Quick Navigation

Report Overview

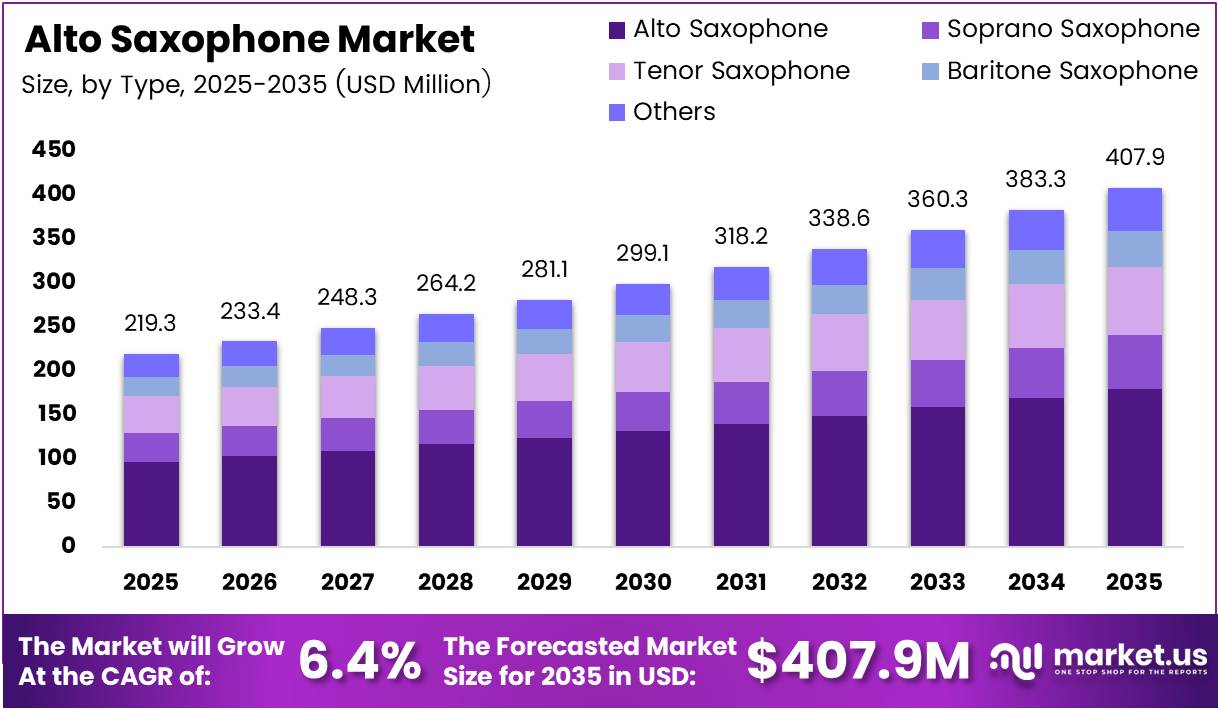

Global Alto Saxophone Market size is expected to be worth around USD 407.9 Million by 2035 from USD 219.3 Million in 2025, growing at a CAGR of 6.4% during the forecast period 2026 to 2035.

The alto saxophone market covers the design, manufacture, and distribution of alto saxophones across student, amateur, and professional segments. Demand concentrates in school music programs, jazz education, and live performance communities. Brick-and-mortar instrument retailers and online channels both serve distinct buyer segments with different price sensitivities.

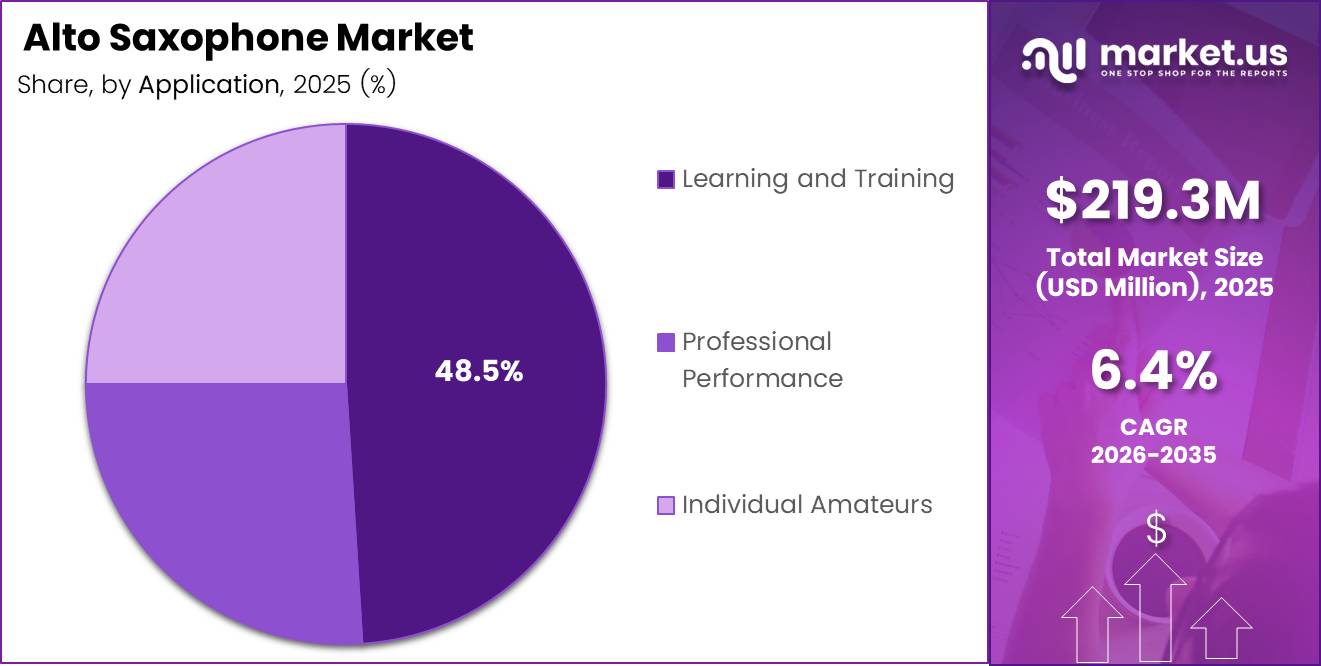

Learning and training applications anchor 48.5% of total market demand. This concentration reflects how deeply institutional music education drives first-time instrument purchases. When school budgets fund instrument programs, manufacturers benefit from predictable, recurring procurement cycles that stabilize revenue even during discretionary spending slowdowns.

The alto saxophone holds 43.9% share within the broader saxophone type segment. Its role as the standard entry instrument in school band programs gives it structural demand advantages over tenor or baritone variants. Music educators consistently recommend it as the first saxophone type, creating a self-reinforcing pipeline from student to lifelong player.

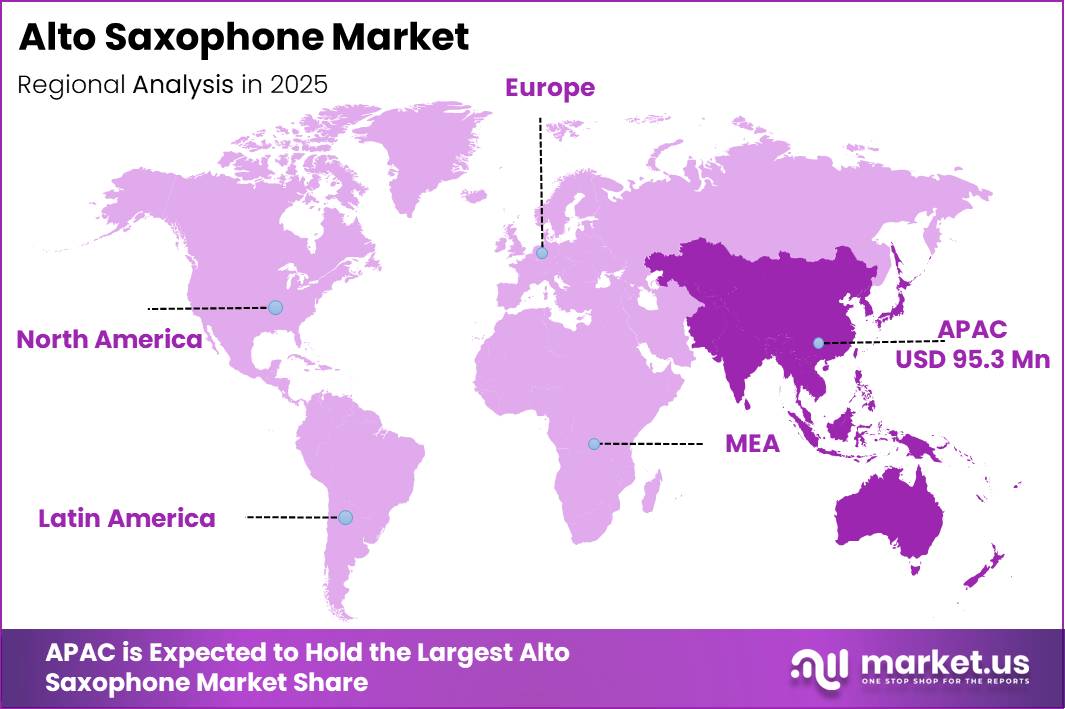

Asia Pacific leads the global market with a 43.50% share valued at USD 95.3 Million. Manufacturing concentration in China and Japan, combined with school enrollment scale across the region, positions APAC as both the production hub and one of the fastest-growing consumer bases. This dual role gives regional manufacturers a cost and distribution advantage that Western brands must navigate carefully.

In January 2026, Selmer Paris officially discontinued the Series III Alto saxophone, repositioning the Signature Alto as the evolution of the Super Action 80 Series II. This signals an intentional shift toward premium consolidation — manufacturers are narrowing product lines to protect margin and reinforce brand hierarchy rather than competing on volume.

According to the NAMM Foundation, over 1,000 school districts and individual schools across more than 46 U.S. states received the 26th-annual Best Communities for Music Education Award in May 2025, including 103 first-time winners. This breadth of institutional recognition signals active policy-level support for music education, which directly translates into sustained instrument procurement at the district level.

According to the ABRSM 2025 Making Music UK report, 84% of young people recognized music’s positive influence on their mental health, and 87% of music teachers viewed musical engagement as essential to students’ wellbeing. These figures reframe instrument learning as a wellness investment — a positioning shift that gives manufacturers and educators a compelling non-academic argument for sustained program funding.

Key Takeaways

- The Global Alto Saxophone Market was valued at USD 219.3 Million in 2025 and is forecast to reach USD 407.9 Million by 2035.

- The market advances at a CAGR of 6.4% over the forecast period 2026 to 2035.

- By Type, Alto Saxophone leads with 43.9% market share, driven by its status as the standard beginner instrument in school band programs.

- By Application, Learning and Training dominates with 48.5% share, reflecting institutional procurement from schools and music academies.

- By Distribution Channel, Brick-and-Mortar Stores command 62.4% share, as players prefer in-person testing before high-value instrument purchases.

- Asia Pacific holds the largest regional share at 43.50%, valued at USD 95.3 Million, supported by manufacturing scale and school enrollment growth.

Type Analysis

Alto Saxophone dominates with 43.9% due to universal adoption in school band programs.

In 2025, Alto Saxophone held a dominant market position in the By Type segment of the Alto Saxophone Market, with a 43.9% share. Music educators consistently designate it as the entry-level saxophone type, creating a self-reinforcing demand cycle from first-time student buyers through to adult enthusiasts. This institutional anchoring insulates alto saxophone sales from discretionary spending fluctuations more effectively than any other type.

Soprano Saxophone serves a specialist role within professional and advanced amateur segments. Its smaller form factor and brighter tonal register attract jazz soloists and chamber musicians, but its intonation difficulty makes it unsuitable for beginners. Consequently, soprano demand concentrates in the upper price tiers, where buyers prioritize acoustic character over accessibility.

Tenor Saxophone carries strong appeal in jazz, rock, and blues performance contexts where a deeper, warmer tone is preferred. It competes closely with alto in school programs at the secondary level but requires greater lung capacity, limiting early adoption. This positions tenor as a secondary purchase for players who progress beyond the alto.

Baritone Saxophone differentiates through its role in ensemble harmonics rather than solo performance. Demand is structurally limited by its size, weight, and higher price point, which restrict it to advanced school ensembles and professional orchestras. However, it commands above-average unit margins precisely because buyers in this segment prioritize quality over cost.

Others in the type segment — including sopranino and bass saxophones — serve niche collector, experimental, and orchestral markets. Their low volume contribution limits broad commercial significance, but they attract premium pricing and sustain brand prestige for manufacturers who offer complete saxophone family portfolios.

Application Analysis

Learning and Training dominates with 48.5% due to deep integration in institutional music curricula.

In 2025, Learning and Training held a dominant market position in the By Application segment of the Alto Saxophone Market, with a 48.5% share. School band programs, university music departments, and private music academies collectively anchor this segment. When institutions standardize the alto saxophone as the beginner instrument of choice, manufacturers benefit from high-volume, repeat procurement cycles driven by annual student enrollment rather than individual purchase decisions. In January 2026, ABRSM launched its new Woodwind Syllabus featuring 400 new pieces and a total of 2,000 pieces across woodwind instruments from Grade 1 to Grade 8, directly expanding structured learning content that sustains institutional demand.

Professional Performance applications attract the highest average transaction values in this market. Touring musicians, studio session players, and ensemble performers demand instruments with consistent intonation, durable key mechanisms, and superior tonal projection. This segment is smaller by volume but disproportionately influences brand perception and product roadmap decisions across the industry.

Individual Amateurs represent the most price-sensitive buyer group in the market. These purchasers balance instrument quality against personal budget constraints, making mid-tier product positioning critical for volume sales. Rental-to-own programs and online retail accessibility have expanded this segment’s reach, particularly among adult learners returning to music after extended breaks.

Distribution Channel Analysis

Brick-and-Mortar Stores dominate with 62.4% due to buyer preference for in-person acoustic testing.

In 2025, Brick-and-Mortar Stores held a dominant market position in the By Distribution Channel segment of the Alto Saxophone Market, with a 62.4% share. Instrument buyers — particularly students guided by music teachers and parents — rely on physical stores for product demonstration, professional fitting advice, and immediate repair access. Alto saxophones require hands-on evaluation before purchase, which sustains the structural advantage of specialist retail over digital channels. In January 2026, Cannonball Musical Instruments launched the Big Bell Stone Series 30th Anniversary Edition alto and tenor saxophones in Black Sapphire and matte black finishes — a limited-edition product type that benefits directly from in-store display and premium retail presentation.

Online Retail serves as an expanding channel for consumables, accessories, replacement parts, and entry-level instrument purchases. Price comparison convenience and global brand accessibility give online platforms an advantage in the amateur and beginner segments. However, the inability to test tone quality and playability before purchase continues to limit online penetration among mid-to-high-end buyers.

Key Market Segments

By Type

- Alto Saxophone

- Soprano Saxophone

- Tenor Saxophone

- Baritone Saxophone

- Others

By Application

- Learning and Training

- Professional Performance

- Individual Amateurs

By Distribution Channel

- Brick-and-Mortar Stores

- Online Retail

Drivers

School Band Programs and Jazz Education Mandates Sustain Structural Alto Saxophone Demand

School music programs remain the most reliable demand driver in this market. The alto saxophone’s status as the standard beginner instrument in school band curricula creates predictable, institution-level procurement that individual consumer spending cannot replicate. When schools commit to music education, instrument purchases follow automatically — making school enrollment a more meaningful leading indicator than consumer sentiment.

Jazz education programs at university level further sustain demand among older, higher-spending buyers. University music departments standardize the alto saxophone for foundational jazz coursework, creating a second procurement wave after initial school adoption. According to a robot-assisted learning study (Kumamoto University, 2026), a technology-supported training system reduced pitch error in 81.8% of novice participants with statistical significance (p = 0.022), demonstrating that structured learning tools measurably improve outcomes — a finding that strengthens the case for institutional investment in guided saxophone programs.

Independent artist culture and live performance expansion add a consumer-side demand layer. As musicians build direct audience relationships through streaming and live events, instrument investment shifts from institutional to personal. This trend broadens the buyer base beyond students and professionals, pulling Individual Amateur demand into the growth mix alongside the institutional foundation already established by school and university programs.

Restraints

High Instrument Costs and Financial Barriers Limit Market Penetration Among New Players

Cost remains the clearest structural barrier in this market. According to the ABRSM 2025 Making Music UK report, 29% of non-learners cited financial cost as the primary reason for not pursuing music lessons. This figure reveals that nearly one-third of the potential addressable market self-selects out before reaching the instrument purchase stage — a meaningful compression of demand that pricing strategy alone cannot fully resolve.

Repair and maintenance costs compound the initial purchase barrier significantly. According to Woodwind London (2025), saxophone servicing in the UK ranges from £30–£50 for individual repairs to £350–£450 for a full repad or overhaul, with strip-and-rebuild work reaching £400–£500+. For student and amateur players, these ongoing costs can equal or exceed annual rental fees — creating a persistent deterrent to long-term instrument ownership at the mid-market level.

Declining wind instrument participation in certain developed regions adds a structural constraint that marketing cannot easily overcome. Cultural shifts away from formal ensemble training in favor of digital music production reduce the school-age pipeline that historically fed professional and amateur saxophone demand. Manufacturers targeting growth must look to emerging markets and digital-assisted learning formats to offset this attrition in traditional Western demand centers.

Growth Factors

Smart Technology Integration and Online Retail Expansion Open New Revenue Channels for Alto Saxophone Manufacturers

Lightweight and portable alto saxophone designs address a practical gap that standard instruments leave unserved — student and travel use cases where full-sized instruments are impractical. Manufacturers who develop ergonomically adapted models can access a buyer segment that currently defers purchases due to transport limitations. This is incremental revenue, not a replacement cycle.

Online musical instrument retail channels extend brand reach to buyers in markets where specialist physical stores are unavailable. Global accessibility removes the geographic ceiling that brick-and-mortar distribution imposes. In January 2026, Ashun Sound Machines introduced the Diosynth electronic wind instrument at approximately USD 1,100, demonstrating how digitally-distributed, direct-to-consumer instrument launches can generate international sales without traditional dealer infrastructure.

Smart sensor technology integration creates a new product category — instruments that provide real-time digital feedback on tone, pitch, and technique. According to a Politecnico di Milano and McGill University study (Forum Acusticum 2025), a feedforward neural network achieved an R² of 0.9883 for predicting alto saxophone mouthpiece acoustic input impedance, compared to 0.8143 for linear regression. This accuracy level validates AI-driven acoustic modeling as a credible engineering tool, opening a path toward instrument customization services and smart learning accessories that carry higher margins than standard instrument sales.

Emerging Trends

Hybrid Acoustic-Digital Integration and Sustainable Manufacturing Reshape Alto Saxophone Product Strategy

Vintage-style alto saxophone designs with retro finishing and classic tonal aesthetics are attracting buyers who value aesthetic heritage alongside acoustic performance. This trend signals that product differentiation is increasingly visual and cultural — not just technical. Manufacturers who invest in heritage-inspired finishes can command premium pricing without requiring fundamental instrument redesign.

Eco-friendly brass processing and sustainable manufacturing practices are moving from optional to expected among premium buyers. Environmental criteria now influence purchasing decisions in professional segments, and manufacturers who cannot demonstrate responsible sourcing face reputational risk. In January 2026, JJ Babbitt and Theo Wanne merged, with Meyer and Otto Link mouthpieces now hand-finished by Theo Wanne — a consolidation move that concentrates artisan manufacturing expertise and positions the combined entity to compete on craftsmanship and sustainable quality rather than scale alone.

According to a Yamaha R&D study (Forum Acusticum 2025), a beginner player’s RMS amplitude and spectral centroid of a sustained Eb4 long tone approximately doubled from the start to end of a 3-month daily training program. This measurable acoustic improvement validates technology-assisted learning as a quantifiable outcome — a finding that manufacturers of smart accessories and hybrid acoustic-electronic alto saxophones can use directly in product positioning to justify premium pricing with evidence-based performance claims.

Regional Analysis

Asia Pacific Dominates the Alto Saxophone Market with a Market Share of 43.50%, Valued at USD 95.3 Million

Asia Pacific commands 43.50% of the global alto saxophone market, valued at USD 95.3 Million. China and Japan anchor this position through large-scale manufacturing infrastructure and deep school music program networks. The region’s role as both primary producer and fast-expanding consumer base gives it a structural cost and distribution advantage that other regions cannot replicate at equivalent scale.

North America Alto Saxophone Market Trends

North America sustains consistent alto saxophone demand through well-funded school band programs and a mature jazz education ecosystem. The NAMM Foundation’s recognition of over 1,000 schools across 46 U.S. states in 2025 reflects active institutional infrastructure for music education. However, rental pricing at USD 35.99–48.99 per month for alto saxophones signals a market where affordability barriers shape buyer behavior meaningfully.

Europe Alto Saxophone Market Trends

Europe presents a bifurcated demand structure. Western European markets — particularly the UK, France, and Germany — maintain structured examination systems like ABRSM that drive instrument purchases at clearly defined learning milestones. However, the ABRSM 2025 Making Music report identified noticeable participation drops at ages 12 and 15, pointing to a retention challenge that constrains the volume of mid-tier instrument upgrades manufacturers rely on for revenue growth.

Latin America Alto Saxophone Market Trends

Latin America’s alto saxophone market develops in parallel with expanding middle-class music education access in Brazil and Mexico. Cultural affinity for brass and wind instruments within regional music traditions creates organic demand that school programs reinforce. However, import costs and currency volatility make premium instrument pricing a persistent friction point for volume sales in this region.

Middle East and Africa Alto Saxophone Market Trends

The Middle East and Africa represent an early-stage market where institutional music education infrastructure remains limited but developing. Government investment in arts and education programs across Gulf states creates episodic demand for quality instruments. Accessibility through online retail channels offers the most practical near-term route to reaching buyers outside major urban centers in this region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Buffet Crampon positions itself at the intersection of heritage craftsmanship and modern manufacturing precision. The company’s August 2024 launch of a modernized production line featuring eco-friendly methods reflects a deliberate alignment with premium buyer expectations around sustainability. This approach lets Buffet Crampon defend its high price points not just on acoustic grounds but on responsible manufacturing credentials — a growing purchase criterion in professional and institutional segments.

Cannonball Musical Instruments differentiates through patented aesthetic innovation. The January 2026 launch of the Big Bell Stone Series 30th Anniversary Edition in Black Sapphire and matte black finishes — featuring sodalite stones under the company’s exclusive patent — demonstrates how proprietary design features can sustain premium pricing and brand loyalty simultaneously. Cannonball’s strategy targets professional and enthusiast buyers who treat instrument ownership as both artistic and personal expression.

Conn Selmer operates at scale across student, professional, and collectible market tiers. The January 2026 Conn Confirmation Saxophone — a limited edition of 150 units priced around USD 7,000, assembled in the USA — serves dual strategic purposes: celebrating 150 years of Conn heritage while generating high-margin, low-volume revenue from collector demand. This approach protects brand premium without cannibalizing volume student product lines.

Giardinelli maintains a focused positioning within the accessories and professional performance supply chain. Its strategic value lies in serving working musicians who require reliable, high-quality ancillary products alongside their primary instruments. In a market where brand loyalty compounds across product categories, Giardinelli’s accessories positioning creates recurring revenue opportunities that instrument-only competitors do not capture as efficiently.

Key Players

- Buffet Crampon

- Cannonball

- Conn Selmer

- Giardinelli

- KHS

- P. Mauriat

- Sahduoo Saxophone

- Selmer Paris

- Theo Wanne

- Yamaha

- Yanagisawa

Recent Developments

- August 2025 — Alto saxophone monthly rental rates at Hickey’s Music Center (USA) stand at $35.99/month (Standard) and $48.99/month (Deluxe), compared to $21.99–$31.99/month for flutes, clarinets, and trumpets — reflecting the premium cost position of alto saxophones within student rental programs.

- 2025 — Mad Music / Milano Music Center (Arizona, USA) set alto saxophone rental rates starting at $44.99/month, versus $24.99/month for flutes, clarinets, and trumpets, reinforcing the consistent price premium for alto saxophone rental across U.S. markets.

- November 2024 — KHS expanded its global distribution network for saxophone products to enhance market accessibility and customer service across international markets, broadening brand reach for student and mid-tier instrument buyers in underserved regions.

- January 2024 — Yamaha introduced the next-generation YAS-62 professional alto saxophone with improved key mechanisms and enhanced acoustic properties, reinforcing the company’s leadership in the professional educator and performance segment.

- March 2024 — Conn Selmer launched a comprehensive student saxophone program with integrated digital learning resources, directly addressing the institutional procurement market with a bundled instrument-plus-curriculum offering.

- June 2024 — Yanagisawa unveiled an innovative bronze saxophone series with advanced metallurgy and customizable acoustic characteristics, expanding material options for professional buyers who prioritize tonal distinctiveness over standard brass construction.

- January 2026 — Trevor James (Vancouver, Canada) launched the EVO soprano saxophone starting at USD 1,500, hand set-up by Sandro Masulo, bringing a new premium-accessible option to the soprano segment through targeted specialist distribution.

- January 2026 — Cloudvocal introduced the Eversync SP-10 wireless stomp pedal for saxophone performers, building on its Isolo Prime wireless mic system to serve the live performance segment with untethered monitoring and stage mobility solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 219.3 Million |

| Forecast Revenue (2035) | USD 407.9 Million |

| CAGR (2026-2035) | 6.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Alto Saxophone, Soprano Saxophone, Tenor Saxophone, Baritone Saxophone, Others), By Application (Learning and Training, Professional Performance, Individual Amateurs), By Distribution Channel (Brick-and-Mortar Stores, Online Retail) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Buffet Crampon, Cannonball, Conn Selmer, Giardinelli, KHS, P. Mauriat, Sahduoo Saxophone, Selmer Paris, Theo Wanne, Yamaha, Yanagisawa |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |