Global Foot and Ankle Devices Market By Product Type (Orthopedic Implants and Devices, Prostheses, Bracing and Support Devices and Others), By Application (Trauma and Hairline Fractures, Rheumatoid Arthritis and Osteoarthritis, Diabetic Foot Diseases, Ligament Injuries, Hammertoe, Neurological Disorders and Others), By End User (Hospitals, Ambulatory Surgical Centers (ASCs), Orthopedic Clinics and Rehabilitation Centers), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183550

- Number of Pages: 313

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

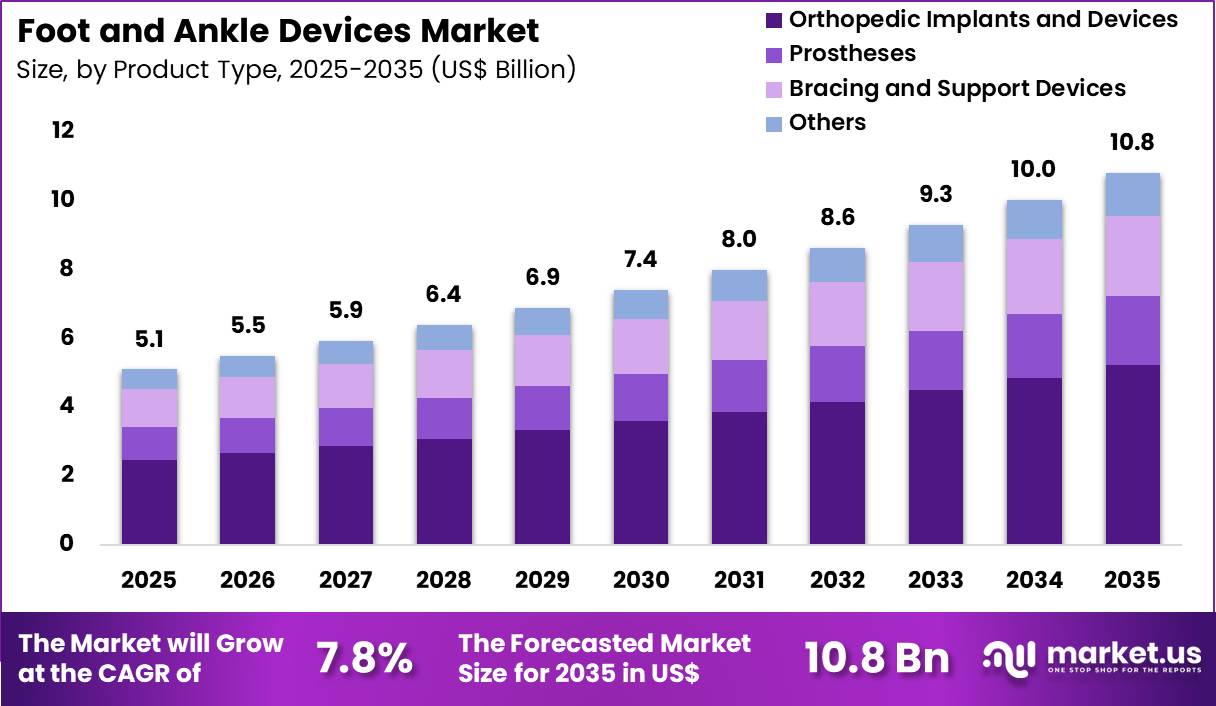

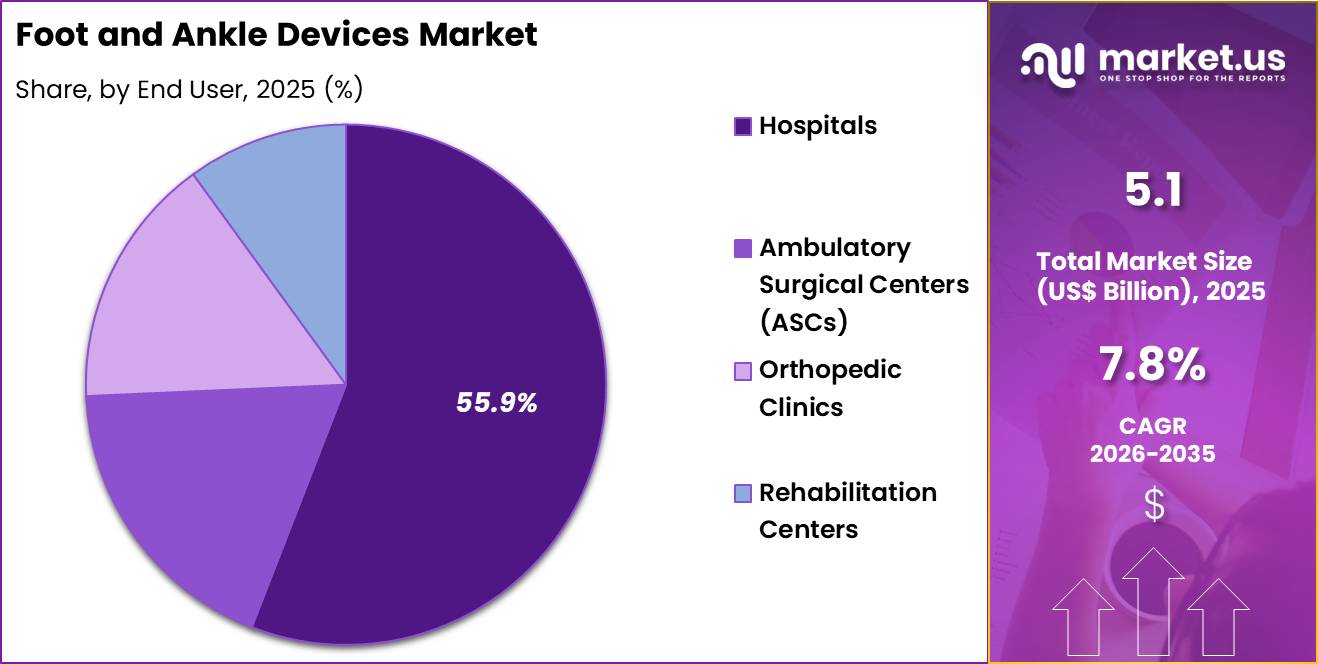

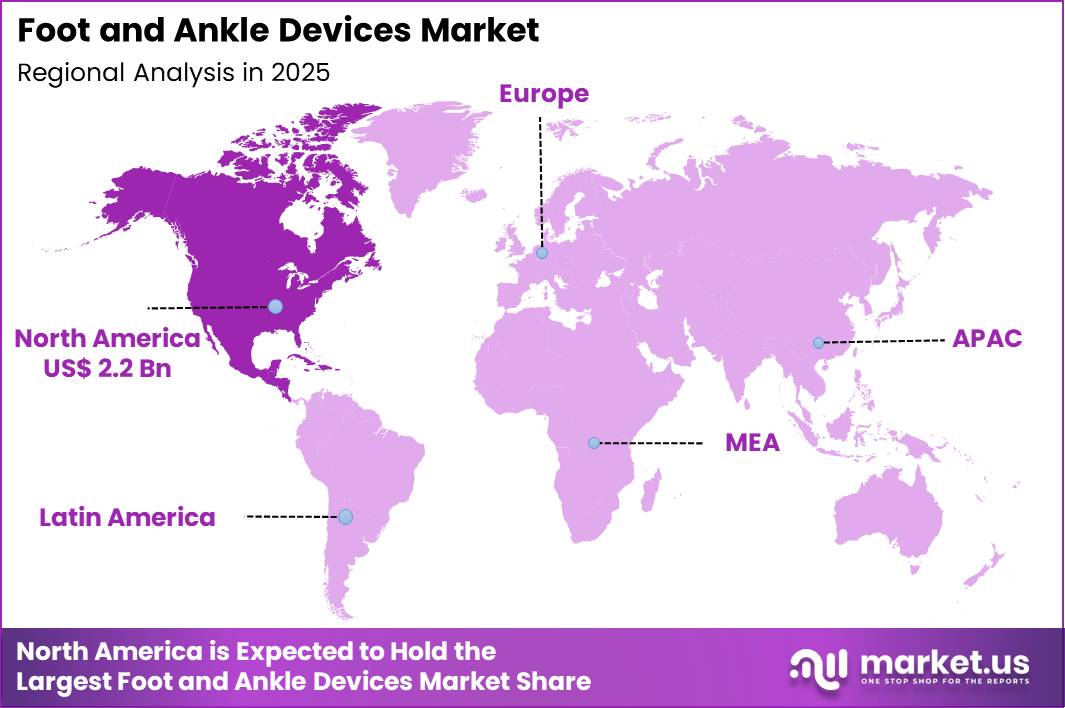

The Global Foot and Ankle Devices Market size is expected to be worth around US$ 10.8 Billion by 2035 from US$ 5.1 Billion in 2025, growing at a CAGR of 7.8% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 43.6% share with a revenue of US$ 2.2 Billion.

Increasing incidence of foot and ankle injuries from sports, trauma, and age-related degeneration propels the Foot and Ankle Devices market as orthopedic surgeons seek advanced implants and instrumentation that restore mobility, stability, and function with improved long-term outcomes.

Surgeons increasingly utilize ankle fracture fixation systems, including locking plates and intramedullary nails, to achieve anatomic reduction and early weight-bearing in complex malleolar and pilon fractures. These devices support total ankle replacement procedures in patients with end-stage ankle arthritis, replacing damaged joint surfaces with prosthetic components that preserve motion and reduce pain compared to traditional fusion techniques.

Foot and ankle surgeons apply midfoot and hindfoot fusion plates and screws to correct deformities such as flatfoot or Charcot arthropathy, stabilizing the arch and preventing further collapse in diabetic patients. Sports medicine specialists employ ligament repair and reconstruction devices, including suture anchors and internal bracing systems, to treat lateral ankle instability and Achilles tendon ruptures, enabling faster return to athletic activity.

In February 2026, Stryker introduced the Synchfix EVT system, a device designed for syndesmotic fixation in ankle injuries. Showcased at the American College of Foot and Ankle Surgeons meeting, the system aims to enhance joint stability while simplifying procedural steps for surgeons managing complex fractures.

Manufacturers pursue opportunities to develop patient-specific implants and instrumentation through 3D printing, expanding applications in revision surgery and complex deformity correction where standard devices provide suboptimal fit.

Developers advance minimally invasive techniques and bioresorbable implants that reduce hardware prominence and the need for secondary removal procedures, broadening utility in active patient populations. These innovations facilitate integration with navigation and robotic systems, improving accuracy in hindfoot arthrodesis and ankle arthroplasty.

Opportunities emerge in biologic augmentation of fixation devices, combining screws and plates with growth factors or stem cells to enhance bone healing in high-risk patients. Companies invest in modular systems that allow intraoperative customization for diverse fracture patterns and soft tissue conditions.

In February 2026, reports indicated that Johnson & Johnson is evaluating strategic options for its DePuy Synthes orthopedics division, including a potential sale rather than a spin-off. The business represents a significant portion of the company’s medical technology portfolio and has attracted interest from private equity investors due to its strong revenue base.

Recent trends emphasize motion-preserving solutions, minimally invasive approaches, and smart implants, positioning the market for growth in personalized, high-performance foot and ankle reconstruction focused on faster recovery and sustained joint function.

Key Takeaways

- In 2025, the market generated a revenue of US$ 5.1 Billion, with a CAGR of 7.8%, and is expected to reach US$ 10.8 Billion by the year 2035.

- The product type segment is divided into orthopedic implants and devices, prostheses, bracing and support devices and others, with orthopedic implants and devices taking the lead with a market share of 48.3%.

- Considering application, the market is divided into trauma and hairline fractures, rheumatoid arthritis and osteoarthritis, diabetic foot diseases, ligament injuries, hammertoe, neurological disorders and others. Among these, trauma and hairline fractures held a significant share of 40.2%.

- Furthermore, concerning the end user segment, the market is segregated into hospitals, ambulatory surgical centers (ASCs), orthopedic clinics and rehabilitation centers. The hospitals sector stands out as the dominant player, holding the largest revenue share of 55.9% in the market.

- North America led the market by securing a market share of 43.6%.

Product Type Analysis

Orthopedic implants and devices accounted for 48.3% of growth within product type and dominate the foot and ankle devices market due to their essential role in surgical fixation, reconstruction, and stabilization of complex injuries. Surgeons use plates, screws, and fixation systems to restore bone alignment and ensure proper healing after fractures or deformities.

Trauma cases involving the foot and ankle continue to rise globally due to road accidents, sports injuries, and aging populations, which strengthens demand for implant-based solutions. Orthopedic implants are expected to expand further as surgical techniques advance and minimally invasive procedures gain adoption.

Healthcare systems report a growing number of orthopedic procedures each year, which supports consistent utilization of these devices. The segment is likely to benefit from improved biomaterials and implant designs that enhance durability and patient outcomes.

Increasing incidence of degenerative bone conditions is projected to drive additional surgical interventions. As clinicians prioritize long-term stability and effective recovery, orthopedic implants and devices are estimated to remain the dominant product segment in this market.

Application Analysis

Trauma and hairline fractures accounted for 40.2% of growth within application and dominate the foot and ankle devices market due to the high frequency of injuries affecting these regions. Foot and ankle fractures are common in both active populations and elderly individuals, which creates continuous demand for treatment solutions.

Healthcare data indicates that fractures represent a significant portion of orthopedic injuries, especially in emergency care settings. This segment is expected to grow as urbanization and physical activity levels increase, leading to higher injury rates.

Trauma-related cases often require immediate intervention, which drives demand for fixation devices and support systems. The segment is likely to benefit from rising awareness of early diagnosis and treatment to prevent complications.

Increasing participation in sports and outdoor activities is projected to further support growth. As trauma cases continue to represent a major share of orthopedic conditions, this application segment is anticipated to maintain its leading position in the market.

End-User Analysis

Hospitals accounted for 55.9% of growth within end user and dominate the foot and ankle devices market due to their capability to handle complex surgical procedures and emergency trauma cases. Hospitals provide advanced infrastructure, skilled orthopedic surgeons, and post-operative care, which makes them the preferred setting for foot and ankle surgeries.

High patient inflow for trauma, fractures, and reconstructive procedures strengthens demand for devices in hospital settings. Hospitals are expected to remain dominant as they manage both acute and chronic orthopedic conditions requiring surgical intervention. The segment benefits from increasing healthcare investments and expansion of surgical facilities.

Hospitals also adopt advanced technologies and standardized treatment protocols, which improves patient outcomes. Rising incidence of orthopedic disorders is projected to support continued demand. As healthcare systems focus on delivering comprehensive surgical care, hospitals are estimated to retain their leading position in the foot and ankle devices market.

Key Market Segments

By Product Type

- Orthopedic Implants and Devices

- Prostheses

- Bracing and Support Devices

- Others

By Application

- Trauma and Hairline Fractures

- Rheumatoid Arthritis and Osteoarthritis

- Diabetic Foot Diseases

- Ligament Injuries

- Hammertoe

- Neurological Disorders

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Orthopedic Clinics

- Rehabilitation Centers

Drivers

Increasing prevalence of orthopedic conditions and sports injuries is driving the Foot and Ankle Devices market.

The rising incidence of foot and ankle disorders, including fractures, osteoarthritis, and deformities, has substantially elevated demand for specialized fixation, reconstruction, and replacement devices. An aging population contributes to higher rates of degenerative joint diseases and osteoporosis-related complications requiring surgical intervention.

Sports participation and recreational activities generate a consistent volume of acute ligament injuries, sprains, and fractures that necessitate prompt device-based treatment. In the United States, over 250,000 ankle fixation surgeries were recorded in 2024, illustrating the procedural burden on healthcare systems.

The global orthopedic fixation segment maintained dominance in 2022 owing to the high number of ankle fractures requiring operative management. Diabetic foot complications and Charcot arthropathy further amplify the need for advanced reconstruction solutions in affected populations.

Healthcare facilities increasingly prioritize durable, anatomically contoured implants to restore mobility and function effectively. Public health awareness campaigns promote early intervention, thereby increasing procedure volumes across trauma and elective categories.

These epidemiological and demographic patterns sustain steady utilization of foot and ankle devices in both hospital and ambulatory settings. Consequently, this clinical demand serves as a primary driver supporting market expansion during the 2022–2025 period.

Restraints

High costs of advanced implants and procedures are restraining the Foot and Ankle Devices market.

Sophisticated patient-specific and 3D-printed implants command premium pricing, which limits accessibility in cost-sensitive healthcare environments and public payer systems. Total ankle replacement and complex reconstruction procedures involve substantial resource utilization, including specialized instrumentation and extended operating times.

Reimbursement variations across regions create uncertainty for providers and may delay adoption of newer technologies. Smaller facilities encounter challenges in justifying capital investments for advanced systems amid broader budgetary constraints. Training requirements for minimally invasive and navigation-assisted techniques add to implementation expenses for surgical teams.

These economic factors contribute to selective utilization, favoring conventional devices in routine cases. Persistent gaps in coverage for innovative solutions slow the replacement cycle for existing inventory. Resource-limited settings particularly defer upgrades despite clinical advantages.

Such financial pressures moderate overall penetration rates of high-value foot and ankle technologies. As a result, cost-related barriers impose measurable restraint on accelerated market growth throughout the 2022–2025 timeframe.

Opportunities

Development of patient-specific and 3D-printed implants is creating growth opportunities in the Foot and Ankle Devices market.

Customization through additive manufacturing enables precise anatomical matching for complex deformities, revisions, and Charcot reconstructions, improving surgical outcomes and implant longevity. Opportunities arise for integration with preoperative planning software that enhances alignment accuracy and reduces intraoperative adjustments.

These solutions support minimally invasive approaches, facilitating shorter recovery periods and outpatient procedures in ambulatory settings. Partnerships between device manufacturers and imaging specialists accelerate validation and regulatory clearance of tailored products. Potential exists for expanded applications in trauma, osteoarthritis, and sports medicine where standard implants may prove suboptimal.

Scalable production methods lower long-term costs while maintaining high precision standards. Alignment with value-based care models rewards demonstrated improvements in patient mobility and reduced revision rates. Expansion into emerging markets benefits from adaptable, cost-effective customization platforms. These technological advancements generate substantial prospects for differentiation and broader clinical adoption across diverse patient profiles.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical dynamics are shaping demand patterns, pricing, and supply continuity in the foot and ankle devices market. Rising incidence of diabetes, sports injuries, and aging populations are supporting procedure volumes, while inflation is increasing the cost of implants, surgical tools, and rehabilitation devices, which can affect affordability in some regions.

Hospitals are prioritizing essential orthopedic procedures, yet budget constraints may delay elective surgeries in cost-sensitive settings. Geopolitical tensions disrupt supply chains for metals, polymers, and precision components used in device manufacturing, leading to procurement delays and cost variability.

Current US tariffs on imported medical devices and raw materials increase production and acquisition costs for manufacturers and healthcare providers, which can influence pricing strategies and margins. These pressures may slow adoption in certain markets, particularly where reimbursement remains limited.

At the same time, tariffs are encouraging domestic production and supplier diversification, strengthening long-term supply resilience. Overall, despite short-term cost and supply challenges, rising clinical need and ongoing innovation in orthopedic care are expected to support sustained market growth.

Latest Trends

Adoption of 3D printing and patient-specific implants represents a recent trend in the Foot and Ankle Devices market.

In 2024 and 2025, the industry has witnessed accelerated integration of additive manufacturing for the production of customized foot and ankle implants tailored to individual patient anatomy. This development addresses challenges in complex deformity corrections, post-traumatic reconstructions, and total ankle arthroplasty through precise fit and optimized load distribution.

Surgeons increasingly utilize 3D-printed titanium cages and patient-specific instrumentation to enhance procedural efficiency and functional restoration. The trend aligns with a broader shift toward minimally invasive techniques that minimize soft tissue disruption and accelerate rehabilitation.

Implementations in 2025 demonstrate notable improvements in mobility for patients with Charcot arthropathy and end-stage arthritis. Industry observations highlight growing collaboration between orthopedic companies and 3D technology providers to streamline design-to-implantation workflows.

This evolution prioritizes personalized solutions over off-the-shelf devices, particularly in revision and high-complexity cases. Prominent in 2024–2025, the incorporation of 3D printing continues to redefine standards for precision and patient-centered care in foot and ankle surgery.

Regional Analysis

North America is leading the Foot and Ankle Devices Market

North America accounted for 43.6% of the foot and ankle devices market in 2025 as orthopedic care providers expanded advanced treatment approaches for trauma cases, chronic joint disorders, and sports-related injuries. The region benefits from a strong clinical ecosystem where specialized surgeons, outpatient orthopedic centers, and rehabilitation facilities work in coordination to manage complex lower extremity conditions.

Data from the American Orthopaedic Foot & Ankle Society indicates that ankle sprains remain among the most frequently reported musculoskeletal injuries, contributing to sustained clinical demand for fixation systems, implants, and supportive devices. Increasing involvement in recreational sports and fitness activities has elevated injury incidence, particularly among younger populations.

Surgeons are favoring anatomically designed implants and minimally invasive fixation techniques that improve alignment and accelerate recovery timelines. Hospitals are also incorporating advanced imaging and intraoperative guidance tools to enhance surgical accuracy.

Device manufacturers are focusing on lightweight materials and improved biomechanics to support long-term patient mobility. Expansion of ambulatory surgical centers has further increased procedure volumes for foot and ankle interventions. These combined factors have driven consistent adoption of orthopedic solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness strong momentum over the forecast period as rising injury rates and expanding healthcare access increase demand for orthopedic treatment solutions. Rapid urban growth and changing lifestyles in countries such as China, India, and Southeast Asia are contributing to higher rates of fractures, ligament injuries, and diabetes-related foot complications.

The World Health Organization recognizes musculoskeletal disorders as a leading cause of disability worldwide, reinforcing the need for improved orthopedic care infrastructure across developing regions. Hospitals are scaling up trauma care units and orthopedic departments to manage growing patient volumes. Governments are prioritizing healthcare investments that strengthen surgical capacity and rehabilitation services.

Private healthcare providers are establishing specialized centers focused on sports injuries and joint reconstruction. Local manufacturers are introducing cost-efficient implants and bracing systems suited to high-volume clinical environments. Training initiatives are improving surgical proficiency and postoperative care practices among healthcare professionals. These developments are expected to accelerate the uptake of foot and ankle treatment technologies across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Foot and Ankle Devices Market expand growth by developing advanced orthopedic implants, strengthening collaborations with surgeons, and introducing minimally invasive surgical solutions that improve mobility and recovery outcomes. Companies invest in anatomically designed plates, screws, and joint replacement systems that enhance fixation stability and patient comfort.

They also focus on expanding training programs and digital surgical planning tools that support precision in complex foot and ankle procedures. Stryker Corporation represents a prominent participant in the Foot and Ankle Devices Market and operates as a U.S.-based medical technology company that develops orthopedic implants, surgical instruments, and digital surgery solutions for global healthcare systems.

The company emphasizes innovation in implant design and surgeon education to improve clinical outcomes. Industry competitors continue to introduce next-generation devices, expand global distribution networks, and strengthen clinical partnerships to drive adoption and sustain long-term market growth.

Top Key Players

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Smith & Nephew plc

- Johnson & Johnson (DePuy Synthes)

- Arthrex Inc.

- Wright Medical Technology Inc. (Stryker)

- Integra LifeSciences Holdings Corporation

- Ottobock Healthcare AG

- Össur hf

- Orthofix Medical Inc.

- Acumed LLC

- CONMED Corporation

- Medtronic plc

- Extremity Medical LLC

- Tornier N.V.

Recent Developments

- In March 2026, Zimmer Biomet released its financial outlook for the year, projecting moderate revenue growth following a solid performance in 2025. The company is focusing on expanding its sports medicine, extremities, and trauma portfolio, including advanced fixation systems used in complex orthopedic procedures.

- In December 2025, Smith & Nephew announced its RISE strategic plan, targeting sustained growth through innovation in soft tissue repair technologies. A key focus area includes regenerative implant solutions designed to support tendon healing and improve outcomes in patients with chronic conditions.

- In February 2026, Stryker initiated a limited release of its Mako Robotic Power System, a handheld robotic-assisted platform. While initially applied in knee procedures, the technology is expected to support future expansion into other orthopedic applications, including ankle replacement, as robotic-assisted surgery adoption continues to grow.

Report Scope

Report Features Description Market Value (2025) US$ 5.1 Billion Forecast Revenue (2035) US$ 10.8 Billion CAGR (2026-2035) 7.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Orthopedic Implants and Devices, Prostheses, Bracing and Support Devices and Others), By Application (Trauma and Hairline Fractures, Rheumatoid Arthritis and Osteoarthritis, Diabetic Foot Diseases, Ligament Injuries, Hammertoe, Neurological Disorders and Others), By End User (Hospitals, Ambulatory Surgical Centers (ASCs), Orthopedic Clinics and Rehabilitation Centers) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Stryker Corporation, Zimmer Biomet Holdings Inc., Smith & Nephew plc, Johnson & Johnson, Arthrex Inc., Wright Medical Technology Inc., Integra LifeSciences, Ottobock Healthcare AG, Össur hf, Orthofix Medical Inc., Acumed LLC, CONMED Corporation, Medtronic plc, Extremity Medical LLC, Tornier N.V. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Foot and Ankle Devices MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Foot and Ankle Devices MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Smith & Nephew plc

- Johnson & Johnson (DePuy Synthes)

- Arthrex Inc.

- Wright Medical Technology Inc. (Stryker)

- Integra LifeSciences Holdings Corporation

- Ottobock Healthcare AG

- Össur hf

- Orthofix Medical Inc.

- Acumed LLC

- CONMED Corporation

- Medtronic plc

- Extremity Medical LLC

- Tornier N.V.

Our Clients

- 183550

- April 2026