Global Dairy Ingredients Market Size, Share, And Industry Analysis Report By Product (Skimmed Milk Powder (SMP), Whole Milk Powder (WMP), Buttermilk Powder, Cream Powder, Blenders and Replacers, Rolled Dried Powder, Fat-filled Powder, Permeate Powder, Lactose and Derivatives, Casein and Caseinate, MPC and MPI, Whey Ingredients), By Application (Bakery and Confectionery, Dairy Products, Convenience Foods, Infant Milk Formula, Sports and Clinical Nutrition, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183533

- Number of Pages: 364

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

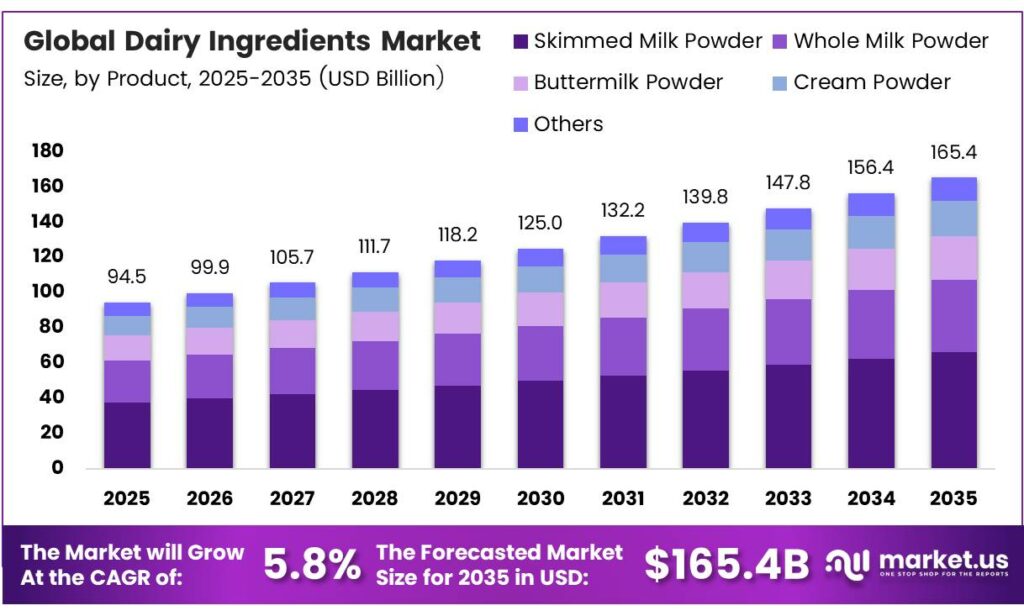

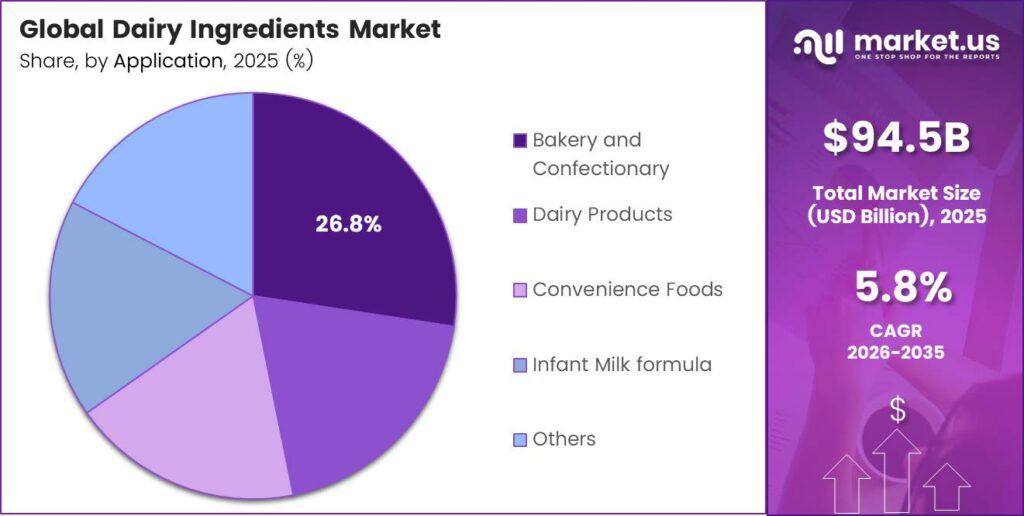

The Global Dairy Ingredients Market size is expected to be worth around USD 165.4 billion by 2035 from USD 94.5 billion in 2025, growing at a CAGR of 5.8% during the forecast period 2026 to 2035.

The dairy ingredients market covers a broad range of processed milk-derived components. These include milk powders, whey proteins, casein, lactose, and milk protein concentrates. Manufacturers supply these ingredients to food, beverage, infant nutrition, and pharmaceutical producers globally.

Dairy ingredients serve as functional building blocks in countless formulations. They provide protein enrichment, emulsification, texture enhancement, and nutritional fortification. Consequently, their role extends well beyond traditional dairy processing into specialized health and performance segments.

According to the International Dairy Foods Association, United States dairy ingredient exports reached $8.2 billion in 2024, marking the second-highest level ever recorded. This performance reflects strong global demand for whey, lactose, and milk powders, confirming the U.S. as a dominant exporter in the ingredient-linked cross-border trade ecosystem.

European Union whey powder exports reached 716,189 tonnes in 2024, keeping the bloc the second-largest whey ingredient exporter globally. This volume highlights the EU’s critical role in supplying high-protein dairy derivatives to food manufacturers in Asia, the Middle East, and the Americas.

Rising consumer awareness of protein intake and immune health fuels demand for fortified dairy derivatives. Infant formula manufacturers, sports nutrition brands, and clinical nutrition companies increasingly rely on specialized dairy ingredients. Therefore, product innovation remains a key competitive priority across the value chain.

Key Takeaways

- The Global Dairy Ingredients Market is valued at USD 94.5 billion in 2025 and is projected to reach USD 165.4 billion by 2035, growing at a CAGR of 5.8%.

- Skimmed Milk Powder (SMP) leads with a 17.3% market share in 2025.

- Bakery and Confectionery holds the largest share at 26.8% in 2025.

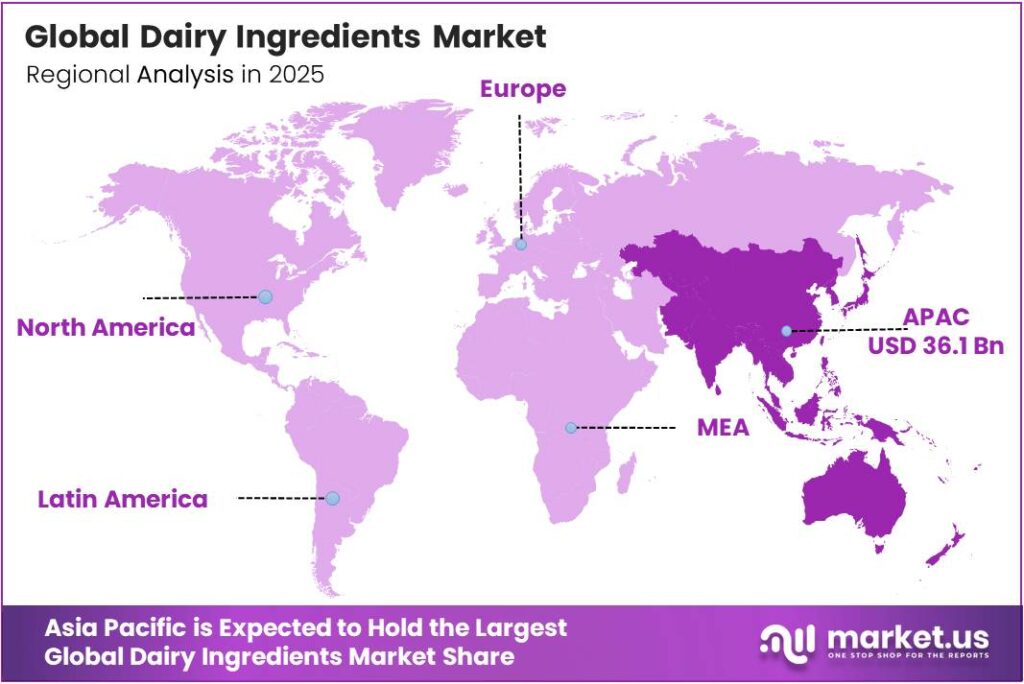

- Asia Pacific dominates the market with a 38.5% share, valued at USD 36.1 billion.

By Product Analysis

Skimmed Milk Powder (SMP) dominates with 17.3% due to its wide application in recombined dairy, bakery, and infant nutrition formulations.

In 2025, Skimmed Milk Powder (SMP) held a dominant market position in the By-Product segment of the Dairy Ingredients Market, with a 17.3% share. SMP offers long shelf life, cost efficiency, and high protein content. Moreover, its widespread use in infant formula, recombined milk, and bakery products reinforces its leading position globally.

Whole Milk Powder (WMP) serves as a full-fat dairy solution for chocolate manufacturing, beverage creamers, and convenience foods. It delivers a rich flavor profile that manufacturers in the confectionery and dessert segments specifically require. Additionally, WMP demand remains strong in Middle Eastern and African markets where fresh milk infrastructure is limited.

Buttermilk Powder and Cream Powder find strong application in bakery, soup, and sauce formulations. These ingredients contribute to texture, flavor, and fat content in processed food recipes. Consequently, food manufacturers value them as functional dairy components in both ambient and refrigerated product lines.

By Application Analysis

Bakery and confectionery dominate with 26.8% due to high consumption of dairy-enriched chocolates, ice creams, and baked goods.

In 2025, Bakery and Confectionery held a dominant market position in the By Application segment of the Dairy Ingredients Market, with a 26.8% share. This segment encompasses Chocolates, Ice Creams, and Others. Rising global chocolate and ice cream consumption drives sustained ingredient demand across this category.

Dairy Products applications include Recombinant Milk and other reformed dairy lines. These applications heavily rely on SMP, WMP, and casein derivatives for formulation. Therefore, regions with limited fresh milk access represent high-growth markets for recombined and reconstituted dairy product manufacturing.

Convenience Foods and Infant Milk Formula represent two of the fastest-growing application areas in the market. Infant formula producers demand high-purity whey proteins, lactose, and milk protein concentrates for nutritional compliance. Additionally, convenience food manufacturers integrate dairy powders for flavor, texture, and protein enrichment across ready meals and snacks.

Key Market Segments

By Product

- Skimmed Milk Powder (SMP)

- Whole Milk Powder (WMP)

- Buttermilk Powder

- Cream Powder

- Blenders and Replacers

- Rolled Dried Powder

- Fat-filled Powder

- Permeate Powder

- Lactose and Derivatives

- Casein and Caseinate

- MPC and MPI

- Whey Ingredients

By Application

- Bakery and Confectionery

- Chocolates

- Ice Creams

- Others

- Dairy Products

- Recombinant Milk

- Others

- Convenience Foods

- Infant Milk Formula

- Sports and Clinical Nutrition

- Others

Emerging Trends

Functional Ingredients and Clean-Label Formulations Reshape Dairy Derivatives

Manufacturers increasingly incorporate probiotics, lactoferrin, collagen, and fiber into next-generation dairy ingredient blends. Consumers demand clean-label, lactose-free, and fortified options that align with health and transparency preferences. Asia-bound U.S. low-protein whey exports increased 13% year over year in late 2025, confirming strong functional dairy ingredient growth in emerging markets.

Sports Nutrition and GLP-1 Solutions Drive Specialty Dairy Demand

Whey and casein proteins dominate sports nutrition formulations due to their superior amino acid profiles and digestibility. Additionally, dairy ingredient developers now create tailored solutions for consumers using GLP-1 weight loss medications. This shift toward therapeutic and performance-driven applications opens a new premium segment for high-protein dairy derivatives.

Drivers

Protein-Enriched Food Demand and Infant Nutrition Growth Accelerate Ingredient Uptake

Global consumer preference for high-protein functional foods and beverages drives sustained dairy ingredient demand. Infant nutrition manufacturers and clinical dietary formulators rely on precise dairy proteins for product compliance. The United States whey protein concentrate production totaled 495 million pounds in 2024, confirming the U.S. as the world’s largest high-protein whey ingredient manufacturing base. Additionally, U.S. lactose export shipments rose 5% year over year in late 2025, driven by expanding infant formula and sports nutrition applications.

Technological Innovation and Government Policies Expand Market Reach

Advanced membrane filtration and fractionation technologies enhance specialty ingredient yields, making premium isolates more commercially viable. Strong government subsidies and export support programs accelerate dairy production in emerging regions. Consequently, these policies improve raw material availability and lower production costs, enabling ingredient suppliers to scale operations and meet growing global demand efficiently.

Restraints

Lactose Intolerance and Milk Allergies Limit Market Penetration

Widespread lactose intolerance and milk protein allergies restrict the broader adoption of conventional dairy ingredients across key consumer segments. Manufacturers face product reformulation costs to address dietary restrictions. The United States lactose production reached 91.7 million pounds in November 2024, yet demand growth faces headwinds from expanding lactose-free and plant-based alternatives in retail channels.

Plant-Based Competition Intensifies Pressure on Dairy Ingredient Suppliers

Plant-based proteins, oat-derived components, and soy isolates increasingly compete with dairy derivatives in food and beverage formulations. Manufacturers of bakery, beverage, and snack products actively seek cost-competitive non-dairy alternatives. Therefore, dairy ingredient suppliers must invest in product differentiation, clean-label credentials, and functional performance to retain formulator preference against growing plant-based substitution pressure.

Growth Factors

Functional Supplement Integration and Premium Isolate Markets Unlock New Revenue Streams

Dairy ingredient suppliers expand into weight management, immunity-boosting, and performance supplement categories. Customized dairy powders for bakery, confectionery, and convenience food sectors attract long-term supply contracts. United States lactose production reached 100 million pounds in May 2025, up 1.7% year over year, reflecting stable demand across infant formula, pharmaceutical excipient, and sports nutrition channels. Moreover, EU skim milk powder exports totaled 208,569 tonnes in 2024, supporting global ingredient supply diversification strategies.

Advanced Separation Technologies and Asia-Pacific Urbanization Drive Expansion

Membrane separation and ultrafiltration advancements unlock premium whey isolate and caseinate markets. These technologies improve ingredient purity while reducing processing costs. Additionally, rapid urban population growth and rising health awareness across Asia-Pacific economies fuel sustained dairy ingredient uptake. Furthermore, U.S. milk protein concentrate exports rose 52% year over year in late 2025, led by strong MENA demand, confirming the global geographic expansion of ingredient trade.

Regional Analysis

Asia Pacific Dominates the Dairy Ingredients Market with a Market Share of 38.5%, Valued at USD 36.1 Billion

Asia Pacific commands the largest share of the global dairy ingredients market, holding 38.5% of the total market value at USD 36.1 billion in 2025. Rapid urbanization, growing middle-class populations, and rising awareness of functional nutrition drive sustained demand. China, India, Japan, and Australia collectively absorb significant volumes of whey proteins, milk powders, and infant formula ingredients.

North America holds a strong second position in the global dairy ingredients market, driven by the United States’ world-leading whey protein manufacturing capacity. The U.S. recorded dairy ingredient exports of $8.2 billion in 2024, with Mexico and Canada as the top destinations. Additionally, domestic demand for sports nutrition, infant formula, and clinical nutrition ingredients supports robust ingredient production volumes across the region.

Europe maintains a significant share of global dairy ingredient trade, anchored by its large-scale milk production base across Germany, France, the Netherlands, and Ireland. The EU remains the second-largest whey powder exporter globally. Furthermore, in Q3 2025, European Union milk deliveries increased 2.3% year over year, expanding the raw material pool available for whey and milk powder ingredient conversion and downstream processing capacity.

Latin America shows moderate growth in dairy ingredient consumption, supported by Brazil and Mexico’s large food processing sectors. Regional manufacturers use imported milk powders and whey derivatives for bakery, beverage, and convenience food applications. Additionally, improving cold chain logistics and rising disposable incomes in urban areas across the region support gradual growth in premium dairy ingredient adoption.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Fonterra Co-Operative Group Limited operates as one of the world’s largest dairy ingredient exporters, headquartered in New Zealand. The company supplies a comprehensive range of milk powders, whey proteins, and casein products to global food manufacturers. Fonterra’s vertically integrated supply chain and extensive global distribution network enable consistent ingredient quality and large-volume delivery capabilities across key markets.

FrieslandCampina is a Netherlands-based dairy cooperative that produces a diverse portfolio of dairy ingredients, including whey derivatives, lactose, and specialized nutritional ingredients. The company serves infant nutrition, sports performance, and pharmaceutical sectors through dedicated ingredient brands. Its research and development capabilities continuously advance ingredient functionality and nutritional performance for industrial food and beverage clients.

Arla Food Ingredients, a division of Arla Foods, specializes in high-value dairy-based ingredients such as whey protein isolates, lactoferrin, and alpha-lactalbumin. The company focuses on science-backed nutritional solutions for infant formula, clinical nutrition, and sports supplement markets. Arla Food Ingredients invests significantly in processing technology to deliver premium-grade functional dairy derivatives at scale.

Glanbia PLC is an Ireland-headquartered global nutrition company with a strong presence in whey protein ingredients and performance nutrition. The company’s ingredient solutions division supplies protein concentrates, isolates, and hydrolysates to sports nutrition brands and clinical food manufacturers. Glanbia’s global production footprint spans North America, Europe, and Asia, supporting consistent ingredient supply to international formulation partners.

Top Key Players in the Market

- Fonterra Co-Operative Group Limited

- FrieslandCampina

- Arla Food Ingredients

- Glanbia PLC

- Sodiaal Group

- Dairy Farmers of America Inc.

- Saputo, Inc.

- Schreiber Foods Inc.

- Lactalis American Group, Inc.

- EPI Ingredients

Recent Developments

- In July 2025, Fonterra highlighted its role in meeting surging demand for functional dairy ingredients in Japan and South Korea. Key products include Whey Protein Isolate (WPI), Whey Protein Concentrate (WPC), and MPC, used in ready-to-mix protein powders, fortified yoghurts for medical nutrition, and sports supplements.

- In December 2025, Friesl and Campina announced the intended acquisition of Wisconsin Whey Protein Inc. (a U.S. producer of whey protein isolates and lactose ingredients for infant, medical, health, and wellness sectors). This significantly boosts whey protein capacity, strengthens its global protein position, and expands FrieslandCampina Ingredients’ presence from Europe/Asia into North America.

Report Scope

Report Features Description Market Value (2025) USD 94.5 Billion Forecast Revenue (2035) USD 165.4 Billion CAGR (2026-2035) 5.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Skimmed Milk Powder (SMP), Whole Milk Powder (WMP), Buttermilk Powder, Cream Powder, Blenders and Replacers, Rolled Dried Powder, Fat-filled Powder, Permeate Powder, Lactose and Derivatives, Casein and Caseinate, MPC and MPI, Whey Ingredients), By Application (Bakery and Confectionery, Dairy Products, Convenience Foods, Infant Milk Formula, Sports and Clinical Nutrition, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Fonterra Co-Operative Group Limited, FrieslandCampina, Arla Food Ingredients, Glanbia PLC, Sodiaal Group, Dairy Farmers of America Inc., Saputo Inc., Schreiber Foods Inc., Lactalis American Group Inc., EPI Ingredients Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Fonterra Co-Operative Group Limited

- FrieslandCampina

- Arla Food Ingredients

- Glanbia PLC

- Sodiaal Group

- Dairy Farmers of America Inc.

- Saputo, Inc.

- Schreiber Foods Inc.

- Lactalis American Group, Inc.

- EPI Ingredients

Our Clients

- 183533

- April 2026