Global Food Containers Market Size, Share, And Enhanced Productivity By Product (Flexible Packaging, Paperboard, Rigid Packaging, Metal, Glass), By Application (Grain Mill Products, Dairy Goods, Fruits and Vegetables, Bakery Products, Meat Processed Goods, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182591

- Number of Pages: 368

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

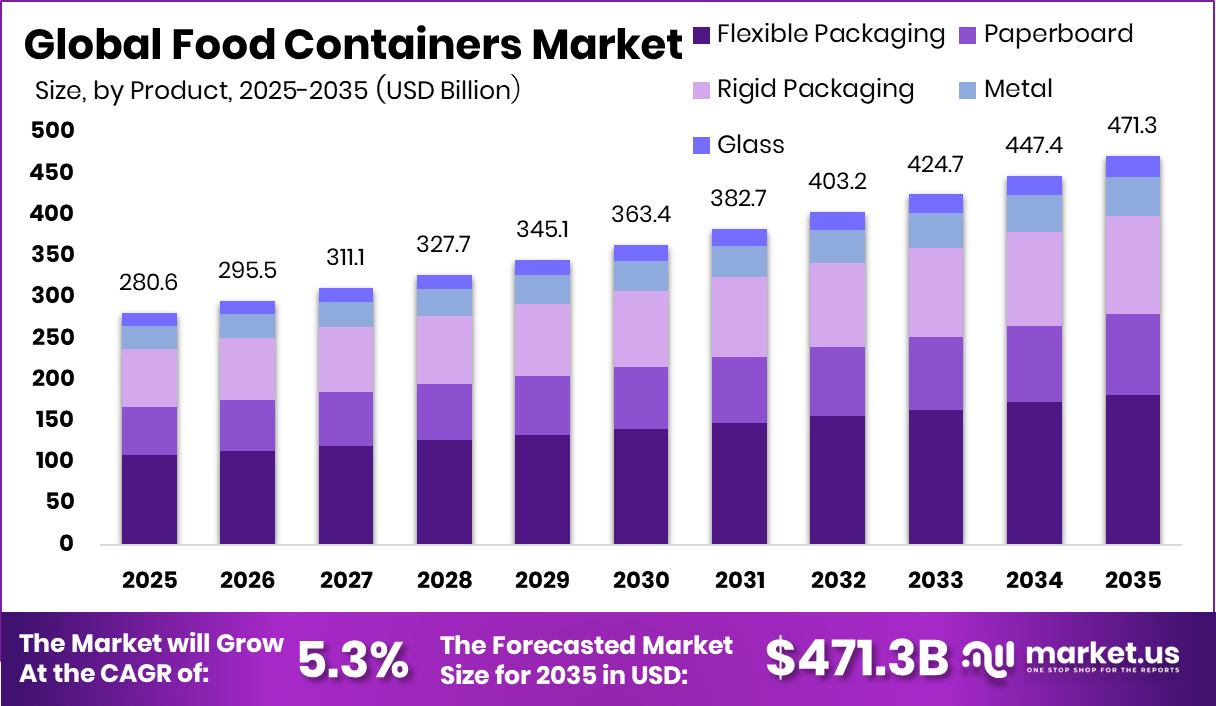

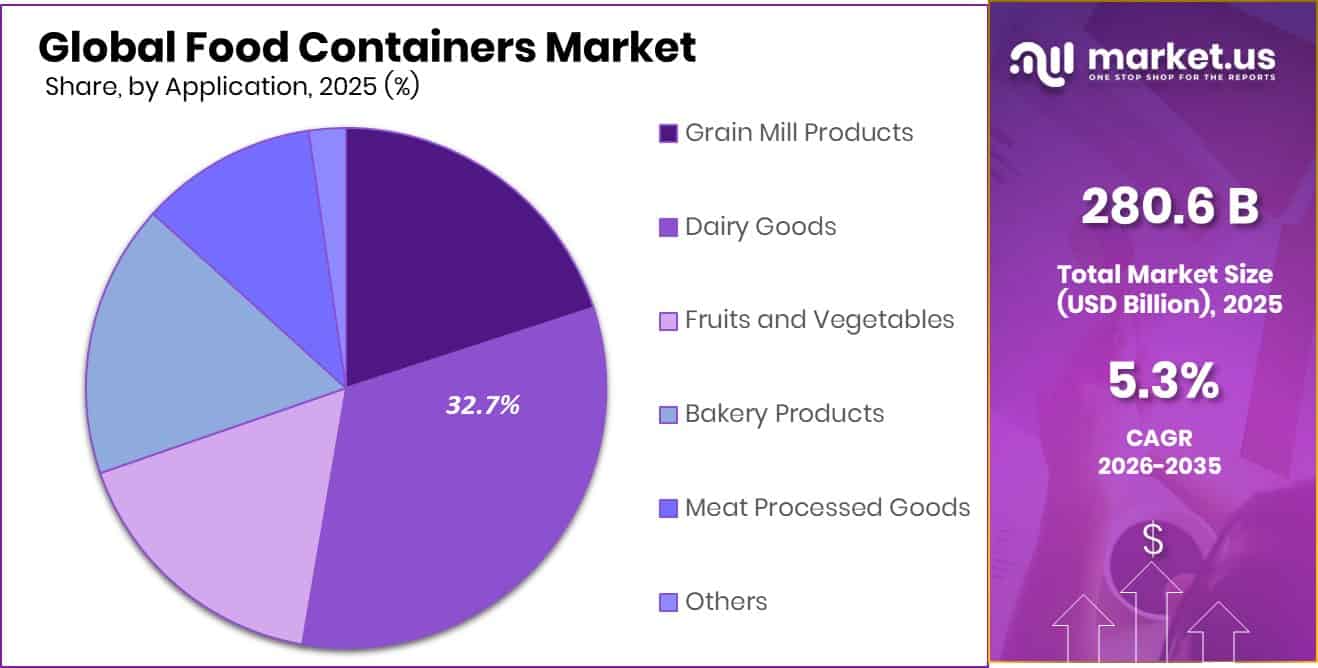

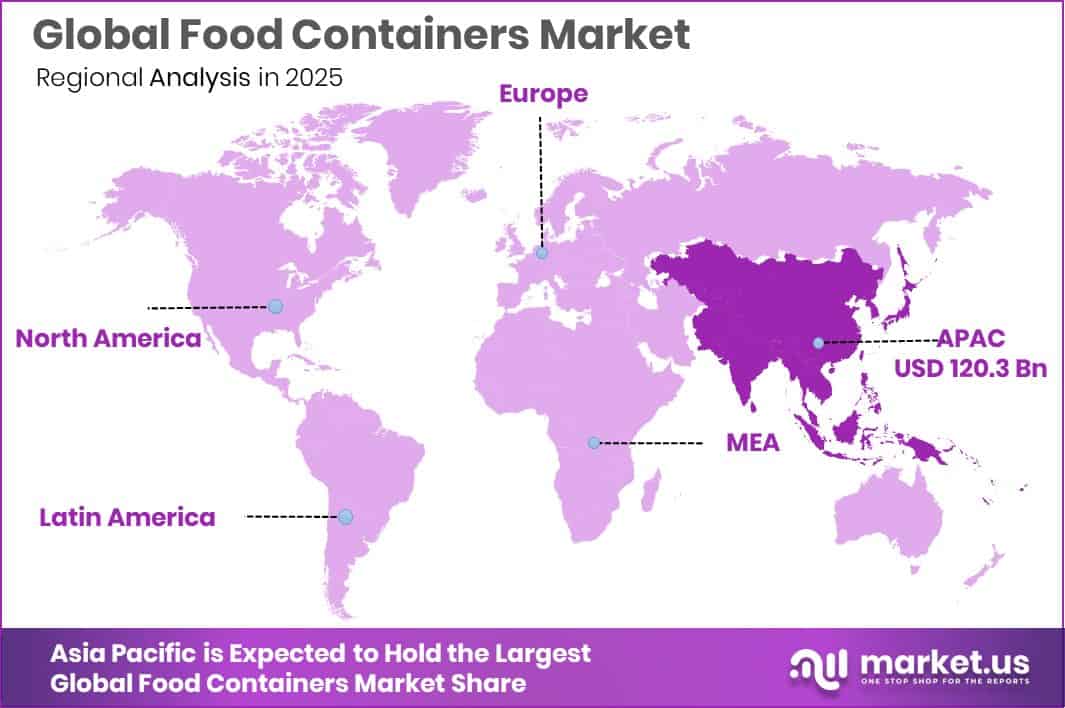

The Global Food Containers Market is expected to be worth around USD 471.3 billion by 2035, up from USD 280.6 billion in 2025. It is projected to grow at a CAGR of 5.3% from 2026 to 2035. With a USD 120.3 Bn valuation, Asia Pacific holds 42.9% food containers market share.

