Quick Navigation

Report Overview

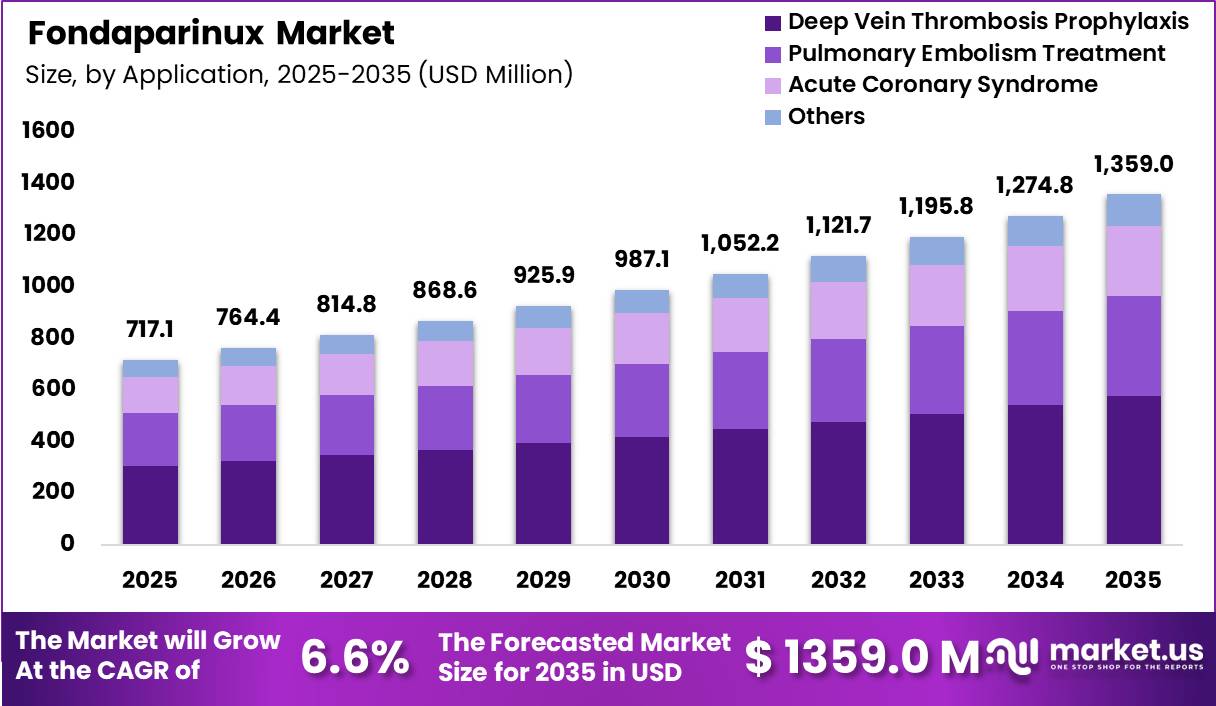

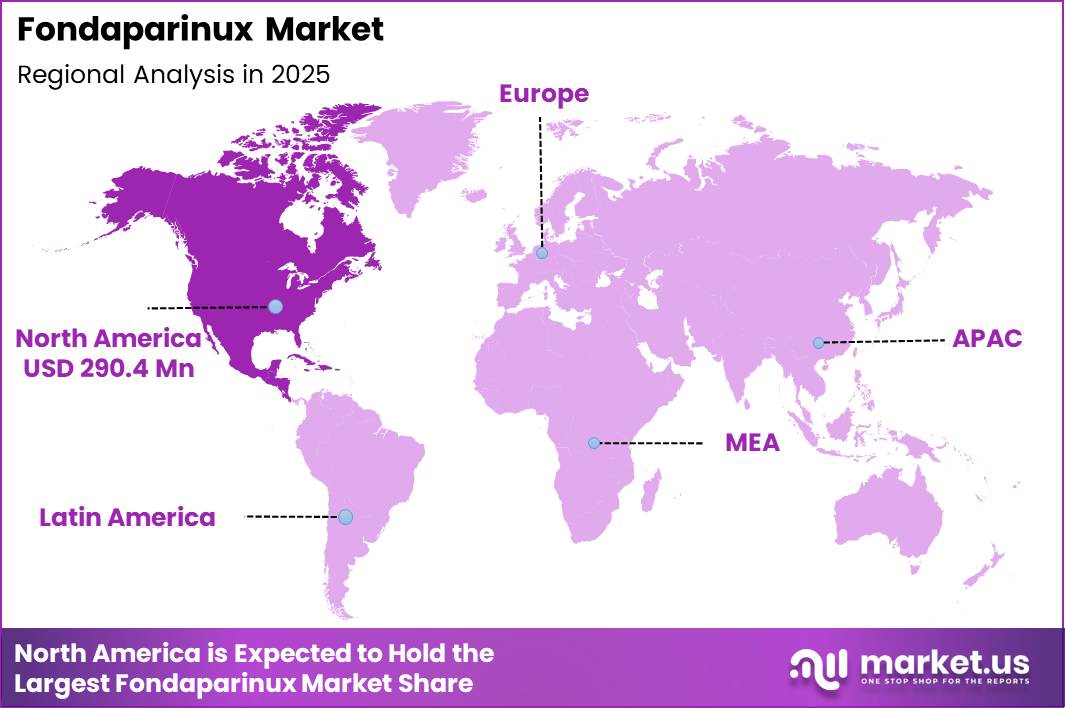

Global Fondaparinux Market size is expected to be worth around US$ 5.6 Million by 2035 from US$ 3.0 Million in 2025, growing at a CAGR of 6.6% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 40.5% share with a revenue of US$ 290.4 Million.

Fondaparinux is a synthetic anticoagulant widely used for the prevention and treatment of thromboembolic disorders, including deep vein thrombosis (DVT) and pulmonary embolism (PE). The drug acts through selective inhibition of Factor Xa, a key component in the blood coagulation cascade, helping to prevent clot formation while maintaining a predictable anticoagulant response.

Due to its favorable safety profile, once-daily dosing regimen, and low risk of heparin-induced thrombocytopenia (HIT), fondaparinux has become an important therapeutic option in thromboprophylaxis, particularly following major orthopedic procedures such as hip and knee replacement surgeries.

The increasing global burden of venous thromboembolism (VTE) continues to support demand for effective anticoagulant therapies. According to the U.S. Centers for Disease Control and Prevention (CDC), up to 900,000 people in the United States are affected by VTE annually, while an estimated 60,000 to 100,000 deaths occur each year as a result of these conditions. The CDC also identifies hospitalization and surgery as major risk factors for clot formation, highlighting the ongoing need for preventive anticoagulation in clinical settings.

A significant factor contributing to the growing adoption of fondaparinux is the rapid expansion of the elderly population, which is more susceptible to thromboembolic events due to reduced mobility, chronic diseases, and age-related physiological changes. According to the World Health Organization (WHO), by 2030, one in every six people worldwide will be aged 60 years or older, with the global population in this age group increasing from 1 billion in 2020 to 1.4 billion by 2030. This demographic shift is expected to increase the incidence of clot-related disorders and strengthen demand for reliable anticoagulant therapies.

Supported by rising surgical volumes, increasing awareness of thrombosis prevention, expanding healthcare access, and growing availability of generic formulations, fondaparinux continues to play a critical role in modern anticoagulation therapy and thromboembolism management worldwide.

Key Takeaways

- Market Size: Global Fondaparinux Market size is expected to be worth around US$ 5.6 Million by 2035 from US$ 3.0 Million in 2025.

- Market Share: The market growing at a CAGR of 6.6% during the forecast period from 2026 to 2035.

- Product Type Analysis: In 2025, the Branded (Arixtra) segment is expected to dominate the market, accounting for approximately 62.5% of total revenue share.

- Application Analysis: Deep Vein Thrombosis Prophylaxis is projected to hold the largest market share of 42.5% in 2025.

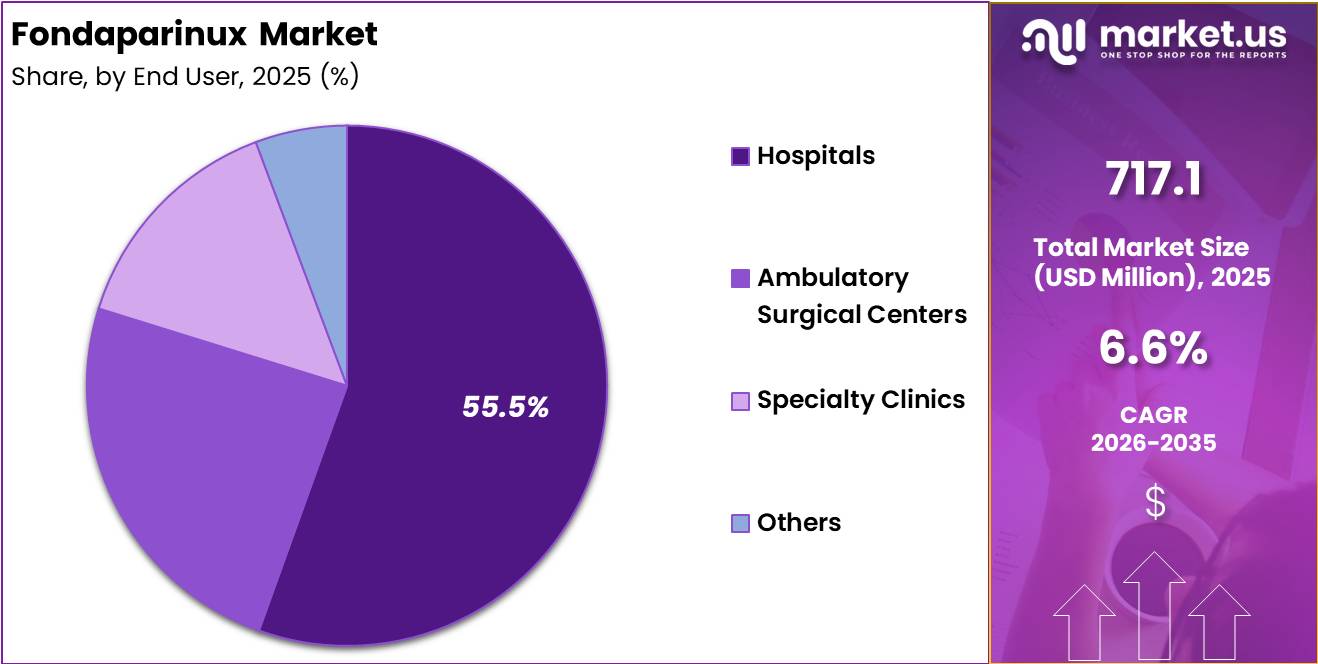

- End User Analysis: Hospitals are anticipated to remain the leading end-user segment, accounting for approximately 55.5% of the global market share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 40.5% share with a revenue of US$ 290.4 Million.

Product Type Analysis

The product type segment of the Fondaparinux market is categorized into Branded (Arixtra) and Generic products. In 2025, the Branded (Arixtra) segment is expected to dominate the market, accounting for approximately 62.5% of total revenue share. The strong position of Arixtra can be attributed to its established clinical efficacy, extensive physician familiarity, proven safety profile, and widespread adoption across hospitals and specialty healthcare facilities.

The brand continues to benefit from strong trust among healthcare professionals for the prevention and treatment of thromboembolic disorders, particularly in high-risk surgical and cardiovascular patients. Additionally, favorable reimbursement coverage in several developed healthcare systems supports its continued market leadership.

