Quick Navigation

- Report Overview

- Key Takeaways

- US Market Expansion

- Analysts’ Viewpoint

- Product Type Insights

- Application Insights

- Technology Insights

- End-User Industry Insights

- Design Type Insights

- Key Market Segments

- Emerging Trends

- Business Benefit

- Driver

- Restraint

- Opportunity

- Challenge

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

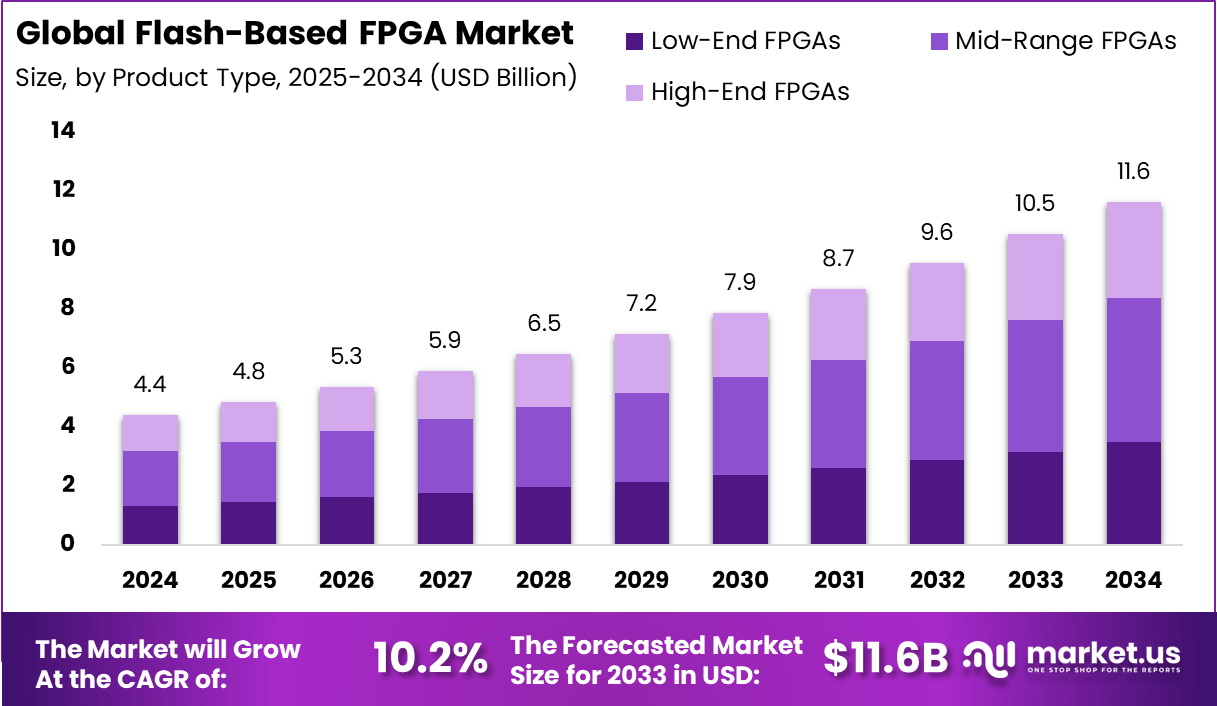

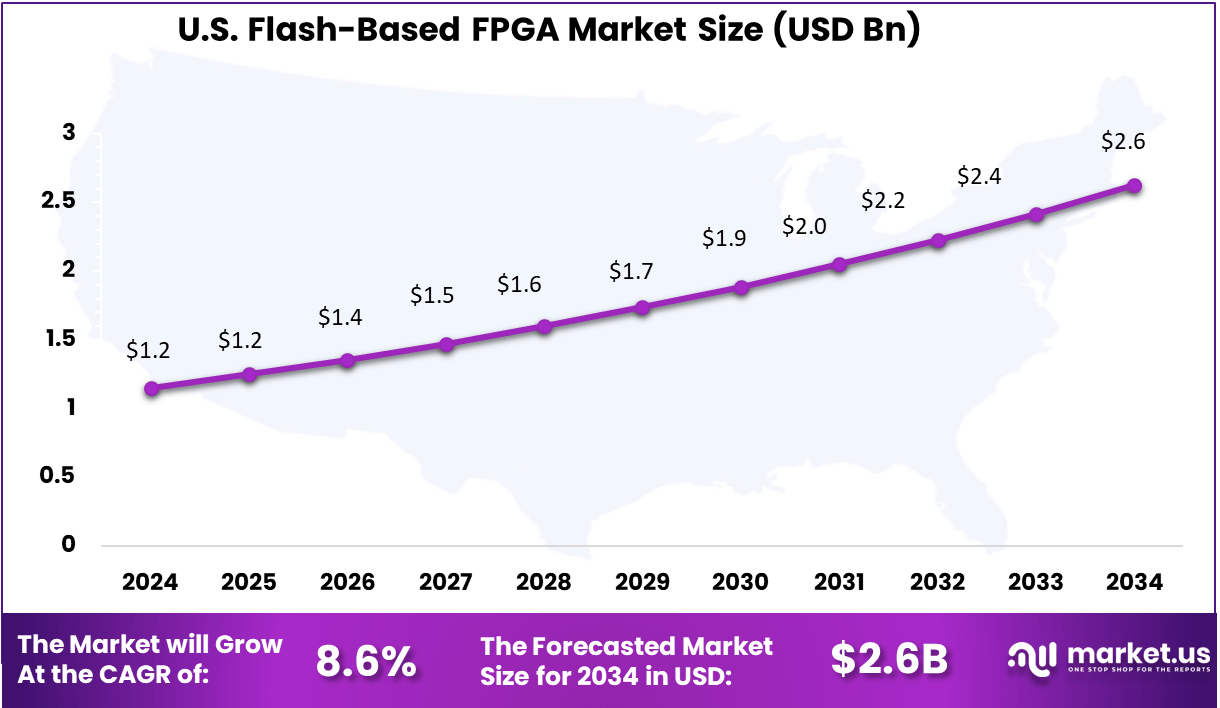

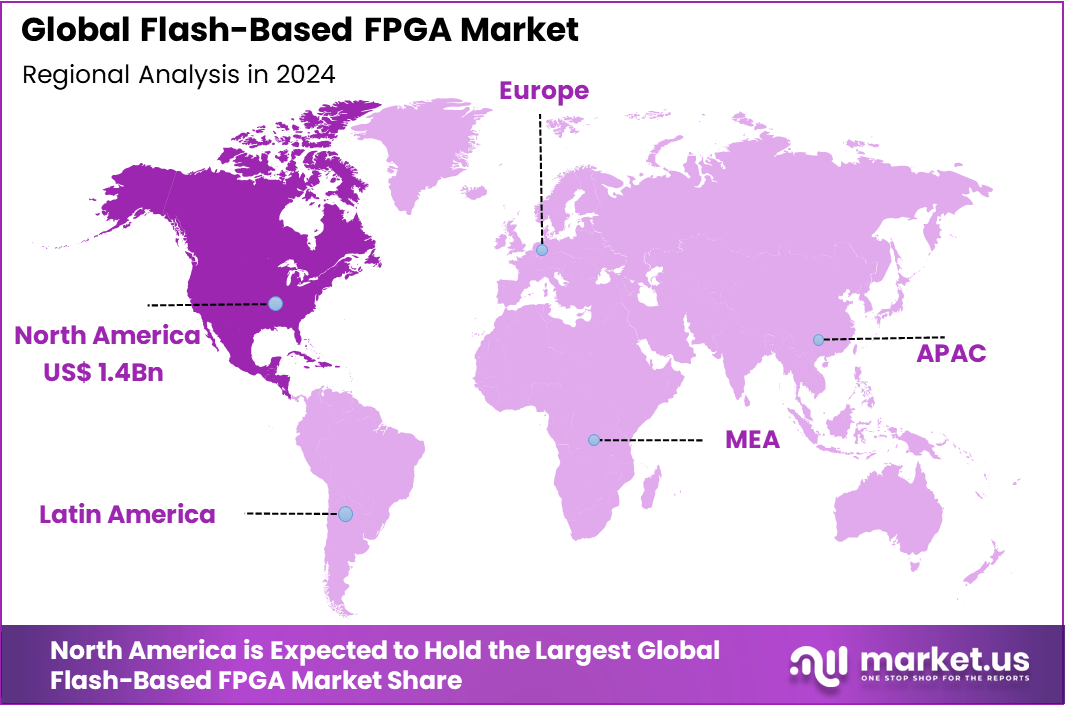

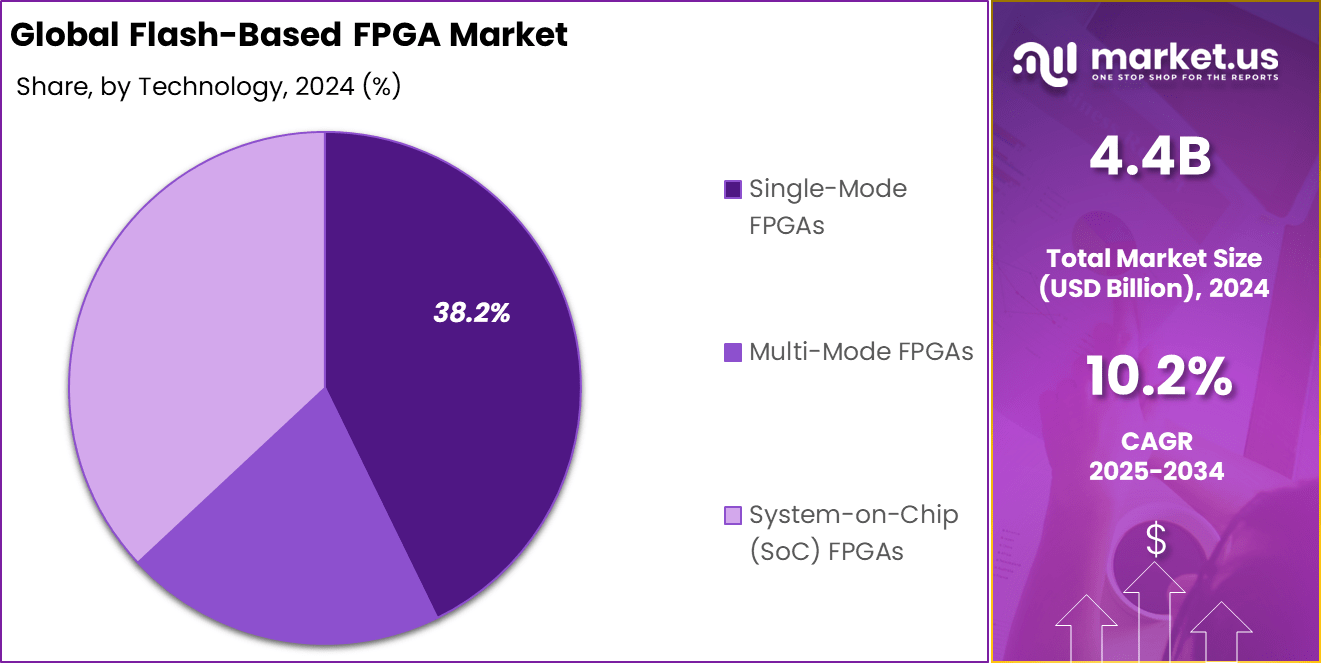

The Global Flash-Based FPGA Market size is expected to be worth around USD 11.6 Billion By 2034, from USD 4.4 billion in 2024, growing at a CAGR of 10.2% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 32.8% share, holding USD 1.4 Billion revenue. Flash-based FPGA sales in the U.S. have reached $1.15 billion, supported by a strong 8.6% CAGR.

Flash-Based Field-Programmable Gate Arrays (FPGAs) are semiconductor devices that utilize non-volatile flash memory to store configuration data. Unlike traditional SRAM-based FPGAs, flash-based variants retain their configuration without the need for continuous power, enabling instant-on capabilities. This feature makes them particularly suitable for applications requiring immediate responsiveness, such as automotive systems, aerospace controls, and industrial automation.

The global Flash-Based FPGA market has been experiencing robust growth, driven by increasing demand across various sectors. Key driving factors include the increasing need for energy-efficient and high-performance computing solutions. Flash-based FPGAs offer advantages such as low power consumption, high reliability, and instant-on capabilities, making them ideal for applications in edge computing and Internet of Things (IoT) devices.

The demand for flash-based FPGAs is particularly strong in the telecommunications sector, where they are used to enhance network performance and support the deployment of 5G infrastructure. Additionally, the automotive industry is increasingly adopting these devices for advanced driver-assistance systems (ADAS) and electric vehicle (EV) applications.

Key Takeaways

- The Global Flash-Based FPGA Market is projected to grow from USD 4.4 Billion in 2024 to approximately USD 11.6 Billion by 2034, advancing at a steady CAGR of 10.2% from 2025 to 2034.

- North America dominated the market in 2024, holding a 32.8% share with revenues of about USD 1.4 Billion, attributed to early adoption in aerospace and industrial automation.

- In the U.S., flash-based FPGA sales have reached USD 1.15 Billion, with sustained momentum driven by a CAGR of 8.6%, fueled by defense modernization and embedded computing demand.

- Mid-Range FPGAs led the product segment with a 42.2% share, due to their balanced performance and affordability for mainstream industrial and telecom applications.

- The Telecommunications sector accounted for the largest application share at 25.5%, driven by network optimization needs and scalable FPGA solutions in 5G infrastructure.

- By technology, Single-Mode FPGAs held a dominant 38.2% share, benefiting from their simplified architecture and lower power consumption.

- The Information Technology industry emerged as the top end-user, contributing 27.5% to the overall market in 2024, supported by growing adoption in data processing and cloud environments.

- Custom Design FPGAs represented 40.0% of the design type segment, highlighting demand for tailored, high-performance solutions across specialized computing and signal processing applications.

US Market Expansion

The US Flash-Based FPGA Market is valued at approximately USD 1.2 Billion in 2024 and is predicted to increase from USD 1.7 Billion in 2029 to approximately USD 2.6 Billion by 2034, projected at a CAGR of 8.6% from 2025 to 2034.

In 2024, North America held a dominant position in the global Flash-Based Field Programmable Gate Array (FPGA) market, capturing more than 32.8% of the total revenue, amounting to approximately USD 1.4 billion. This leadership is primarily attributed to the region’s robust technological infrastructure, significant investments in research and development, and the presence of key industry players.

Te United States, in particular, has been at the forefront of adopting advanced FPGA technologies across various sectors, including telecommunications, automotive, aerospace, and defense. The rapid deployment of 5G networks, coupled with the increasing demand for high-performance computing and real-time data processing, has further propelled the adoption of flash-based FPGAs in the region.

Moreover, the integration of artificial intelligence (AI) and machine learning (ML) capabilities into these devices has opened new avenues for innovation and application, reinforcing North America’s leading position in the market.

Analysts’ Viewpoint

Investment opportunities in the flash-based FPGA market are substantial, particularly in emerging sectors like smart cities, autonomous vehicles, and industrial IoT. Companies investing in research and development of advanced FPGA solutions are well-positioned to capitalize on the growing demand for customizable and energy-efficient hardware.

Businesses are increasingly adopting flash-based FPGAs to achieve greater flexibility, reduce time-to-market, and enhance product longevity. The ability to reprogram these devices post-deployment allows for rapid adaptation to evolving technological requirements. Additionally, their low power consumption and high reliability contribute to reduced operational costs and improved system performance.

The regulatory environment for flash-based FPGAs is influenced by industry-specific standards and compliance requirements. In sectors such as automotive, aerospace, and healthcare, adherence to safety, security, and performance standards is critical. Manufacturers must ensure that their FPGA-integrated systems meet relevant regulations to ensure product reliability and market acceptance.

Product Type Insights

In 2024, the Mid-Range FPGAs segment held a dominant market position, capturing more than a 42.2% share. This dominance can be attributed to their balanced performance and cost-effectiveness, making them suitable for a wide range of applications across various industries.

Mid-Range FPGAs offer sufficient logic density and processing capabilities to handle complex tasks without the higher costs associated with high-end FPGAs, thus appealing to sectors like automotive, industrial automation, and telecommunications.

The automotive industry, in particular, has seen increased adoption of Mid-Range FPGAs due to the growing demand for advanced driver-assistance systems (ADAS) and infotainment systems. These FPGAs provide the necessary computational power and flexibility to process real-time data from various sensors, enhancing vehicle safety and user experience.

Similarly, in industrial automation, Mid-Range FPGAs are employed for real-time control and monitoring systems, benefiting from their reconfigurability and reliability. The telecommunications sector also leverages these FPGAs for network infrastructure, where they facilitate efficient data processing and adaptability to evolving standards.