Food containers refer to materials and products used to store, protect, and transport food while maintaining freshness, safety, and quality. These include flexible packaging, paperboard, rigid packaging, metal, and glass formats designed for different food types. The Food Containers Market represents the overall demand and supply of such packaging solutions across industries handling grain mill products, dairy goods, fruits and vegetables, bakery items, meat processed goods, and other food categories.

Growth in the Food Containers Market is strongly influenced by rising food consumption, urban lifestyles, and the need for convenient packaging. Increasing investments are also supporting innovation, such as the £4.75 million secured by a Gateshead-based packaging firm, iPac, and the £1.1 billion boost to improve local recycling services across England, which enhances packaging sustainability and infrastructure development.

Demand for food containers continues to rise due to changing consumer habits, including ready-to-eat meals and takeaway culture. Funding initiatives like the $4.5 million raised by Friendlier and the $3.7 million secured by Dispatch Goods highlight the growing shift toward reusable and sustainable food container systems, particularly in food service and delivery segments.

Opportunities in this market are expanding with innovation and sustainability trends. Support from initiatives such as USDA funding for packaging innovations in the $143B specialty crop export industry and Sufresca’s $500k seed round for food coating solutions indicates strong potential for advanced materials that reduce waste while preserving food quality.

- In February 2025, Berry Global introduced pantry jars made from 100% recycled plastic, designed for food storage applications. These containers help reduce the use of new plastic while maintaining food safety and durability. The company, known for food packaging solutions, focused on sustainability by eliminating over 1,300 metric tons of virgin plastic annually through this product.

Key Takeaways

- The Global Food Containers Market is expected to be worth around USD 471.3 billion by 2035, up from USD 280.6 billion in 2025. It is projected to grow at a CAGR of 5.3% from 2026 to 2035.

- In the Food Containers Market, flexible packaging dominates with a significant 38.6% share globally.

- Within the Food Containers Market, dairy goods application accounts for 32.7% demand share worldwide.

- Food Containers Market in the Asia Pacific accounts for 42.9%, reaching a USD 120.3 Bn value.

By Product Analysis

In Food Containers Market, flexible packaging holds 38.6% share globally today.

In 2025, the Food Containers Market continues to witness steady growth, with flexible packaging emerging as a dominant product segment, accounting for 38.6% of the market share. This growth is driven by increasing demand for lightweight, cost-effective, and sustainable packaging solutions across the food industry. Flexible packaging offers advantages such as extended shelf life, reduced material usage, and convenience in storage and transportation, making it highly attractive for manufacturers and consumers alike.

Additionally, the rise of on-the-go consumption patterns and e-commerce food delivery services has further accelerated the adoption of flexible formats like pouches and wraps. As sustainability becomes a key focus, manufacturers are also investing in recyclable and biodegradable materials to align with evolving regulatory and consumer expectations.

By Application Analysis

In Food Containers Market, dairy goods account for 32.7% demand.

In 2025, the application of food containers in dairy goods represents a significant 32.7% share of the overall market, highlighting the sector’s strong reliance on effective packaging solutions. Dairy products such as milk, yogurt, cheese, and butter require packaging that ensures freshness, hygiene, and temperature control throughout the supply chain. The increasing consumption of dairy products, particularly in urban areas, is driving demand for innovative and durable container formats.

Packaging solutions are evolving to include tamper-proof designs, resealable features, and improved barrier properties to maintain product quality. Furthermore, the growing popularity of value-added dairy products and single-serve portions is encouraging manufacturers to adopt more versatile and consumer-friendly container designs, supporting sustained market expansion.

Key Market Segments

By Product

- Flexible Packaging

- Paperboard

- Rigid Packaging

- Metal

- Glass

By Application

- Grain Mill Products

- Dairy Goods

- Fruits and Vegetables

- Bakery Products

- Meat Processed Goods

- Others

Driving Factors

Rising demand for convenient food packaging

The Food Containers Market is benefiting from the growing preference for convenience in food consumption, particularly as busy lifestyles push consumers toward ready-to-eat and easy-to-store products. Packaging that supports portability, longer shelf life, and minimal preparation is gaining strong traction across multiple food categories. This shift is also reflected in business expansion activities, such as Food group Vandemoortele raising 100 million euros for expansion and acquisitions, indicating rising production and packaging needs.

As food producers scale operations, the requirement for efficient container solutions increases, supporting steady demand for flexible, rigid, and paper-based packaging formats that align with modern consumption patterns.

Increasing urbanization is boosting packaged food consumption

Rapid urbanization continues to shape the Food Containers Market, as more consumers rely on packaged and processed food products for daily consumption. Urban populations tend to prefer standardized, hygienic, and easy-to-handle food formats, which directly drives the need for reliable packaging solutions. This trend is supported by large-scale investments such as Ares leading a €300 million continuation fund for bakery Europastry, highlighting expansion in packaged food production.

As urban centers grow, food distribution networks become more complex, further increasing reliance on durable and efficient containers. This ongoing shift ensures consistent demand for diverse packaging materials suited to various food applications.

Restraining Factors

High cost of sustainable packaging materials

The transition toward sustainable packaging presents cost challenges within the Food Containers Market, particularly as eco-friendly materials often require higher production and sourcing expenses. While there is a strong interest in reducing environmental impact, manufacturers must balance affordability with sustainability goals. This challenge is evident in funding activities like a baked foods maker raising $21 million, reflecting efforts to manage operational and packaging costs while scaling production.

The higher price of biodegradable or recyclable materials can limit widespread adoption, especially among smaller producers, creating pressure on margins and slowing the pace of transition toward greener container solutions.

Stringent regulations on plastic usage globally

Regulatory pressure on plastic usage continues to impact the Food Containers Market, as governments introduce stricter rules to reduce environmental harm. Compliance with these regulations often requires redesigning packaging formats and investing in alternative materials, which can increase operational complexity. This environment is reflected in fast-moving business developments such as Hero Bread raising $21 million in less than 90 days to accelerate its bakery operations, where packaging compliance plays a role in scaling. Companies must adapt quickly to evolving standards, and while this drives innovation, it also creates short-term constraints and added costs across the packaging value chain.

Growth Opportunity

Expansion of reusable and recyclable packaging

The Food Containers Market is seeing strong opportunities in reusable and recyclable packaging systems as sustainability becomes a priority across the food industry. Businesses are exploring circular packaging models that reduce waste and improve resource efficiency. This direction is supported by investment activity such as biomass fermentation startup MOA Foodtech securing a $15.4 million commitment, reflecting broader innovation in sustainable food solutions.

As awareness grows, both producers and consumers are shifting toward packaging that can be reused or easily recycled. This creates long-term opportunities for companies to develop durable, cost-effective, and environmentally responsible container formats across multiple food applications.

Innovation in biodegradable food container materials

Advancements in biodegradable materials are opening new pathways for the Food Containers Market, enabling packaging that breaks down naturally without harming the environment. These innovations are particularly relevant for single-use food containers, where waste reduction is critical. The momentum is reinforced by funding developments such as Country Delight, raising $108 million led by Venturi Partners and Temasek, supporting expansion in food delivery and packaging needs.

As companies seek alternatives to conventional plastics, biodegradable solutions are gaining attention for their ability to balance functionality and sustainability, creating strong growth potential across dairy, fresh produce, and ready-to-eat segments.

Latest Trends

Shift toward eco friendly packaging solutions

A clear trend in the Food Containers Market is the transition toward eco-friendly packaging, driven by consumer awareness and regulatory expectations. Companies are increasingly adopting materials that reduce environmental impact while maintaining performance standards. This shift is supported by funding activity such as Hero Bread raising a total of $47.5 million to expand its retail presence, where packaging plays a key role in brand positioning.

Sustainable packaging is becoming a competitive differentiator, encouraging manufacturers to innovate in areas like recyclable films, paperboard containers, and reduced-plastic formats, aligning product offerings with evolving market preferences.

Growing adoption of smart food packaging

Smart packaging is emerging as a notable trend in the Food Containers Market, offering features that enhance food safety, tracking, and shelf-life monitoring. Technologies such as freshness indicators and intelligent labeling are gaining interest, particularly in processed and perishable food segments. This innovation-driven trend is reflected in funding such as Final Boss Sour securing $3 million in seed funding, indicating a broader interest in advanced food-related solutions.

As supply chains become more complex, smart packaging provides added value by improving transparency and reducing waste, positioning it as a key development area in modern food container design.

Regional Analysis

Asia Pacific region leads the Food Containers Market with 42.9% share, valued at USD 120.3 Bn.

The Food Containers Market demonstrates varied regional performance across North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, shaped by consumption patterns and packaging demand. Asia Pacific emerges as the dominating region, accounting for 42.9% of the market with a valuation of USD 120.3 Bn, driven by high population density and strong demand for packaged food products.

North America represents a mature market characterized by steady demand for convenience-oriented food packaging solutions. Europe follows closely, supported by established food processing industries and consistent consumption of packaged goods.

Meanwhile, the Middle East & Africa region reflects gradual market development, influenced by urbanization and evolving retail infrastructure. Latin America also shows steady progress, supported by rising demand for affordable and practical food container solutions.

Overall, regional dynamics indicate that while developed markets maintain stable demand, emerging economies—particularly in Asia Pacific—continue to drive volume growth and reinforce their leading market position.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Amcor plc, Silgan Holdings, Inc., and Ardagh Group represent three distinct yet complementary forces shaping the global Food Containers Market in 2025. Amcor plc stands out for its broad product portfolio and global footprint, enabling it to address diverse food packaging requirements across flexible and rigid formats. Its strategic focus on innovation and material optimization strengthens its position among large-scale food producers.

Silgan Holdings, Inc. maintains a strong presence through its specialization in rigid packaging solutions, particularly metal containers and closures. The company’s operational efficiency and consistent supply capabilities support long-term relationships with food manufacturers. Its focus on reliability and standardized packaging formats ensures stability in high-volume food packaging segments, making it a dependable industry participant.

Ardagh Group differentiates itself through its expertise in sustainable metal and glass packaging solutions. The company’s emphasis on recyclability and durable container formats aligns with evolving industry preferences for environmentally responsible packaging. Its ability to cater to both premium and mass-market food segments enhances its competitive positioning, particularly where product preservation and packaging integrity are critical factors.

Top Key Players in the Market

- Amcor plc

- Silgan Holdings, Inc.

- Ardagh Group

- Berry Plastics Corp.

- Plastipak Holdings, Inc.

- Sonoco Products Company

- Graham Packaging Company, Inc.

- Weener Plastics

- Ball Corp.

- Tetra Pak

Recent Developments

- In November 2024, Amcor plc, a global company that develops and produces food packaging solutions like flexible packs and containers, announced an all-stock acquisition of Berry Global in November 2024. The deal was valued at around $8.4 billion and aimed to expand Amcor’s packaging portfolio across flexible films, containers, and closures used in food applications. This merger was designed to strengthen product offerings and improve scale in food packaging solutions.

- In July 2024, Silgan Holdings, Inc., which manufactures rigid food containers and packaging solutions, announced an agreement to acquire Weener Plastics Holdings B.V. for about €838 million. The acquired company produces dispensing solutions used in food, healthcare, and consumer packaging. This move helped Silgan expand its product range, especially in closures and packaging components used in food containers.

Report Scope

Report Features Description Market Value (2025) USD 280.6 Billion Forecast Revenue (2035) USD 471.3 Billion CAGR (2026-2035) 5.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Flexible Packaging, Paperboard, Rigid Packaging, Metal, Glass), By Application (Grain Mill Products, Dairy Goods, Fruits and Vegetables, Bakery Products, Meat Processed Goods, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Amcor plc, Silgan Holdings, Inc., Ardagh Group, Berry Plastics Corp., Plastipak Holdings, Inc., Sonoco Products Company, Graham Packaging Company, Inc., Weener Plastics, Ball Corp., Tetra Pak Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Amcor plc

- Silgan Holdings, Inc.

- Ardagh Group

- Berry Plastics Corp.

- Plastipak Holdings, Inc.

- Sonoco Products Company

- Graham Packaging Company, Inc.

- Weener Plastics

- Ball Corp.

- Tetra Pak

Our Clients

- 182591

- March 2026