The Generic segment represents the remaining market share and is anticipated to witness steady growth during the forecast period. Increasing patent expirations, rising healthcare cost-containment initiatives, and growing acceptance of cost-effective anticoagulant therapies are encouraging the adoption of generic fondaparinux formulations.

Healthcare providers and public healthcare institutions are increasingly incorporating generics into treatment protocols to reduce overall treatment expenses while maintaining therapeutic effectiveness. As emerging economies continue expanding access to affordable anticoagulation therapies, the generic segment is expected to gain momentum and contribute significantly to future market expansion.

Application Analysis

Based on application, the Fondaparinux market is segmented into Deep Vein Thrombosis (DVT) Prophylaxis, Pulmonary Embolism Treatment, Acute Coronary Syndrome, and Others. Among these, Deep Vein Thrombosis Prophylaxis is projected to hold the largest market share of 42.5% in 2025.

The segment’s dominance is driven by the increasing number of orthopedic and major surgical procedures worldwide, where anticoagulant prophylaxis is routinely recommended to prevent post-operative thrombotic complications. Growing awareness regarding venous thromboembolism prevention and adherence to evidence-based clinical guidelines further support segment growth.

The Pulmonary Embolism Treatment segment represents a significant share of the market due to the rising incidence of pulmonary embolism and increasing use of fondaparinux as an effective anticoagulant therapy. The Acute Coronary Syndrome segment is also witnessing notable growth, supported by expanding cardiovascular disease prevalence and the use of fondaparinux in managing unstable angina and non-ST-elevation myocardial infarction cases.

Meanwhile, the Others category includes various off-label and specialized anticoagulation applications. Continuous advancements in diagnostic capabilities and increasing demand for targeted thrombosis management are expected to sustain growth across all application segments throughout the forecast period.

End User Analysis

Based on end users, the Fondaparinux market is segmented into Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, and Others. Hospitals are anticipated to remain the leading end-user segment, accounting for approximately 55.5% of the global market share in 2025.

The dominance of hospitals is primarily attributed to the high volume of surgical procedures, inpatient treatment of thromboembolic disorders, and management of acute cardiovascular conditions requiring anticoagulant therapy. Hospitals also possess advanced diagnostic and monitoring infrastructure, enabling the safe administration of fondaparinux for complex patient populations.

The Ambulatory Surgical Centers (ASCs) segment is expected to register steady growth due to the increasing shift toward outpatient surgical procedures and cost-efficient healthcare delivery models. These facilities are increasingly utilizing anticoagulant prophylaxis protocols to minimize post-surgical complications. The Specialty Clinics segment is gaining traction as dedicated cardiovascular and hematology clinics expand their role in thrombosis management and long-term anticoagulation care.

The Others segment includes rehabilitation centers, long-term care facilities, and home healthcare settings where fondaparinux is prescribed for specific patient needs. Rising healthcare accessibility, growing focus on preventive care, and expanding treatment options across various healthcare settings are expected to drive demand across all end-user categories.

Key Market Segments

By Product Type

- Branded (Arixtra)

- Generic

By Application

- Deep Vein Thrombosis Prophylaxis

- Pulmonary Embolism Treatment

- Acute Coronary Syndrome

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Others

Driving Factors

Rising VTE burden and surgical procedures

The main driver for the fondaparinux market is the growing clinical need to prevent and treat venous thromboembolism (VTE) associated with hospitalisation and surgery. Each year, up to 900,000 people in the United States are affected by VTE, and an estimated 100,000 of them die, highlighting a substantial unmet need for effective anticoagulation.

Modelling data from six European countries (combined population b) estimated 296,000 pulmonary embolism and 370,000 deep vein thrombosis cases annually, underlining the scale of demand in high-income health systems where fondaparinux is routinely used. Globally, VTE is estimated to affect nearly 10 million people per year. Ageing populations further intensify this driver because VTE incidence and case-fatality rates rise steeply after 60 years.

In parallel, the volume of major orthopedic, cancer and cardiovascular surgeries—procedures for which pharmacological thromboprophylaxis is recommended in many guidelines—continues to increase, expanding the eligible patient pool for fondaparinux and supporting sustained market growth.

Trending Factors

Shift to guideline-driven prophylaxis and safer anticoagulation

A key trend shaping the fondaparinux market is the progressive shift toward standardized, guideline-driven VTE prophylaxis in hospitals and post-acute care settings. CDC highlights that VTE is the leading cause of preventable hospital death in the United States, which has triggered hospital quality programs and payer incentives to ensure appropriate anticoagulant use.

These initiatives increase uptake of agents such as fondaparinux in high-risk surgical and medical inpatients. At the same time, epidemiological studies show that pulmonary-embolism-related deaths, while still significant (0.46% of all global deaths in one analysis of 18.7 million deaths), have started to decline in some regions, reflecting broader adoption of prophylaxis and early treatment. This environment favours anticoagulants with predictable pharmacokinetics, once-daily dosing and low heparin-induced thrombocytopenia risk, characteristics associated with fondaparinux and competing factor-Xa-focused regimens.

Growing awareness campaigns on blood clot prevention, run by public health agencies, are also pushing earlier diagnosis and longer prophylaxis durations in high-risk groups, which supports a steady expansion of fondaparinux use volumes rather than short, acute-only courses.

Restraining Factors

Bleeding risk, monitoring gaps and competing therapies

The principal restraint for the fondaparinux market is safety and management complexity, especially the risk of major bleeding in fragile patients. Hospital-based CDC data show that among the hundreds of thousands of annual VTE events in the United States, a substantial fraction are associated with serious comorbidities, renal impairment and polypharmacy, which heighten bleeding risk when potent anticoagulants like fondaparinux are used.

Clinical guidance notes that fondaparinux must be used cautiously in patients with body weight under 50 kg or creatinine clearance below 30 ml/min, which excludes a measurable proportion of elderly VTE candidates and limits eligible volume growth. Unlike vitamin K antagonists, there is no widely available, specific reversal agent for fondaparinux, and management of severe hemorrhage can require complex supportive care, which makes some clinicians and payers favour alternatives.

In addition, the rapid penetration of direct oral anticoagulants (DOACs) in indications such as non-valvular atrial fibrillation and long-term VTE secondary prevention introduces strong competition, diluting fondaparinux share despite its established role in peri-operative and initial treatment settings.

Opportunity

Under-penetrated high-burden regions and prevention focus

A major opportunity for the fondaparinux market lies in expanding access in regions where VTE prevention remains under-implemented despite high disease burden. Global estimates suggest nearly 10 million people develop VTE annually, yet many low- and middle-income countries lack systematic prophylaxis in surgical and medical inpatients.

As these health systems scale up surgery (orthopedic, cancer, obstetric and cardiovascular) and adopt international hospital-accreditation standards that emphasise VTE prevention, demand for guideline-listed anticoagulants such as fondaparinux can increase markedly from a relatively low base. There is also scope to grow in outpatient prophylaxis and extended post-discharge use, since nearly 3 in 10 people who experience a blood clot will have a recurrence within 10 years, reinforcing the need for sustained secondary prevention strategies that can include fondaparinux-based regimens in select patients.

Regional Analysis

North America dominated the global Fondaparinux market in 2025, accounting for more than 40.5% of the total market share and generating revenue of approximately US$ 290.4 million. The region’s leading position can be attributed to the high prevalence of cardiovascular diseases, venous thromboembolism (VTE), deep vein thrombosis (DVT), and pulmonary embolism, which continue to drive demand for effective anticoagulant therapies. The presence of a well-established healthcare infrastructure, widespread access to advanced diagnostic services, and strong awareness regarding thrombosis prevention have further supported market growth across the region.

