Quick Navigation

Report Overview

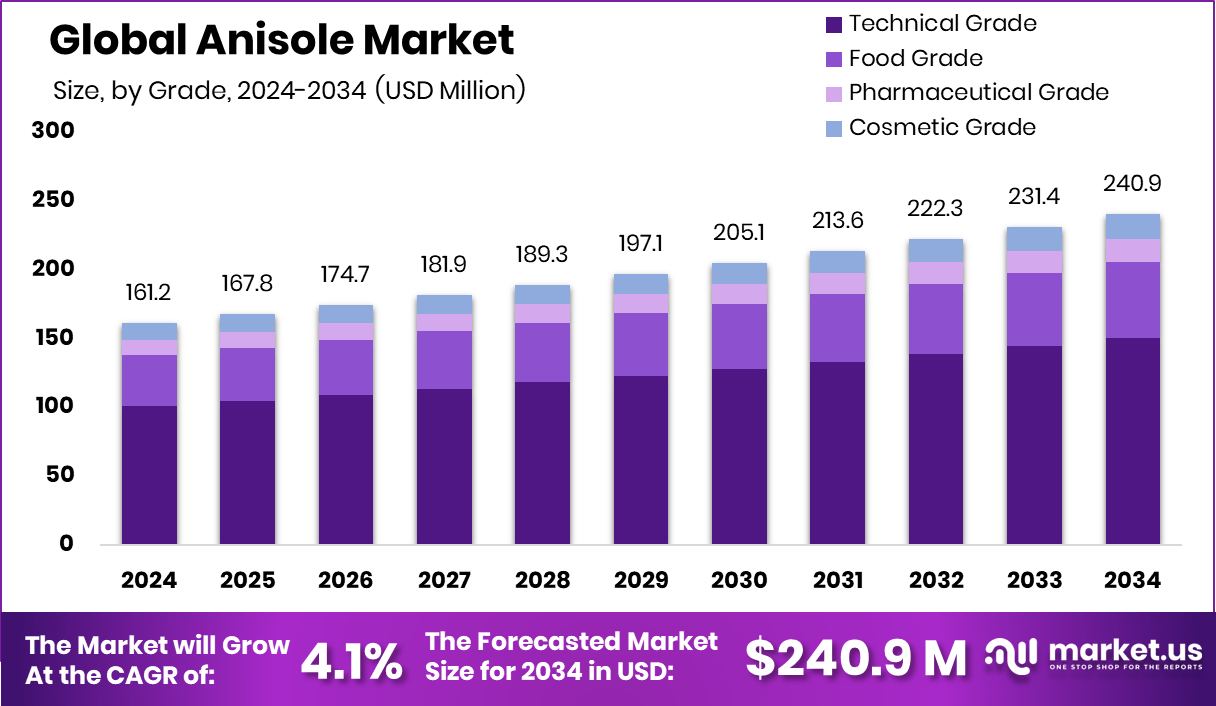

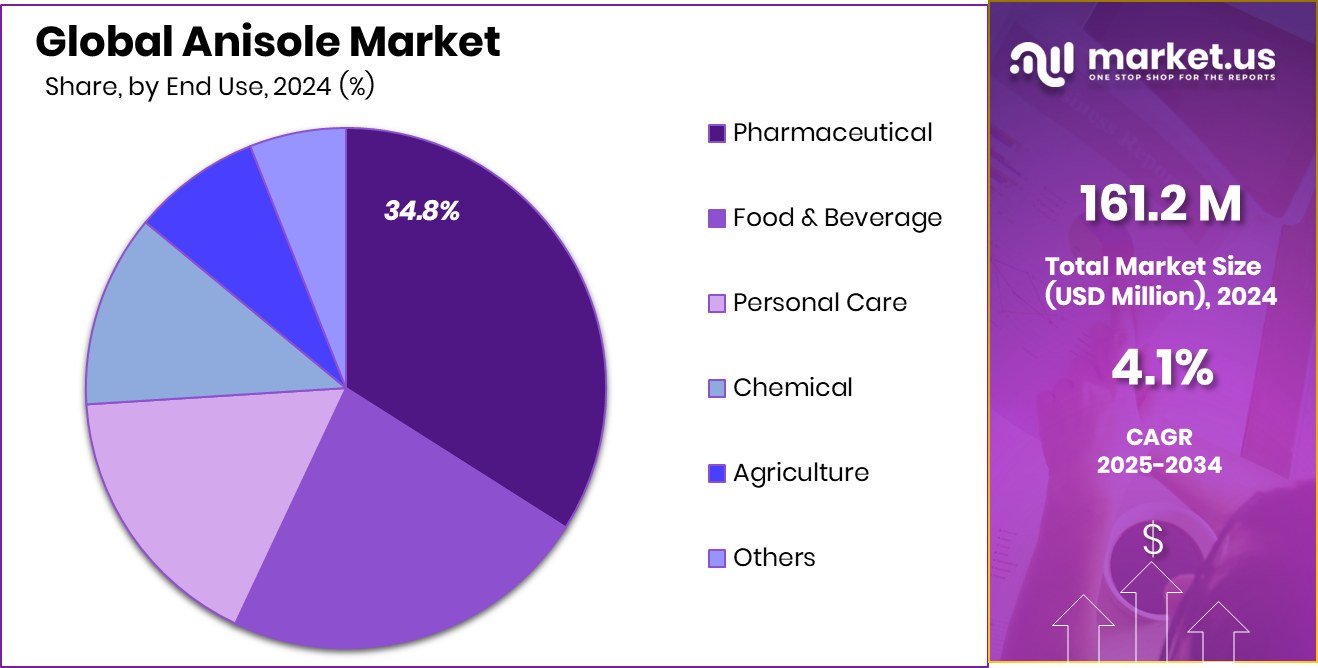

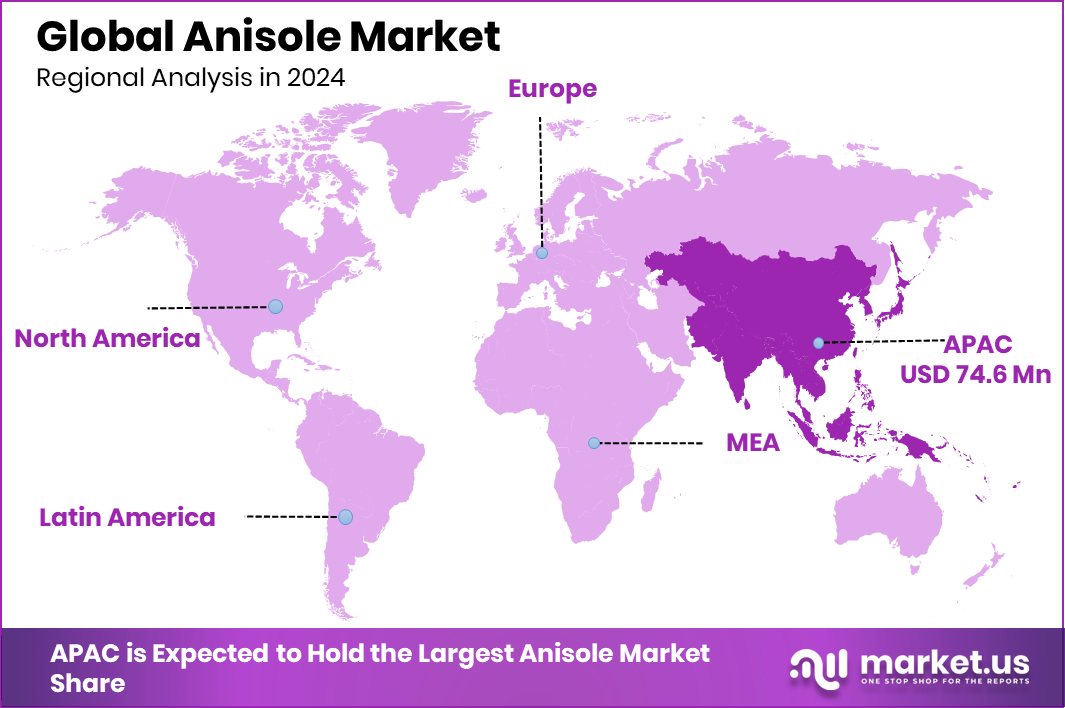

Global Anisole Market is expected to be worth around USD 240.9 Million by 2034, up from USD 161.2 Million in 2024, and grow at a CAGR of 4.1% from 2025 to 2034. Asia-Pacific leads the Anisole Market with a 46.3% share due to rapid industrial growth.

Anisole, also known as methoxybenzene, is an organic compound derived from phenol, with a methoxy group (-OCH₃) attached to a benzene ring. It is a colorless, flammable liquid with a sweet, ether-like aroma and is primarily used as a chemical intermediate in the manufacture of fragrances, dyes, and pharmaceuticals. Due to its aromatic structure and stability, anisole is often used in organic synthesis and as a precursor to various fine chemicals.

The Anisole market is largely driven by its growing application in the pharmaceutical and cosmetic industries. With the increasing demand for active pharmaceutical ingredients (APIs) and perfumery compounds, the consumption of anisole has been steadily rising. Additionally, its role as a solvent in chemical synthesis and formulation contributes to consistent industrial usage, especially in developing countries with expanding manufacturing bases.

In terms of growth factors, rising investments in specialty chemicals and the expansion of fragrance and flavor industries are propelling the demand for anisole. The shift toward cleaner, more efficient chemical intermediates in fine chemical production also supports its growth. Its relative safety and ease of handling further boost its appeal for large-scale usage.

The demand for anisole is closely linked to consumer preferences in cosmetics and personal care. As natural-scented and organic products trend globally, manufacturers are using anisole-derived compounds to meet this demand. Its use in manufacturing synthetic anethole—a flavoring agent—also supports demand from the food and beverage industry.

Key Takeaways

- Global Anisole Market is expected to be worth around USD 240.9 Million by 2034, up from USD 161.2 Million in 2024, and grow at a CAGR of 4.1% from 2025 to 2034.

- Technical grade anisole dominates the market, accounting for 62.4% due to broad industrial usage.

- The pharmaceutical sector leads anisole consumption, holding a 34.8% share due to active ingredient production.

- Strong pharmaceutical and cosmetic industries drive Asia-Pacific’s anisole demand to USD 74.6 Mn.

By Grade Analysis

Technical-grade anisole holds a 62.4% share in the global anisole market.

In 2024, Technical Grade held a dominant market position in the By Grade segment of the Anisole Market, with a 62.4% share. This dominance is primarily attributed to its widespread use across multiple industrial applications, particularly in the synthesis of dyes, agrochemicals, and pharmaceuticals.

The cost-efficiency and functional performance of technical grade anisole make it a preferred choice for bulk production environments where ultra-high purity is not essential. Manufacturers across Asia-Pacific and Europe continue to rely heavily on technical grade formulations due to their consistent availability and compatibility with standard chemical processing setups.

The high adoption of technical grade anisole also stems from its use as an intermediate in the production of perfumes and flavors, especially in markets that prioritize scale and formulation stability over analytical purity. Additionally, its effectiveness as a solvent in laboratory and industrial chemistry supports continuous demand across chemical manufacturing clusters.

With industries such as cosmetics, personal care, and pharmaceuticals expanding in emerging economies, the preference for technical grade remains strong due to favorable pricing and sufficient purity levels for non-critical applications.

By End Use Analysis

The pharmaceutical sector contributes 34.8% to the total anisole market consumption.

In 2024, Pharmaceutical held a dominant market position in the By End Use segment of the Anisole Market, with a 34.8% share. This significant share reflects anisole’s critical role as an intermediate in the synthesis of various active pharmaceutical ingredients (APIs) and formulation agents.

The pharmaceutical industry extensively utilizes anisole in the development of analgesics, antipyretics, and other therapeutic compounds due to its stability and chemical versatility. The compound’s aromatic nature and functional group compatibility make it highly suitable for multi-step synthesis pathways commonly used in modern drug development.

The rising demand for over-the-counter and prescription medications, particularly in emerging healthcare markets, has further contributed to this segment’s lead. Pharmaceutical manufacturers prefer anisole for its consistent performance and ability to act as a precursor for several ether- and phenol-based drug molecules.

Additionally, stringent regulatory requirements in drug formulation have supported the demand for high-quality intermediates like anisole that meet industry safety and performance standards.

Key Market Segments

By Grade

- Technical Grade

- Food Grade

- Pharmaceutical Grade

- Cosmetic Grade

By End Use

- Pharmaceutical

- Food and Beverage

- Personal Care

- Chemical

- Agriculture

- Others

Driving Factors

Rising Pharmaceutical Manufacturing Drives Anisole Demand Globally

One of the biggest driving factors for the anisole market is the steady rise in pharmaceutical manufacturing across the world. Anisole is widely used as a chemical intermediate in the production of active pharmaceutical ingredients (APIs) and other drug compounds. As demand for medicines continues to increase—especially in developing countries—pharmaceutical companies are expanding their production lines.

This results in higher consumption of anisole, particularly the technical and pharmaceutical-grade variants. The growth in generic drugs and over-the-counter medications also supports this trend. Moreover, the pharmaceutical industry prefers anisole for its chemical stability and reliable performance in drug synthesis.

Restraining Factors

Health and Safety Concerns Limit Industrial Usage

One key restraining factor for the anisole market is the concern over its health and safety risks during handling and processing. Although anisole is widely used, it is still classified as a flammable and potentially harmful chemical if inhaled or exposed to the skin in large amounts. In industrial settings, improper storage or accidental leaks can lead to fire hazards or health issues for workers.

As a result, companies may be required to invest in strict safety measures, ventilation systems, and personal protective equipment, which increases operational costs. In some regions, environmental and occupational safety regulations are also becoming stricter, which can limit the use of anisole or slow down its adoption in sensitive applications.

Growth Opportunity

Eco-Friendly Production Methods Offer Future Potential

A major growth opportunity in the anisole market lies in developing eco-friendly production methods. Traditional synthesis of anisole often involves petrochemical feedstocks and harsh reaction conditions, which can raise environmental concerns. However, there is growing interest in producing anisole through greener, more sustainable processes, such as using renewable raw materials or cleaner catalysts.

This shift is supported by global efforts to reduce carbon emissions and chemical waste. Companies that invest in cleaner anisole production methods can gain an edge in markets with strict environmental rules. As industries like pharmaceuticals and cosmetics look for cleaner supply chains, demand for sustainably sourced anisole is likely to grow, offering long-term benefits for both producers and end users.

Latest Trends

Growing Demand for High-Purity Anisole in Pharmaceuticals

A notable trend in the anisole market is the increasing demand for high-purity anisole, especially within the pharmaceutical industry. As drug formulations become more complex, there’s a heightened need for ultrapure intermediates to ensure the efficacy and safety of medications.

High-purity anisole serves as a crucial component in synthesizing various active pharmaceutical ingredients (APIs). The shift towards stringent quality standards in drug manufacturing has propelled the adoption of anisole with purity levels exceeding 99.5%.

This trend is further supported by advancements in purification technologies, enabling manufacturers to produce anisole that meets the rigorous requirements of modern pharmaceutical applications. As the global healthcare sector continues to expand, the demand for high-purity anisole is expected to grow, reinforcing its significance in the production of safe and effective pharmaceuticals.

Regional Analysis

Asia-Pacific held a 46.3% share in the Anisole Market, reaching USD 74.6 Mn.

In 2024, Asia-Pacific emerged as the dominant region in the global Anisole Market, accounting for 46.3% of the total share, valued at USD 74.6 million. The region’s leadership is primarily driven by strong demand from the pharmaceutical and personal care industries, especially in countries like China, India, and Japan.

Rapid industrial growth and rising consumption of intermediates for fragrance, dyes, and drug formulations have made Asia-Pacific the focal point for anisole manufacturers. In contrast, North America and Europe maintain steady market shares, supported by established chemical manufacturing bases and ongoing innovations in synthetic organic compounds.

These regions benefit from a consistent need for anisole in the production of active pharmaceutical ingredients and fine chemicals, though growth is comparatively moderate. Meanwhile, the Middle East & Africa and Latin America represent emerging opportunities but currently hold a smaller market share due to limited domestic production and slower industrial uptake.

However, rising investments in local pharmaceutical and agrochemical sectors could support gradual demand growth in these regions. Overall, with nearly half of the market share, Asia-Pacific is expected to remain the key revenue contributor, backed by robust industrial infrastructure, expanding end-user sectors, and increasing preference for technical and pharmaceutical-grade anisole.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Arkema SA maintained a strong presence by leveraging its portfolio of specialty chemicals. The company’s integrated production capabilities and focus on high-purity intermediates supported its anisole supply for pharmaceutical and fragrance applications. Arkema’s strength lies in its ability to serve regulated markets with reliable quality standards, especially across Europe and North America.

Atul Ltd, an Indian chemical manufacturer, contributed notably to the Asia-Pacific anisole market. With a robust base in aromatic compounds, Atul’s vertical integration and backward-linked raw material sourcing helped maintain cost efficiency and supply consistency. Its proximity to high-growth pharmaceutical and agrochemical industries in India supported strong regional demand fulfillment.

BASF, a global chemical leader, continued to focus on offering high-performance intermediates, including anisole, within its diversified chemical segment. Its emphasis on innovation, regulatory compliance, and sustainability positioned it well in premium applications such as cosmetics and active pharmaceutical ingredients, particularly in developed economies.

Benzo Chem Industries Pvt. Ltd., also based in India, strengthened its market positioning through focused production of anisole and related aromatic intermediates. The company’s specialty approach, supported by reliable exports and growing domestic demand, enabled it to serve customers across pharmaceuticals, dyes, and fragrances efficiently.

Top Key Players in the Market

- Arkema SA

- Atul Ltd

- BASF

- Benzo Chem Industries Pvt. Ltd.

- Camlin Fine Sciences Ltd.

- Emmennar Pharma Pvt. Ltd.

- Huntsman Corporation

- Merck KGaA

- Solvay

- SURYA LIFE SCIENCES LTD.

- Tokyo Chemical Industry Co., Ltd.

Recent Developments

- In May 2025, Huntsman announced the commissioning of a new purification and packaging unit under its E-GRADE® product line at its Conroe, Texas, facility. This unit is designed to produce high-purity, low-trace metal amines, including quaternary amines and amine oxides, essential for semiconductor chip manufacturing.

- In April 2025, Merck KGaA entered into a definitive agreement to acquire SpringWorks Therapeutics, a U.S.-based biopharmaceutical company, for approximately $3.9 billion. This acquisition is expected to strengthen Merck’s presence in the United States and expand its portfolio in the treatment of rare tumors.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 161.2 Million |

| Forecast Revenue (2034) | USD 240.9 Million |

| CAGR (2025-2034) | 4.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade (Technical Grade, Food Grade, Pharmaceutical Grade, Cosmetic Grade), By End Use (Pharmaceutical, Food and Beverage, Personal Care, Chemical, Agriculture, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Arkema SA, Atul Ltd, BASF, Benzo Chem Industries Pvt. Ltd., Camlin Fine Sciences Ltd., Emmennar Pharma Pvt. Ltd., Huntsman Corporation, Merck KGaA, Solvay, SURYA LIFE SCIENCES LTD., Tokyo Chemical Industry Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |