Quick Navigation

Report Overview

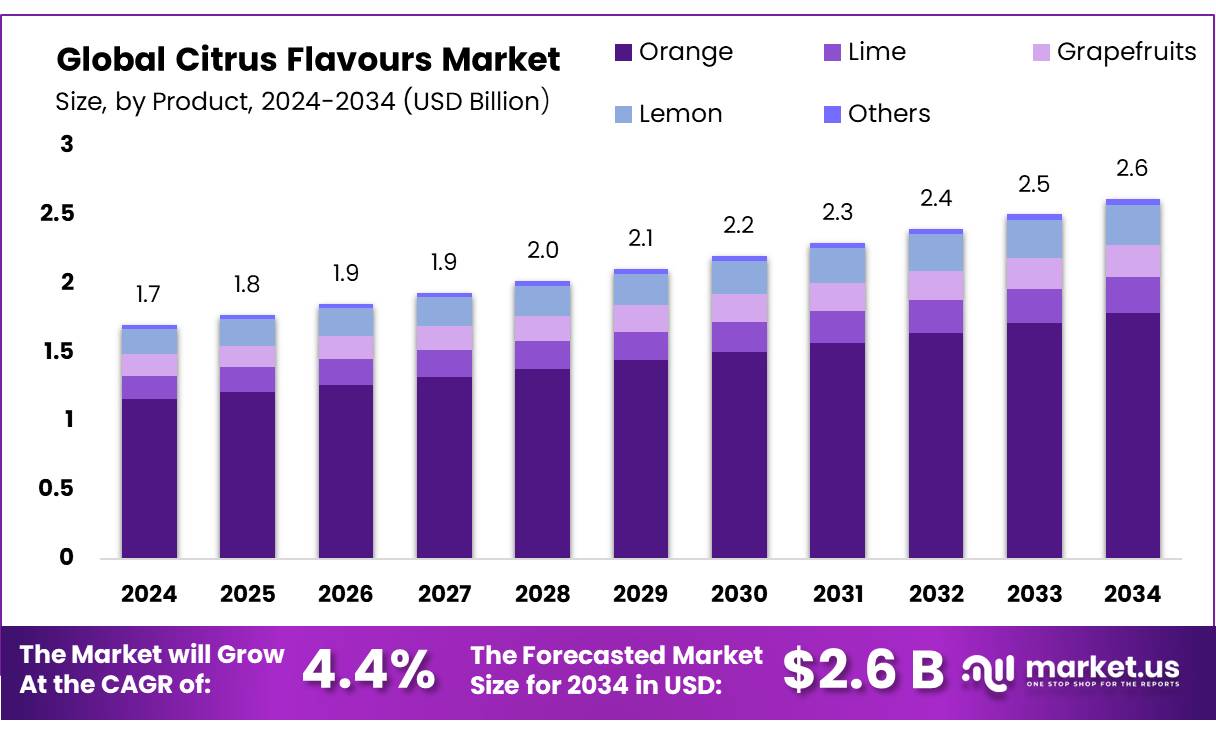

The Global Citrus Flavours Market size is expected to be worth around USD 2.6 Billion by 2034, from USD 1.7 Billion in 2024, growing at a CAGR of 4.4% during the forecast period from 2025 to 2034.

The citrus flavors concentrate industry is a pivotal segment within the global food and beverage sector, encompassing the extraction and concentration of flavors from citrus fruits such as oranges, lemons, and limes. These concentrates serve as essential ingredients in a myriad of products, including beverages, confectioneries, dairy items, and baked goods, owing to their ability to impart authentic and consistent citrus notes.

In terms of export, India has demonstrated a positive trajectory. In the fiscal year 2023-24, the country exported citrus fruits and their preparations worth approximately USD 1.44 billion, marking a 13.33% increase from the previous year. This growth underscores the expanding global demand for Indian citrus products, including concentrates.

The industry faces challenges due to environmental factors and diseases affecting citrus production. In Brazil, the world’s largest producer and exporter of orange juice, orange output is expected to hit a 30-year low in the 2024/25 season due to adverse weather conditions and the spread of citrus greening disease . Similarly, in the United States, particularly in Florida, orange production has significantly declined due to hurricanes and diseases, leading to a 28% decrease in orange juice production.

Moreover, government-backed initiatives focusing on climate-resilient agriculture and sustainable farming practices are expected to stabilize raw material availability and lower production costs over time. For instance, India’s Ministry of Agriculture launched the National Horticulture Mission, allocating US$ 50 million in 2024 to support citrus fruit growers through modern farming techniques and infrastructure development. These initiatives will strengthen the industry’s supply chain resilience and promote environmental sustainability, underpinning long-term growth in the citrus flavors and concentrates market.

Key Takeaways

- Citrus Flavours Market size is expected to be worth around USD 2.6 Billion by 2034, from USD 1.7 Billion in 2024, growing at a CAGR of 4.4%

- Orange held a dominant market position, capturing more than a 68.4% share of the global citrus flavours market.

- Liquid held a dominant market position, capturing more than a 52.2% share of the global citrus flavours market.

- Natural held a dominant market position, capturing more than a 69.8% share of the global citrus flavours market.

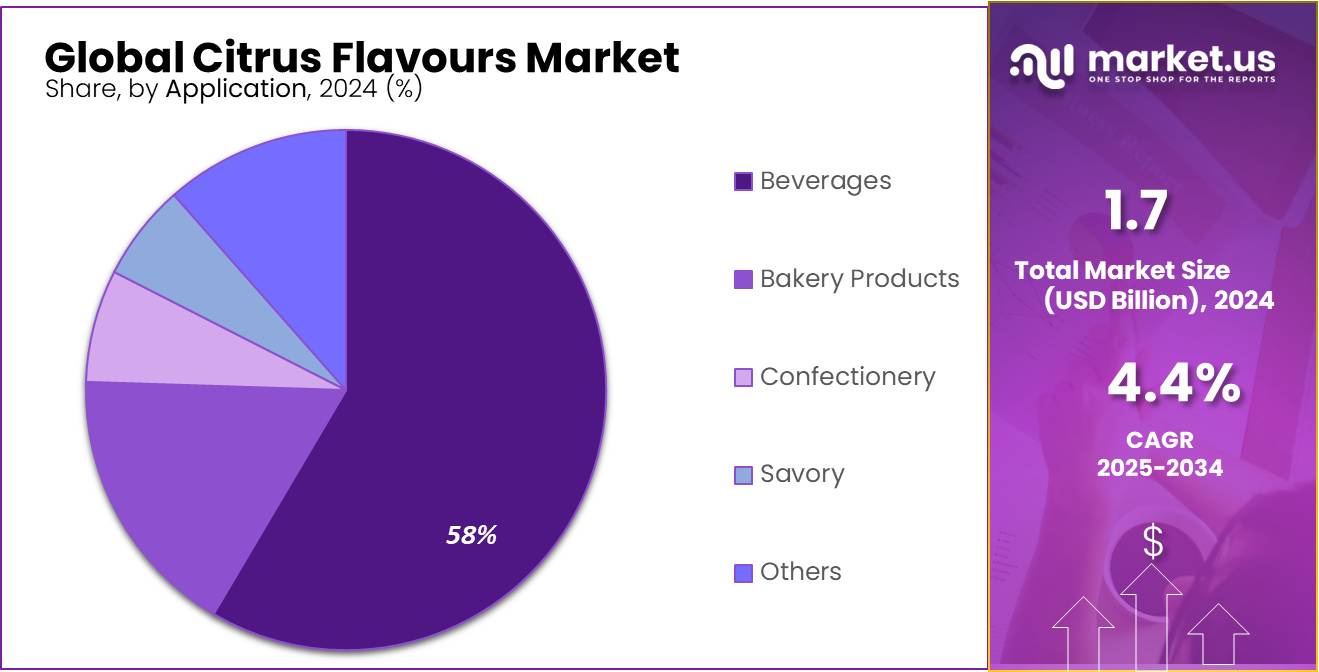

- Beverages held a dominant market position, capturing more than a 58.5% share.

- Supermarkets held a dominant market position, capturing more than a 37.3% share of the global citrus flavours market.

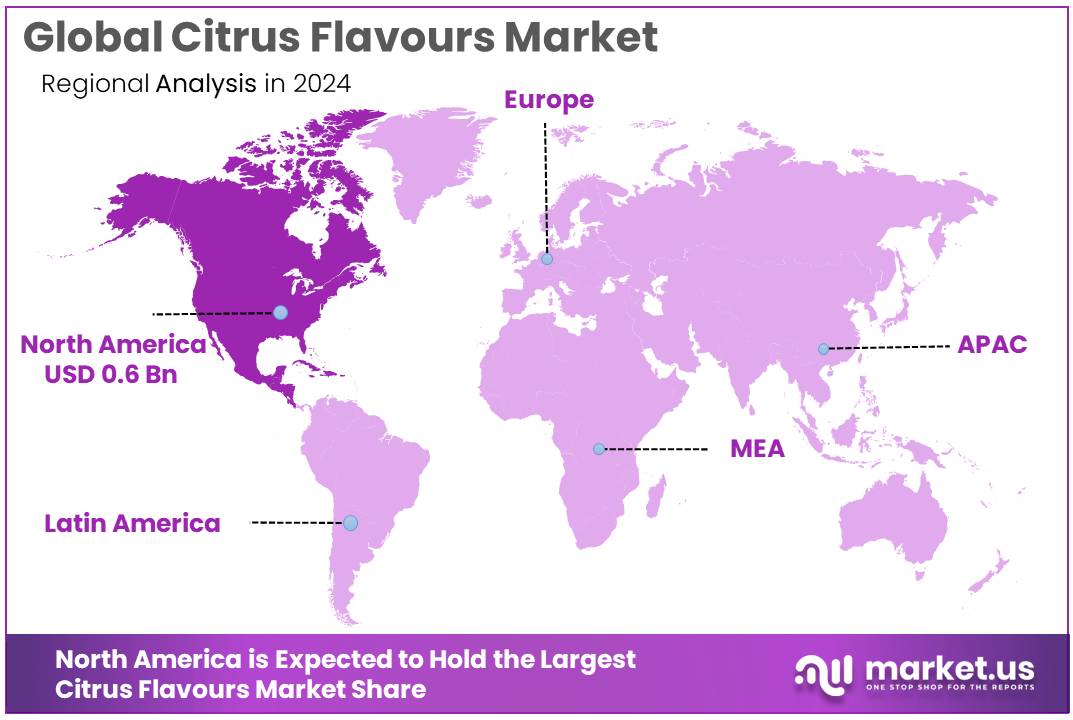

- North America held a dominant market position in the global citrus flavours market, capturing more than a 39.5% share, equivalent to approximately USD 0.6 billion.

By Product

Orange dominates with 68.4% in 2024, driven by global preference for classic citrus taste.

In 2024, Orange held a dominant market position, capturing more than a 68.4% share of the global citrus flavours market. This strong lead is largely due to orange’s universal acceptance across both food and beverage categories. Whether it’s soft drinks, juices, candies, or baked goods, orange remains the go-to flavour for both manufacturers and consumers seeking freshness, familiarity, and a sweet-tart profile that appeals to all age groups.

By Form

Liquid form dominates with 52.2% in 2024, thanks to its ease of blending in food and beverage applications.

In 2024, Liquid held a dominant market position, capturing more than a 52.2% share of the global citrus flavours market by form. This leading position can be credited to the flexibility and convenience liquid flavours offer, especially for manufacturers in the beverage, dairy, and confectionery sectors. Liquid citrus flavours are easy to mix, measure, and process, making them a preferred option for both small-scale artisans and large food and drink producers.

By Nature

Natural citrus flavours lead with 69.8% in 2024, fueled by rising clean-label demand and health-conscious choices.

In 2024, Natural held a dominant market position, capturing more than a 69.8% share of the global citrus flavours market by nature. This strong preference reflects the growing consumer shift toward clean-label products, where ingredients that are perceived as natural, safe, and health-friendly are increasingly favored. Natural citrus flavours, often derived directly from fruits like oranges, lemons, and limes, are seen as a healthier and more authentic choice compared to synthetic alternatives.

By Application

Beverages take the lead with 58.5% in 2024, driven by growing demand for refreshing and functional drinks.

In 2024, Beverages held a dominant market position, capturing more than a 58.5% share of the global citrus flavours market by application. The strong presence of citrus in this category is no surprise, as citrus profiles—especially orange, lemon, and lime—are widely associated with freshness, hydration, and revitalization. These attributes make citrus flavours a natural fit for juices, carbonated drinks, flavored waters, energy drinks, and even alcoholic beverages.

By Sales Channel

Supermarkets lead citrus flavour sales with 37.3% in 2024, thanks to wide reach and strong brand visibility.

In 2024, Supermarkets held a dominant market position, capturing more than a 37.3% share of the global citrus flavours market by sales channel. This leadership stems from the convenience and accessibility that supermarkets offer to everyday consumers. With their extensive shelf space and organized product categories, supermarkets allow citrus-flavoured goods—from beverages and snacks to bakery items and condiments—to be prominently displayed and easily discovered by shoppers.

Key Market Segments

By Product

- Orange

- Lime

- Grapefruits

- Lemon

- Others

By Form

- Liquid

- Concentrate

- Powder

- Emulsion

By Nature

- Natural

- Artificial

By Application

- Beverages

- Bakery Products

- Confectionery

- Savory

- Others

By Sales Channel

- Supermarkets

- Departmental stores

- E-retailers

- Others

Drivers

Increasing Demand for Natural and Clean-Label Ingredients

A significant driver of the citrus flavors market is the growing consumer preference for natural and clean-label ingredients. As consumers become more health-conscious, there’s a noticeable shift towards products that are perceived as healthier and free from artificial additives. Citrus flavors, derived from fruits like oranges, lemons, and limes, are naturally refreshing and rich in nutrients, making them an attractive choice for both manufacturers and consumers.

According to a report by the European Commission, 73% of consumers in the EU consider natural ingredients essential when buying food products. This preference is driving the demand for citrus flavors, which are often associated with natural and clean-label products. In the United States, nearly 70% of consumers express a preference for products with natural flavors, further emphasizing the trend towards natural ingredients in food and beverages.

This shift towards natural and clean-label products is not only influencing consumer choices but also prompting manufacturers to innovate and reformulate their products to meet these evolving preferences. The demand for citrus flavors is expected to continue growing as consumers increasingly seek out products that align with their health and wellness goals.

Restraints

High Production Costs and Supply Chain Instability

A significant challenge facing the citrus flavors market is the escalating production costs and supply chain instability, primarily due to environmental factors and diseases affecting citrus crops. In regions like Florida and Brazil, citrus greening disease has severely impacted orange yields, leading to increased prices for raw materials. For instance, in the 2024-2025 season, Florida’s orange production dropped by 30%, reaching its lowest levels since World War II . Similarly, Brazil’s orange juice production is projected to decline by 15% in the 2024-2025 period due to adverse weather conditions and disease.

These disruptions have led to a surge in citrus fruit prices, with wholesale prices more than doubling to over $6,500 per tonne in Brazil, resulting in a 34% increase in supermarket prices . Such volatility poses challenges for manufacturers in maintaining consistent product pricing and quality.

In response, some companies are exploring alternatives to traditional citrus ingredients. Flavor suppliers are expanding their offerings of flavor extenders and replacers for conventional citrus ingredients to mitigate the impact of these supply chain challenges. Additionally, the Indian Council of Agricultural Research-Central Citrus Research Institute (ICAR-CCRI) is developing value-added citrus-based products and technologies to address post-harvest waste and enhance economic opportunities for citrus growers.

Opportunity

Government Support and Infrastructure Development

A significant growth opportunity for the citrus flavors market lies in the Indian government’s strategic initiatives aimed at boosting citrus production and exports. In the Union Budget 2024, the Indian government allocated ₹1.5 lakh crore to enhance agricultural productivity, promote eco-friendly farming practices, and strengthen agri-logistics infrastructure . This investment is expected to improve the supply chain, reduce post-harvest losses, and increase the availability of high-quality citrus fruits for flavor extraction

Additionally, the Directorate General of Foreign Trade (DGFT) proposed a harmonized export policy based on 8-digit HS codes, aiming to streamline export procedures and enhance market access for Indian citrus products. Such policy reforms are anticipated to facilitate smoother international trade and open new markets for Indian citrus flavors.

Trends

Emerging Trends in the Citrus Flavors Market: Natural Ingredients and Functional Beverages

The citrus flavors market is experiencing a significant shift towards natural ingredients and functional beverages, driven by changing consumer preferences and health-conscious trends. A key driver of this growth is the increasing demand for clean-label products. Consumers are becoming more aware of the ingredients in their food and beverages, leading to a preference for products with natural flavors and minimal additives.

This trend is particularly evident in the beverage industry, where citrus flavors are prominently featured in new product developments. According to Innova 2024 data, citrus flavors were featured in 22% of all new beverage launches over the past three years, reflecting a 4% growth rate.

The rise of functional beverages is also contributing to the popularity of citrus flavors. Consumers are seeking beverages that offer health benefits beyond basic nutrition, such as enhanced hydration, immunity support, and digestive health. Citrus fruits, rich in vitamin C and antioxidants, are well-suited to meet these demands. The incorporation of citrus flavors into functional beverages aligns with the broader trend of health and wellness, positioning citrus as a preferred ingredient in this category.

In response to these trends, companies are innovating to offer natural and functional citrus-flavored products. Advancements in extraction technologies and sustainable sourcing practices are enabling the production of high-quality citrus flavors that meet consumer expectations for health-conscious and clean-label products. This innovation is essential for companies aiming to capitalize on the growing demand for natural and functional citrus-flavored offerings in the market.

Regional Analysis

North America leads citrus flavours market with 39.5% share, valued at USD 0.6 Billion in 2024

In 2024, North America held a dominant market position in the global citrus flavours market, capturing more than a 39.5% share, equivalent to approximately USD 0.6 billion in market value. This leadership is largely driven by the region’s mature food and beverage industry, coupled with evolving consumer preferences that increasingly favor natural, refreshing, and functional flavour profiles. Citrus flavours, particularly orange, lemon, lime, and grapefruit, are widely used across multiple segments including carbonated drinks, sports beverages, bakery, dairy, confectionery, and processed foods.

The United States remains the key contributor to the region’s dominance, owing to high product innovation, premium brand positioning, and growing demand for clean-label and health-centric offerings. For example, citrus flavours are increasingly being used in low-calorie beverages, organic snacks, and vitamin-enriched foods, aligning with consumer expectations for health-conscious consumption. Canada and Mexico also contribute to regional growth with rising urbanization and increasing availability of flavoured products across supermarkets and specialty stores.

Moreover, North America’s robust distribution infrastructure and strong retail presence—including supermarket chains, health food stores, and convenience outlets—further boost the accessibility and visibility of citrus-flavoured products. In-store promotions and digital marketing campaigns also play a role in sustaining consumer interest.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Firmenich SA is a global leader in flavour and fragrance innovation, with a strong footprint in the citrus flavours segment. The company leverages advanced extraction technologies and sustainable sourcing to produce authentic and natural citrus profiles for a wide range of food and beverage applications. Firmenich’s deep research capabilities and consumer insight tools help brands align with regional taste trends and health preferences, making it a preferred partner for multinational and premium food producers across North America, Europe, and Asia-Pacific.

Kerry Group is a prominent player in the global taste and nutrition industry, offering a broad portfolio of citrus flavour solutions. With a focus on clean-label, natural ingredients, and functional health benefits, Kerry integrates citrus notes into beverages, dairy products, and wellness-oriented foods. Its expertise in sensory science and regional flavour development enables the company to serve diverse markets. The group continues to invest in sustainable practices and innovation to meet evolving consumer demand for transparency and authenticity.

Dohler Group specializes in natural ingredients and integrated solutions for the food and beverage industry, with citrus flavours being a core part of its offerings. Known for its “from field to flavour” approach, Dohler manages every step from fruit sourcing to flavour creation. The company offers customized citrus flavour profiles suitable for juices, teas, alcoholic drinks, and plant-based products. With global production facilities and a strong sustainability focus, Dohler is well-positioned to serve both traditional and emerging markets.

Top Key Players in the Market

- Firmenich SA

- Kerry Group

- Dohler Group

- Archer Daniels Midland Company (ADM)

- Robertet Group

- Givaudan SA

- International Flavors & Fragrances Inc. (IFF)

- Symrise AG

- Sensient Technologies Corporation

- Takasago International Corporation

- Firmenich SA

- Kerry Group

- Dohler Group

- Archer Daniels Midland Company (ADM)

- Robertet Group

Recent Developments

In 2024, Robertet Group reported a revenue of €807 million, marking a 12% increase from the previous year.

In 2024, Archer Daniels Midland Company (ADM) reported net earnings of $1.8 billion, with adjusted net earnings of $2.3 billion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.7 Bn |

| Forecast Revenue (2034) | USD 2.6 Bn |

| CAGR (2025-2034) | 4.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Orange, Lime, Grapefruits, Lemon, Others), By Form (Liquid, Concentrate, Powder, Emulsion), By Nature (Natural, Artificial), By Application (Beverages, Bakery Products, Confectionery, Savory, Others), By Sales Channel (Supermarkets, Departmental stores, E-retailers, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Firmenich SA, Kerry Group, Dohler Group, Archer Daniels Midland Company (ADM), Robertet Group, Givaudan SA, International Flavors & Fragrances Inc. (IFF), Symrise AG, Sensient Technologies Corporation, Takasago International Corporation, Firmenich SA, Kerry Group, Dohler Group, Archer Daniels Midland Company (ADM), Robertet Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |