Global Aluminum Hydroxide Market Size, Share and Report Analysis By Grade (Pharma Grade, Industrial Grade, Others), By Manufacturing Process (Bayer Process, Lime-Soda Process, Sinter Process), By Application (Flame-Retardant and Smoke-Suppressant, Filler and Pigment, Antacid, Water-Treatment Chemicals, Catalyst, Others), By End-use (Construction, Pharmaceuticals, Automotive, Electronics, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 179632

- Number of Pages: 353

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

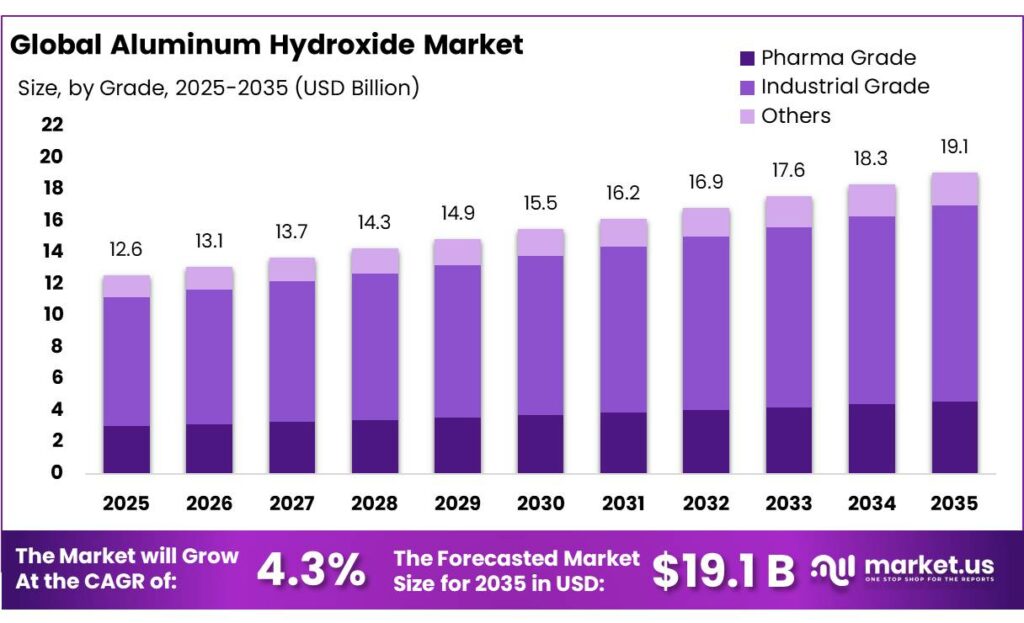

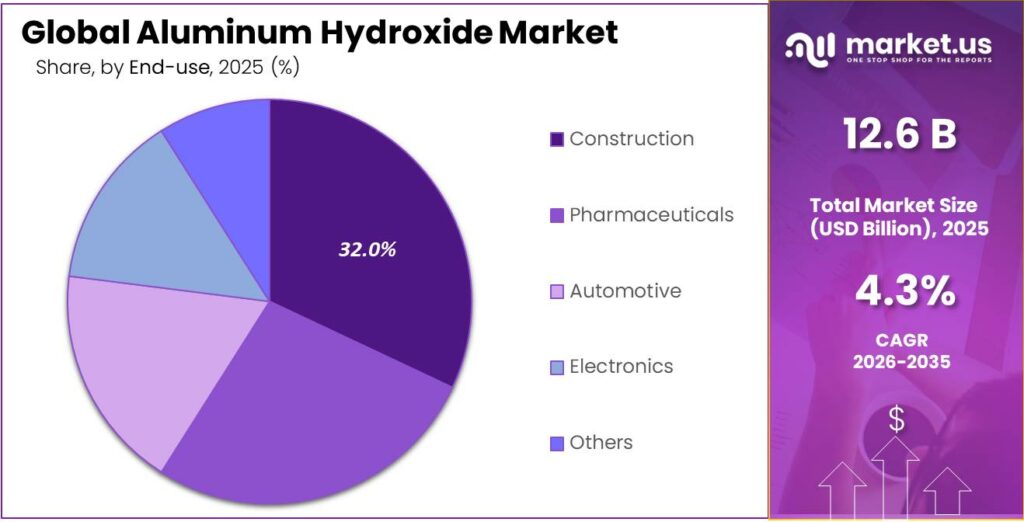

The Global Aluminum Hydroxide Market is expected to be worth around USD 19.1 Billion by 2035, up from USD 12.6 Billion in 2025, at a CAGR of 4.3% from 2026 to 2035. The Asia Pacific segment maintained 43.4%, supporting a Aluminum Hydroxide value of USD 5.4 Bn.

Aluminium hydroxide is positioned at the crossroads of mining, chemicals, pharmaceuticals and food processing. Industrially it is produced mainly as a hydrate intermediate in the Bayer process and then refined into alumina or specialty grades for flame-retardant fillers, antacids, water treatment and food additives.

- According to the U.S. Geological Survey, about 76% of mined bauxite is refined by the Bayer process into alumina or aluminium hydroxide, with the remainder going to cement, abrasives and other niche uses.

Capacity expansion in major producing countries underpins raw material availability for aluminium hydroxide producers. India’s Ministry of Mines notes that China’s bauxite output rose from 9.8 million tonnes in 2001 to 93 million tonnes in 2023, a 9.5-fold increase, while alumina production reached 82 million tonnes, representing about 60% of global alumina output. In contrast, U.S. alumina production was an estimated 920,000 tonnes in 2022, about 8% lower than in 2021, highlighting regional shifts in refining activity.

In food and pharmaceuticals, regulatory benchmarks from global public-health bodies frame both risk and opportunity for aluminium hydroxide. The Joint FAO/WHO Expert Committee on Food Additives (JECFA) established a provisional tolerable weekly intake of 2 mg of aluminium per kg body weight for total aluminium from all food sources, including additives. The European Food Safety Authority (EFSA) has adopted a more conservative tolerable weekly intake of 1 mg aluminium per kg body weight.

Recent dietary exposure assessments reinforce this margin of safety, which in turn supports stable industrial demand. A probabilistic intake study in infants 0–36 months estimated mean aluminum intakes of 0.184 mg/kg body weight per week and 95th-percentile intakes of 0.474 mg/kg body weight per week—both below the 1–2 mg/kg body weight weekly limits set by EFSA and JECFA.

Regulation of aluminum in food and health applications is an important structural driver. The European Food Safety Authority (EFSA) set a tolerable weekly intake (TWI) of 1 mg aluminum per kilogram of body weight per week in 2008.

- The Joint FAO/WHO Expert Committee on Food Additives (JECFA) revised its provisional tolerable weekly intake for aluminum compounds to 2 mg/kg body weight in 2011, based on a NOAEL of 30 mg/kg body weight per day. EFSA’s exposure assessment indicated mean dietary intakes for adults between 0.2 and 1.5 mg/kg body weight per week, and higher values of roughly 0.7–2.3 mg/kg for children and adolescents.

Key Takeaways

- Aluminum Hydroxide Market is expected to be worth around USD 19.1 Billion by 2035, up from USD 12.6 Billion in 2025, at a CAGR of 4.3%.

- Industrial Grade held a dominant market position, capturing more than a 65.2% share.

- Bayer Process held a dominant market position, capturing more than a 76.3% share.

- Flame-Retardant and Smoke-Suppressant held a dominant market position, capturing more than a 41.8% share.

- Construction held a dominant market position, capturing more than a 32.7% share.

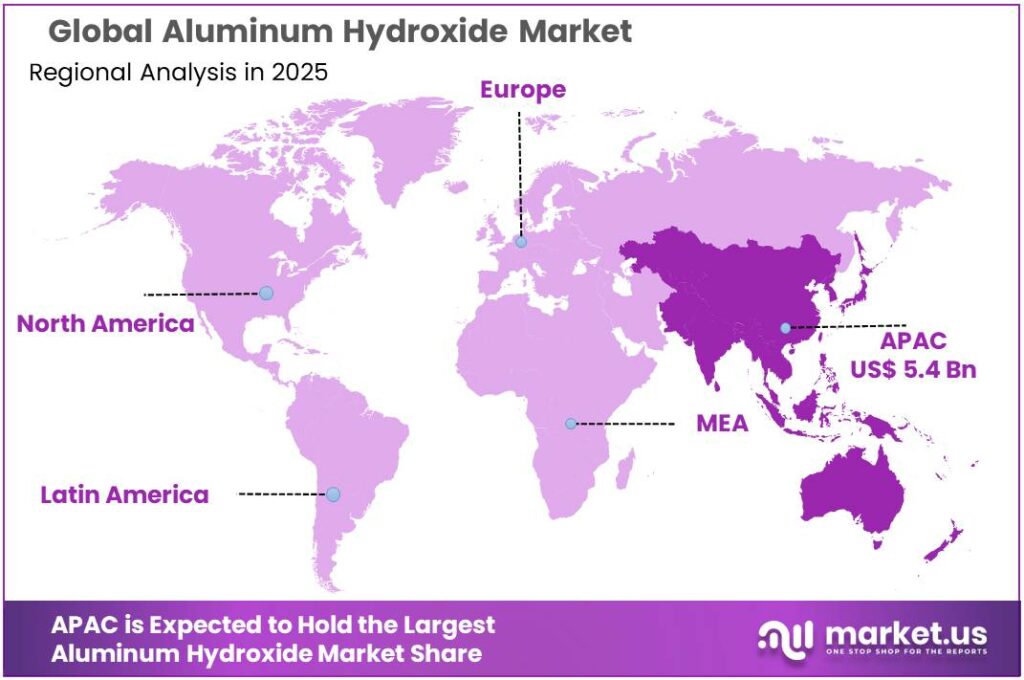

- Asia Pacific held a dominant position in the aluminum hydroxide market, capturing more than a 43.4% share, with regional demand estimated at around USD 5.4 billion.

By Grade Analysis

Industrial Grade Aluminum Hydroxide leads the market with a strong 65.2% share.

In 2024, Industrial Grade held a dominant market position, capturing more than a 65.2% share, driven by its extensive use across plastics, rubber, electrical cables, engineered composites, and construction materials. Industrial customers favor this grade because it offers consistent particle size, good flame-retardant efficiency, and reliable thermal stability, making it a preferred additive in halogen-free formulations.

What further supports its scale is the steady supply of upstream alumina and the expansion of manufacturing clusters in Asia, where cable and polymer processing industries continue to grow. During 2024, demand for industrial-grade aluminum hydroxide increased noticeably, supported by rising consumption in electrical insulation materials and the shift toward safer, environmentally conscious flame-retardant systems.

By Manufacturing Process Analysis

Bayer Process dominates the market with a strong 76.3% share.

In 2024, Bayer Process held a dominant market position, capturing more than a 76.3% share, mainly because it remains the most efficient and scalable method for producing high-purity aluminum hydroxide. This process allows manufacturers to achieve consistent quality, controlled particle distribution, and large-volume production—features heavily favored by industries such as flame-retardant fillers, water treatment, engineered materials, and pharmaceuticals.

The strong availability of alumina refineries operating on the Bayer route in major producing regions further reinforced its lead in 2024. The method’s ability to support cost-effective, mass-scale output made it the preferred choice for manufacturers that depend on stable supply and uniform product grades for downstream formulations.

By Application Analysis

Flame-Retardant and Smoke-Suppressant dominates the market with a solid 41.8% share.

In 2024, Flame-Retardant and Smoke-Suppressant held a dominant market position, capturing more than a 41.8% share, reflecting the growing global shift toward safer and cleaner material technologies. Aluminum hydroxide plays a central role in halogen-free flame-retardant systems used in electrical cables, insulation materials, building panels, automotive components, and consumer electronics.

Its ability to release water during decomposition helps reduce heat, suppress smoke generation, and delay ignition, making it highly valuable in industries that prioritize safety standards. Through 2024, stricter fire-safety regulations in construction and transportation supported steady demand, alongside consistent use in wire coatings and polymer-based materials where low toxicity and smoke reduction are essential.

By End-use Analysis

Construction sector leads the market with a strong 32.7% share.

In 2024, Construction held a dominant market position, capturing more than a 32.7% share, largely because aluminum hydroxide has become a preferred ingredient in materials where fire safety, durability, and reliability are non-negotiable. Its widespread use in building panels, insulation boards, flooring materials, sealants, and cable insulation reflects the industry’s shift toward halogen-free and low-smoke solutions.

As construction projects expanded across residential and commercial sectors in 2024, the demand for fire-resistant polymers and coatings grew steadily, reinforcing the role of aluminum hydroxide as a key additive. Builders and material manufacturers continued to adopt it due to its stable performance, low toxicity, and ability to meet tightening fire-safety standards.

Key Market Segments

By Grade

- Pharma Grade

- Industrial Grade

- Others

By Manufacturing Process

- Bayer Process

- Lime-Soda Process

- Sinter Process

By Application

- Flame-Retardant and Smoke-Suppressant

- Filler and Pigment

- Antacid

- Water-Treatment Chemicals

- Catalyst

- Others

By End-use

- Construction

- Pharmaceuticals

- Automotive

- Electronics

- Others

Emerging Trends

Surge in halogen-free, food-safe flame-retardant systems is redefining aluminum hydroxide use

A clear, recent trend for aluminum hydroxide is its growing role in halogen-free, low-smoke materials used around food, cold chains and modern food plants. The Food and Agriculture Organization (FAO) reports that 13.2% of food is lost between harvest and retail, and a further 19% is wasted at retail, in food service and households. These losses and waste together account for 8–10% of global greenhouse-gas emissions. The UN Environment Programme’s Food Waste Index work shows that in 2022, 1.05 billion tonnes of food were wasted by households, food service and retail – about 19% of food available to consumers – while around 783 million people faced hunger.

On the policy side, the EU Farm to Fork Strategy under the Green Deal is pushing Europe toward “fair, healthy and environmentally-friendly food systems,” with measures on sustainable production, processing and food contact materials. Part of this agenda is safer infrastructure: better insulation, safer wiring, and building products that are not only fire-resistant but also low in toxic smoke and compliant with stricter food-plant standards. At the same time, FAO and UNEP steward SDG target 12.3, which aims to halve per-capita food waste at the retail and consumer level and reduce losses along supply chains by 2030.

Governments are also tightening rules around wiring and cable safety in ways that directly favour aluminum-hydroxide-rich HFFR formulations. In India, for example, BIS certification and ISI marking have been made mandatory for all halogen-free flame-retardant cables since 1 August 2020, raising the bar for fire performance and smoke toxicity in critical installations.

Put together, these food-system and safety policies mean that every new cold store, processing plant, supermarket distribution hub or data-rich logistics centre built to reduce the 13.2% food loss and 19% waste problem is likely to contain more aluminum-hydroxide-based cables, panels and coatings than the facilities they replace. Over time, this steady, regulation-backed shift toward food-safe, halogen-free fire protection stands out as one of the strongest and most durable trends shaping the aluminum hydroxide market.

Drivers

Growing demand for safer, halogen-free materials in food facilities and cold-chain infrastructure

A major driving factor for the aluminum hydroxide market today is the surging global push to modernize food systems, strengthen cold-chain infrastructure, and improve safety across food-processing, storage and distribution environments. Food systems worldwide are facing unprecedented pressure to reduce losses, improve hygienic standards and ensure safer operations.

- According to the Food and Agriculture Organization (FAO), about 13.2% of all food produced is lost between harvest and retail, and an additional 19% is wasted at retail, in food service, and in households.

Governments and global organizations now view safer infrastructure—cold rooms, logistics hubs, processing lines, warehouses and packaging plants—as essential to reducing these losses. This is where aluminum hydroxide plays a central role. As a halogen-free flame retardant and smoke suppressant, it is widely used in power cables, insulations, wall systems, coated panels and polymer components found throughout food-handling and cold-storage environments.

The urgency of upgrading food-system infrastructure is backed by strong data. The UN Environment Programme (UNEP) reports that in 2022, food waste reached 1.05 billion tonnes, nearly one-fifth of all food available to consumers, while 783 million people still faced hunger. These numbers have pushed countries to adopt policies aligned with SDG Target 12.3, which aims to halve per-capita food waste by 2030 and reduce losses throughout supply chains.

Sustainable Energy for All estimates that 13% of all food produced—around 526 million tonnes—is lost every year due to inadequate cold chains, with the potential to feed nearly 950 million people if properly preserved. Upgrading these systems requires fire-safe, halogen-free materials, particularly in electrical wiring and insulated composite structures.

Restraints

Strict food-safety limits on aluminium exposure are slowing broader use of aluminum hydroxide

A major restraining factor for the aluminum hydroxide market is the tight regulatory cap on aluminium intake in food and health applications, which makes large buyers in the food, beverage, infant nutrition and pharmaceutical sectors very cautious. The European Food Safety Authority (EFSA) has recommended a tolerable weekly intake (TWI) of 1 mg aluminium per kilogram of body weight per week from all dietary sources.

- EFSA’s exposure work shows that many Europeans are already close to that ceiling: average weekly intakes were estimated in the range of 0.2–1.5 mg/kg body weight for adults, and 0.7–2.3 mg/kg body weight for children and young people, meaning a significant share of the population can exceed the TWI depending on diet.

Global food-safety bodies have reinforced this cautious stance. The Joint FAO/WHO Expert Committee on Food Additives (JECFA) set a provisional tolerable weekly intake (PTWI) of 2 mg/kg body weight for total aluminium, covering all aluminium compounds in food, including aluminium-based additives. That figure was derived from a no-observed-adverse-effect level (NOAEL) of 30 mg/kg body weight per day, applying a standard safety factor of 100.

Even though the PTWI is numerically higher than EFSA’s TWI, both benchmarks are low enough that high-aluminium product concepts quickly run into regulatory and public-health concerns. A recent European risk-assessment exercise found that children aged 3–6 years can reach mean weekly aluminium intakes of 0.64 mg/kg body weight, and 95th-percentile values of 1.02 mg/kg body weight, already hitting or slightly exceeding EFSA’s 1 mg/kg TWI.

Governments have translated these scientific opinions into concrete restrictions. The European Union’s Commission Regulation (EU) No 380/2012 amended Annex II of Regulation (EC) No 1333/2008 by tightening the conditions of use and use levels for aluminium-containing food additives. In practice, this regulation removed some aluminium silicates from the approved list and introduced lower maximum levels or narrower permitted categories for several aluminium-containing additives.

Opportunity

Expanding cold chains and safer food infrastructure open a big growth window for aluminum hydroxide

One of the clearest growth opportunities for aluminum hydroxide sits inside the global push to fix food loss, food waste and cold-chain gaps. The Food and Agriculture Organization (FAO) estimates that 13.2% of food is lost in the supply chain after harvest and before retail, and another 19% is wasted at retail, in food service and in households. Combined, food loss and waste are responsible for around 8–10% of global greenhouse-gas emissions, making them a major climate issue as well as a food-security problem.

- The UN Environment Programme (UNEP) Food Waste Index 2024 puts some hard numbers on this: in 2022, food waste reached 1.05 billion tonnes, almost one-fifth of all food available to consumers, while 783 million people experienced hunger in the same year.

Cold-chain infrastructure is one of the biggest levers, and here aluminum hydroxide has real room to grow. Sustainable Energy for All reports that 13% of all food production is lost because of missing or weak cold chains, equivalent to 526 million tonnes of food every year, enough to feed around 950 million people.

The same analysis notes that food loss and waste cost nearly USD 1 trillion per year and that closing cooling gaps could cut these losses sharply. To support this, FAO and UNEP act as custodians of SDG target 12.3, which calls for halving per-capita food waste at retail and consumer level and reducing food losses along production and supply chains by 2030.

Policy frameworks reinforce this trajectory. FAO’s SDG monitoring shows no real progress in reducing food losses since 2015, with global post-harvest and pre-retail losses climbing slightly to 13.3% in 2023, underlining the need for new investment in storage, transport and processing infrastructure. Sustainable Energy for All estimates that enabling policies for sustainable cold chains translate into an investment opportunity of about USD 270 billion in supply-chain infrastructure and efficiency upgrades.

Regional Insights

Asia Pacific leads the aluminum hydroxide market with a 43.4% share, worth about USD 5.4 billion.

In 2024, Asia Pacific held a dominant position in the aluminum hydroxide market, capturing more than a 43.4% share, with regional demand estimated at around USD 5.4 billion. This leadership is underpinned by the region’s role as the manufacturing and infrastructure hub of the world. Asia Pacific is home to more than half of the global population, which concentrates construction, power, automotive, and electronics activity in a relatively compact geography.

Construction alone is a major pillar: recent infrastructure analysis shows that Asia-Pacific accounts for roughly 39.7% of global construction industry value, underscoring how much cement, steel, cables, insulation, and composite panels are being installed in this region. Those same materials are key outlets for aluminum-hydroxide-based flame-retardant and smoke-suppressant systems.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Alteo is a major specialty alumina and hydrate supplier into flame-retardant and technical polymer markets. It runs over 700 kt/year of specialty alumina capacity and generates around €280 million in annual turnover, serving roughly 600 customers across 60 countries and about 1,000 delivery sites.

Chalco is one of the largest integrated alumina and aluminum groups and a leading producer of chemical alumina and aluminum hydroxide grades. Its chemical-alumina operations in Shandong, Zhongzhou and Zhengzhou provide around 1.05 million tons per year of capacity, positioning Chalco as the world’s largest chemical alumina producer and supplier.

Sumitomo Chemical offers a broad portfolio of aluminum hydroxide and alumina products engineered via a controlled Bayer precipitation process. Its aluminum hydroxide line covers low-viscosity ATH, high-loading ATH and thermally conductive filler grades, all under CAS No. 21645-51-2, tailored for flame-retardant CCL, solid surface materials and polymer compounds.

Top Key Players Outlook

- Almatis

- Alteo

- ALUMINA – CHEMICALS & CASTABLES

- Chalco

- Sumitomo Chemical Co. Ltd.

- Huber Materials.

- Sibelco

- LKAB Minerals AB

- Donau Carbon GmbH

- TOR Minerals International, Inc.

- Hindalco

Recent Industry Developments

In 2025, Sumitomo Chemical Co. Ltd aimed for a 30% increase in ultrahigh purity alumina (derived from aluminum hydroxide) sales revenue compared to 2023, highlighting demand growth for highly engineered materials with particle sizes of 150 nm or less for electronics and energy applications.

In 2024, Sibelco reported €2,225 million in revenue, up 6% from 2023, and €471 million in EBITDA, growing 14% year-over-year, reflecting resilience and market demand for industrial minerals even under challenging conditions.

Report Scope

Report Features Description Market Value (2025) USD 12.6 Bn Forecast Revenue (2035) USD 19.1 Bn CAGR (2026-2035) 4.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Grade (Pharma Grade, Industrial Grade, Others), By Manufacturing Process (Bayer Process, Lime-Soda Process, Sinter Process), By Application (Flame-Retardant and Smoke-Suppressant, Filler and Pigment, Antacid, Water-Treatment Chemicals, Catalyst, Others), By End-use (Construction, Pharmaceuticals, Automotive, Electronics, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Almatis, Alteo, ALUMINA – CHEMICALS & CASTABLES, Chalco, Sumitomo Chemical Co. Ltd., Huber Materials., Sibelco, LKAB Minerals AB, Donau Carbon GmbH, TOR Minerals International, Inc., Hindalco Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Almatis

- Alteo

- ALUMINA - CHEMICALS & CASTABLES

- Chalco

- Sumitomo Chemical Co. Ltd.

- Huber Materials.

- Sibelco

- LKAB Minerals AB

- Donau Carbon GmbH

- TOR Minerals International, Inc.

- Hindalco

Our Clients

- 179632

- Feb 2026