Quick Navigation

Report Overview

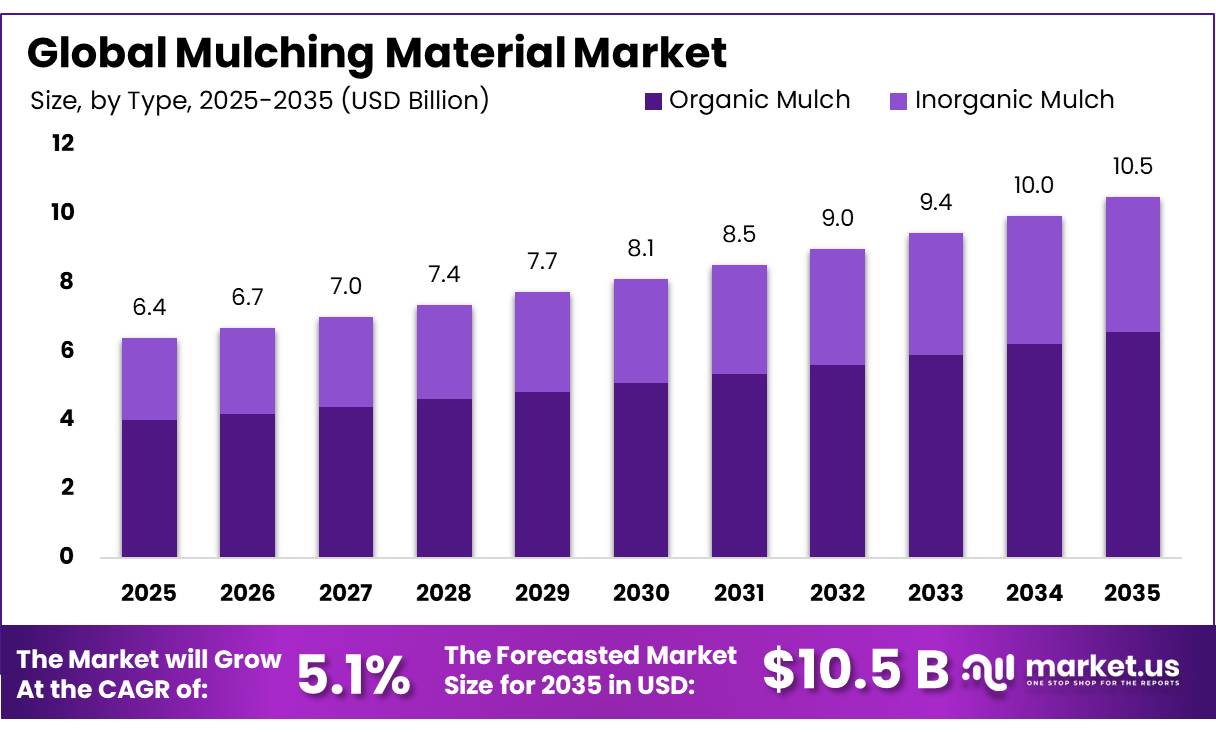

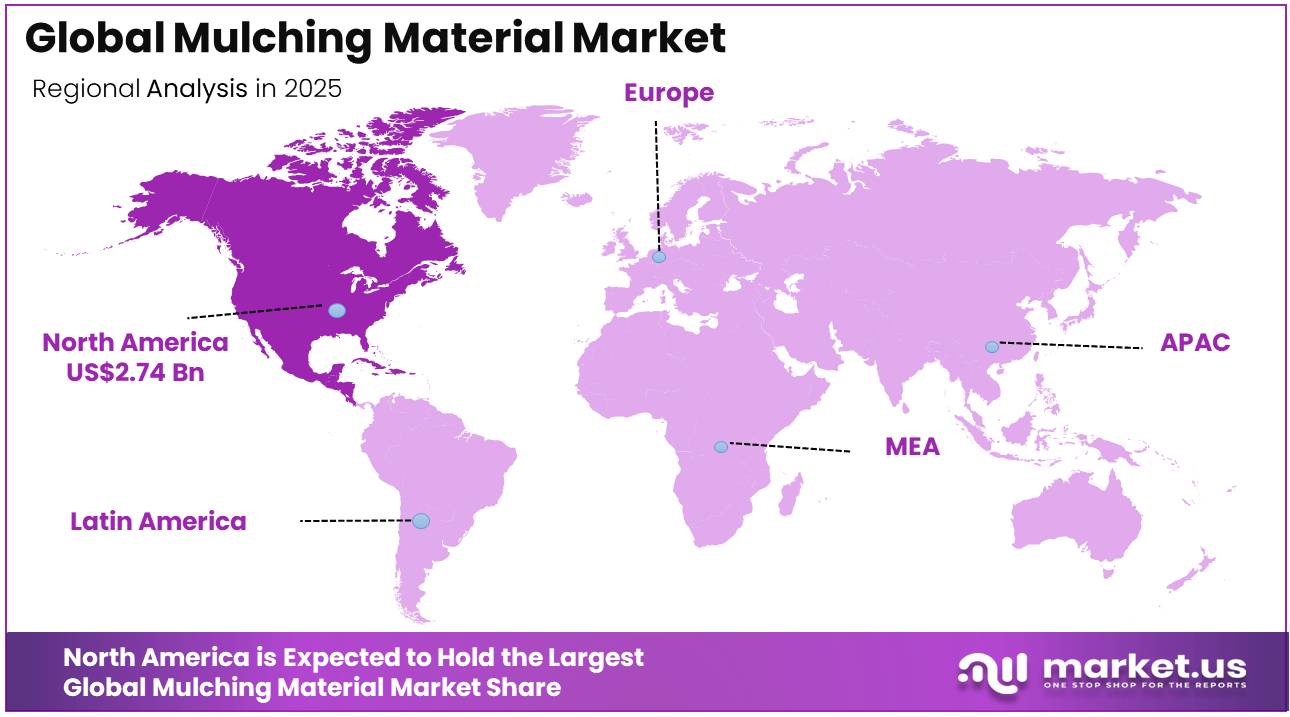

In 2025, the Global Mulching Material Market was valued at US$6.4 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.1%, reaching about US$10.5 billion by 2035. North America held a dominant market position, capturing more than a 36.2% share, holding USD 2.74 billion in revenue.

Key Takeaways

- The global mulching market was valued at US$6.4 billion in 2025.

- The market is projected to grow at a CAGR of 5.1% and is estimated to reach US$10.5 billion by 2035.

- On the basis of type, the organic mulch dominated the market, constituting 62.6% of the total market share.

- Based on the application, agriculture dominated the mulch market, with a substantial market share of around 48.2%.

- Based on the material type, wood chips led the market, comprising 32.8% of the total market.

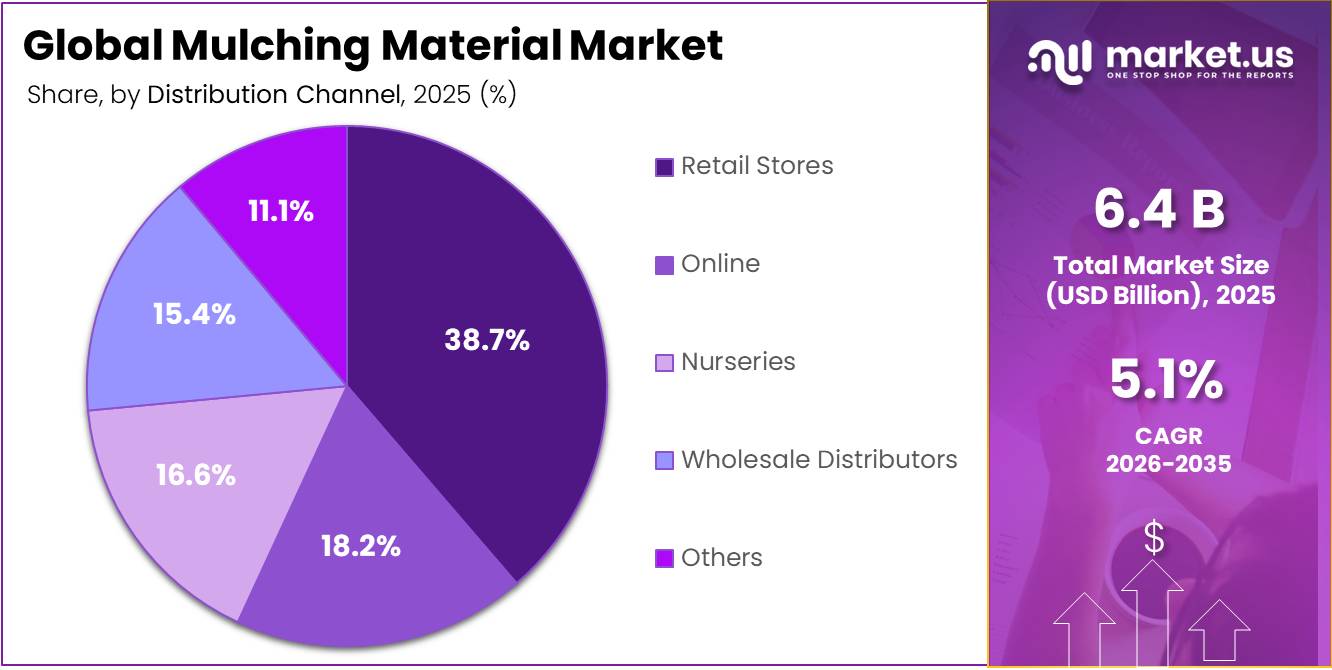

- Among the distribution channels, retail stores held a major share in the mulch market, accounting for 38.7% of the market share.

- In 2025, North America was the most dominant region in the mulch market, accounting for 36.2% of the total global consumption.

Mulching material are protective layers placed over agricultural soil to conserve moisture, regulate soil temperature, control weeds, reduce erosion, and support crop productivity. Common materials include wood chips, bark, straw, crop residues, compost, gravel, polyethylene films, paper-based sheets, and biodegradable plastic films. The U.S. Department of Agriculture states that mulch helps extend available water, suppress competing weeds, protect soil from erosion, and moderate temperature extremes. These functions make mulching important across fruit, vegetable, nursery, greenhouse, landscaping, and conservation agriculture systems.

The industry is influenced by the growing pressure on farmers to improve water efficiency and protect declining soil resources. Agriculture accounts for approximately 70% of global freshwater withdrawals, increasing the importance of farming practices that reduce evaporation and surface runoff. FAO explains that soil protected with mulch allows more rainwater to infiltrate rather than flow over the surface, thereby reducing erosion and improving moisture availability.

- According to the Food and Agriculture Organization (FAO), in its 2025 guidance on sustainable water management and mulching practices, the use of black mulch reduced irrigation water demand from 2,282.49 cubic metres under unmulched conditions to 1,878.66 cubic metres, demonstrating the material’s effectiveness in conserving soil moisture and improving irrigation efficiency. The same study recorded water-use efficiency of 14.59 kilograms per cubic metre with black mulch, compared with 8.35 kilograms per cubic metre without mulch.

FAO defines permanent organic soil cover as one of the three main principles of conservation agriculture and recommends that crop residues or cover crops protect at least 30% of the soil surface. In the United States, organic materials such as food, yard trimmings, wood, paper, and paperboard represent around 51.4% of municipal solid waste placed in landfills. This creates a sizeable feedstock opportunity for compost, shredded wood, bark, and other recycled organic mulches. The U.S. Environmental Protection Agency reported that 66.2 million tons of wasted food were generated across retail, food service, and residential activities in 2019, while only 5% was composted. Greater composting capacity could therefore expand the supply of low-cost organic mulching inputs.

Future growth opportunities are expected to emerge from biodegradable films, recycled organic materials, precision irrigation, and climate-smart farming. Conventional polyethylene films offer reliable weed and moisture control but can create collection costs and persistent plastic residues. The European Commission is consequently encouraging clear sustainability standards for bio-based, biodegradable, and compostable plastics, while stressing that their complete environmental life cycle must be assessed.

Type Analysis

Organic Mulch Type represents dominant Segment in the Market.

Organic mulch represents the dominant segment in the mulching material market, accounting for 62.6% of global share. When organic materials decompose on the soil surface, they do not just protect they feed. Bacteria, fungi, and other soil microorganisms break down wood chips, straw, and compost into compounds that build aggregate structure, cycle nutrients, and build long-term fertility. Research comparing organically managed soils with those under synthetic fertilizer found that microbial biomass carbon increased by 40 percent and microbial biomass nitrogen by 55 percent in the organically managed plots a difference that compounds over growing seasons.

- According to the Food and Agriculture Organization (FAO), 2024, compost-based organic soil inputs can improve soil health by up to 31%, increase water-holding capacity by 35–57%, and boost crop yields by up to 25%, supporting the growing adoption of organic mulch materials, particularly compost-based mulches, in moisture-sensitive farming systems.

Inorganic mulch, delivers immediate agronomic benefits in weed control and temperature management but contributes nothing to the soil food web. This biological limitation is increasingly difficult to justify as farming systems globally shift toward regenerative models that measure soil carbon and microbial diversity as core productivity indicators a shift that structurally favors organic mulch’s continued market leadership

Application Analysis

Mulching Material Are Most Widely Used Across Agricultural Applications

In 2025, the agriculture segment accounted for a leading 48.2% share in the mulching material market. Farmers across the world are under growing pressure to produce more with less water, fewer chemicals, and healthier soils and mulching directly addresses all three. In India, ICAR’s National Innovations in Climate Resilient Agriculture programme, running across 151 climatically vulnerable districts, has officially built in-situ moisture conservation and mulching into its prescribed farming practices, giving government weight to what has long been field-level knowledge.

Landscaping, supported by consistent demand across North American and European residential, commercial, and municipal projects where wood chip and bark mulches are standard around ornamental plantings and public green spaces. Erosion control accounts for the remaining 14.3%, a smaller portion, but one that holds steady importance in infrastructure development and land rehabilitation work, particularly in fast-urbanising regions.

Material Type Analysis

Wood Chips Are the Most Widely Used Material

In 2025, wood chips led the mulching material market by material type, capturing a 32.8% share due to their unmatched combination of wide regional availability, cost-effectiveness, and proven agronomic performance across diverse soil and climate conditions. Their dominance is supported by the fact that wood chips are generated as a byproduct of timber processing, urban tree maintenance, and forestry operations, allowing supply to expand alongside existing industrial activity rather than relying on dedicated manufacturing.

- According to the U.S. Department of Agriculture (USDA) Agricultural Research Service (ARS), a three-year study highlighted in October 2024 found that applying wood-chip mulch at depths of 5–10 cm significantly reduced weed growth compared with unmulched soil or soil covered with only 5 cm of mulch.

Under EN 17033, certified soil-biodegradable mulch films must demonstrate complete biodegradation of a minimum of 90 percent into carbon dioxide within two years, while also passing ecotoxicity testing that confirms no acute harm to soil invertebrates a rigorous bar that separates credible products from greenwashing claims and gives buyers, regulators, and organic certifiers a reliable procurement reference point.

Distribution Analysis

Retail Stores Held a Major Share of the Mulching Material Market.

Retail stores account for 38.7% of mulching material sales globally, making them the single largest distribution channel. This reflects something fairly fundamental about how most buyers whether homeowners, landscapers, or small farmers actually shop for these products. Garden centres, hardware chains, and agricultural supply stores offer immediate access, product visibility, and staff guidance that online platforms cannot fully replicate, particularly for buyers who want to see and feel what they are purchasing before committing.

Nurseries function as a complementary outlet, typically serving customers who are already buying plants and want matching mulch. Wholesale distributors handle bulk movement of straw, wood chips, and agricultural film mulches to commercial farms and large landscaping contractors. Online is the fastest-growing channel without question agricultural e-commerce is expanding quickly across Asia-Pacific and Latin America, and direct-to-farmer digital platforms are making specialty biodegradable mulches accessible to smallholders who previously could not source them locally.

Key Market Segments

By Type

- Organic Mulch

- Inorganic Mulch

By Application

- Agriculture

- Landscaping

- Erosion Control

By Material Type

- Wood Chips

- Bark

- Compost

- Straw

- Plastic

By Distribution Channel

- Online

- Retail Stores

- Nurseries

- Wholesale Distributors

Driver Analysis

Water-stress yield protection in irrigated horticulture

FAO-linked field evidence shows ginger reached 32 t/ha under drip plus plastic mulch, while the same study recommended 80% of estimated crop-water application with mulch at 267.4 mm as a higher-productivity operating point, indicating that mulch is not merely an input add-on but a water-productivity tool that can shift grower ROI even before seed, fertigation, and labor savings are counted.

In pineapple, FAO AGRIS records show mulched groundcover maintained soil-water availability at least around 80% through the crop cycle, versus 15% to 70% without mulch, and reported irrigation water productivity of 667.12 kg mm−1 ha−1 with a 109.0 L kg−1 water footprint in the best-performing configuration, reinforcing why mulching demand is strongest in water-constrained horticulture corridors rather than broad-acre grains.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-stress yield protection in irrigated horticulture | +1.6% | APAC corridors, North America core, MENA, South America spill-over | Short term (≤ 2 years) |

| Soil-moisture retention and irrigation productivity gains | +1.3% | India, China, U.S. West, Mediterranean EU, Brazil | Short term (≤ 2 years) |

| Biodegradable mulch qualification under soil-plastics regulation | +1.1% | EU core, North America premium crops, Japan, South Korea | Medium term (2-4 years) |

| Disposal cost and collection friction for conventional plastic films | +0.9% | EU, U.S., Canada, Australia | Medium term (2-4 years) |

| Labor substitution through weed suppression and field-pass reduction | +0.8% | North America, EU, high-wage APAC, Gulf greenhouse clusters | Short term (≤ 2 years) |

| Protected cultivation and high-value crop intensity | +1.0% | China, India, Spain, Italy, Mexico, Türkiye | Medium term (2-4 years) |

Restraint Analysis

Plastic waste recovery cost

Conventional mulch film economics remain structurally constrained by end-of-life recovery, because official and university-linked U.S. analysis of agricultural mulch disposal shows that used film often exits the field with heavy contamination and, in a 2025 U.S. agriculture plastic-footprint study, mulch film at end-of-life can contain roughly 60% to 80% adhered soil by mass, which destroys recyclability, inflates freight on low-value waste streams, and pushes cleaning and handling costs above the recovered resin value in many local markets.

The strategic effect is margin compression for suppliers trying to preserve price parity with bare-soil or organic mulches, slower replacement demand where disposal is unpopular, and delayed municipal or cooperative procurement of collection infrastructure, supporting an estimated 1.2 percentage-point CAGR drag through short-term adoption friction across North America, the EU, China, and India.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organic compliance gap | -1.4% | North America core, EU organic belts | Medium term (2-4 years) |

| Plastic waste recovery cost | -1.2% | North America core, EU, China, India | Short term (≤ 2 years) |

| Resin price pass-through | -1.0% | EU, North America core, APAC import corridors | Short term (≤ 2 years) |

| Standards and certification friction | -0.9% | EU, EEA, export-oriented APAC suppliers | Medium term (2-4 years) |

| Trade-duty and import exposure | -0.8% usitc | North America import channels, Asia supply hubs | Medium term (2-4 years) |

| Farm labor and application costs | -0.7% | U.S., Canada, labor-tight horticulture zones | Short term (≤ 2 years) |

Opportunity Analysis

Certified biodegradable mulch conversion

This is an opportunity rather than a baseline driver because conventional mulch demand is already embedded in current vegetable and specialty-crop acreage, whereas the upside comes from converting incumbent polyethylene users into higher-value certified biodegradable systems that solve future compliance and residue-removal pain points in regulated channels; USDA’s organic rule already defines technical thresholds for biodegradable biobased mulch, including at least 90% soil biodegradation within two years and recognized compostability/biobased standards, creating a standards-backed premiumization pathway rather than merely sustaining current volume demand.

The monetizable white space is amplified by the EU’s expansion to 16.9 million hectares of organic area in 2022, equal to 10.5% of total agricultural land, alongside continued growth in high-value fruit and vegetable production globally to 2.1 billion tonnes in 2023, which supports a realistic strategy where suppliers convert even 6% to 9% of existing premium horticulture mulch users to biodegradable grades at 1.4x to 2.0x average selling prices, lifting category revenue growth by about 2.4 percentage points through mix expansion, lower removal labor costs, and margin improvement that can plausibly reach 300 to 600 basis points for integrated players with in-house certification and resin formulation capabilities.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Certified biodegradable mulch conversion | +2.4% | EU, North America core, Japan, South Korea | Short term (≤ 2 years) |

| Recycling-led closed-loop ag-plastics platforms | +1.9% | North America core, EU, Australia | Short term (≤ 2 years) |

| Smallholder horticulture penetration packs | +2.1% | India, Southeast Asia, Africa emerging markets | Medium term (2-4 years) |

| Orchard and perennial crop white-space expansion | +1.6% | Mediterranean EU, U.S., China, Turkey, India | Medium term (2-4 years) |

| Protected cultivation systems bundling | +2.0% | China, India, Spain, Mexico, Middle East | Medium term (2-4 years) |

| Bio-based resin integration and carbon premium models | +1.4% | EU, North America, selected APAC premium markets | Long term (≥ 4 years) |

Challenges Analysis

Fragmented agri logistics

Chronic fragmentation in agricultural logistics creates a structural drag on mulching material deployment by increasing end‑to‑farmgate lead times by 3–7 days and inflating delivered costs by an estimated 6–12% in key Asia and Africa production corridors, where cold‑chain and storage deficits result in post‑harvest losses of around 20–30% for perishables and crowd out capital for on‑farm inputs such as mulch films and organic mulches.

Government assessments of food supply chains in India and other developing markets highlight under‑investment in rural roads, packhouses, and last‑mile distribution, with utilization rates of existing logistics assets still below 60–70% in many districts, forcing mulching suppliers to operate high‑variability distribution networks with standard deviation in monthly offtake often exceeding 15–20% compared with 5–8% in more integrated North American or EU markets.

This volatility raises working capital requirements by an estimated 10–15% for distributors and encourages smaller inventory buffers at the rural retailer level, which in turn leads to stock‑out rates of 8–12% during peak planting windows, effectively trimming potential annual mulching adoption growth by roughly 0.8 percentage points relative to a fully optimized logistics baseline.

Strategically, leading firms must respond by co‑investing with governments and development agencies in hub‑and‑spoke distribution, deploying route‑to‑market digitization to reduce order‑to‑delivery variance by at least 1–2 days, and experimenting with micro‑warehousing and regional manufacturing cells that cut average haul distance by 50–150 km, thereby narrowing the delivered cost penalty to under 5% and stabilizing service levels across dispersed smallholder clusters.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Fragmented agri logistics | -0.8% | Asia & Africa corridors | Long term (≥ 4 years) |

| Plastic waste compliance risk | -0.7% | EU & high-reg markets | Medium term (2–4 years) |

| Biodegradable tech cost gap | -0.6% | North America & EU | Long term (≥ 4 years) |

| Farmer adoption capability gap | -0.9% | Emerging smallholder belts | Medium term (2–4 years) |

| Recycling & EoL bottlenecks | -0.7% | North America & EU | Long term (≥ 4 years) |

| Input price & water stress | -0.5% | Global arid & semi-arid | Medium term (2–4 years) |

Geopolitical Impact Analysis

Active Conflict Disruption to Petrochemical Raw Material Supply Chains

Geopolitical tensions are creating new cost and supply risks for conventional mulch film producers. Conflict-related disruptions have affected petrochemical raw materials used in polyethylene and polypropylene-based mulch films. The reported strike on the Stavrolen petrochemical plant in Russia in November 2025 disrupted a key production source for polyethylene, polypropylene, and petroleum resins, adding pressure to European-adjacent supply chains.

Feedstock instability has also increased due to conflict in the Middle East, a region that accounts for a large share of global polyethylene exports. Reduced availability of polyethylene supply and sharp increases in European wholesale plastics prices have raised input costs for mulch film manufacturers. These pressures are supporting faster interest in bio-based, biodegradable, and locally sourced Mulching Material as more resilient alternatives.

Regional Analysis

North America Held the Largest Share of the Mulching Material Market

North America held a dominant position in the Mulching Material market, accounting for 36.2% of the global share. This leadership can be attributed to the widespread use of mulching across commercial farming, residential landscaping, nursery operations, and municipal land management. The most significant regional growth dynamic, however, is playing out in Asia-Pacific, where protected cultivation is expanding rapidly and pulling mulching material demand with it.

- India’s Mission for Integrated Development of Horticulture has facilitated a total investment of ₹2,963.91 crore into protected cultivation projects, with a dedicated allocation of ₹85 crore designated for 2025 to promote greenhouse farming across seven water-stressed states directly expanding the physical area requiring mulching coverage inside tunnel and polyhouse structures.

Europe follows with steady demand anchored in established horticultural clusters across the Netherlands, Spain, and Italy. Latin America and the Middle East are earlier-stage but expanding, as protected cultivation gains momentum in Egypt, Saudi Arabia, and Colombia, regions where controlled environment agriculture is being used to overcome climate and water constraints and generate year-round, export-quality produce that commands the consistent crop quality that mulching systems help deliver.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Mulching material manufacturers are prioritising material innovation, biodegradability certification, and supply chain resilience to maintain competitive positioning amid tightening environmental regulations and rising sustainable agriculture adoption. A key strategic priority is the continuous development of next-generation bio-based polymer formulations including PBAT blends, PHA-based films, thermoplastic starch composites, and liquid biodegradable systems that deliver agronomic performance comparable to conventional polyethylene while satisfying soil-biodegradability standards such as EN 17033 and evolving USDA National Organic Program requirements.

Production capacity expansion across Asia-Pacific and Latin America is being pursued to align with concentrated demand from greenhouse farming, precision irrigation, and organic cultivation ecosystems. Vertical integration with biopolymer resin suppliers helps stabilise raw material access amid petroleum feedstock price volatility, while long-term supply agreements with commercial horticulture operators and government-funded farming programs reinforce customer retention across high-value protected cultivation segments.

The Major Players in The Industry

- BASF SE

- Berry Global Inc.

- Novamont S.p.A.

- BioBag International AS

- RKW Group

- Armando Alvarez Group

- AEP Industries Inc.

- Plastika Kritis S.A.

- Kingfa Sci. & Tech. Co., Ltd.

- Trioplast Industrier AB

- Ab Rani Plast Oy

- Al-Pack Enterprises Ltd.

- British Polythene Industries PLC

- Agriplast Tech India Pvt. Ltd.

- Dubois Agrinovation

- Other Key Players

Key Development

- In January 2026, Novamont renewed the visual identity of its Mater-Bi portfolio at Marca 2026, highlighting nearly 30 years of bioplastics development. In November 2025, Mater-Bi became the first soil-biodegradable mulch film certified under EU Regulation 2019/1009. The films comply with EN 17033, biodegrade in soil within about 24 months, and are supported under the 2023–2027 CAP frameworks of Spain, Portugal and Italy.

- In February 2025, BASF promoted its certified soil-biodegradable ecovio M 2351 grade for mulch films used in greenhouse fruit and vegetable cultivation. The material complies with EN 17033 and can be processed into films as thin as 8, 10 or 12 micrometres, while allowing farmers to plough the film into the soil after harvest instead of collecting conventional polyethylene waste. BASF states that the grade can support earlier harvesting, lower water use and reduced herbicide requirements across different crops and climate conditions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$6.4 Bn |

| Forecast Revenue (2035) | US$10.5 Bn |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2025 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Organic Mulch and Inorganic Mulch), By Application (Agriculture, Landscaping, and Erosion Control), By Material (Wood Chips, Bark, Compost, Straw, Plastic), By Distribution Channel (Online, Retail Stores, Nurseries, Wholesale Distributors, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BASF SE, Berry Global Inc., Novamont S.p.A., BioBag International AS, RKW Group, Armando Alvarez Group, AEP Industries Inc., Plastika Kritis S.A., Kingfa Sci. & Tech. Co., Ltd., Trioplast Industrier AB, Ab Rani Plast Oy, Al-Pack Enterprises Ltd., British Polythene Industries PLC, Agriplast Tech India Pvt. Ltd., Dubois Agrinovation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |