Quick Navigation

Report Overview

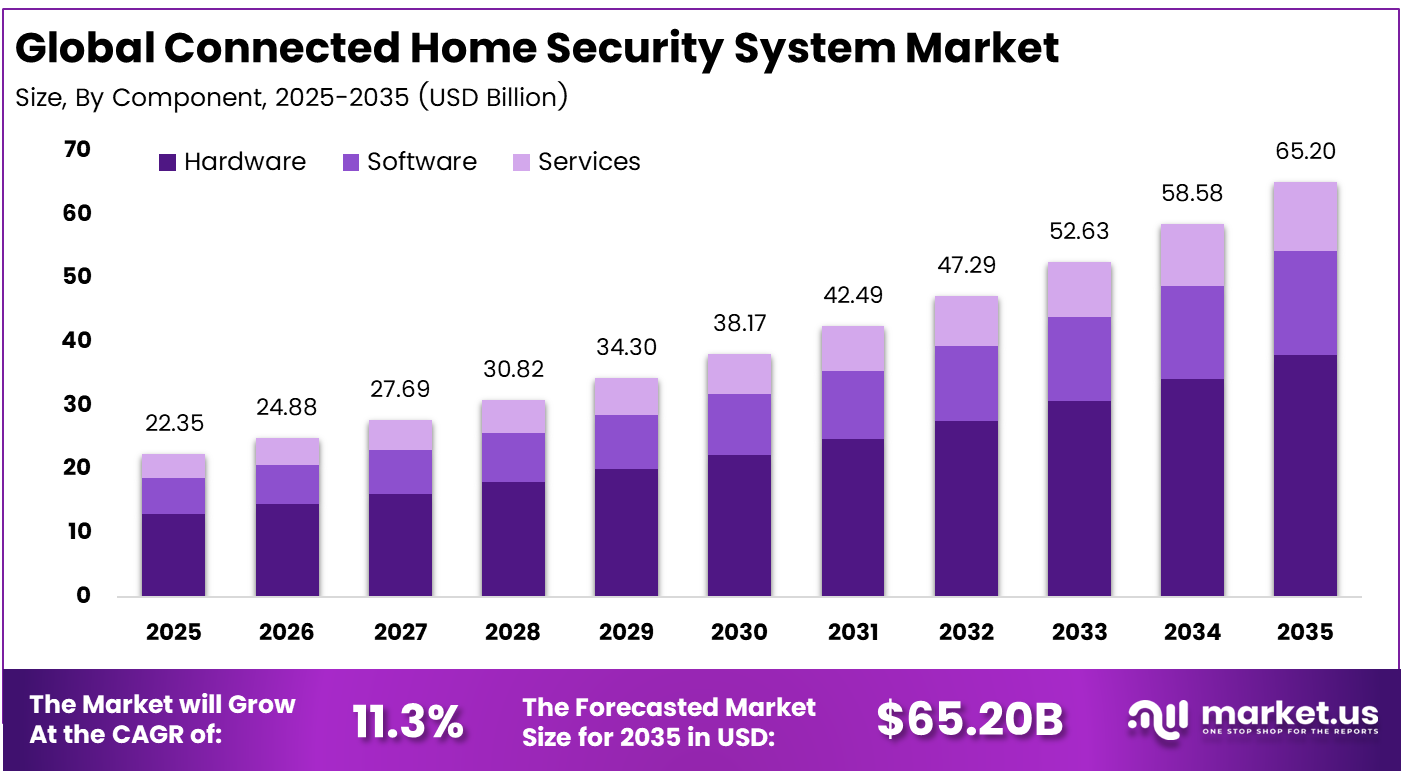

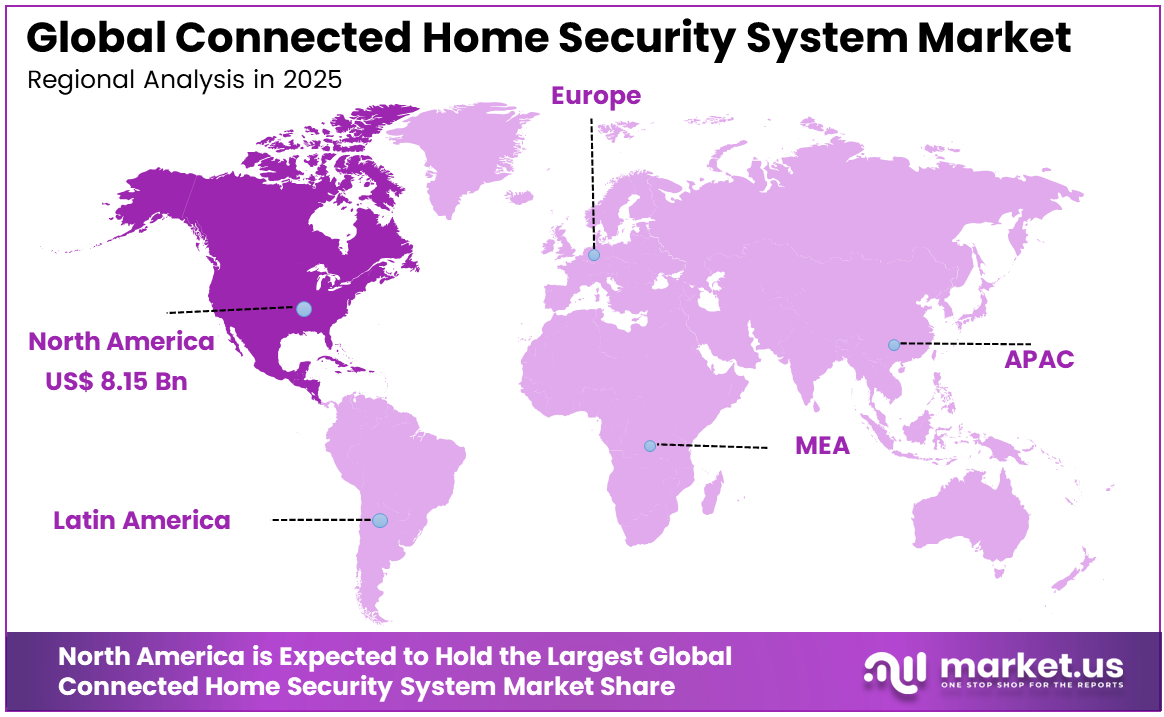

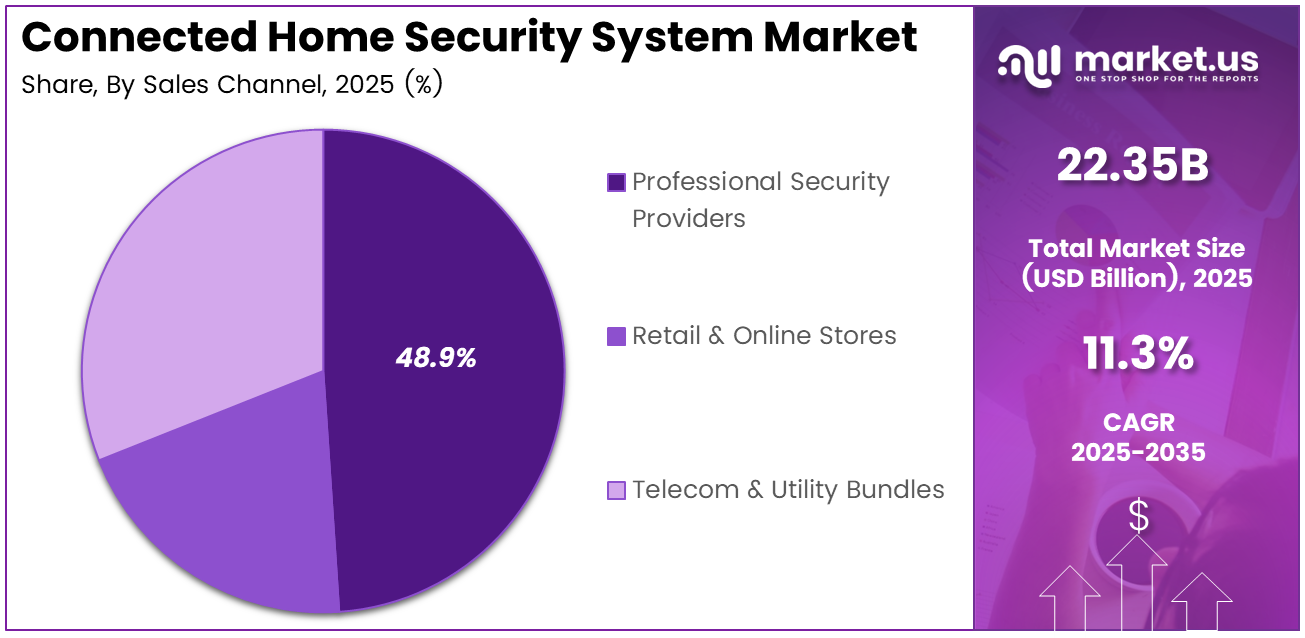

The Global Connected Home Security System Market size is expected to be worth around USD 65.20 billion by 2035, from USD 22.35 billion in 2025, growing at a CAGR of 11.3% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 36.5% share, holding USD 8.15 billion in revenue.

A connected home security system refers to a network of smart devices designed to protect residential spaces through monitoring, detection, and remote control. It usually includes cameras, sensors, alarms, locks, and mobile access features. These systems help homeowners improve safety, respond quickly to threats, and manage security more conveniently.

The growth of smart home adoption continues to support connected security solutions, supported by declining sensor and Wi-Fi hardware costs. High-speed broadband now reaches over 60% of households in many regions, improving reliability. At the same time, widespread smartphone use makes remote alerts, live video, and voice control easy for users.

The market for Connected Home Security Systems is driven by rising awareness of home safety and the growing use of smart devices in daily life. Consumers prefer systems that offer remote monitoring and easy control through mobile apps. Improved internet access and affordable devices are also supporting adoption, while the need for convenience and real-time alerts continues to encourage wider use across households.

Demand remains strongest in urban areas where burglary rates are several times higher than in rural regions. Apartment living increases security complexity due to shared spaces. Studies indicate that homes without protection face up to 3 times higher burglary risk, which encourages homeowners to adopt connected and monitored security systems for better safety.

For instance, in February 2026, Brinks Home Security sharpened its connected security value proposition with updated smart panels and deeper integrations with modern cameras and locks. The company is focusing on predictable monthly plans and professional installation, targeting households that feel overwhelmed by piecemeal DIY systems but still want smartphone‑centric control.

Key Takeaway

- In 2025, the Hardware segment held a dominant market position, capturing a 58.3% share of the Global Connected Home Security System Market.

- In 2025, the Professionally Monitored Systems segment held a dominant market position, capturing a 52.7% share of the Global Connected Home Security System Market.

- In 2025, the Video Surveillance Systems segment held a dominant market position, capturing a 41.6% share of the Global Connected Home Security System Market.

- In 2025, the Professional Security Providers segment held a dominant market position, capturing a 48.9% share of the Global Connected Home Security System Market.

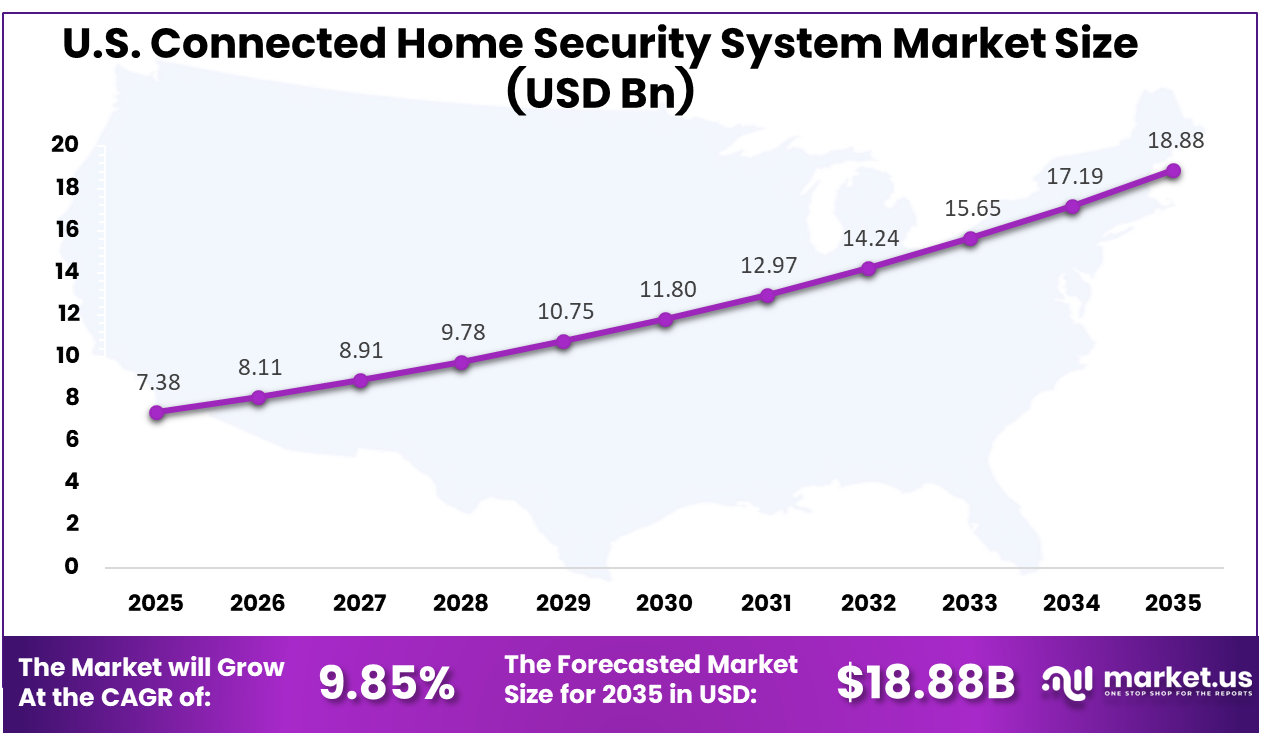

- The U.S. Connected Home Security System Market was valued at USD 7.38 billion in 2025, with a robust CAGR of 9.85%.

- In 2025, North America held a dominant market position in the Global Connected Home Security System Market, capturing more than a 36.5% share.

Role of Generative AI

Generative AI is reshaping connected home security by shifting systems from rule-based alerts to context-aware decisions. Advanced vision models have achieved detection accuracy above 90%, improving reliability. Hybrid AI and IoT setups also deliver double-digit efficiency gains, helping systems respond faster and more accurately to real-world threats.

Generative AI also supports the simulation of new attack scenarios and the creation of synthetic training data. This improves model performance based on household routines and reduces unnecessary alerts. Some deployments show that AI-based filtering can lower nuisance notifications by 40–60%, allowing users to focus only on important security events.

Investment and Business Benefits

Investment activity is expanding across hardware devices, cloud platforms, analytics software, and monitoring services. Recurring subscriptions contribute more than 50% of long-term value for providers, creating stable revenue streams. New opportunities are emerging for firms focused on cybersecurity, interoperability, and privacy, as over a third of users remain concerned about device security.

Business benefits are visible through increased service revenues and reduced operational costs using remote diagnostics. Mobile applications strengthen customer engagement as they are accessed several times per week. In addition, insurance providers in many countries offer premium discounts for certified systems, improving affordability and supporting wider adoption among homeowners.

Regional Analysis

In 2025, North America held a dominant market position in the Global Connected Home Security System Market, capturing more than a 36.5% share, holding USD 8.15 billion in revenue. This dominance is due to high smart home adoption, strong digital infrastructure, and early acceptance of connected technologies across North America. Consumers in the region show higher spending capacity and awareness of home security solutions. Widespread broadband access and smartphone usage support real-time monitoring. In addition, the presence of advanced service providers, insurance incentives, and a strong focus on safety continue to drive consistent demand and market leadership.

For instance, in July 2023, Comcast expanded its Xfinity Home Security service across additional U.S. markets, combining 24/7 professional monitoring with remote control of cameras, lights, and thermostats via broadband and mobile apps, helping cement North American leadership in converged connectivity, entertainment, and connected home security offerings.

U.S. Connected Home Security System Market Size

The market for Connected Home Security Systems within the U.S. is growing tremendously and is currently valued at USD 7.38 billion; the market has a projected CAGR of 9.85%. The market is growing due to rising concerns around home safety, increasing urban population, and higher adoption of smart home technologies across the U.S. Consumers are showing strong interest in real-time monitoring and remote access through mobile devices. Falling hardware costs and improved internet connectivity are also supporting adoption. In addition, insurance incentives and growing awareness of integrated security solutions are encouraging homeowners to invest in connected systems for better protection and convenience.

For instance, in January 2026, at CES 2026, Ring unveiled new AI‑enhanced capabilities, including Fire Watch, which analyzes camera footage for signs of smoke or fire and shares real‑time incident data via the Neighbors app. Ring also launched Ring Sensors, a Sidewalk‑based line delivering always‑on, hub‑free protection, deepening Amazon’s dominance in U.S. connected home security.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Component Analysis

In 2025, the Hardware segment held a dominant market position, capturing a 58.3% share of the Global Connected Home Security System Market. This dominance is due to the essential role of physical devices in any home security setup. Cameras, sensors, locks, and control units form the base layer of protection. Without these elements, advanced features cannot function effectively, making hardware the first and most important investment for homeowners seeking reliable security solutions.

Hardware also continues to improve in design, ease of use, and connectivity. Many devices now support simple installation and integration with mobile apps. As consumers focus on visible and tangible protection, demand for dependable equipment remains strong, supporting steady adoption across both new and existing smart home environments.

For instance, in April 2024, ADT continued rolling out its ADT+ platform, bringing more of its sensors, cameras, and control panels into a single, app-centric experience. The focus is on smoother installation, better device interoperability, and stronger remote management for homeowners, which naturally supports higher demand for connected hardware in the home security space.

System Type Analysis

In 2025, the Professionally Monitored Systems segment held a dominant market position, capturing a 52.7% share of the Global Connected Home Security System Market. This dominance is due to the preference for expert-managed security services among homeowners. Professionally monitored systems provide continuous oversight, ensuring alerts are handled quickly and correctly. This reduces the burden on users and offers reassurance, especially for families seeking dependable support during emergencies or uncertain situations.

In addition, these systems offer guided installation and ongoing service, which simplifies the overall experience. Users benefit from expert setup and reliable monitoring without needing technical knowledge. This convenience, combined with improved response coordination, continues to attract customers who prioritize safety, ease of use, and consistent system performance.

For instance, in November 2023, Comcast expanded its mix of self-setup sensors while still tying them into its professional monitoring options. Customers can start with simple door, window, and motion devices and later choose round-the-clock monitoring, which keeps professionally supervised systems attractive for people who want extra reassurance.

Product Analysis

In 2025, the Video Surveillance Systems segment held a dominant market position, capturing a 41.6% share of the Global Connected Home Security System Market. This dominance is due to the growing demand for real-time visibility within home environments. Video surveillance systems allow users to monitor activities instantly, review past events, and stay informed through mobile devices. This direct visual access makes them one of the most trusted and widely adopted security solutions in modern households.

These systems also support advanced features such as motion alerts, remote access, and smart integration. As users seek better awareness and control, cameras play a central role in daily security management. Their ability to provide clear evidence and continuous monitoring strengthens their importance across various residential applications.

For instance, in October 2024, Arlo launched a wired floodlight camera that combines bright lighting with integrated video in a single fixture. The product targets homeowners who want clear views of driveways and yards at night, showing how stronger illumination and sharper video together can drive fresh interest in camera-based home security.

Sales Channel Analysis

In 2025, the Professional Security Providers segment held a dominant market position, capturing a 48.9% share of the Global Connected Home Security System Market. This dominance is due to the trust and convenience offered by professional security providers. Many homeowners prefer complete solutions that include installation, system setup, and ongoing support. This approach reduces complexity and ensures that all components work together effectively from the beginning of the security deployment process.

Professional providers also offer maintenance, upgrades, and customer assistance, which improves long-term reliability. Users benefit from a single point of contact for all service needs. This structured support model continues to attract customers who value consistent performance, expert guidance, and a smooth overall security experience.

For instance, in February 2026, Vivint announced a dedicated program for residential builders that bundles security hardware, energy tools, and setup services into a single package. By working directly with construction partners, Vivint is helping make professionally delivered connected security the default option in many new homes rather than an afterthought.

Key Market Segments

By Component

- Hardware

- Software

- Services

By System Type

- Professionally Monitored Systems

- Self-Monitored/DIY Systems

By Product

- Video Surveillance Systems

- Access Control Systems

- Intrusion Detection Systems

- Environmental Monitoring

- Others

By Sales Channel

- Professional Security Providers

- Retail & Online Stores

- Telecom & Utility Bundles

Emerging Trends

A key trend is the integration of AI across video, access control, and environmental sensors to form a unified security system. Technologies such as facial recognition, behavior tracking, and object detection are gaining traction. More than 50% of new residential camera installations now include embedded AI analytics for improved monitoring.

Cybersecurity is advancing as more connected devices increase exposure to risks. Zero trust frameworks, encrypted communication, and secure IoT platforms are gaining adoption. Studies indicate strong growth in AI-driven cyber monitoring over the next three to five years, supported by rising concerns around data protection and connected device vulnerabilities.

Growth Factors

The increasing number of connected devices per household is a key growth driver. Cameras, smart locks, and sensors are becoming common even in mid-range homes. Adoption of smart home security is growing at high single-digit to mid-teens rates annually, supported by improved connectivity and more affordable hardware solutions.

Consumer awareness regarding safety and privacy is also strengthening demand. Many buyers now rank security among their top three priorities when selecting smart home solutions. Over 60% of users prefer systems that combine intrusion detection with privacy features such as on-device processing and encrypted data storage.

Market Dynamics

Drivers - Rising Adoption of Smart Home and IoT Devices

The growing use of smart home devices is supporting the demand for connected security systems. Households are increasingly installing smart locks, cameras, and sensors that work together through mobile apps. This shift is making security systems easier to control and more relevant for everyday home management needs.

As more devices become connected, users expect seamless integration and real-time updates. This creates a strong need for security solutions that can manage multiple devices on one platform. The convenience of automation and remote access continues to encourage homeowners to adopt connected security technologies.

For instance, in May 2025, Arlo Technologies, Inc. announced its Secure 6 service, which uses AI features like fire and advanced audio detection on top of its cameras, allowing households to connect several smart devices and manage security through the cloud, reflecting how rising camera adoption and always online homes are creating demand for more intelligent, connected protection options.

Restraint - Data Privacy Concerns

Data privacy remains a key concern as connected security systems collect sensitive information such as video footage and user behavior. Many users worry about how their data is stored and who can access it. These concerns can slow adoption, especially among individuals who are cautious about digital security risks.

In addition, the risk of unauthorized access and data misuse creates hesitation among potential buyers. If users do not trust how their data is handled, they may avoid installing connected systems. This makes privacy protection and clear data policies important for gaining consumer confidence.

For instance, in June 2025, a smart home security services analysis highlighted Ring’s introduction of more selective, AI-based alerts for deliveries and unusual events, which also raised fresh discussion about how much data the system sees. While the features improve usefulness, privacy advocates point to continuous recording and cloud analysis as reasons some users hesitate to install cameras around their homes.

Opportunities - Remote Services

Remote services are creating new opportunities in the connected home security market. Users can monitor their homes, receive alerts, and control devices from anywhere using mobile applications. This level of access improves convenience and allows homeowners to stay informed even when they are away.

Service providers are also expanding offerings such as remote troubleshooting and system updates. These features reduce the need for physical visits and improve customer experience. As more users prefer digital services, remote capabilities are expected to play a larger role in future security solutions.

For instance, in March 2026, SimpliSafe promotes self-install hardware paired with app control, optional professional monitoring, and camera recording plans, giving customers a choice between pure self-monitoring and remote staffed support, which illustrates how flexible remote services can turn basic alarm kits into ongoing protection solutions that match different comfort levels and budgets for homeowners.

Challenges - High Upfront Cost

High initial cost remains a challenge for many potential buyers. Installing a complete system with cameras, sensors, and control units can require a significant investment. This can discourage price-sensitive consumers, especially in developing markets where affordability plays a major role in purchase decisions.

In addition, ongoing costs such as maintenance and service fees can add to the financial burden. While long-term benefits are recognized, some users hesitate to commit due to immediate expenses. Reducing entry-level costs and offering flexible pricing models will be important to improve adoption across wider customer segments.

For instance, in February 2026, recent breakdowns of Xfinity Home packages show hardware kits that can cost several hundred dollars, with more sensors and cameras lifting the entry price further, and while monthly payment options exist, the figures demonstrate why some households hesitate to commit to full-featured connected security when balancing this against other home spending priorities.

Key Players Analysis

One of the leading players in December 2025, SimpliSafe expanded its DIY connected home security range with updated hubs and Wi‑Fi cameras designed for quicker self‑installation and app‑based control. The brand is doubling down on contract‑free monitoring and flexible pricing to attract renters and cost‑sensitive households moving from stand‑alone cameras to full connected alarm ecosystems.

Top Key Players in the Market

- ADT, Inc.

- Vivint Smart Home, Inc.

- SimpliSafe, Inc.

- Ring LLC (an Amazon company)

- Google LLC (Nest)

- Arlo Technologies, Inc.

- Comcast Corporation (Xfinity Home)

- Honeywell International, Inc.

- Johnson Controls International plc

- Allegion plc (Schlage)

- Assa Abloy AB (Yale)

- Frontpoint Security Solutions, LLC

- Brinks Home Security

- Scout Security, Inc.

- Canary Connect, Inc.

- Others

Recent Developments

- In January 2026, Vivint continued to push its fully integrated home platform, sharpening its pitch around a single app that manages security, energy, and automation. The firm is investing in AI‑driven video analytics and tighter device orchestration, aiming to justify premium monitoring fees in a market crowded with low‑cost connected solutions.

- In March 2026, Ring reinforced its leadership in connected home security by enhancing video doorbell and camera integration within the Amazon smart home ecosystem. New software features focus on shared accounts, neighborhood alerts, and tighter Alexa control, helping Ring defend its position as the primary security brand for over 40% of U.S. camera users.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 22.35 Billion |

| Forecast Revenue (2035) | USD 65.20 Billion |

| CAGR (2026-2035) | 11.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware, Software, Services), By System Type (Professionally Monitored Systems, Self-Monitored/DIY Systems), By Product (Video Surveillance Systems, Access Control Systems, Intrusion Detection Systems, Environmental Monitoring, Others), By Sales Channel (Professional Security Providers, Retail & Online Stores, Telecom & Utility Bundles) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ADT, Inc., Vivint Smart Home, Inc., SimpliSafe, Inc., Ring LLC (an Amazon company), Google LLC (Nest), Arlo Technologies, Inc., Comcast Corporation (Xfinity Home), Honeywell International, Inc., Johnson Controls International plc, Allegion plc (Schlage), Assa Abloy AB (Yale), Frontpoint Security Solutions, LLC, Brinks Home Security, Scout Security, Inc., Canary Connect, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |