Quick Navigation

Report Overview

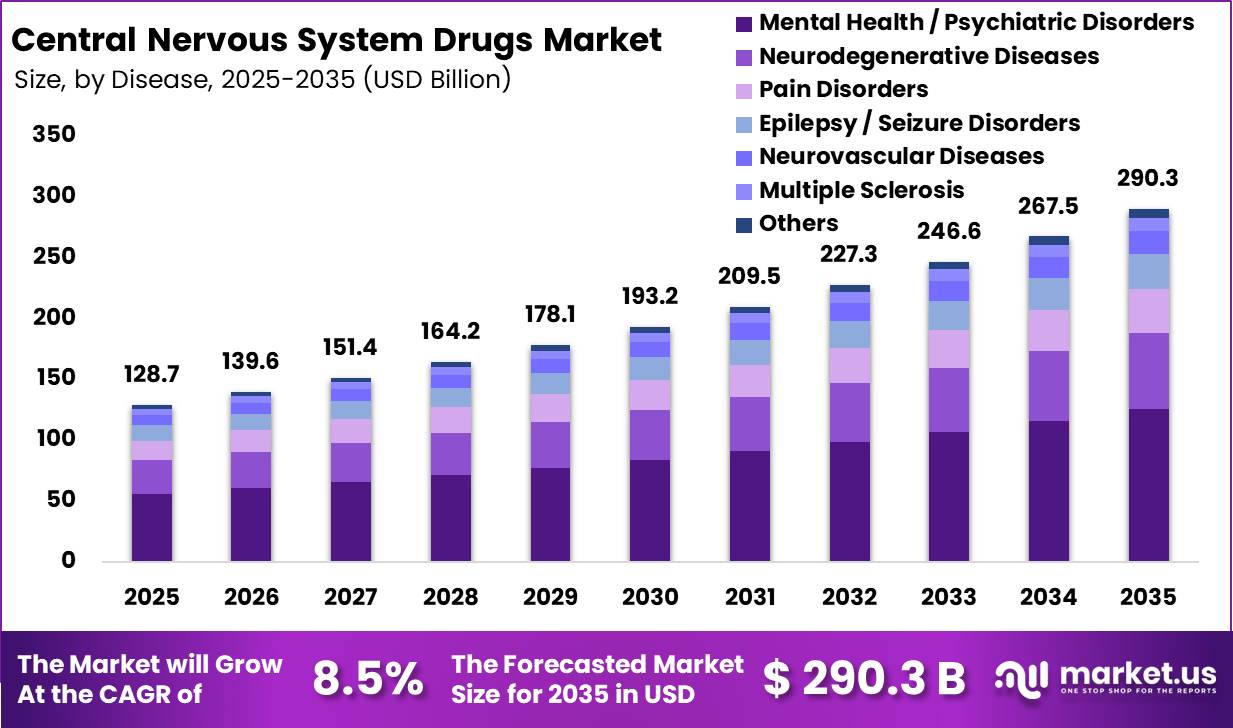

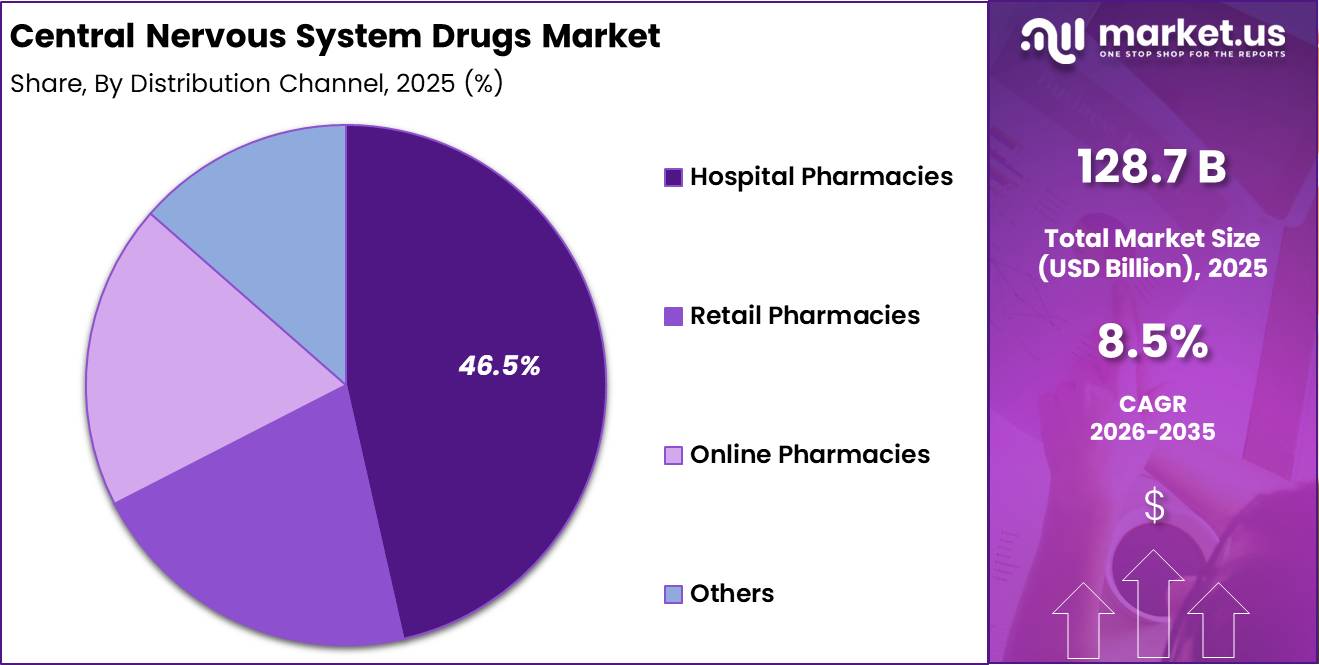

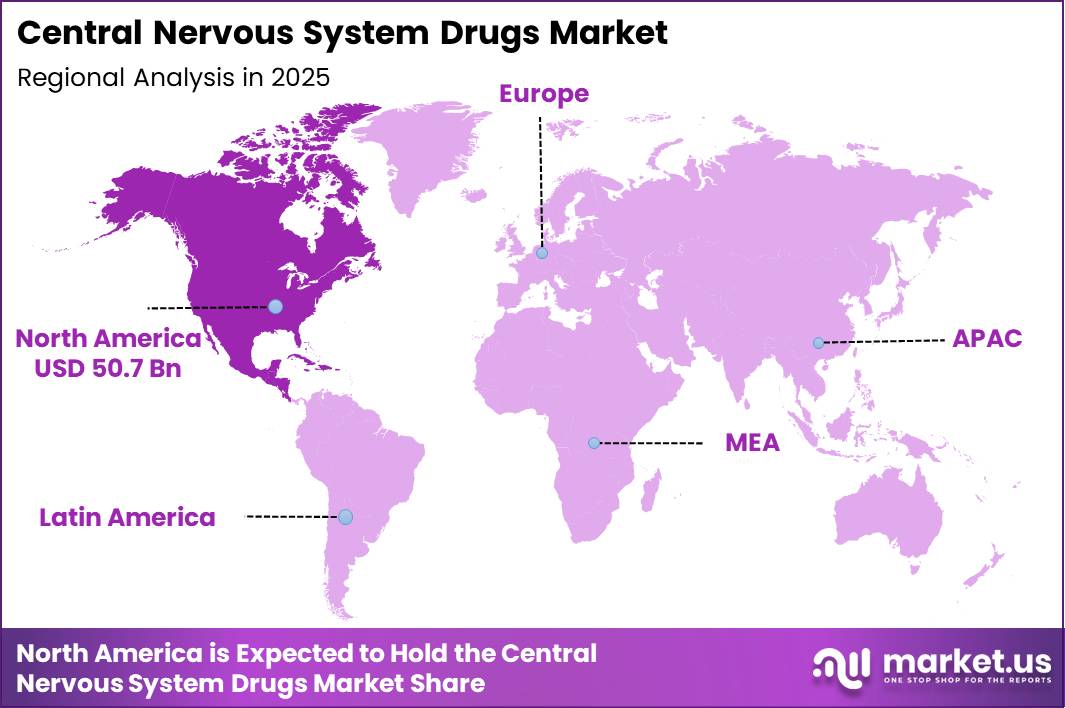

Global Central Nervous System Drugs Market size is expected to be worth around US$ 290.3 Billion by 2035 from US$ 128.7 Billion in 2025, growing at a CAGR of 8.5% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 39.4% share, holding US$ 50.7 Billion in revenue.

Market growth is being driven by the rising global prevalence of chronic brain disorders and psychiatric conditions requiring long-term therapeutic intervention. According to the WHO Global Status Report on Neurology (2024), neurological conditions including stroke, dementia, epilepsy, migraine, and Parkinson’s disease—affect more than 3 billion people, representing over 1 in 3 individuals globally.

The overall neurological disease burden has increased by 18% since 1990, and a subsequent 2024 study in Neurology projects that total brain disorder cases will reach 4.9 billion by 2050. As the vast majority of these neurological and psychiatric conditions require sustained, multi-year drug regimens, this expanding patient pool ensures a highly resilient demand curve for CNS therapeutics.

North America accounted for the largest market share of 39.4% in 2025, generating US$ 50.7 billion in revenue. The region’s leadership is supported by high healthcare spending, advanced treatment infrastructure, and rapid patient access to innovative medicines.

According to the U.S. Centers for Medicare & Medicaid Services (CMS), U.S. National Health Expenditure reached US$ 5.3 trillion in 2024 (equal to 18.0% of GDP), while prescription drug spending specifically increased by 11.4%. The U.S. CDC reports that nearly 90% of total healthcare spending is directed toward chronic and mental health conditions.

Alzheimer’s and dementia care alone cost approximately US$ 360 billion in 2024 and are projected to approach US$ 1 trillion by 2050. Combined with a high average annual healthcare expenditure of US$ 14,775 per capita, robust private and public insurance coverage, and a steady pipeline of FDA approvals, North America is securely positioned to sustain its market leadership.

Meanwhile, a profound treatment gap in low-income countries, where fewer than 10% of individuals currently receive mental healthcare, represents a significant unaddressed landscape for long-term global expansion.

Key Takeaways

- Market Size: Global Central Nervous System Drugs Market size is expected to be worth around US$ 290.3 Billion by 2035 from US$ 128.7 Billion in 2025

- Market Share: The market is growing at a CAGR of 8.5% during the forecast period from 2026 to 2035.

- Disease Analysis: Mental Health/Psychiatric Disorders dominated the global CNS drugs market, accounting for 43.3% of the total market share, driven by the rising prevalence of depression, anxiety, schizophrenia, and other psychiatric conditions worldwide.

- Drug Class Analysis: Analgesics/Pain Relievers held the largest market share at 18.8%, supported by the growing burden of chronic pain disorders and increasing demand for effective pain management therapies.

- Route of Administration Analysis: The Oral segment dominated the market, representing 64.3% of the total market share, owing to its convenience, high patient compliance, and widespread use across CNS therapeutic categories.

- Distribution Channel Analysis: Hospital Pharmacies led the market with a 46.5% share, primarily due to the high volume of prescription-based CNS medications and the treatment of complex neurological and psychiatric disorders in hospital settings.

- Regional Analysis: In 2025, the North America was the most dominant region in the Central Nervous System Drugs market, accounting for 39.4% of the total global consumption.

Disease Analysis

Mental Health / Psychiatric Disorders disease represents dominant Segment in the Market.

Psychiatric disorders account for the leading 43.3% share of the global CNS drugs market, driven by a massive global disease burden and a well-established commercial market for long-term maintenance therapies.

According to the World Health Organization (WHO) Mental Health Atlas, more than 1 billion people worldwide live with a mental health disorder, including 359 million individuals living with anxiety disorders and 332 million with depression.

Data from the Institute for Health Metrics and Evaluation (IHME) highlights that mental disorders caused 171 million Disability-Adjusted Life Years (DALYs) in 2023, accelerating from the 12th leading cause of global disease burden in 1990 to the 5th leading cause today.

Furthermore, a joint WHO-World Bank study published in The Lancet Psychiatry estimates that the secondary economic toll of depression and anxiety results in approximately US$ 1 trillion in lost global productivity annually, underscoring the critical need for effective medical management.

Sustained market momentum is further reinforced by expanding government initiatives and rising clinical treatment adoption rates. The WHO Comprehensive Mental Health Action Plan 2013–2030 continues to push member states to widen treatment coverage frameworks for severe mental illnesses.

Data from the OECD (Health at a Glance) indicates that antidepressant utilization across member nations surged by more than 40% over a ten-year period, while global psychotropic medicine consumption maintained a steady average annual growth rate of 2.94%. Despite these clinical advancements, over 70% of individuals exhibiting mental health conditions worldwide still do not receive formal treatment.

This vast, underserved patient population coupled with diminishing social stigma, rising diagnostic screening rates, and supportive corporate wellness policies is projected to maintain aggressive demand for psychiatric drugs, cementing the segment’s dominant position within the global broader CNS architecture.

The Neurodegenerative Diseases segment represented the second-largest share of the market, driven by the rising incidence of Alzheimer’s disease, Parkinson’s disease, and other age-related neurological disorders. Increasing life expectancy and the growing global geriatric population continue to create substantial demand for therapies targeting neurodegenerative conditions.

Meanwhile, Pain Disorders maintained a significant market presence owing to the widespread prevalence of chronic pain, neuropathic pain, migraine, and other CNS-related pain conditions. Epilepsy/Seizure Disorders, Neurovascular Diseases, and Multiple Sclerosis also contributed notably to market revenue, supported by ongoing drug development efforts, improved diagnostic capabilities, and expanding access to specialized neurological care.

Drug Class Analysis

Analgesics/Pain Relievers Held the Largest Share in the CNS Drugs Market.

Analgesics/pain relievers dominated the global Central Nervous System (CNS) pharmaceuticals market in 2025, accounting for 18.8% of total revenue. The segment’s dominant position is mostly due to the rising global burden of chronic pain and musculoskeletal disorders.

According to the World Health Organization (WHO), around 1.71 billion people worldwide live with musculoskeletal conditions such as low back pain, neck pain, and osteoarthritis. These conditions account for 17% of all global Years Lived with Disability (YLDs). Low back pain alone affects 619 million people globally and is projected to increase to 843 million by 2050, cementing pain relief medicines as a primary, high-volume therapeutic requirement.

Demand is further strengthened by the high prevalence of headache disorders and cancer-related pain. While severe neurological diseases affect over 3 billion individuals globally, WHO estimates that broader headache disorders including episodic and chronic migraines impact approximately 3.1 billion people (nearly 40% of the global population).

Consequently, migraine ranks as the third-leading cause of global Disability-Adjusted Life Years (DALYs). In addition, the International Association for the Study of Pain (IASP) estimates that 7% to 10% of adults globally live with chronic neuropathic pain. Oncology is another major driver; with 20 million new cancer cases reported worldwide in 2022, and 55% to 66% of patients experiencing significant treatment-related pain, the International Agency for Research on Cancer (IARC) projection of 35 million annual cases by 2050 will sustain heavy long-term demand for both opioid and non-opioid analgesics.

Finally, the rapidly expanding global geriatric population is acting as a major catalyst for sustained market growth. As the global population aged 60 and older accelerates toward 1.4 billion by 2030, the prevalence of osteoarthritis and degenerative joint pain is rising proportionally. A 2026 meta-analysis published in the Indian Journal of Medical Research found that chronic pain now affects more than 46.7% of adults aged over 45 years.

In the United States, the CDC reported that 24.3% of adults experienced chronic pain in 2023 (up from 20.4% in 2019), while 8.5% suffered from high-impact chronic pain. Similarly, in Europe, approximately 150 million people 20% of the population—live with chronic pain, creating an economic burden exceeding €440 billion annually. These compounding demographic and economic factors continue to drive robust global demand for analgesic therapies.

Route of Administration Analysis

Oral route Held a Major Share of the Central Nervous System Drugs Market.

The oral route dominated the global CNS drugs market, accounting for 64.3% of the market share in 2025, driven by its suitability for long-term treatment of chronic neurological and psychiatric disorders. According to the WHO, non-communicable diseases (NCDs) caused at least 43 million deaths in 2021, representing 75% of all non-pandemic-related deaths worldwide.

Most CNS disorders require lifelong or long-duration treatment, making oral dosage forms such as tablets, capsules, and oral solutions the most practical option for self-administration at home. Unlike injectable and infusion therapies, oral medicines do not require healthcare professionals or specialized medical facilities, making them more convenient and cost-effective for chronic disease management.

The strong market position of oral CNS drugs is also supported by regulatory and clinical trends. Based on FDA Orange Book data from 1938 to 2022, oral drug products account for approximately 54% of all approved New Drug Applications (NDAs), including 46% immediate-release and 8% modified-release formulations. According to the WHO, around 50 million people worldwide live with epilepsy, and up to 70% can become seizure-free through regular use of oral antiseizure medicines.

In addition, approximately 332 million people live with depression globally, where oral SSRIs and other antidepressants remain the first-line treatment. For Parkinson’s disease, oral levodopa/carbidopa continues to be the most widely used and effective therapy and is included in the WHO Model List of Essential Medicines.

Furthermore, IQVIA projects global medicine use to reach nearly 4 trillion defined daily doses (DDDs) by 2030, while prescription medicine use reached 215 billion days of therapy in 2024, reinforcing the continued demand for oral maintenance therapies in CNS treatment.

The parenteral category held the second-largest proportion of the CNS medicines market, thanks to its crucial role in hospital settings, emergency care, anesthesia, and the treatment of severe neurological diseases that require immediate therapeutic action. Injectable formulations are widely utilized in applications requiring fast medication delivery or increased bioavailability, such as abrupt seizures, severe pain treatment, and intensive care.

Meanwhile, the other group, which includes transdermal patches, nasal sprays, sublingual formulations, and future drug delivery technologies, is slowly gaining popularity. These alternate administration methods have benefits such as increased drug absorption, more patient convenience, and targeted distribution, making them more appealing for specific CNS therapy and future pharmaceutical breakthroughs.

Distribution Channel Analysis

Hospital pharmacies accounted for 46.5% of the global CNS drugs market in 2025, making them the leading distribution channel. Their dominance is driven by the high number of patients requiring emergency neurological care, hospital-only treatment protocols, and specialist monitoring for complex CNS therapies.

According to the World Stroke Organization, there were 93.8 million people living with stroke worldwide in 2021, with 11.9 million new stroke cases each year. Acute stroke treatment requires hospital-administered medicines such as thrombolytics, anticoagulants, and neuroprotective drugs, which can only be dispensed through hospital pharmacies under medical supervision. The global economic burden of stroke already exceeds US$ 890 billion annually, equal to 0.66% of global GDP, and is expected to nearly double by 2050, supporting sustained demand for hospital-based CNS medicines.

Hospital pharmacies also benefit from mandatory dispensing requirements for severe psychiatric disorders. According to the WHO, nearly 50% of patients in mental hospitals are diagnosed with schizophrenia. The leading treatment for treatment-resistant schizophrenia, clozapine, requires weekly blood monitoring for the first 18 weeks, restricting its dispensing to designated hospital pharmacies in many countries.

In addition, neurological disorders account for 15.3% of all pediatric inpatients and 17.7% of hospital admission episodes, with epilepsy representing 26% of neurological admissions. Each admission requires hospital-dispensed CNS medicines, including IV antiepileptics and benzodiazepines. Furthermore, the Lancet Commission estimates 143 million additional surgical procedures are needed annually, while approximately 312.9 million surgeries are performed globally each year.

Every surgical procedure requires CNS anesthetics and analgesics supplied through hospital pharmacies. The OECD also reports average retail pharmaceutical spending of USD 614 per capita in 2021, excluding hospital-administered medicines, highlighting the significant contribution of hospital pharmacies to total CNS drug revenue.

Retail pharmacies dominated the market, owing to the broad availability of prescription drugs used to treat depression, anxiety, chronic pain, and other prevalent CNS diseases. Their accessibility and convenience make them the main avenue for outpatient care.

Meanwhile, online pharmacies are expanding rapidly as healthcare becomes more digital, internet usage grows, and consumers choose home delivery options. The others category, which includes specialty pharmacies and alternative distribution channels, continues to help the market grow by offering tailored services to patients who require specific CNS treatments and personalized medication management programs.

Key Market Segments

By Disease

- Mental Health / Psychiatric Disorders

- Neurodegenerative Diseases

- Pain Disorders

- Epilepsy / Seizure Disorders

- Neurovascular Diseases

- Multiple Sclerosis

- Others

By Drug Class

- Analgesics / Pain Relievers

- Antidepressants

- Antipsychotics

- Anticonvulsants / Antiepileptics

- Anti-Alzheimer’s / Anti-Parkinson’s Agents

- CNS Stimulants

- Anesthetics

- Antiemetics

- Others

By Route of Administration

- Oral

- Parenteral

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

Driver

Alzheimer’s Disease-Modifying Therapy Rollout

The U.S. Food and Drug Administration approval of Kisunla (donanemab-azbt) in July 2024 marks a pivotal shift in the Alzheimer’s market from symptomatic management to disease modification. Indicated for adults with early symptomatic Alzheimer’s disease and confirmed amyloid pathology, Kisunla is administered via IV infusion every four weeks, anchoring treatment in high-value specialty care settings.Commercially, the impact extends well beyond drug sales.

Each treated patient drives incremental demand for amyloid diagnostics, infusion-center capacity, serial MRI monitoring for safety, specialist neurologist oversight, and adverse-event management. As a result, revenue expansion is disproportionate to patient numbers, with higher annual spend per patient, stronger service attachment, and closer persistence tracking than legacy cognitive therapies.

Even under Centers for Medicare & Medicaid Services evidence-linked coverage constraints, the launch resets pricing benchmarks and investment priorities across neurodegeneration. It accelerates capital and R&D flow into next-generation Alzheimer’s pipelines, including tau-targeted agents, combination regimens, and earlier preclinical interventions, structurally elevating the long-term CNS market opportunity.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-led neuro burden expansion | +1.8% | North America core, EU, Japan, urban China spill-over | Medium term (2-4 years) |

| Alzheimer disease-modifying therapy rollout | +2.4% | U.S. core, EU selective, Japan early adopter | Short term (≤ 2 years) |

| New-mechanism psychiatry launches | +1.9% | U.S. core, EU, Australia, high-income APAC | Short term (≤ 2 years) |

| Earlier diagnosis via biomarkers and imaging | +1.5% | U.S. core, EU, Japan, tertiary APAC corridors | Medium term (2-4 years) |

| Payer push for outcomes and specialty pathways | +1.3% | U.S. core, EU reimbursement hubs | Medium term (2-4 years) |

| Untreated mental-health and neuro access gap | +1.6% | India, Latin America, ASEAN, Middle East, Africa | Long term (≥ 4 years) |

Challenge

High-Complexity Trial Execution in CNS Drug Development

Central nervous system (CNS) drug development faces structurally high trial complexity due to variable endpoints such as cognition and functional status, which typically require 30–50% larger sample sizes than non-CNS indications. Pivotal trials for depression, Alzheimer’s disease, or stroke adjuncts often enroll 1,500–3,000 patients and involve long baseline and follow-up periods of 18–36 months.

As a result, phase II–III execution commonly spans 5–7 years, with per-program costs reaching USD 600–900 million and late-stage attrition rates exceeding 60%.Operational challenges further extend timelines. Screen-failure rates of 30–40%, driven by comorbidities and biomarker requirements, and site activation periods of 6–9 months due to specialized staffing and imaging needs, slow enrollment and limit portfolio throughput.

Collectively, these factors delay launches and reduce the number of assets that can be advanced in parallel, trimming an estimated 1.4 % points from realizable market CAGR.To mitigate this drag, sponsors are adopting adaptive and platform trial designs, enriched patient selection using imaging and digital biomarkers, and hybrid decentralized models that reduce visit burden by 20–30%. Increased investment in centralized data monitoring and site-network consolidation is helping compress timelines and stabilize portfolio-level risk.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| High-complexity trial execution | -1.4% | North America core, EU hubs, Japan | Medium term (2-4 years) |

| Neurology talent and skills crunch | -1.2% | US, Western EU, Japan, China tier-1 | Long term (≥ 4 years) |

| Data integration and real-world evidence gaps | -0.9% | US, EU, APAC large economies | Medium term (2-4 years) |

| Advanced modality manufacturing bottlenecks | -1.0% | US, EU, East Asia bioclusters | Long term (≥ 4 years) |

| Pricing pressure and access pathway complexity | -1.1% | US, EU, emerging markets | Medium term (2-4 years) |

| Chronic burden and multimorbidity care fragmentation | -0.8% | Global, stronger in LMICs | Long term (≥ 4 years) |

Restraints

High CNS Clinical Failure Rates and Extended Development Cycles

CNS drug development continues to face structurally high risk, with lower approval probabilities and longer timelines than most therapeutic areas. Recent data show that only about 4–5% of novel drug approvals between 2018 and 2022 were in psychiatry or neurology, despite rising neurological disease burden, underscoring persistent translational and clinical challenges acknowledged by the U.S. Food and Drug Administration.

These challenges include complex disease biology, blood–brain barrier constraints, and endpoints that are difficult to standardize. Typical CNS development timelines span 10–12 years from first-in-human studies to approval, with Phase II/III failure rates exceeding 60% in many neurology segments. Large pivotal trials often require 1,000–3,000 patients and multi-year follow-up, significantly increasing capital at risk per program.

As a result, for every successful CNS launch, multiple programs are delayed or terminated.Strategically, this drives higher development burn rates, lower portfolio-level returns, and more cautious capital allocation. Many companies now prioritize CNS assets supported by strong biomarker or genetic validation, delaying broader commercialization waves by 3–5 years. Collectively, these dynamics impose a structural drag of roughly 1.5 % points on forward CNS market CAGR despite substantial unmet medical need.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating CNS drug pricing & access controls | -2.0% | US, EU5, select APAC | Medium term (2–4 years) |

| High CNS clinical failure rates & extended development cycles | -1.5% | Global | Long term (≥ 4 years) |

| Neuro-specialist and infrastructure gaps in LMICs | -1.2% | EMs, LMICs, APAC, Africa | Long term (≥ 4 years) |

| HTA, value-based and budget impact constraints | -1.0% | EU, UK, Canada, select APAC | Medium term (2–4 years) |

| Manufacturing complexity & biologics supply risk | -0.8% | Global (US, EU, APAC corridors) | Medium term (2–4 years) |

Opportunity

Oral and Home-Based Alzheimer’s & Dementia Care

Oral and home-based Alzheimer’s and dementia therapies offer a clear opportunity to expand access beyond infusion-centered models that are constrained by capacity, monitoring, and geography. While current disease-modifying treatments rely on specialty-center infusions or injections, successful oral alternatives could shift care into the home and primary-care settings.

Such a transition could cut administration and facility costs by 25–40%, reduce caregiver burden by 10–15%, and bring treatment to many early-stage patients who currently fall outside infusion networks, especially in APAC and smaller EU markets. Strategically, oral regimens enable chronic-care models combining medication with remote monitoring and digital cognitive assessment, improving lifetime value even at lower annual prices.

Although not yet a near-term growth driver due to immature reimbursement and support infrastructure, oral and home-based regimens could add roughly 1.5–2.0 % points to market growth, with ~1.9% incremental CAGR potential by 2035 if they reach 30–40% penetration of eligible early-stage patients.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Pre-symptomatic neurodegeneration therapies | +2.2% | North America, EU, Japan, China urban | Medium term (2-4 years) |

| Oral and home-based Alzheimer’s & dementia care | +1.9% | North America core, EU, APAC emerging | Medium term (2-4 years) |

| Digital neurology & remote CNS disease management | +1.6% | Global, LMIC-heavy | Short to medium (≤4 years) |

| CNS drugs access platforms for LMICs | +1.4% | Africa, South Asia, Latin America | Long term (≥4 years) |

| Precision CNS therapies for underserved populations | +1.3% | US, EU, Middle East, Latin America | Medium to long (≥3 years) |

| Integrated pain–neurology & mental health bundles | +1.1% | Global, primary care centric | Short to medium (≤4 years) |

Geopolitical Impact Analysis

Rising Trade Tensions and Pharmaceutical Supply Chain Realignment Impacting CNS Drug Availability.

The CNS drugs market is facing rising cost pressures due to higher trade barriers and ongoing global shipping disruptions. The market depends heavily on imported Active Pharmaceutical Ingredients (APIs), particularly from Asia. On April 2, 2026, the U.S. announced a 100% tariff on patented pharmaceutical products and related APIs under Section 232, effective from July 31, 2026 for major manufacturers and September 29, 2026 for all others. Lower tariff rates of 15% apply to imports from the EU, Japan, South Korea, and Switzerland, while the UK faces a 10% tariff.

According to the White House, about 53% of patented medicines sold in the U.S. are manufactured overseas, while only 15% of patented APIs are produced domestically. This creates significant cost pressure for manufacturers of patented CNS drugs, including antidepressants, antipsychotics, and Alzheimer’s therapies.

In addition, China supplies 39.9% of U.S. pharmaceutical inputs by volume and faces combined tariffs of up to 245%, including reciprocal and fentanyl-related duties. Although India is a major alternative supplier, it imports nearly 70% of its bulk drug intermediates from China, limiting supply chain diversification.

Logistics challenges are adding further pressure. Since November 2023, more than 190 attacks in the Red Sea have forced many vessels to reroute around the Cape of Good Hope, increasing voyage distances by about 40% and delaying shipments by 2 to 5 weeks. The World Bank reported that container traffic through the Suez Canal declined by 90% between December 2023 and March 2024.

According to UNCTAD, the disruption affected 30% of global container trade, reduced shipping capacity by 15% to 20% in Q2 2024, and increased global freight rates by about 120% compared with October 2023. These delays raise logistics costs, increase inventory requirements, and create additional challenges for temperature-sensitive CNS biologics and specialty injectables. Reflecting these pressures, the WTO reduced its 2026 global merchandise trade growth forecast from 1.8% to 0.5%, indicating a more challenging cost environment for the global CNS drugs market.

Regional Analysis

North America Held the Largest Share of the Global Central Nervous System Drugs Market.

In 2025, North America dominated the worldwide Central Nervous System (CNS) medicine market, with 39.4% of the total market share. The region’s leadership is mostly due to its modern healthcare infrastructure, high healthcare expenditure, excellent pharmaceutical research and development skills, and rising prevalence of neurological and mental illnesses.

The United States continues to contribute the most to regional revenue due to the presence of major pharmaceutical companies, advantageous reimbursement systems, and widespread acceptance of novel CNS medicines.

Increased awareness of mental health disorders, higher diagnosis rates, and ongoing funding in brain research have all contributed to market expansion. Furthermore, regulatory support for innovative drug approvals and a strong clinical trial environment are helping to boost North America’s position in the global CNS medicines market.

Europe was the second-largest geographical market, thanks to well-established healthcare systems, an increased government focus on mental health services, and an aging population vulnerable to neurological disorders like Alzheimer’s and Parkinson’s disease.

Asia Pacific is predicted to develop the fastest throughout the forecast period, owing to its huge patient population, expanding healthcare infrastructure, improved access to treatment, rising healthcare spending, and growing awareness of neurological and mental illnesses.

Meanwhile, Latin America’s market is steadily expanding, because to improved healthcare access and more investment in neurological care. The Middle East and Africa region is progressively emerging as a promising market, aided by healthcare modernization programs, disease awareness campaigns, and ongoing attempts to improve access to specialized neurological and mental health therapies.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global Central Nervous System (CNS) medicine industry is very competitive, with top pharmaceutical and biotechnology companies prioritizing innovation, pipeline growth, and strategic collaborations to strengthen their market positions.

Manufacturers prioritize the development of innovative treatments to treat neurological and psychiatric disorders with major unmet medical requirements, such as Alzheimer’s disease, Parkinson’s disease, multiple sclerosis, depression, schizophrenia, and epilepsy. Companies are expanding their investments in disease-modifying treatments, biologics, gene therapies, monoclonal antibodies, and precision medicine approaches in order to improve clinical results and differentiate their product offerings.

Strategic acquisitions, license agreements, and collaborations with biotechnology companies, academic institutions, and research organizations allow market participants to speed up medication discovery and obtain access to developing technologies. In addition, corporations are extending clinical trial programs, chasing regulatory approvals in significant markets, and using artificial intelligence and biomarker-based research to increase development success rates.

Long-term supply agreements, geographic expansion strategies, and ongoing investment in neuroscience research all contribute to competitive positioning, while strong intellectual property portfolios and diverse CNS pipelines remain critical for maintaining market leadership in the changing global CNS therapeutics landscape.

Top Key Players

- Biogen Inc.

- Johnson & Johnson

- Hoffmann-La Roche Ltd

- Novartis AG

- UCB

- Sanofi

- Pfizer Inc.

- Merck KGaA

- Sumitomo Dainippon Pharma

- AbbVie

- Recipharm AB

- Neuraxpharm

- Sun Pharmaceutical Ltd

- Ranbaxy Laboratories

- Merz Pharma GmbH & Co. KGaA

Key Development

- January 2026 – Novartis AG signed a global licensing and development agreement with SciNeuro Pharmaceuticals worth up to USD 1.7 billion to develop next-generation antibody therapies for Alzheimer’s disease. The partnership combines SciNeuro’s proprietary brain-delivery technology with Novartis’ global clinical development and commercialization expertise, supporting the advancement of innovative CNS therapies.

- January 2025 – Johnson & Johnson announced the acquisition of Intra-Cellular Therapies for approximately USD 14.6 billion. The transaction significantly strengthens the company’s neuroscience portfolio by adding CAPLYTA (lumateperone), an approved therapy for schizophrenia and bipolar depression, along with a promising pipeline of central nervous system (CNS) candidates targeting major depressive disorder and other neuropsychiatric conditions. The acquisition reflects the growing strategic focus on innovative CNS therapeutics.

- September 2025 – AbbVie entered into a definitive agreement to acquire Aliada Therapeutics for approximately USD 1.4 billion. The acquisition expands AbbVie’s neuroscience pipeline through ALIA-1758, an investigational Alzheimer’s disease therapy designed with a novel blood-brain barrier delivery platform. The deal is expected to enhance the company’s long-term position in neurodegenerative disease treatment.

- December 2025 – Novartis AG announced the acquisition of Avidity Biosciences in a deal valued at approximately USD 12 billion. The transaction broadens Novartis’ neuroscience and neuromuscular disease portfolio by strengthening its capabilities in RNA-based therapies for rare neurological disorders, reinforcing the company’s investment in advanced CNS treatment technologies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 128.7 Billion |

| Forecast Revenue (2035) | US$ 290.3 Billion |

| CAGR (2026-2035) | 8.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Disease (Mental Health/Psychiatric Disorders, Neurodegenerative Diseases, Pain Disorders, Epilepsy/Seizure Disorders, Neurovascular Diseases, Multiple Sclerosis, and Others), By Drug Class (Analgesics/Pain Relievers, Antidepressants, Antipsychotics, Anticonvulsants/Antiepileptics, Anti-Alzheimer’s/Anti-Parkinson’s Agents, CNS Stimulants, Anesthetics, Antiemetics, and Others), By Route of Administration (Oral, Parenteral, and Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, and Others). |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Biogen Inc., Johnson & Johnson, Hoffmann-La Roche Ltd, Novartis AG, UCB, Sanofi, Pfizer Inc., Merck KGaA, Sumitomo Dainippon Pharma, AbbVie, Recipharm AB, Neuraxpharm, Sun Pharmaceutical Ltd, Ranbaxy Laboratories, Merz Pharma GmbH & Co. KGaA. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |