Global Frozen Vegetable Market Size, Share, And Business Benefits By Vegetable Type (Broccoli and Cauliflower, Green Peas, Asparagus, Mushrooms, Spinach, Corn, Green Beans, Others), By Nature (Organic, Conventional), By End Use (Retail Consumers, Food Service Industry, Food Manufacturing, Institutional Buyers), By Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Grocery Stores, Online Retailers, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: August 2025

- Report ID: 156620

- Number of Pages: 303

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

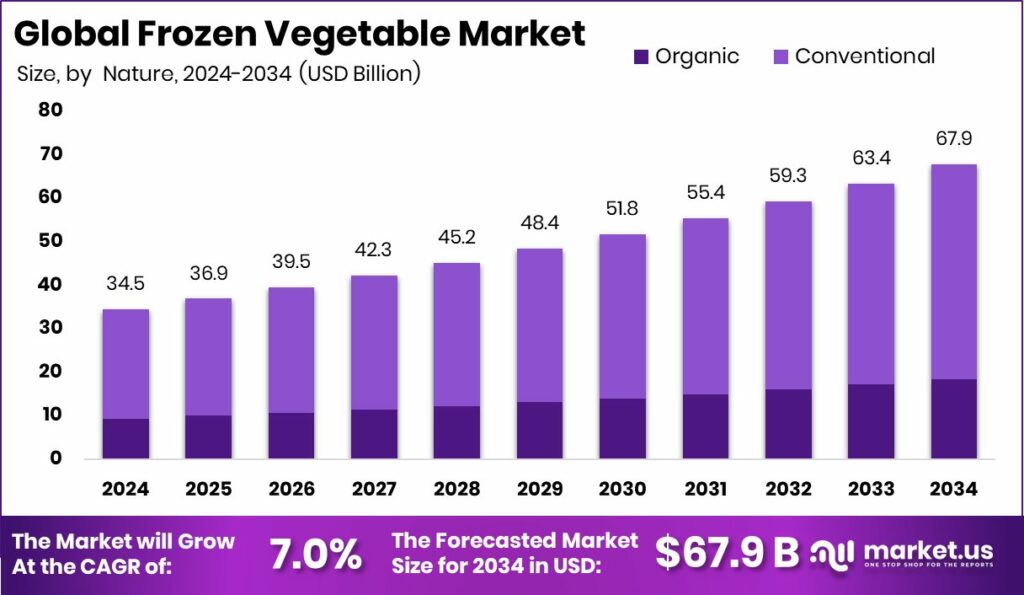

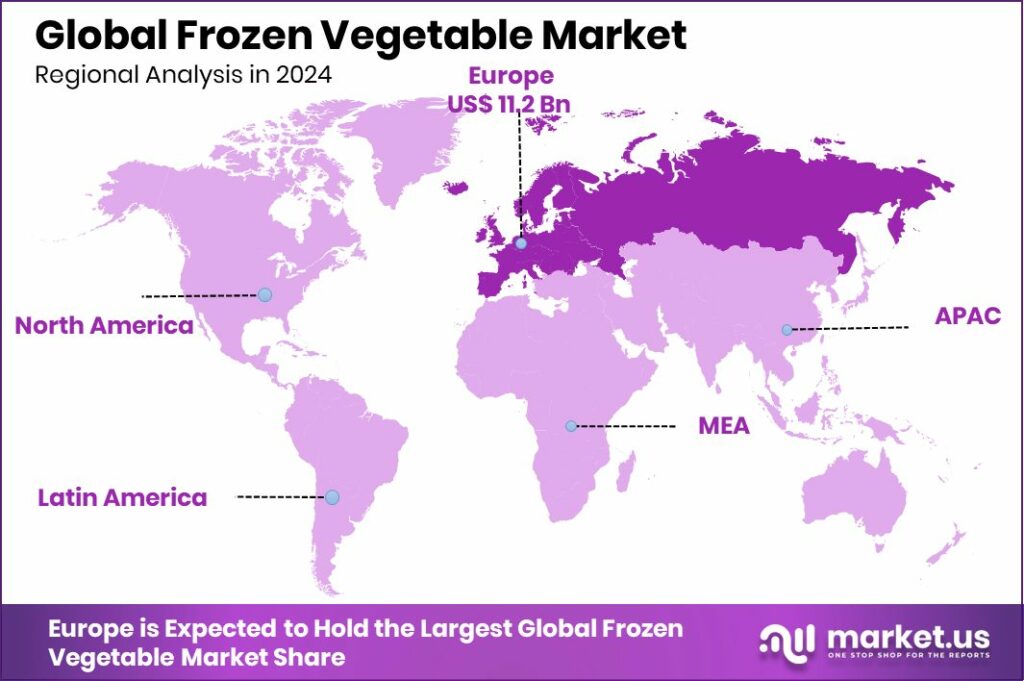

The Global Frozen Vegetable Market is expected to be worth around USD 67.9 billion by 2034, up from USD 34.5 billion in 2024, and is projected to grow at a CAGR of 7.0% from 2025 to 2034. With a 32.7% share, Europe led the Frozen Vegetable Market, generating USD 11.2 Bn revenue.

Frozen vegetables are fresh vegetables that are washed, cut, and quickly frozen to preserve their nutritional value, taste, and texture. This method of preservation allows them to be stored for longer periods without losing much of their natural quality. They are convenient for consumers because they require minimal preparation and reduce food waste compared to fresh produce.

The frozen vegetable market refers to the global trade and consumption of vegetables preserved through freezing techniques. It covers various products like peas, corn, broccoli, spinach, and mixed vegetables that are distributed through supermarkets, hypermarkets, online platforms, and food service outlets. This market is growing as frozen foods provide a balance of nutrition, convenience, and affordability to consumers across the world.

One key growth factor is the rising demand for ready-to-cook meals as busy lifestyles push consumers toward time-saving food solutions. Frozen vegetables are pre-cleaned and pre-cut, making them a practical choice for quick cooking. Additionally, advancements in cold storage and freezing technology help maintain their quality, boosting consumer trust. According to an industry report, 4AG Robotics Secures $40M CAD Series B to Advance Autonomous Mushroom Harvesting

In terms of demand, the health-conscious population is increasingly turning to frozen vegetables because they retain essential nutrients like vitamins and minerals. With more people focusing on balanced diets, frozen vegetables are viewed as an affordable and accessible way to maintain healthy eating habits throughout the year. According to an industry report, KÄÄPÄ Biotech Secures €900K in Fresh Funding.

The market also presents opportunities in expanding distribution channels, especially online grocery platforms. As e-commerce food delivery grows and more households shift to digital shopping, frozen vegetables are finding wider acceptance. This shift opens new avenues for producers and retailers to connect with consumers who value convenience, nutrition, and affordability together. According to an industry report, a B.C.-based tech Company Raises $40M to grow AI-driven mushroom Harvesting.

Key Takeaways

- The Global Frozen Vegetable Market is expected to be worth around USD 67.9 billion by 2034, up from USD 34.5 billion in 2024, and is projected to grow at a CAGR of 7.0% from 2025 to 2034.

- In 2024, corn led the frozen vegetable market, capturing a strong 19.3% share.

- Conventional products dominated the frozen vegetable market in 2024, holding more than 73.7% overall share.

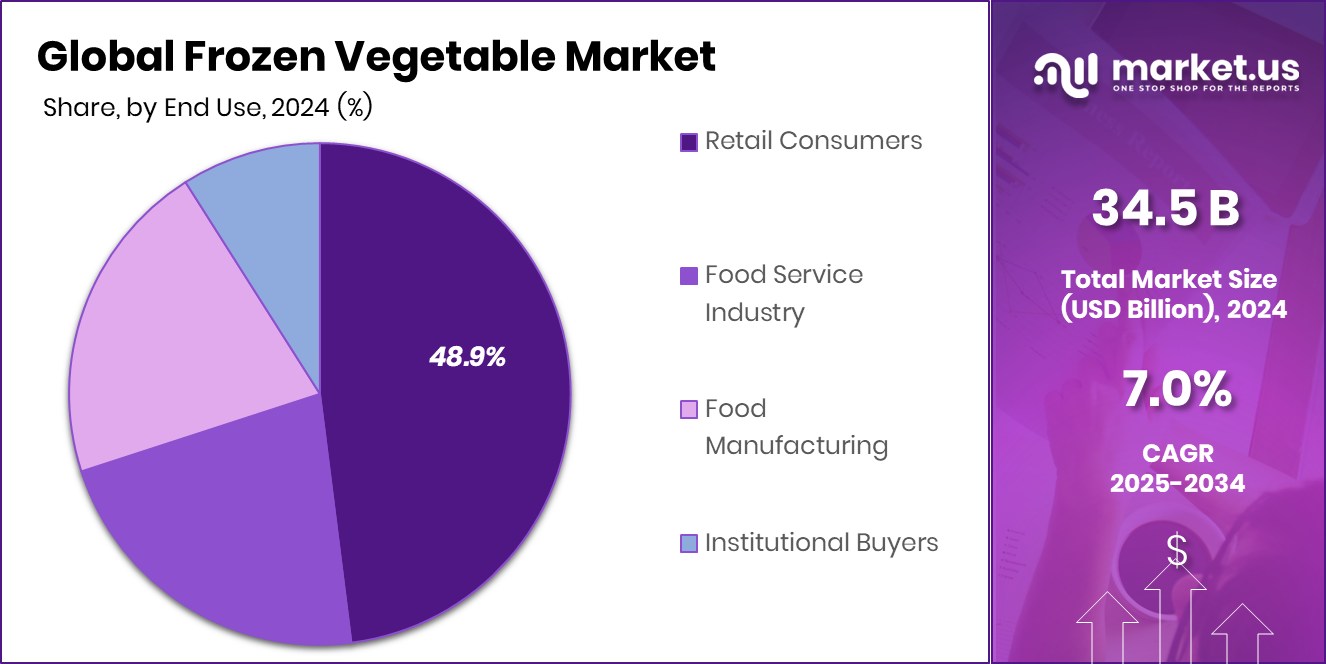

- Retail consumers accounted for a 48.9% share, showing their strong preference in the frozen vegetable market.

- Hypermarkets and supermarkets drove sales in the frozen vegetable market with a 39.6% share.

- Europe’s Frozen Vegetable Market, valued at USD 11.2 Bn, captured a strong 32.7% share.

By Vegetable Type Analysis

In 2024, corn dominated the frozen vegetable market with a 19.3% share.

In 2024, Corn held a dominant market position in the By Vegetable Type segment of the Frozen Vegetable Market, with a 19.3% share. This highlights the strong consumer preference for corn, which is widely consumed across households and food service sectors.

Frozen corn offers versatility as it is used in a variety of meals, including soups, salads, ready-to-eat dishes, and as a side serving, making it a staple in both domestic kitchens and commercial food preparations. Its naturally sweet taste, ease of preparation, and year-round availability contribute significantly to its high demand in the frozen food category.

The popularity of frozen corn also stems from its nutritional profile, being a rich source of fiber, vitamins, and antioxidants. Consumers seeking healthy, quick, and affordable meal options continue to favor corn as a convenient choice that balances taste and nutrition. Moreover, with freezing technology ensuring minimal nutrient loss, frozen corn retains its appeal for health-conscious buyers.

The strong 19.3% share underlines how corn has become a key driver in the overall frozen vegetable market, not only for its affordability but also for its adaptability across diverse cuisines. This steady demand ensures corn remains a vital product shaping market dynamics.

By Nature Analysis

The conventional segment led the frozen vegetable market, holding 73.7% overall share.

In 2024, Conventional held a dominant market position in the By Nature segment of the Frozen Vegetable Market, with a 73.7% share. This strong preference reflects the wide consumer reliance on conventionally produced frozen vegetables, primarily due to their affordability and widespread availability across markets.

Conventional frozen vegetables are produced at a large scale, allowing for lower costs and consistent supply, which makes them highly accessible to both households and food service providers. Their dominance is also supported by established farming practices and supply chains that ensure steady production and distribution across regions.

The appeal of conventional frozen vegetables lies in their balance of price, convenience, and nutritional value. Consumers across income groups find them a practical choice for daily cooking, as they save time while maintaining taste and freshness. With freezing technology preserving essential vitamins and minerals, conventional products remain trusted options for families seeking nutritious meals without overspending.

Furthermore, supermarkets and retail outlets continue to focus heavily on conventional frozen products, reinforcing their large market presence. The 73.7% share underscores the importance of this category in driving overall market growth, as it caters to the majority of demand while shaping purchasing trends in the frozen vegetable industry.

By End Use Analysis

Retail consumers drove the Frozen Vegetable Market demand, accounting for 48.9% share.

In 2024, Retail Consumers held a dominant market position in the By End Use segment of the Frozen Vegetable Market, with a 48.9% share. This dominance reflects the growing preference of households for convenient and ready-to-use frozen vegetables that reduce meal preparation time.

Retail consumers are increasingly opting for frozen vegetables because they fit well into fast-paced lifestyles, offering both nutrition and ease of storage. The ability to purchase in smaller, flexible pack sizes also makes them more attractive for everyday cooking needs.

The 48.9% share highlights the significant role of retail demand in driving the overall frozen vegetable market. Households view frozen vegetables as a cost-effective way to access seasonal produce year-round, eliminating concerns about perishability and food waste. This steady uptake has been further supported by improved freezing techniques that retain natural taste, color, and nutrients, making them a reliable alternative to fresh produce.

With more consumers embracing healthier diets while balancing time constraints, retail demand continues to strengthen. The segment’s leadership position shows that frozen vegetables have become a staple in modern kitchens, reflecting changing food consumption habits and reinforcing retail consumers as a central pillar of market growth.

By Distribution Channel Analysis

Hypermarkets and supermarkets captured 39.6 of % Frozen Vegetable Market share.

In 2024, Hypermarkets/Supermarkets held a dominant market position in the By Distribution Channel segment of the Frozen Vegetable Market, with a 39.6% share. This dominance reflects the trust and convenience consumers associate with these large retail outlets when purchasing frozen vegetables.

Hypermarkets and supermarkets provide a wide variety of frozen products under one roof, allowing customers to choose from different brands, pack sizes, and price ranges. Their ability to maintain strong cold storage facilities ensures that frozen vegetables are preserved in the best condition until purchase, further enhancing consumer confidence.

The 39.6% share highlights how these retail formats remain the most preferred shopping destinations for frozen vegetables. Shoppers benefit from promotional offers, bulk discounts, and loyalty programs that make purchasing frozen products more affordable. Additionally, the physical visibility of products in well-maintained freezer sections helps consumers compare options instantly, encouraging higher sales.

The role of hypermarkets and supermarkets extends beyond convenience—they act as primary touchpoints for consumers to access frozen vegetables regularly. Their strong presence in both urban and semi-urban areas ensures steady demand, positioning them as the backbone of distribution in this market. This dominance emphasizes their critical role in shaping consumer purchasing behavior and sustaining market growth.

Key Market Segments

By Vegetable Type

- Broccoli and Cauliflower

- Green Peas

- Asparagus

- Mushrooms

- Spinach

- Corn

- Green Beans

- Others

By Nature

- Organic

- Conventional

By End Use

- Retail Consumers

- Food Service Industry

- Food Manufacturing

- Institutional Buyers

By Distribution Channel

- Hypermarkets/Supermarkets

- Convenience Stores

- Grocery Stores

- Online Retailers

- Others

Driving Factors

Rising Demand for Convenient and Healthy Food Choices

One of the top driving factors for the Frozen Vegetable Market is the growing consumer demand for convenience, combined with health benefits. Busy lifestyles and increasing urbanization have made people look for food options that are quick to prepare yet nutritious. Frozen vegetables meet this need perfectly, as they are pre-cleaned, pre-cut, and preserved with minimal nutrient loss.

Consumers see them as a reliable way to access seasonal vegetables throughout the year without worrying about spoilage or waste. The shift toward healthier eating, where people prefer foods rich in vitamins, fiber, and minerals, is adding further momentum. This factor highlights how frozen vegetables are no longer just about convenience, but also about supporting everyday healthy living choices.

Restraining Factors

Limited Cold Storage and Supply Chain Challenges

A major restraining factor for the Frozen Vegetable Market is the lack of sufficient cold storage and reliable supply chain systems, especially in developing regions. Frozen vegetables need consistent low-temperature facilities during transportation and storage to maintain their quality. However, in many areas, poor infrastructure, frequent power outages, and limited cold chain networks create significant challenges.

This leads to product spoilage, reduced shelf life, and higher costs for both producers and retailers. Consumers in such regions may also hesitate to buy frozen vegetables if they doubt the product’s freshness. These limitations restrict the market’s expansion potential, as reliable logistics and advanced storage remain essential for ensuring consistent availability and building consumer trust in frozen vegetables.

Growth Opportunity

Expanding Online Grocery Platforms Boost Frozen Vegetable Sales

A key growth opportunity for the Frozen Vegetable Market lies in the rapid expansion of online grocery platforms. With more consumers turning to digital shopping for daily essentials, frozen vegetables are gaining wider visibility and accessibility. Online platforms provide detailed product information, customer reviews, and home delivery services, which make it easier for buyers to trust and purchase frozen products.

The convenience of ordering from home, combined with discounts and subscription models, is encouraging higher adoption. As internet penetration and mobile app usage continue to grow globally, especially in emerging markets, online sales channels will create fresh opportunities for producers and retailers. This shift not only increases reach but also strengthens long-term consumer engagement with frozen vegetables.

Latest Trends

Rising Preference for Mixed and Ready-to-Cook Packs

One of the latest trends in the Frozen Vegetable Market is the increasing popularity of mixed and ready-to-cook vegetable packs. Consumers are looking for solutions that save time while offering balanced nutrition, and these combination packs meet both needs effectively. Instead of buying single vegetables, people prefer pre-mixed options like stir-fry blends, soup mixes, or ready-to-steam packs that require minimal effort in cooking.

This trend is especially strong among urban households, working professionals, and young consumers who prioritize convenience without compromising on health. The appeal of variety, portion control, and reduced food preparation time is driving sales of these packs. This shift highlights how innovation in product formats is reshaping consumer choices in the frozen vegetable market.

Regional Analysis

In 2024, Europe dominated the Frozen Vegetable Market with 32.7%, reaching USD 11.2 Bn.

The Frozen Vegetable Market shows steady growth across all major regions, with Europe emerging as the leading hub in 2024. Europe accounted for a dominant 32.7% share of the global market, valued at USD 11.2 billion. This leadership is driven by strong consumer demand for convenient, healthy, and sustainable food options.

European consumers are increasingly shifting toward frozen vegetables due to their year-round availability, reduced food waste, and preserved nutritional value. The region’s advanced cold storage infrastructure, strict quality regulations, and widespread retail penetration further strengthen its position.

Countries such as Germany, France, and the UK remain key contributors, as rising urbanization and busy lifestyles encourage greater reliance on ready-to-use vegetable packs. Moreover, the growing awareness of balanced diets and increasing adoption of vegetarian and plant-based meals are supporting higher frozen vegetable consumption.

While other regions like North America, Asia Pacific, Latin America, and the Middle East & Africa are witnessing notable growth, Europe’s clear dominance highlights its mature market structure, strong consumer acceptance, and established distribution networks.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Ajinomoto Co., Inc. plays a vital role with its expertise in food processing and preservation, bringing forward frozen vegetable offerings that align with consumer needs for nutrition and convenience. Its focus on quality and technological capabilities allows it to strengthen its footprint in both domestic and international markets.

General Mills Inc. leverages its wide presence in the food industry to diversify into frozen vegetables, ensuring accessibility through robust retail and distribution channels. The company’s emphasis on packaged and easy-to-cook options aligns with the growing global preference for time-saving meal solutions.

ITC Limited, with its strong presence in emerging markets, brings value to the frozen vegetable space by focusing on freshness, packaging, and affordability. Its extensive distribution network across urban and semi-urban regions helps reach a wider consumer base that is increasingly shifting toward frozen products.

ConAgra Foods, Inc. continues to demonstrate leadership with a diverse frozen food portfolio that includes vegetable-based options. Its ability to integrate consumer insights into product development ensures relevance in a highly competitive environment.

Top Key Players in the Market

- Ajinomoto Co., Inc.

- General Mills Inc.

- ITC Limited

- ConAgra Foods, Inc.

- Uren Food Group Limited

- B&G Foods Holdings Corp.

- Greenyard NV

- J.R. Simplot Co.

- The Kraft Heinz Company

- Nature’s Garden

Recent Developments

- In June 2025, Conagra Brands launched a broad range of over 50 new frozen products, including “vegetable side dishes” under popular labels like Birds Eye and Alexia. These new veggie options arrive in convenient trays and bags, offering consumers flavorful and easy-to-prepare vegetable sides.

- In May 2025, B&G Foods revealed it was considering selling its frozen and canned vegetable brands, including Green Giant and Le Sueur, as part of a strategic review to sharpen its portfolio focus.

- In March 2025, Greenyard entered exclusive talks with Gelagri Bretagne, a leading frozen‑vegetable specialist in Brittany, France. The plan aims to form a partnership—likely with Greenyard holding a majority stake—to integrate Greenyard’s global reach with Gelagri’s local grower base and manufacturing strengths. This joint effort is expected to boost efficient production and sales of Brittany‑sourced frozen vegetables on a broader scale.

Report Scope

Report Features Description Market Value (2024) USD 34.5 Billion Forecast Revenue (2034) USD 67.9 Billion CAGR (2025-2034) 7.0% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Vegetable Type (Broccoli and Cauliflower, Green Peas, Asparagus, Mushrooms, Spinach, Corn, Green Beans, Others), By Nature (Organic, Conventional), By End Use (Retail Consumers, Food Service Industry, Food Manufacturing, Institutional Buyers), By Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Grocery Stores, Online Retailers, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Ajinomoto Co., Inc., General Mills Inc., ITC Limited, ConAgra Foods, Inc., Uren Food Group Limited, B&G Foods Holdings Corp., Greenyard NV, J.R. Simplot Co., The Kraft Heinz Company, Nature’s Garden Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Ajinomoto Co., Inc.

- General Mills Inc.

- ITC Limited

- ConAgra Foods, Inc.

- Uren Food Group Limited

- B&G Foods Holdings Corp.

- Greenyard NV

- J.R. Simplot Co.

- The Kraft Heinz Company

- Nature’s Garden

Our Clients

- 156620

- August 2025