The United States represented the largest contributor to regional revenue, supported by increasing surgical procedures, a growing geriatric population, and favorable reimbursement frameworks. Additionally, the adoption of evidence-based treatment guidelines and the availability of specialized healthcare professionals have encouraged the use of Fondaparinux in both hospital and outpatient settings. Canada also contributed significantly to regional market expansion through rising healthcare expenditures and improved access to anticoagulant therapies.

Furthermore, ongoing clinical research activities, strong pharmaceutical distribution networks, and the presence of major market participants have strengthened the market landscape in North America. Regulatory support for innovative anticoagulation therapies and continuous investments in healthcare modernization are expected to sustain market growth. As a result, North America is anticipated to maintain its dominant position in the global Fondaparinux market throughout the forecast period.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Fondaparinux market is characterized by the presence of established pharmaceutical manufacturers focused on expanding their anticoagulant portfolios through product innovation, geographic expansion, and strategic partnerships. Key players are actively investing in research and development to enhance product efficacy, improve patient outcomes, and strengthen their competitive positioning. Market participants are also emphasizing the development of generic formulations to address the growing demand for cost-effective anticoagulant therapies, particularly in emerging economies.

Companies compete on factors such as product quality, regulatory compliance, manufacturing capabilities, pricing strategies, and distribution network strength. The increasing prevalence of thromboembolic disorders and cardiovascular diseases has encouraged manufacturers to expand production capacities and improve supply chain efficiency. In addition, collaborations with healthcare providers, hospitals, and research institutions are supporting greater product adoption and market penetration.

Regulatory approvals and product launches remain important growth strategies, enabling companies to access new markets and broaden their customer base. As healthcare systems increasingly prioritize effective thrombosis management, leading players are expected to focus on innovation, market expansion, and operational excellence to sustain long-term growth in the global Fondaparinux market.

Market Key Players

- Aspen Pharmacare Holdings Limited

- GlaxoSmithKline plc (GSK)

- Dr. Reddy’s Laboratories Ltd.

- Mylan N.V.

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Cipla Inc.

- Apotex Inc.

- Alvogen, Inc.

- Fresenius Kabi AG

- Sandoz International GmbH

- Pfizer Inc.

- Sanofi S.A.

- Baxter International Inc.

- Hikma Pharmaceuticals PLC

- Others

Recent Developments

- March 2025 – Fresenius Kabi AG received U.S. FDA approval for its denosumab biosimilars, Conexxence® and Bomyntra®, and simultaneously secured a global settlement agreement with Amgen. The development strengthened Fresenius Kabi’s injectable and biosimilar portfolio while expanding its presence in hospital-based pharmaceutical markets, which are closely aligned with the distribution channels used for anticoagulant products such as fondaparinux.

- September 2025 – Sanofi S.A. committed an additional $625 million to Sanofi Ventures, increasing total assets under management to more than $1.4 billion. The investment is intended to accelerate innovation across biotechnology and digital health, strengthening Sanofi’s long-term pharmaceutical pipeline and specialty-care portfolio.

- 2025 – Sandoz International GmbH entered a global collaboration and licensing agreement with Henlius to commercialize ipilimumab, an oncology biologic. The agreement strengthened Sandoz’s specialty pharmaceutical portfolio and reinforced its strategy of expanding through partnerships and licensing arrangements in complex therapeutic categories.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 3.0 Million |

| Forecast Revenue (2035) | US$ 5.6 Million |

| CAGR (2026-2035) | 6.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Branded (Arixtra), Generic) By Application (Deep Vein Thrombosis Prophylaxis, Pulmonary Embolism Treatment, Acute Coronary Syndrome, Others) By End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Aspen Pharmacare Holdings Limited, GlaxoSmithKline plc (GSK), Dr. Reddy’s Laboratories Ltd., Mylan N.V., Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Cipla Inc., Apotex Inc., Alvogen, Inc., Fresenius Kabi AG, Sandoz International GmbH, Pfizer Inc., Sanofi S.A., Baxter International Inc., Hikma Pharmaceuticals PLC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |