Global Food Contract Manufacturing Market Size, Share Analysis Report By Product Type (Ready-to-Eat Meals, Dairy Products, Meat Products, Frozen Meals, Baked Goods, Others), By Service Type (Manufacturing Processing, Formulation Development, Packaging Distribution, Quality Control Assurance, Logistics Transportation, Seafood, Meat And Poultry Products, Bakery Products), By Packaging Type (Frozen, Refrigerated, Aseptic, Canned, Dry), By Ingredient Type (Dairy Alternatives, Fruits, Vegetables, Meat, Poultry Fish, Bakery Cereals, Oil Fat) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181626

- Number of Pages: 205

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

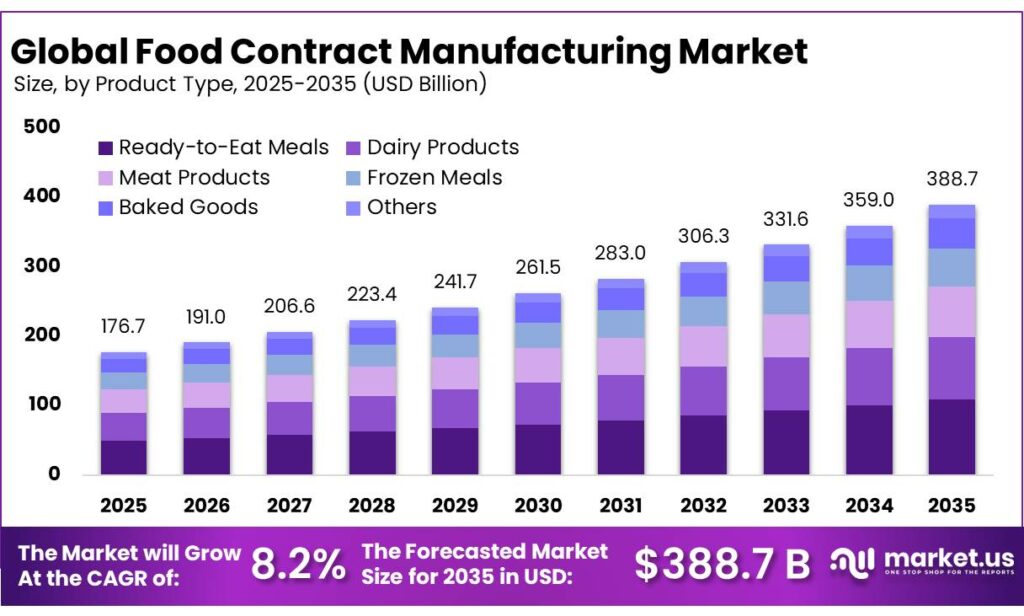

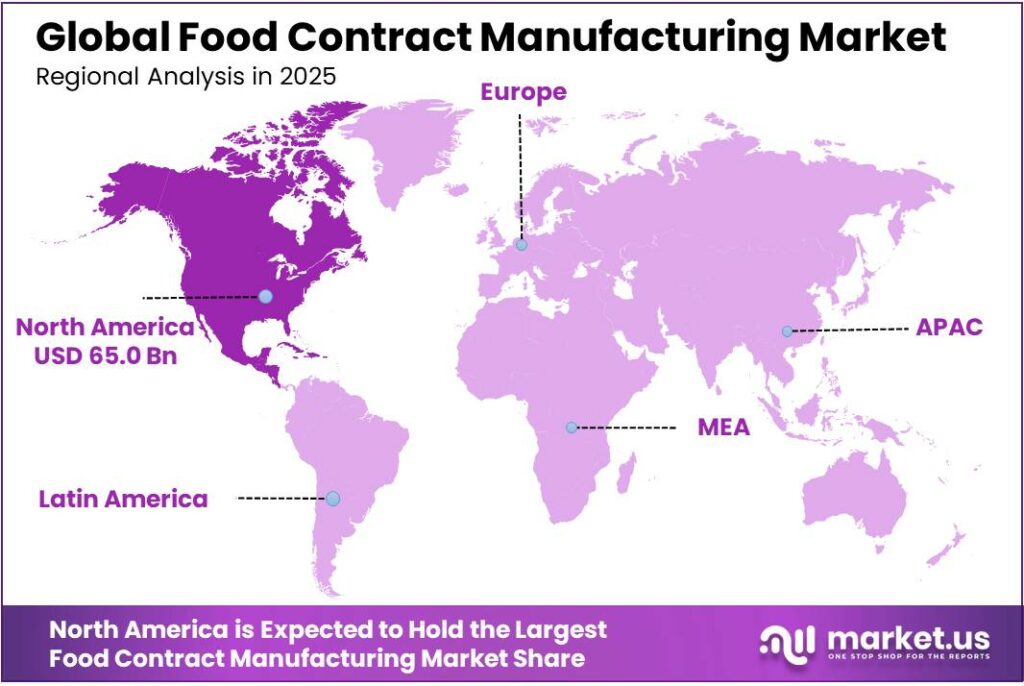

The Global Food Contract Manufacturing Market size is expected to be worth around USD 388.7 Billion by 2035, from USD 176.7 Billion in 2025, growing at a CAGR of 8.2% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 36.8% share, holding USD 65.0 billion revenue.

Food contract manufacturing is an outsourced production model in which brand owners transfer part or all of formulation execution, processing, packaging, quality control, and sometimes logistics to specialist manufacturers, allowing them to concentrate on commercialization and channel expansion. Its industrial relevance is supported by the scale of food processing itself: in the United States, food and beverage manufacturing represented 16.8% of manufacturing sales, 15.4% of manufacturing employment, and 15.0% of manufacturing value added in 2021, while the country counted 42,708 food and beverage processing establishments in 2022.

In the European Union, food and drink industry production increased 1.4% year on year in Q2 2025, and turnover advanced 5.0% year on year; by Q3 2025, year-on-year production still rose 1.0% and turnover 3.8%. Exports reached €48.4 billion in Q2 2025 and €48.5 billion in Q3 2025, while food-industry employment rose 1.4% year on year in Q2 2025 and 2.4% year on year in Q3 2025. This indicates that outsourced manufacturers are operating in a large, trade-linked, employment-stable food ecosystem rather than a niche supply base.

The main demand drivers are input volatility, portfolio diversification, and the need for flexible capacity. FAO reported that the global Food Price Index averaged 127.2 points for 2025, up 4.3% from 2024, while the index stood at 128.0 points in June 2025, showing that commodity cost pressure did not disappear even as some categories softened. At the same time, the OECD-FAO Agricultural Outlook projects that the share of calories from livestock and fish products will rise 6% globally by 2034, while lower-middle-income countries are expected to increase daily intake of livestock and fish products by about 25%. Such shifts favor contract manufacturers that can scale specialized, shelf-stable, and value-added formats quickly.

Government and regulatory initiatives are also reshaping the sector’s operating standards. The U.S. FDA stated that its Human Foods Program entered its first year after the reorganization that took effect on October 1, 2024, with formal FY 2025 priority deliverables designed to strengthen program execution. On June 30, 2025, FDA published its 2025 Human Foods Program guidance agenda, and on July 25, 2025, FDA and USDA jointly requested information to help establish a uniform definition for ultra-processed foods. For food contract manufacturers, these developments raise the value of robust documentation, traceability, formulation transparency, and label-readiness across customer portfolios.

Key Takeaways

- Food Contract Manufacturing Market size is expected to be worth around USD 388.7 Billion by 2035, from USD 176.7 Billion in 2025, growing at a CAGR of 8.2%.

- Ready-to-Eat Meals held a dominant market position, capturing more than a 28.5% share.

- Manufacturing Processing held a dominant market position, capturing more than a 38.1% share.

- Frozen held a dominant market position, capturing more than a 31.6% share.

- Meat held a dominant market position, capturing more than a 22.3% share.

- North America holds a leading position in the food contract manufacturing market, accounting for 36.8% share and valued at around USD 65.0 billion.

By Product Type Analysis

Ready-to-Eat Meals dominates with 28.5% driven by convenience and busy lifestyles

In 2025, Ready-to-Eat Meals held a dominant market position, capturing more than a 28.5% share. This strong position was mainly supported by changing consumer habits, where people increasingly preferred quick and hassle-free food options. With rising urbanization and longer working hours, consumers leaned toward meals that require little to no preparation. The demand was particularly noticeable among working professionals, students, and single-person households who value both time savings and consistent taste. Manufacturers also expanded their offerings with healthier, preservative-conscious, and regionally inspired meal options, making these products more appealing to a wider audience.

By Service Type Analysis

Manufacturing Processing dominates with 38.1% supported by rising demand for scalable production

In 2025, Manufacturing Processing held a dominant market position, capturing more than a 38.1% share. This growth was largely driven by food brands relying on contract manufacturers to handle large-scale production efficiently. Many companies chose to outsource processing to reduce operational costs and focus more on branding and distribution. The increasing demand for packaged and ready-to-consume food products also pushed the need for advanced processing capabilities. Contract manufacturers offered consistency in quality, better compliance with food safety standards, and the ability to scale production quickly, which made them a preferred choice across the industry.

By Packaging Type Analysis

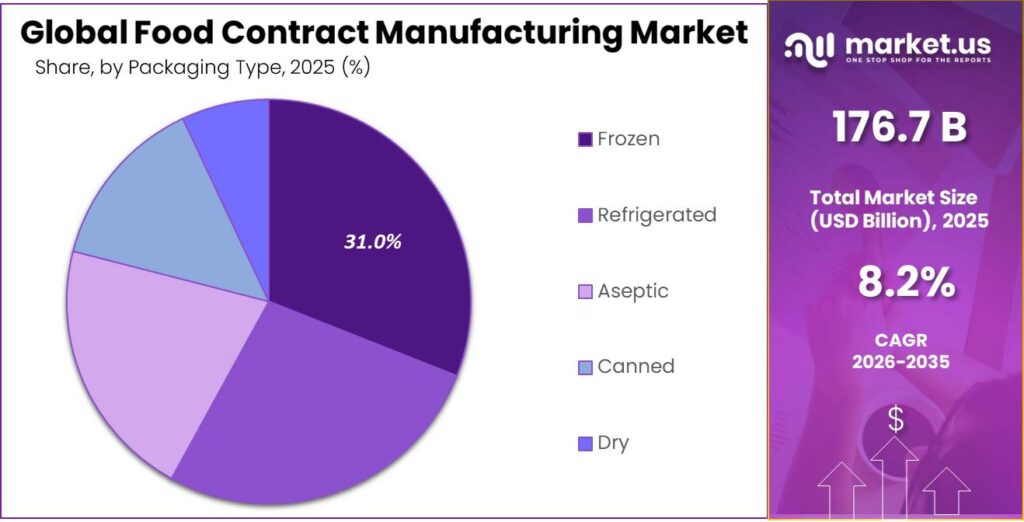

Frozen packaging dominates with 31.6% as consumers prefer longer shelf life and convenience

In 2025, Frozen held a dominant market position, capturing more than a 31.6% share. This was mainly due to the growing demand for food products that can be stored for longer periods without losing quality. Consumers increasingly preferred frozen options because they offer convenience, reduce food waste, and maintain taste and nutrition over time. Food brands also relied on frozen packaging to expand their product reach across regions, as it allows safe transportation and storage. Categories like ready meals, meat products, and snacks contributed strongly to this segment’s growth.

By Ingredient Type Analysis

Meat segment dominates with 22.3% driven by high demand for protein-rich food products

In 2025, Meat held a dominant market position, capturing more than a 22.3% share. This was largely due to the strong global demand for protein-rich diets and the widespread use of meat in a variety of processed and ready-to-eat food products. Contract manufacturers played a key role in handling meat processing, packaging, and maintaining safety standards, which are critical in this segment. Food brands increasingly relied on these services to ensure consistent quality while meeting rising consumption needs. Products such as frozen meat meals, snacks, and convenience foods contributed significantly to this segment’s growth.

Key Market Segments

By Product Type

- Ready-to-Eat Meals

- Dairy Products

- Meat Products

- Frozen Meals

- Baked Goods

- Others

By Service Type

- Manufacturing Processing

- Formulation Development

- Packaging Distribution

- Quality Control Assurance

- Logistics Transportation

- Seafood, Meat & Poultry Products

- Bakery Products

By Packaging Type

- Frozen

- Refrigerated

- Aseptic

- Canned

- Dry

By Ingredient Type

- Dairy Alternatives

- Fruits

- Vegetables

- Meat

- Poultry Fish

- Bakery Cereals

- Oil Fat

Emerging Trends

Better tracking is no longer optional

One of the clearest latest trends in food contract manufacturing is the move toward digital traceability. Food brands now want manufacturing partners that can do more than just produce at scale. They also want clear batch tracking, faster recall response, better recordkeeping, and stronger visibility across ingredients, processing, packaging, and shipment. This trend is growing because food safety expectations are rising, and regulators are pushing the industry toward tighter documentation. In the United States, the FDA’s Food Traceability Rule has become a major signal for the market. In February 2026, the FDA said Congress directed the agency not to enforce the rule before July 20, 2028, after a proposed 30-month extension.

This matters directly to contract manufacturers. When a food brand outsources production, it expects the manufacturing partner to maintain clean records on lots, ingredients, storage conditions, and shipment history. That is why digital record systems, barcode-linked production runs, and traceability-ready workflows are becoming part of day-to-day manufacturing decisions. The trend is also supported by the scale of the industry itself. USDA data shows the United States had about 42,708 food and beverage manufacturing establishments in 2022.

Cold chain and smarter handling are shaping new contracts

A second part of this same trend is stronger cold-chain integration. More food brands are expanding into frozen meals, chilled snacks, dairy-based products, meat items, and prepared foods that need tight temperature control. That puts pressure on contract manufacturers to offer not only processing capacity, but also cold storage discipline and reliable logistics support. The World Bank says at least 25% of food produce in developing countries is lost due to lack of cold chain. In another World Bank resource, it notes that up to 30% of food produced globally is lost or wasted, while food loss and waste generate an estimated 8% to 10% of total greenhouse gas emissions. These are major numbers, and they explain why cold-chain capable manufacturing is becoming more valuable.

Drivers

Rising demand for packaged and ready-to-eat food is a major driver for food contract manufacturing

One of the biggest reasons the food contract manufacturing market is growing is simple: food demand is getting larger, faster, and more convenience-led. Brands want to launch products quickly, scale output without building new factories, and keep quality steady across regions. That is exactly where contract manufacturers fit in. A clear sign of this shift can be seen in U.S. food spending. According to the USDA, total food spending reached $2.58 trillion in 2024, up from $2.48 trillion in 2023. Within that, food-away-from-home spending rose from $1.45 trillion to $1.52 trillion, while food-at-home spending also increased from $1.04 trillion to $1.06 trillion.

This trend is not limited to one country. India’s processed food ecosystem also shows why outside manufacturing capacity is becoming more important. APEDA states that India’s food processing sector received USD 13.01 billion in foreign direct investment from April 2000 to December 2024, and about USD 7 billion of that came during 2014–2024 alone. That level of investment shows strong confidence in processed food capacity, export readiness, and value-added food production. When investment rises, brands usually move faster on product launches, regional expansion, and export-linked production, and that increases the need for specialist manufacturing partners who can handle different formats, ingredients, and packaging needs.

Government support and stricter food systems are making outsourcing more practical

Another reason this driver has become stronger is government support for food processing infrastructure. In India, the PMFME scheme provides 50% financial grant for branding and marketing support to groups of FPOs, SHGs, cooperatives, or special purpose vehicles of micro food processing enterprises. Alongside that, the Ministry of Food Processing Industries continues to push schemes under PMKSY and agro-processing cluster development to expand modern food infrastructure, preservation capacity, and cold-chain-linked processing. These efforts make it easier for smaller and mid-sized food brands to enter the market, but many of them still prefer contract manufacturers instead of building full production systems from scratch. That is why public support often ends up strengthening the contract manufacturing model as well.

Restraints

Declining workforce and skill gaps are slowing production capacity

One of the most serious restraints in the food contract manufacturing market today is the shortage of skilled and stable labor. Food manufacturing depends heavily on workers for processing, packaging, quality checks, and logistics. But across many regions, the availability of this workforce is becoming uncertain. According to the Food and Agriculture Organization, around 1.3 billion people were employed in agrifood systems globally in 2021, representing about 39.2% of the global workforce. While this seems large, the issue is not the total number, but the steady decline in active and skilled workers in certain areas of the food chain, especially in processing and manufacturing roles.

In the United States, the United States Department of Agriculture reports that food and beverage manufacturing employed around 1.7 million people in 2021, which is just over 1.1% of total nonfarm employment. This shows that even though the sector is critical, it relies on a relatively small share of the workforce. Any disruption whether due to migration issues, health crises, or labor shortages can quickly impact production capacity. Contract manufacturers, who depend on consistent throughput, often face delays, increased costs, and reduced efficiency when labor is not stable.

Workforce disruptions and reliance on temporary labor add operational risk

Another layer of this restraint comes from the unstable nature of the food industry workforce. A large portion of workers are seasonal, temporary, or migrant laborers. According to the Food Chain Workers Alliance, nearly 70% of the 28 million workers in the U.S. food system are in frontline roles, which are often low-paid and high-turnover jobs. This creates a constant cycle of hiring and training, making it difficult for contract manufacturers to maintain consistency in production quality and speed.

Real-world events also highlight how fragile the system can be. In 2025, a meat processing facility in the U.S. saw its workforce drop to about 30% of normal levels, which reduced production to only 20% of its usual capacity after a labor disruption. This kind of situation directly affects supply chains and shows how dependent food manufacturing is on labor availability. When such disruptions happen, contract manufacturers struggle to meet client demand, leading to delays and financial losses.

Opportunity

Expanding global demand for packaged and value-added food is creating strong growth opportunities

One of the biggest growth opportunities in the food contract manufacturing market is the rapid rise in demand for packaged, processed, and value-added food across the world. Consumers are no longer just buying basic staples; they are shifting toward ready meals, snacks, protein-rich foods, and premium packaged items. According to the Food and Agriculture Organization, global food consumption is increasing alongside production, with strong demand growth across multiple food categories. This change is important because value-added food products require more processing, packaging, and standardization, which often pushes brands to rely on contract manufacturers instead of building everything in-house.

Government push and investment in food processing is opening new doors

Another strong opportunity comes from government initiatives and rising investments in the food processing sector. In India, for example, the food processing industry already accounts for about 32% of the total food market, showing how important value-added food has become in the overall ecosystem. The sector is also expanding steadily, with expected annual growth of around 8–10%, especially in smaller cities where demand for packaged food is increasing quickly. This kind of growth creates a need for more production capacity, better technology, and efficient supply chains—areas where contract manufacturers play a key role.

Government schemes are also making a difference. Programs like India’s PMKSY and other food processing initiatives are helping build infrastructure such as mega food parks, cold chains, and agro-processing clusters. These initiatives reduce entry barriers for new food brands and startups. However, many of these companies still do not have their own manufacturing setups, so they depend on third-party manufacturers to produce and package their products. This directly increases demand for contract manufacturing services.

Regional Insights

North America holds a leading position in the food contract manufacturing market, accounting for 36.8% share and valued at around USD 65.0 billion. The region’s dominance is largely supported by its well-established food processing ecosystem, strong demand for packaged and convenience foods, and the presence of large-scale contract manufacturing companies. The United States plays a major role in this regional strength, with a highly developed food and beverage industry generating close to USD 1.9 trillion in annual sales across more than 21,000 companies

Another key factor supporting North America’s leadership is its advanced infrastructure and skilled workforce. The U.S. food and beverage manufacturing sector alone employs around 1.7 million workers, highlighting the depth of industrial capability available in the region . In addition, high consumer spending on food continues to drive production needs. According to USDA data, total food spending in the U.S. has remained above USD 2.5 trillion annually, reflecting strong consumption patterns across both retail and foodservice channels

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Fibro Foods is an emerging player in food contract manufacturing, founded in 2015 and based in India. The company reported annual revenue of around ₹2.24 crore, with an operating revenue range between ₹1–10 crore for FY2024. Its EBITDA showed a growth of 36.6%, indicating improving operational performance. With authorized and paid-up capital of ₹10 lakh, the company remains a small-scale but growing manufacturer focusing on niche food processing and contract production capabilities.

SK Food Group is a major U.S.-based contract manufacturer specializing in fresh and ready-to-eat food products. The company operates multiple production facilities and continues to expand, including a fourth manufacturing facility announced in 2023, expected to be completed by 2025. It produces a wide range of sandwiches, snacks, and meal solutions for retail and foodservice clients. With large-scale operations and continuous expansion, SK Food Group plays a strong role in meeting growing demand for convenience foods.

Hindustan Foods Limited is one of the leading contract manufacturers in India, with revenue exceeding ₹3,019 crore (USD 300+ million). The company operates with a workforce of over 1,000 employees and has shown strong financial performance with profits of around ₹120 crore. It has a market capitalization of about ₹5,700 crore and operates across multiple FMCG categories including food and beverages. Its large-scale production capacity and diversified portfolio make it a key player in contract manufacturing.

Top Key Players Outlook

- Fibro Foods

- Hindustan Foods Limited

- Christy Quality Foods (CQF)

- HACO AG

- SK Food Group

- Pacmoore Products Inc.

- Cremica

- Kilfera Food Manufacturers Ltd

- Thrive Foods LLC.

- Orion Food Co., Ltd

Recent Industry Developments

In FY2025, Hindustan Foods Limited reported total revenue of around ₹3,578.9 crore, reflecting a sharp 30% year-on-year growth from ₹2,761.9 crore in FY2024, showing strong demand from outsourcing clients.

Orion Food Co showed continued momentum, with quarterly net sales rising 60.1% to EUR 695.3 million in late 2025, highlighting strong production and distribution growth.

Report Scope

Report Features Description Market Value (2025) USD 176.7 Bn Forecast Revenue (2035) USD 388.7 Bn CAGR (2026-2035) 8.2%% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Ready-to-Eat Meals, Dairy Products, Meat Products, Frozen Meals, Baked Goods, Others), By Service Type (Manufacturing Processing, Formulation Development, Packaging Distribution, Quality Control Assurance, Logistics Transportation, Seafood, Meat And Poultry Products, Bakery Products), By Packaging Type (Frozen, Refrigerated, Aseptic, Canned, Dry), By Ingredient Type (Dairy Alternatives, Fruits, Vegetables, Meat, Poultry Fish, Bakery Cereals, Oil Fat) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Fibro Foods, Hindustan Foods Limited, Christy Quality Foods (CQF), HACO AG, SK Food Group, Pacmoore Products Inc., Cremica, Kilfera Food Manufacturers Ltd, Thrive Foods LLC., Orion Food Co., Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Food Contract Manufacturing MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Food Contract Manufacturing MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Fibro Foods

- Hindustan Foods Limited

- Christy Quality Foods (CQF)

- HACO AG

- SK Food Group

- Pacmoore Products Inc.

- Cremica

- Kilfera Food Manufacturers Ltd

- Thrive Foods LLC.

- Orion Food Co., Ltd

Our Clients

- 181626

- Mar 2026