Global Depth Filtration Market Size, Share Analysis Report By Media (Diatomaceous Earth, Cellulose, Activated Carbon, Perlite, Others), By Product (Cartridge Filters, Capsule Filters, Filter Sheets, Filter Modules, Plate And Frame Filters, Others), By Application (Final Product Processing, Cell Clarification, Raw Material Filtration, Diagnostics, Viral Clearance), By End Use (Water Filtration, Food And Beverages, Healthcare, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182238

- Number of Pages: 322

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

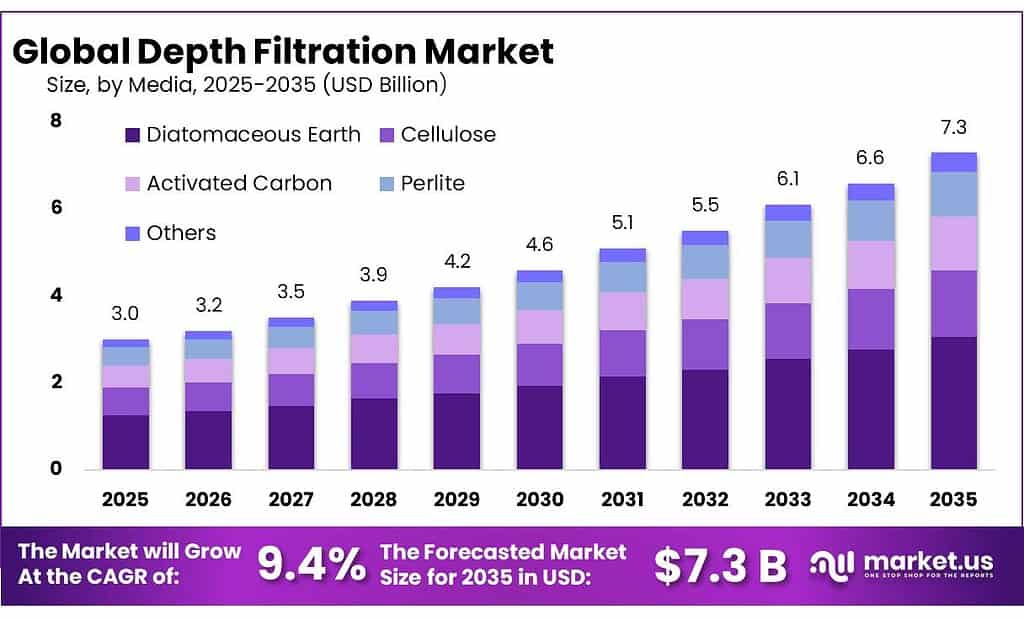

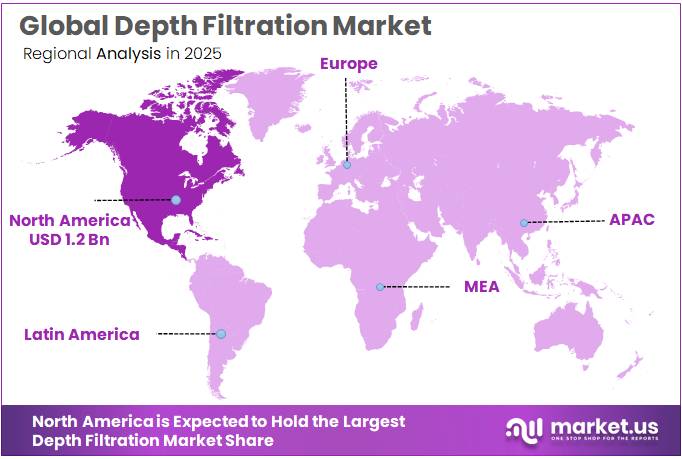

The Global Depth Filtration Market size is expected to be worth around USD 7.3 Billion by 2035, from USD 3.0 Billion in 2025, growing at a CAGR of 9.4% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 41.9% share, holding USD 1.2 Billion revenue.

Depth filtration is a critical separation technology used to remove suspended solids, colloids, haze-forming particles, and microbial load from liquid food and beverage streams. In industrial practice, it is widely applied in beer, wine, edible oils, sweeteners, dairy ingredients, flavor systems, and process water polishing because the media captures contaminants through the full thickness of the filter rather than only on the surface.

This is especially significant in a global food environment where unsafe food is estimated to cause 600 million cases of foodborne disease and 420,000 deaths each year, according to the World Health Organization.

The industrial scenario remains favorable because food processing volumes are large and becoming more quality-sensitive. In the United States alone, food and beverage processing employed 1.7 million workers in 2021, and the country had 42,708 food and beverage manufacturing establishments in 2022; meat processing represented 26.2% of sector sales, while beverages accounted for 11.3%. Such scale supports recurring demand for clarification, prefiltration, and contaminant-control systems, including depth filtration in both batch and continuous operations.

In Europe, the food and drink industry employs 4.7 million people, generates €1.2 trillion in turnover, and contributes €250 billion in value added, confirming a large installed base for filtration-intensive processing across beverages, dairy, ingredients, and specialty foods.

The main demand drivers are food safety, regulatory tightening, process yield improvement, and sustainability. The U.S. FDA states that the Food Safety Modernization Act shifts the system from reaction to prevention, while the preventive controls rule requires covered facilities to maintain a food safety plan based on hazard analysis and risk-based controls.

Merck KGaA announced in September 2025 the opening of a €150 million climate-neutral filter manufacturing facility in Ireland, part of a broader €440 million investment in the country and a €2 billion Life Science expansion program; the site includes a 3,000-square-meter cleanroom, is expected to create more than 200 jobs by 2028, and is designed to reuse up to 95% of high-purity reverse-osmosis water.

For 3M Company, a notable 2025 development was the launch of the Filtrete refillable filter platform, with a reusable frame lasting up to 20 years, refills lasting up to 12 months, storage-space reduction of 75%, and disposable-waste reduction of 20%; in parallel, 3M confirmed completion of its PFAS manufacturing exit at the end of 2025, signaling a stronger sustainability direction around filtration-related product portfolios.

Key Takeaways

- Depth Filtration Market size is expected to be worth around USD 7.3 Billion by 2035, from USD 3.0 Billion in 2025, growing at a CAGR of 9.4%.

- Diatomaceous Earth held a dominant market position, capturing more than a 42.7% share.

- Cartridge Filters held a dominant market position, capturing more than a 37.5% share.

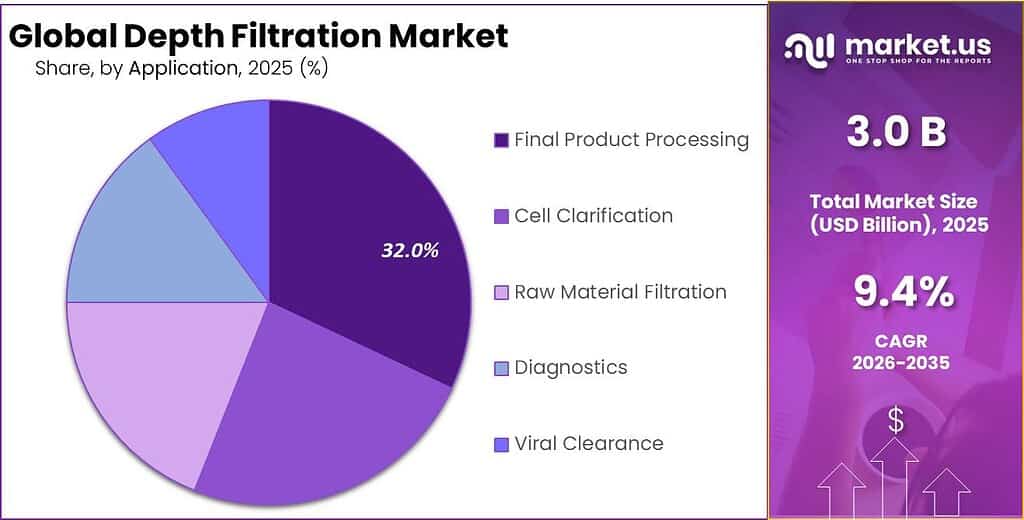

- Final Product Processing held a dominant market position, capturing more than a 32.6% share.

- Food & Beverages held a dominant market position, capturing more than a 39.1% share.

- North America continues to lead the depth filtration market, holding a dominant share of 41.9% with an estimated value of around USD 1.2 billion.

By Media Analysis

Diatomaceous Earth leads the depth filtration market with a 42.7% share driven by its strong filtration efficiency and versatility

In 2025, Diatomaceous Earth held a dominant market position, capturing more than a 42.7% share. Its strong hold in the market comes from its excellent ability to remove very fine particles, making it a preferred choice across industries like food & beverage, pharmaceuticals, and water treatment. Many manufacturers continue to rely on this medium because it offers consistent filtration results and is relatively easy to handle in large-scale operations. The material’s natural porous structure allows for high flow rates while still maintaining clarity, which adds to its demand.

By Product Analysis

Cartridge Filters lead the market with 37.5% share thanks to their ease of use and reliable performance

In 2025, Cartridge Filters held a dominant market position, capturing more than a 37.5% share. This strong position is mainly due to their simple design, easy installation, and low maintenance needs, which make them a popular choice across multiple industries. Many users prefer cartridge filters because they offer consistent filtration quality without requiring complex setups. They are widely used in applications like pharmaceuticals, food processing, and water purification, where clean and controlled filtration is essential.

By Application Analysis

Final Product Processing leads with 32.6% share as industries focus on quality and purity at the last stage

In 2025, Final Product Processing held a dominant market position, capturing more than a 32.6% share. This segment plays a key role because it is the last step before products reach customers, where maintaining high quality and removing any remaining impurities becomes critical. Industries such as pharmaceuticals, food & beverage, and biotechnology depend heavily on this stage to ensure safety, clarity, and compliance with standards. Depth filtration is widely used here as it provides reliable and consistent results without affecting the final product.

By End Use Analysis

Food & Beverages dominates with 39.1% share driven by high demand for safe and clear products

In 2025, Food & Beverages held a dominant market position, capturing more than a 39.1% share. This segment leads mainly because filtration is a critical step in ensuring product safety, taste, and appearance. Manufacturers rely heavily on depth filtration to remove impurities, particles, and unwanted residues from products like juices, beer, wine, and edible oils. The need for consistent quality and compliance with food safety standards keeps the demand strong in this segment.

Key Market Segments

By Media

- Diatomaceous Earth

- Cellulose

- Activated Carbon

- Perlite

- Others

By Product

- Cartridge Filters

- Capsule Filters

- Filter Sheets

- Filter Modules

- Plate & Frame Filters

- Others

By Application

- Final Product Processing

- Cell Clarification

- Raw Material Filtration

- Diagnostics

- Viral Clearance

By End Use

- Water Filtration

- Food & Beverages

- Healthcare

- Others

Emerging Trends

Shift toward advanced and cleaner filtration technologies is shaping the future of depth filtration

One of the latest trends in the depth filtration market is the growing shift toward advanced and cleaner filtration technologies, especially in food and beverage processing. As production volumes rise, industries are moving beyond traditional methods and adopting more efficient systems that ensure better product quality. According to industry data, the global food and beverage filtration sector was valued at around $46.9 billion in 2024 and continues to expand as demand for clean-label and contaminant-free products increases.

By 2025 and 2026, manufacturers are focusing on filtration systems that not only remove particles but also improve taste, shelf life, and safety. This includes combining depth filtration with newer technologies to achieve better results. Consumers today are more aware of what they consume, pushing companies to invest in filtration that ensures purity without affecting product quality. As a result, depth filtration is evolving from a basic process into a more advanced and value-adding step in production.

Integration of sustainability and waste reduction practices in filtration processes

Another important trend is the growing focus on sustainability in filtration processes. Industries are now looking for ways to reduce waste, reuse materials, and improve overall efficiency. According to the Food and Agriculture Organization, global food systems are undergoing major transformation with new technologies and sustainable practices being introduced across production and processing.

In 2025 and 2026, companies are increasingly adopting eco-friendly filtration media and processes that reduce environmental impact. There is also a push from governments and regulatory bodies to support sustainable manufacturing practices. This includes better waste management and reduced resource usage in food processing industries. As sustainability becomes a key priority, depth filtration systems are being redesigned to last longer and generate less waste.

Drivers

Rising demand for safe and high-quality food products is pushing filtration adoption

One of the biggest drivers for depth filtration is the growing demand for safe and clean food products. As food production scales up globally, manufacturers are under constant pressure to maintain hygiene and product quality. Depth filtration plays an important role in removing unwanted particles, microbes, and impurities before products reach consumers. According to the Food and Agriculture Organization, global food production needs to increase by nearly 60% by 2050 to meet rising demand. This puts strong pressure on processing industries to improve filtration systems.

In addition, the World Health Organization has reported that unsafe food causes around 600 million cases of foodborne diseases every year, which makes filtration even more critical in preventing contamination. Governments are also tightening food safety regulations, pushing companies to invest in reliable filtration technologies. As a result, depth filtration is becoming a standard part of food processing operations, helping producers maintain safety, consistency, and compliance while meeting increasing global demand.

Government focus on food safety and processing standards supports filtration growth

Government initiatives around food safety and processing standards are another strong factor driving the depth filtration market. Many countries are introducing stricter rules to ensure that food products are free from contamination and safe for consumption. For example, India’s Food Safety and Standards Authority of India (FSSAI) continues to strengthen guidelines for food processing and hygiene practices, especially in packaged and processed foods. At the same time, the U.S. Food and Drug Administration enforces strict requirements under the Food Safety Modernization Act (FSMA), focusing on preventive controls rather than reactive measures.

These policies are encouraging manufacturers to adopt advanced filtration methods like depth filtration to meet compliance. In addition, increasing investment in food processing infrastructure by governments, especially in developing economies, is boosting the use of filtration systems. With more focus on export quality and global standards, companies are upgrading their processes, where filtration becomes essential. This regulatory push is steadily increasing the adoption of depth filtration across food and beverage industries worldwide.

Restraints

High operational waste and disposal challenges limit wider adoption of depth filtration

One major restraining factor in the depth filtration market is the issue of waste generation and disposal. Depth filters, especially those used in food and beverage processing, often have a limited lifecycle and need to be replaced frequently. This creates a significant amount of solid waste, which industries must manage carefully. According to the Food and Agriculture Organization, around 1.3 billion tonnes of food is wasted globally every year, and a portion of this waste is linked to processing inefficiencies, including filtration losses and disposal challenges.

Governments are also pushing for stricter environmental norms, making disposal more complex and sometimes expensive. These factors make some industries hesitant to fully depend on depth filtration, especially where continuous operations require frequent media replacement.

Rising environmental regulations increase pressure on filtration waste management

Another key restraint comes from tightening environmental regulations around industrial waste handling. Many countries are focusing on reducing industrial waste and promoting sustainable practices. For example, the European Environment Agency highlights that waste from manufacturing sectors continues to be a major concern, with millions of tonnes generated annually across industries. Filtration media used in depth filtration often contains trapped contaminants, making disposal more regulated and costly. In food processing industries, maintaining compliance while managing waste adds an extra operational burden.

Similarly, guidelines from the Central Pollution Control Board require industries to treat and dispose of solid waste properly, which can increase costs for manufacturers using disposable filtration systems. As sustainability becomes a priority, companies are exploring alternative filtration methods that produce less waste. This shift is slowing down the adoption of traditional depth filtration systems in some regions, especially where environmental compliance costs are rising steadily.

Opportunity

Growing global food processing and trade expansion is creating strong opportunities for depth filtration

One of the biggest growth opportunities for depth filtration comes from the rapid expansion of the global food processing and trade industry. As food moves across borders and supply chains become more complex, the need for clean, safe, and stable products becomes critical. According to the UNCTAD and World Health Organization, global food trade increased by around 350% between 2000 and 2021, reaching nearly $1.7 trillion in value. This massive growth means more processing, packaging, and preservation steps, all of which require reliable filtration systems.

Looking at 2025 and 2026, this trend is only getting stronger as more countries invest in food exports and processed food manufacturing. With increasing demand for packaged and ready-to-eat products, companies are expanding their production capacity. This creates a clear need for efficient filtration solutions that can handle higher volumes without compromising quality. As global food supply chains grow, depth filtration becomes more important in maintaining product standards across different regions.

Rising food production levels and government support for processing infrastructure boost demand

Another strong opportunity comes from the steady increase in global food production and government-backed investments in food processing infrastructure. The Food and Agriculture Organization reports that global agricultural production is expected to grow by about 14% over the next decade. Another strong opportunity comes from the steady increase in global food production and government-backed investments in food processing infrastructure. The Food and Agriculture Organization reports that global agricultural production is expected to grow by about 14% over the next decade.

Governments are also actively supporting this growth. For example, initiatives to strengthen food processing sectors and improve value addition are being introduced in many countries. These efforts are aimed at reducing food losses, improving export quality, and supporting local industries. As production volumes grow and processing becomes more advanced, filtration becomes a necessary step rather than an option. This creates a long-term opportunity for depth filtration systems, especially in regions where food processing industries are expanding rapidly.

Regional Insights

North America dominates the depth filtration market with 41.9% share, reaching around USD 1.2 billion driven by strong industrial and healthcare demand

North America continues to lead the depth filtration market, holding a dominant share of 41.9% with an estimated value of around USD 1.2 billion. The region’s leadership is mainly supported by its well-established pharmaceutical, biotechnology, and food processing industries, all of which rely heavily on advanced filtration systems.

The United States plays a major role here, with strong investments in biologics manufacturing and strict regulatory standards that require high levels of product purity. In 2025, North America remained the largest regional contributor, supported by continuous demand for filtration in vaccine production, food safety, and water treatment applications.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Merck KGaA stands as a strong player in the depth filtration market, supported by its broad life sciences and bioprocessing portfolio. The company reported revenue of around €21 billion in 2024, with a significant contribution from its life science segment, which includes filtration technologies. With operations in over 60 countries and more than 62,000 employees, Merck continues to expand its filtration capabilities to meet growing global demand.

3M Company plays a key role in the filtration industry through its advanced materials and purification technologies. The company generates annual revenues exceeding $30 billion, with filtration products forming an important part of its healthcare and industrial segments. Its depth filtration solutions are widely applied in food safety, water purification, and pharmaceutical processing. 3M’s strong R&D investment, which crosses $1 billion annually, helps in developing innovative filtration systems.

Parker-Hannifin Corporation is a major contributor to the depth filtration market, particularly through its filtration and engineered materials segment. In 2025, this segment alone generated about $5.81 billion, accounting for 42.5% of total company revenue. The company offers advanced filtration systems for industrial and pharmaceutical applications. Its continuous expansion strategy, including a $9.25 billion acquisition to strengthen filtration capabilities, highlights its focus on growth.

Top Key Players Outlook

- Merck KGaA

- 3M Company

- Parker-Hannifin Corporation

- Amazon Filters Ltd.

- Pall Corporation

- Eaton Corporation plc

- Sartorius AG

- Filtrox AG

- Graver Technologies LLC

- Donaldson Company, Inc.

Recent Industry Developments

In 2025, Merck KGaA reported total net sales of around €21.1 billion, showing stable performance despite global challenges, while its Life Science division recorded about 4.0% organic growth, mainly driven by demand for filtration and purification technologies used in biologics production.

In 2025, 3M reported total sales of around $24.6 billion, with its Safety & Industrial business contributing nearly $11.0 billion, showing how important industrial filtration-related products are within its portfolio.

Report Scope

Report Features Description Market Value (2025) USD 3.0 Bn Forecast Revenue (2035) USD 7.3 Bn CAGR (2026-2035) 9.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Media (Diatomaceous Earth, Cellulose, Activated Carbon, Perlite, Others), By Product (Cartridge Filters, Capsule Filters, Filter Sheets, Filter Modules, Plate And Frame Filters, Others), By Application (Final Product Processing, Cell Clarification, Raw Material Filtration, Diagnostics, Viral Clearance), By End Use (Water Filtration, Food And Beverages, Healthcare, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Merck KGaA, 3M Company, Parker-Hannifin Corporation, Amazon Filters Ltd., Pall Corporation, Eaton Corporation plc, Sartorius AG, Filtrox AG, Graver Technologies LLC, Donaldson Company, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Merck KGaA

- 3M Company

- Parker-Hannifin Corporation

- Amazon Filters Ltd.

- Pall Corporation

- Eaton Corporation plc

- Sartorius AG

- Filtrox AG

- Graver Technologies LLC

- Donaldson Company, Inc.

Our Clients

- 182238

- Mar 2026