Global Frozen Bread Market Size, Share Analysis Report By Type (Wheat Bread, Rye Bread, Multigrain Bread, and Others), By Product Type (Leavened Bread and Unleavened Bread), By End-Use (Household and Foodservice), By Distribution Channel (B2B and B2C), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2034

- Published date: Mar 2026

- Report ID: 180948

- Number of Pages: 231

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

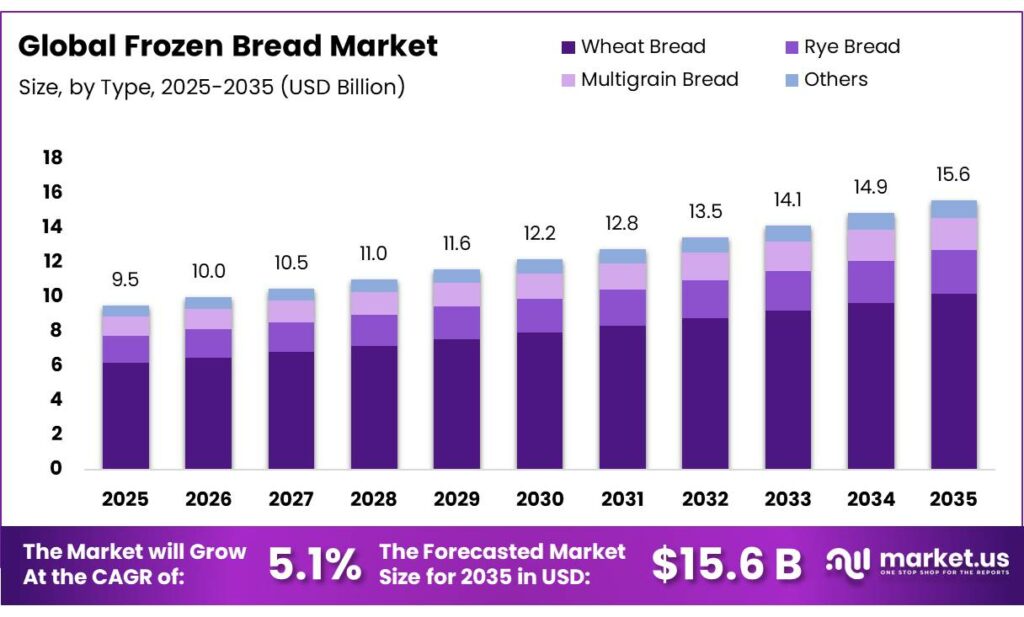

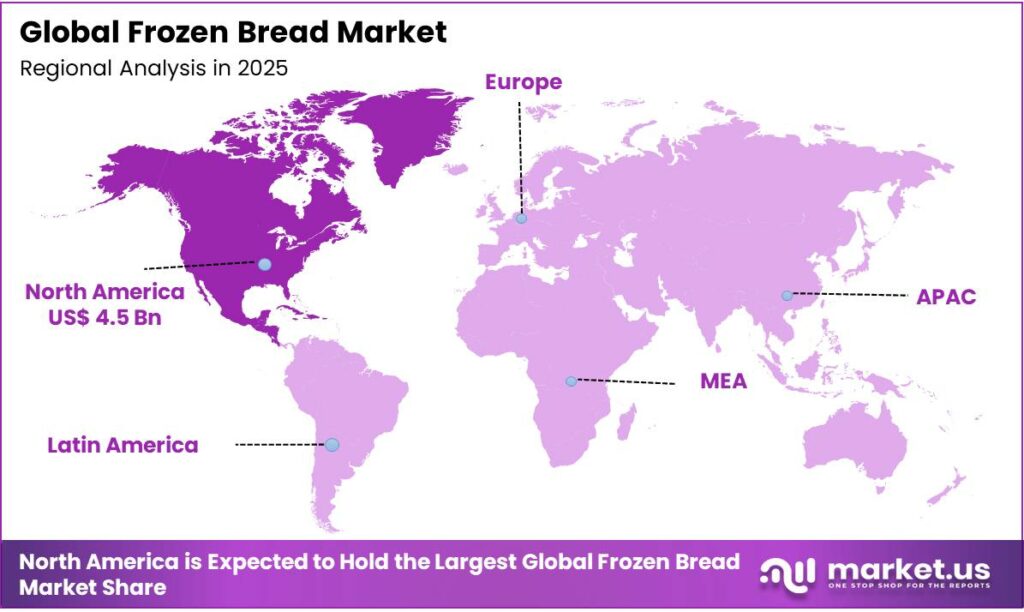

The Global Frozen Bread Market size is expected to be worth around USD 15.6 Billion by 2035, from USD 9.5 Billion in 2025, growing at a CAGR of 5.1% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 34.8% share, holding USD 2.3 Billion revenue.

Frozen bread refers to bread that has been frozen to preserve its freshness, extend its shelf life, or achieve specific health benefits. The frozen bread market operates at the intersection of industrial bakery manufacturing, cold-chain logistics, and foodservice procurement systems. Demand is structurally supported by time-constrained consumption patterns, particularly in urban markets where standardized, ready-to-bake or thaw-and-serve formats enhance operational efficiency. Leavened, wheat-based products dominate due to superior gluten functionality, freeze–thaw stability, and broader sensory acceptance relative to rye or multigrain alternatives.

Commercial channels represent the primary distribution pathway. Foodservice operators—including quick-service restaurants, hotels, and institutional caterers—leverage frozen bread for portion control, inventory flexibility, and labor optimization. B2B procurement models further support bulk distribution and cold-chain consolidation.

However, the sector faces structural constraints, including high energy intensity in frozen storage, cold-chain infrastructure gaps in emerging markets, and input volatility linked to geopolitical disruptions in global wheat trade and energy markets.

Emerging trends include organic and gluten-free formulations, clean-label positioning, and supply-chain localization strategies to enhance resilience and competitive differentiation within temperature-controlled bakery systems.

- According to data from the U.S. Census and the Simmons National Consumer Survey (NHCS), an estimated 326.91 million individuals in the United States consumed bread in 2020. This figure increased to approximately 335.49 million consumers by 2024, indicating a rise in bread usage over the period.

Key Takeaways:

- The global frozen bread market was valued at US$9.5 billion in 2024.

- The global frozen bread market is projected to grow at a CAGR of 5.1% and is estimated to reach US$15.6 billion by 2034.

- On the basis of types of breads, frozen wheat breads dominated the market, constituting 65.1% of the total market share.

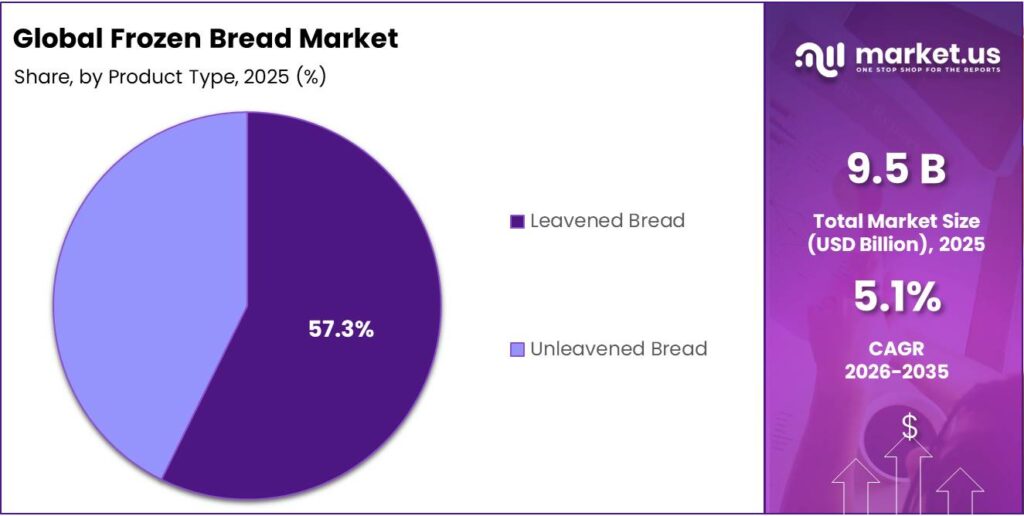

- Based on the product types, leavened bread dominated the frozen bread market, with a substantial market share of around 57.3%.

- Based on the end-users, the food service sector led the frozen bread market, comprising 65.5% of the total market.

- Among the distribution channels, B2B sales held a major share in the frozen bread market, 60.7% of the market share.

- In 2024, North America was the most dominant region in the frozen bread market, accounting for 46.9% of the total global consumption.

Type Analysis

Wheat Breads are a Prominent Segment in the Frozen Bread Market.

The frozen bread market is segmented based on types of bakery products into wheat bread, rye bread, multigrain bread, and others. The wheat breads led the frozen bread market, comprising 65.1% of the market share, primarily due to functional, sensory, and supply-chain advantages. The wheat flour contains higher levels of gluten-forming proteins, which create a strong viscoelastic dough network. This structure tolerates mechanical processing, freezing, thawing, and reheating with minimal loss of volume and crumb softness.

On the contrary, rye flour has lower gluten strength and higher pentosan content, resulting in a denser texture and greater susceptibility to structural collapse during freeze-thaw cycles. Additionally, wheat bread offers a neutral flavor profile, lighter crumb, and softer texture, making it suitable for sandwiches, burgers, and food-service applications.

Similarly, wheat has more standardized global cultivation, milling infrastructure, and quality grading systems, enabling consistent raw-material specifications. Furthermore, multigrain formulations introduce variability in hydration, shelf stability, and processing parameters, increasing formulation complexity and production costs relative to conventional wheat frozen bread.

Product Type Analysis

Leavened Bread Dominated the Frozen Bread Market.

On the basis of the product type, the frozen bread market is segmented into leavened bread and unleavened bread. The leavened bread dominated the frozen bread market, comprising 57.3% of the market share, due to structural functionality, sensory preference, and broader application versatility. Leavened dough undergoes yeast or biological fermentation, generating carbon dioxide that forms an aerated gluten network. This cellular structure improves loaf volume, crumb softness, and elasticity. In frozen formats, particularly par-baked or ready-to-bake products, the developed gluten matrix withstands freezing and reheating while retaining texture and palatability.

In contrast, unleavened breads lack this internal gas structure, resulting in denser, flatter products with limited textural recovery after freezing. Furthermore, leavened bread aligns with mainstream eating patterns, including sandwich, burger, and toast applications in retail and food service channels. Its neutral flavor and soft crumb support diverse fillings and menu formats. Similarly, leavened frozen bread integrates efficiently into automated production lines and standardized baking cycles, making it more adaptable for large-scale manufacturing and distribution than niche unleavened alternatives.

End-User Analysis

Frozen Bread Products Are Mostly Utilized in the Food Service Sector.

Based on the end-uses, the frozen bread market is divided into residential and foodservice. The food service sector dominated the frozen bread market, with a notable market share of 65.5%, due to operational efficiency, demand predictability, and product standardization requirements. Foodservice operators, such as quick-service restaurants, institutional caterers, and hotels, prioritize portion control, consistency, and reduced preparation time.

Frozen bread enables bake-off or thaw-and-serve formats, minimizing on-site labor while ensuring uniform size, crumb structure, and sensory quality across outlets. Similarly, the frozen format reduces daily fresh-bread waste, as inventory can be thawed based on demand cycles. In contrast, residential consumers often prefer freshly baked or ambient bread due to higher household access to nearby retail bakeries and limited freezer space allocated to staple bread products. Household consumption volumes are typically smaller and less standardized than foodservice requirements. The bulk frozen distribution aligns better with centralized procurement systems in foodservice chains, making frozen bread operationally more advantageous in commercial environments than in individual households.

Distribution Channel Analysis

B2B Sales Held a Major Share of the Frozen Bread Market.

Among the distribution channels, 60.7% of the total global consumption of frozen bread products is sold through B2B sales, as their value proposition aligns more strongly with institutional procurement than with household retail demand. Commercial buyers, such as quick-service restaurants, hotels, caterers, and institutional kitchens, require high-volume, standardized, and batch-consistent products. By contrast, B2C retail channels face slower turnover rates and freezer space constraints.

Ambient packaged bread competes directly in supermarkets with high visibility and lower storage complexity. Frozen bread in retail requires dedicated freezer infrastructure, higher energy use, and consumer willingness to allocate freezer capacity to staple items that are widely available fresh. Additionally, B2B distribution benefits from palletized bulk logistics and fewer handling points, improving cold-chain integrity compared with fragmented retail distribution networks serving individual consumers.

Key Market Segments:

By Type

- Wheat Bread

- Rye Bread

- Multigrain Bread

- Others

By Product Type

- Leavened Bread

- Unleavened Bread

By End-User

- Residential

- Foodservice

By Distribution Channel

- B2B

- B2C

- Supermarkets and Hypermarkets

- Convenience Store

- Specialty Stores

- Online

- Others

Drivers

Busy Lifestyles of Consumers and Demand for Convenience Drive the Frozen Bread Market.

The demand for frozen bread is increasingly driven by the convergence of consumer time-poverty and a structural shift toward convenience-oriented food systems. According to the U.S. Department of Agriculture (USDA) Economic Research Service, the trend of food away from home and the rising value of time have fundamentally altered household procurement patterns.

- According to the U.S. Bureau of Labor Statistics’ American Time Use Survey, only 57.2% of Americans aged 15 and over spent any time on food and drink preparation on an average day, with those who did spend about 53 minutes daily on such activities, underscoring the limited time available for traditional cooking routines.

Additionally, bread is one of the most wasted food categories, and freezing extends shelf life from days to months, aligning with consumer efforts to reduce grocery frequency and household waste. The ready-to-bake and re-heatable frozen bakery products appeal to busy households and working professionals who require quick meal components with an extended shelf life. Such convenience attributes directly map to objective measures of constrained meal-preparation time, positioning frozen bread as a practical response to busy lifestyles.

Restraints

High Operational Costs and Cold Chain Logistics Infrastructure Gaps Might Pose a Challenge to the Frozen Bread Market.

The frozen bread market faces significant operational challenges stemming from the inherent complexities of temperature-controlled supply chains and localized infrastructure deficits. High operational costs and gaps in cold chain logistics infrastructure present constraints to the frozen bread segment of the broader frozen food supply chain. Maintaining temperature-controlled storage and transport systems is energy-intensive. Cold storage facilities are among the most energy-intensive industrial buildings.

- According to the U.S. International Trade Administration, electricity costs typically account for 18% of a facility’s total operating expenses, with the global industry spending over US$30 billion annually on energy.

In addition, transporting frozen goods is structurally more expensive than ambient delivery, as it includes higher capital costs for refrigerated trailers and increased maintenance. Moreover, cold-chain services are concentrated regionally, leaving large areas underserved, which increases transit distances and the risk of temperature excursions. These factors underline systemic operational cost pressures and infrastructure gaps that constrain reliable frozen bread distribution within temperature-sensitive supply networks.

Opportunities

Growth in Food Service & QSRs Creates Opportunities in Frozen Bread

Expansion in food service, particularly quick-service restaurants (QSRs) and limited-service outlets, creates structural demand for frozen bakery inputs such as frozen bread products used in sandwiches, toasts, and ready-to-serve items. The growth of Quick Service Restaurants (QSRs) and broader food service channels represents a structural opportunity for the frozen bread market, driven by the need for operational efficiency and consistent product quality.

In the United States, food service, defined as food away from home, accounted for around 58.9% of total food expenditures in 2024, with limited-service establishments (which include QSRs) supplying about 36.3% of that share, indicating the scale of meal occasions where standardized, frozen bread can be operationally advantageous. To manage this volume, QSRs utilize frozen, par-baked, or “ready-to-bake” products to ensure uniform texture and taste across thousands of locations without requiring skilled on-site bakers. Similarly, this technology reduces on-site preparation time and specialized labor requirements, allowing lean staff models in high-traffic urban centers.

Trends

Demand for Organic and Gluten-Free Frozen Bread.

The demand for organic and gluten-free frozen bread is driven by a structural shift in consumer health priorities, specifically the convergence of free-from dietary requirements and the functional benefits of cryopreservation. Several consumers actively seek products without artificial preservatives or additives. Freezing serves as a natural preservation method, allowing organic brands to maintain “clean label” status with shelf lives extending up to 15 months without synthetic stabilizers.

- According to USDA, National Agricultural Statistics Service (NASS) surveys (2011 and 2021), certified organic cropland acres increased by 79%, to 3.6 million acres, pastureland/rangeland decreased by 22%, to 1.3 million acres, and certified operations increased by more than 90 percent (to 17,445 farms) over the 2011–21 period.

Furthermore, U.S. federal gluten-free labeling rules, such as the FDA’s voluntary standard of less than 20 ppm gluten for a gluten-free claim, create regulatory transparency that supports consumer confidence and choice for gluten-free baked goods, including frozen formats. A household survey indicates that consumers with wheat/gluten avoidance are more likely to purchase both organic and gluten-free breads and consider combined label attributes of organic and gluten-free desirable, with substantial shares of respondents willing to pay premiums for these labels.

Geopolitical Impact Analysis

Increased Crop Prices Affecting Frozen Bread Market Amid Geopolitical Tensions.

The ongoing geopolitical tensions, particularly the Russo-Ukrainian conflict, have demonstrable effects on global agricultural supply chains that extend to inputs for the frozen bread segment. Ukraine historically ranked among the top global exporters of wheat and other grains, accounting for about 9% of global wheat trade annually, with additional shares in maize and barley export markets. War-related disruptions curtailed export volumes and constrained logistics, including port closures and damaged infrastructure, reducing Ukraine’s ability to move staple cereals to international markets. This has implications for the upstream supply of wheat and flour used in frozen bread production and processing. Furthermore, the maritime tensions impacting the Strait of Hormuz have forced rerouting of container traffic and extended shipping times, raising freight costs and logistical complexity for temperature-controlled transport of frozen goods. These factors illustrate how geopolitical instability alters availability and cost structures for agricultural inputs and cold-chain logistics, with cascading effects on the frozen bread market’s supply continuity and operational resilience.

Regional Analysis

North America Held the Largest Share of the Global Frozen Bread Market.

In 2024, North America dominated the global frozen bread market, holding about 46.9% of the total global consumption, underpinned by high freezer penetration and established retail networks in the United States and Canada. The region serves as the primary global market for frozen bread, supported by a highly established consumer reliance on convenience-oriented food formats. In addition, this format aligns with the American Frozen Food Institute (AFFI) finding that 30% of U.S. shoppers expanded their home freezer capacity post-2020 to accommodate bulk purchases.

Furthermore, U.S. Census Bureau data indicate that over 99% of households own a refrigerator, supporting widespread adoption of frozen foods, including frozen bread formats at home. In addition, the strong retail distribution channels with supermarkets and convenience stores deeply integrating temperature-controlled frozen sections, which facilitate consumer access to frozen bread products across North American markets.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of frozen bread focus on integrated strategic levers across product, operations, and distribution to strengthen competitive positioning. The companies expand portfolios into organic, whole-grain, high-fiber, and gluten-free variants, alongside ready-to-bake and par-baked formats tailored for retail and food service channels.

In addition, producers invest in automation, energy-efficient freezing systems (IQF and blast freezing), and optimized cold-chain logistics to reduce unit costs and ensure product consistency. Channel expansion strategies include partnerships with quick-service restaurants, private-label manufacturing for large retailers, and strengthening freezer aisle presence through category management initiatives.

Additionally, firms pursue geographic expansion, co-manufacturing agreements, and supply-chain localization to mitigate input volatility and improve service reliability, enhancing market penetration and share retention.

The major players in the industry

- Europastry S.A.

- Vandemoortele NV

- Grupo Bimbo

- Lantmännen Unibake

- Flower Foods Inc.

- The Campbell’s Company

- Bridgford Foods Corporation

- Sunbulah Group

- Dawn Food Products Inc.

- Gonnella Baking Co.

- Custom Foods Inc.

- Cole’s Quality Foods, Inc.

- Panamar Bakery Group

- Gonnella Baking Company

- Monbake

- Other Key Players

Key Development:

- In May 2025, Vandemoortele, a well-established family-owned food company with a presence across Europe, and VIVESCIA Group, a prominent French grain cooperative, revealed that they reached an agreement for Vandemoortele to acquire Délifrance.

- In July 2025, Europastry, the Spanish baking powerhouse with a significant subsidiary in Milan, Italy, acquired Thailand’s Art of Baking, expanding in Southeast Asia. The acquisition, made from Minor International Public Co. and Srifa Frozen Food, is part of a strategic partnership, with both remaining entities holding a 20% share in Art of Baking.

Report Scope

Report Features Description Market Value (2024) US$9.5 Bn Forecast Revenue (2034) US$15.6 Bn CAGR (2025-2034) 5.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Wheat Bread, Rye Bread, Multigrain Bread, and Others), By Product Type (Leavened Bread and Unleavened Bread), By End-Use (Household and Foodservice), By Distribution Channel (B2B and B2C) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Europastry S.A., Vandemoortele NV, Grupo Bimbo, Lantmännen Unibake, Flower Foods Inc., The Campbell’s Company, Bridgford Foods Corporation, Sunbulah Group, Dawn Food Products Inc., Gonnella Baking Co., Custom Foods Inc., Cole’s Quality Foods, Inc., Panamar Bakery Group, Gonnella Baking Company, Monbake, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Europastry S.A.

- Vandemoortele NV

- Grupo Bimbo

- Lantmännen Unibake

- Flower Foods Inc.

- The Campbell's Company

- Bridgford Foods Corporation

- Sunbulah Group

- Dawn Food Products Inc.

- Gonnella Baking Co.

- Custom Foods Inc.

- Cole’s Quality Foods, Inc.

- Panamar Bakery Group

- Gonnella Baking Company

- Monbake

- Other Key Players

Our Clients

- 180948

- Mar 2026