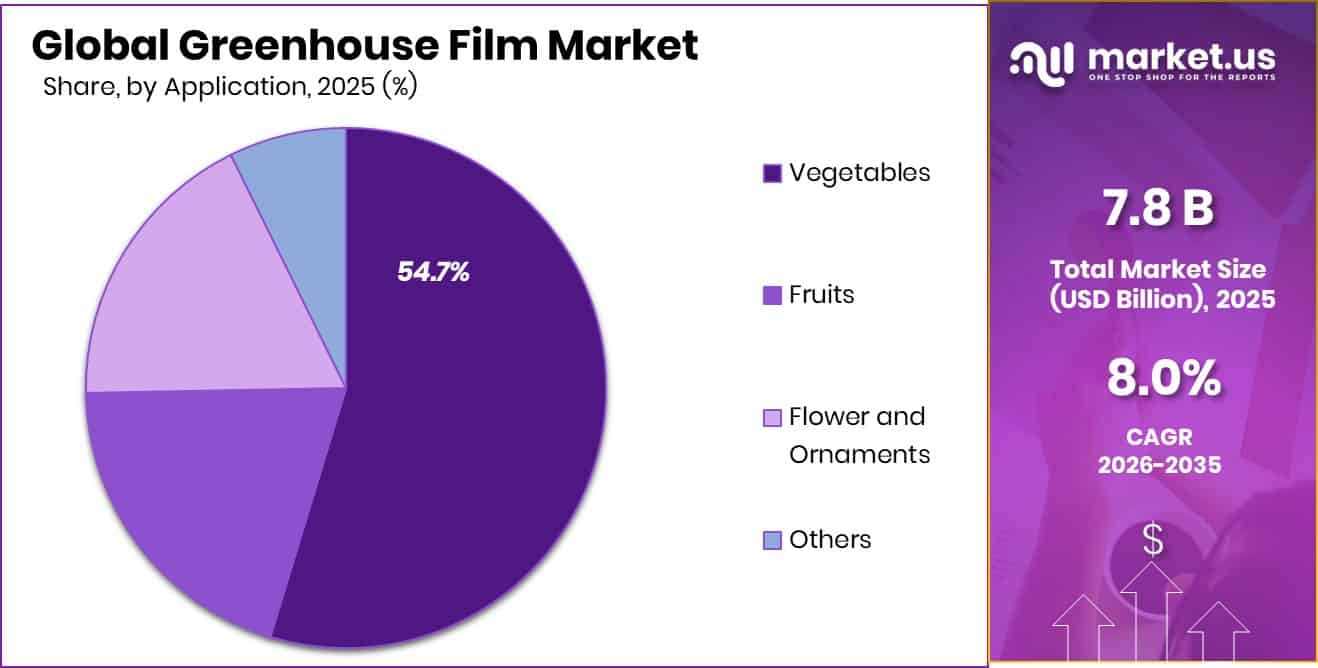

- Vegetables holding 54.7% share indicate the Greenhouse Film Market benefits from increasing protected cultivation needs.

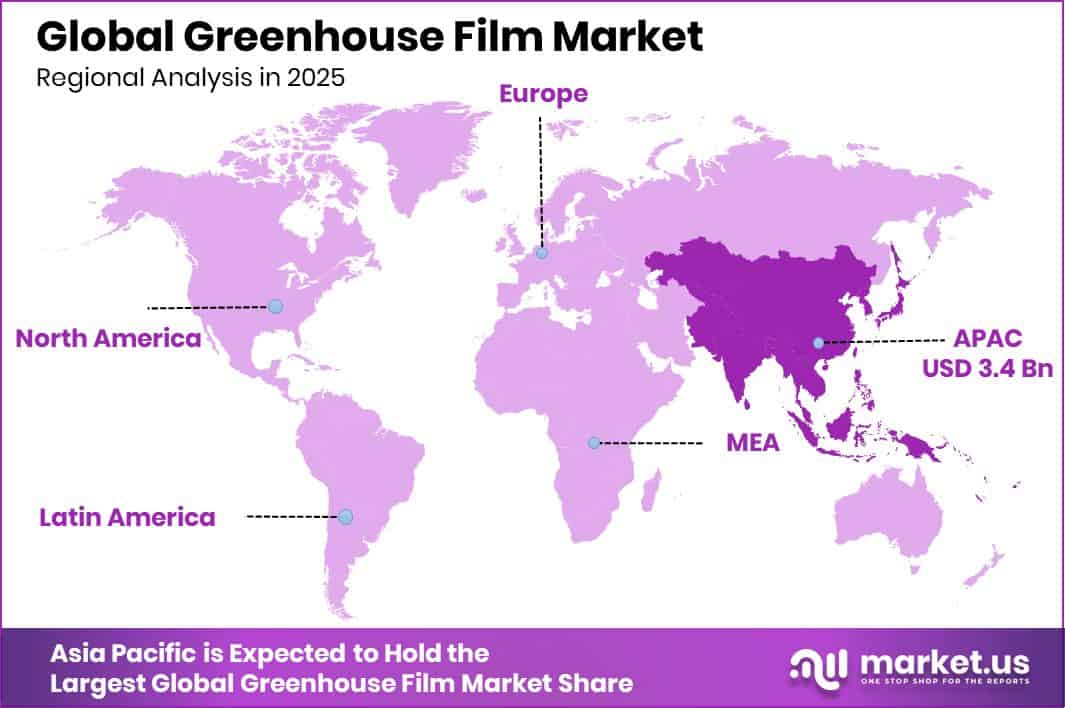

- The Asia Pacific market value stood at USD 3.4 Bn, driven by expanding protected cultivation.

By Resin Type Analysis

The greenhouse film market is dominated by the LDPE resin type, holding a 46.7% share.

In 2025, the Greenhouse Film Market is expected to see low-density polyethylene dominate with a 46.7% share, driven by its flexibility, durability, and ability to withstand temperature variations. LDPE continues to be the preferred resin type because growers rely on films that offer strong light transmission and resistance to tearing during long cultivation cycles. Its adaptability across multiple climatic zones keeps it ahead of alternative materials, especially in large-scale farming regions.

As sustainability pressures grow, LDPE films remain relevant due to improved recyclability and enhanced mechanical strength, supporting vegetable and floriculture producers who require consistent protection and predictable performance throughout the growing season.

By Width Analysis

The greenhouse film market is dominated by the 9-meter width segment, capturing 36.4% share.

In 2025, the Greenhouse Film Market will see the 9-meter width segment maintain dominance with a 36.4% share, as it fits the structural requirements of commercial greenhouse setups across Asia-Pacific, Europe, and emerging agricultural regions. This width allows farmers to cover larger spans without excessive joints, reducing heat loss and improving overall crop uniformity.

Its adoption is especially strong among vegetable growers who operate mid-size to large greenhouse structures. The balance between manageable installation and coverage efficiency keeps this width ahead of wider or narrower alternatives. As protected cultivation expands, the 9-meter format remains a cost-effective and operationally reliable choice for modern farming units.

By Thickness Analysis

The greenhouse film market is dominated by the 150-200 micron thickness segment with a 52.6% share.

In 2025, the Greenhouse Film Market continues to be dominated by the 150 to 200-micron thickness range, capturing a 52.6% share due to its superior durability and multi-season use potential. Farmers prefer this thickness because it provides strong UV resistance, better tensile strength, and stability under harsh weather conditions.

The long service life reduces replacement frequency, making it economically appealing for both small and large growers. This thickness range also supports additives such as anti-drip, anti-fog, and thermal stabilizers, which further improve plant growth. Its performance advantages make it the standard choice for greenhouse installations focused on maximizing yield and reducing operational risks.

By Application Analysis

The greenhouse film market is dominated by vegetable applications, securing a strong 54.7% share.

In 2025, the Greenhouse Film Market is led by the vegetables segment, accounting for 54.7%, as growers continue to expand protected farming to meet rising demand for fresh produce. Greenhouse films provide controlled temperature, humidity, and light conditions essential for crops like tomatoes, cucumbers, peppers, and leafy greens. The dominance of this segment reflects increasing adoption of year-round cultivation practices and the need to stabilize crop output despite seasonal fluctuations.

Vegetable producers rely heavily on high-quality films to protect against pests, rainfall, and excessive heat, allowing consistent productivity. This strong dependence ensures vegetables remain the largest and most influential application area in the market.

Key Market Segments

By Resin Type

- Low-density polyethylene (LDPE)

- Linear low-density polyethylene (LLDPE)

- Ethylene-vinyl acetate (EVA)

- Polyvinyl Chloride (PVC)

By Width

- 4.5

- 5.5

- 7

- 9

- Others (9 to 20 meters)

By Thickness

- 80 to 150 Micron

- 150 to 200 Micron

- More than 200 Micron

By Application

- Vegetables

- Fruits

- Flower and Ornaments

- Others

Driving Factors

Rising demand for protected crop cultivation

The Greenhouse Film Market continues to grow as farmers increasingly rely on protected crop cultivation to secure stable yields and shield crops from unpredictable weather. This rising shift toward controlled farming environments strengthens the need for reliable films that offer temperature management, UV protection, and improved plant growth conditions. Alongside this demand, governments are becoming more active in environmental responsibility.

A key example is the £60 million allocation to fight plastic waste, which encourages innovation in recyclable and longer-lasting film materials. Such initiatives support the transition toward sustainable greenhouse solutions while reinforcing market confidence, helping growers adopt modern farming structures with improved durability and lower environmental impact.

Restraining Factors

High installation costs limit adoption

Despite strong demand, high installation and maintenance costs continue to limit greenhouse film adoption, especially among small farmers who struggle with the upfront expenses of large greenhouse setups. Cost pressures are further influenced by ongoing challenges in plastic recycling and material sustainability.

Research aimed at solving these issues is gaining attention, illustrated by engineering professors securing $1 million to advance plastics recycling and sustainable design. While such research strengthens long-term prospects, the near-term financial burden still slows broader adoption. This combination of economic limitations and material-management challenges remains a key restraint in the market’s expansion.

Growth Opportunity

Increased adoption in emerging farming regions

Emerging farming regions are increasingly adopting greenhouse films to enhance productivity, manage limited land availability, and reduce vulnerability to climate variability. These areas present strong opportunities as growers seek cost-effective structures that improve the output of vegetables, fruits, and ornamental crops. Growth potential is further supported by expanding innovations tied to environmental sustainability.

A major boost comes from the U.S. Department of Energy’s $13.4 million investment aimed at reducing plastic waste and lowering emissions in the plastics industry. This funding encourages the development of improved resins, recyclable film designs, and advanced multilayer solutions, opening pathways for more efficient and climate-friendly greenhouse films across global markets.

Latest Trends

Shift toward UV-stabilized greenhouse materials

A leading trend in the Greenhouse Film Market is the shift toward UV-stabilized and performance-enhanced materials that increase film lifespan and improve light diffusion for better crop productivity. Farmers are also exploring advanced technologies that optimize sunlight and promote healthier plant development.

One notable example is UbiQD securing $20 million to scale quantum-dot technology designed to modify light spectra for agriculture, offering growers potential gains in growth rates and crop quality. Such innovations reflect a broader movement toward smarter greenhouse materials, where films do more than provide coverage—they actively support plant performance and energy efficiency.

Regional Analysis

Greenhouse Film Market Asia Pacific reached 44.8% share, showing strong dominance across regional agriculture production.

The Greenhouse Film Market shows varied regional performance, with each area contributing differently to the expansion of protected cultivation. Asia Pacific remains the dominant region, holding a 44.8% share valued at USD 3.4 Bn, driven by extensive vegetable production and increasing adoption of greenhouse structures across China, India, and Southeast Asia.

North America continues to expand steadily as growers focus on controlled-environment agriculture to support year-round output, while advancements in commercial greenhouse operations strengthen demand.

Europe maintains a mature market with widespread use of greenhouse films in countries with strong horticulture industries, supporting consistent regional consumption. In the Middle East & Africa, rising reliance on protected farming to overcome harsh climates boosts usage, particularly in vegetable and high-value crop segments.

Latin America shows gradual growth, supported by expanding greenhouse coverage in major agricultural economies seeking improved productivity. Across these regions, the market evolves as growers prioritize film durability, crop protection, and operational efficiency, with the Asia Pacific firmly leading overall adoption.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, the global Greenhouse Film Market reflects a competitive landscape shaped strongly by established material innovators such as Amcor plc. The company continues leveraging its deep expertise in film engineering, enabling growers to access durable, high-clarity materials suited for temperature-sensitive crops. Amcor’s focus on improving light transmission and extending film service life positions it as a trusted supplier for commercial greenhouse operators seeking reliability. Its long-standing manufacturing capabilities support consistent product quality across regions with increasing protected cultivation demand.

Avient Corporation strengthens its market presence through advanced polymer formulations that support greenhouse film stability, UV resistance, and performance under fluctuating climatic conditions. In 2025, the company’s emphasis on specialty additives allows film manufacturers to enhance thermal control, anti-fog behavior, and structural toughness. Avient’s solutions enable growers to optimize crop cycles, making it a critical technology partner for film producers who require tailored material enhancements for diverse agricultural environments.

GreenPro remains an important contributor, particularly in regions with rising greenhouse gas adoption. The company’s focus on providing cost-effective films with properties aligned to local cultivation needs helps expand usage among medium and small growers. In 2025, GreenPro’s emphasis on practical field performance, ease of installation, and reliable crop protection strengthens its relevance across emerging agricultural markets.

Top Key Players in the Market

- Amcor plc.

- Avient Corporation

- GreenPro

- POLIFILM

- Ginegar Plastic Products Ltd.

- Lumite Inc.

- Agriplast Tech India Private Limited

- Essen Multipack Limited

- Thai Charoen Thong Karntor Co. Ltd.

- Tuflex India

- PLASTIKA KRITIS

Recent Developments

- In March 2025, Amcor extended its Amcor Lift-Off challenge to seek advanced barrier coating solutions that enhance sustainability and functionality in packaging films, which could include antimicrobial or high-performance surface additives for film formulations. This R&D initiative invited innovators to develop barrier coatings that are either compostable or recyclable and improve packaging protection.

- In February 2025, Avient launched Cesa™ WithStand™ SX Low Haze Antimicrobial Additives, a new additive that protects clear plastics like polycarbonate and acrylic from bacteria, mold, and fungi while keeping them visually clear — even when recycled materials are used. This development helps plastic products stay cleaner longer and reduce staining or odor caused by microbes.

Report Scope

Report Features Description Market Value (2025) USD 7.8 Billion Forecast Revenue (2035) USD 16.9 Billion CAGR (2026-2035) 8.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Resin Type (Low-density polyethylene (LDPE), Linear low-density polyethylene (LLDPE), Ethylene-vinyl acetate (EVA), Polyvinyl Chloride (PVC)), By Width (4.5, 5.5, 7, 9, Others (9 to 20-meter)), By Thickness (80 to 150 Micron, 150 to 200 Micron, More than 200 Micron), By Application (Vegetables, Fruits, Flower and Ornaments, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Amcor plc., Avient Corporation, GreenPro, POLIFILM, Ginegar Plastic Products Ltd., Lumite Inc., Agriplast Tech India Private Limited, Essen Multipack Limited, Thai Charoen Thong Karntor Co. Ltd., Tuflex India, PLASTIKA KRITIS Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Greenhouse Film MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Greenhouse Film MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Amcor plc.

- Avient Corporation

- GreenPro

- POLIFILM

- Ginegar Plastic Products Ltd.

- Lumite Inc.

- Agriplast Tech India Private Limited

- Essen Multipack Limited

- Thai Charoen Thong Karntor Co. Ltd.

- Tuflex India

- PLASTIKA KRITIS

Our Clients

- 179264

- February 2026