Application Insights

In 2024, the telecommunications segment held a dominant position in the Flash-Based FPGA market, capturing more than a 25.5% share. This leadership is attributed to the escalating demand for high-speed, low-latency communication networks, driven by the proliferation of 5G infrastructure and the increasing reliance on data-intensive applications.

Flash-based FPGAs, with their non-volatile memory and instant-on capabilities, offer the flexibility and performance required to meet the dynamic needs of modern telecommunication systems. Their reprogrammable nature allows for rapid deployment and adaptation to evolving standards, making them indispensable in the development and maintenance of advanced network infrastructures.

The integration of flash-based FPGAs in telecommunications equipment, such as base stations, routers, and switches, has become increasingly prevalent due to their ability to handle complex signal processing tasks efficiently. These FPGAs support the implementation of network functions virtualization (NFV) and software-defined networking (SDN), enabling service providers to optimize network performance and reduce operational costs.

Technology Insights

In 2024, the Single-Mode FPGAs segment held a dominant market position, capturing more than a 38.2% share. This leadership is primarily attributed to their streamlined architecture, which offers optimized performance for specific applications.

Single-Mode FPGAs are particularly favored in industries where dedicated functionalities are paramount, such as telecommunications, automotive, and industrial automation. Their design simplicity translates to lower power consumption and reduced latency, making them ideal for real-time processing tasks.

The telecommunications sector, for instance, benefits from Single-Mode FPGAs in managing fixed signal processing tasks, ensuring consistent and reliable performance. In the automotive industry, these FPGAs are utilized in systems like electronic control units (ECUs) where specific, unchanging functions are required.

Moreover, the industrial automation field leverages Single-Mode FPGAs for tasks such as motor control and sensor data processing, where deterministic behavior is crucial. The cost-effectiveness and reliability of Single-Mode FPGAs make them a preferred choice for applications where flexibility is less critical than performance and efficiency.

End-User Industry Insights

In 2024, the Information Technology (IT) segment held a dominant position in the Flash-Based FPGA market, capturing more than a 27.5% share. This prominence is primarily driven by the escalating demand for high-performance computing, data centers, and cloud services, which require adaptable and efficient hardware solutions.

Flash-based FPGAs, with their non-volatile memory and instant-on capabilities, offer the flexibility and performance needed to meet the dynamic requirements of modern IT infrastructures. Their reprogrammable nature allows for rapid deployment and adaptation to evolving standards, making them indispensable in the development and maintenance of advanced IT systems.

The integration of flash-based FPGAs in IT applications, such as data centers and cloud computing platforms, has become increasingly prevalent due to their ability to handle complex processing tasks efficiently. These FPGAs support the implementation of virtualization and software-defined networking (SDN), enabling service providers to optimize system performance and reduce operational costs.

Furthermore, the growing emphasis on edge computing and the Internet of Things (IoT) has necessitated the deployment of adaptable and secure hardware solutions, further cementing the role of flash-based FPGAs in the IT sector.

Design Type Insights

In 2024, the Custom Design FPGAs segment held a dominant market position, capturing more than a 40% share. This leadership is primarily attributed to the increasing demand for tailored hardware solutions that meet specific application requirements across various industries.

Custom Design FPGAs offer the flexibility to optimize performance, power consumption, and integration, making them ideal for specialized applications in sectors such as aerospace, defense, and telecommunications. The ability to fine-tune these FPGAs to exact specifications allows for enhanced system efficiency and reliability, which is crucial in mission-critical operations.

Moreover, the rise of emerging technologies like artificial intelligence (AI), machine learning (ML), and edge computing has further propelled the adoption of Custom Design FPGAs. These technologies often require unique processing capabilities and rapid adaptability, which custom FPGAs can provide.

For instance, in AI applications, custom FPGAs can be designed to accelerate specific algorithms, resulting in faster processing times and reduced latency. Additionally, the growing complexity of systems in automotive and industrial automation sectors necessitates bespoke FPGA solutions that can seamlessly integrate with existing architectures while meeting stringent performance standards.

Key Market Segments

By Product Type

- Low-End FPGAs

- Mid-Range FPGAs

- High-End FPGAs

By Application

- Telecommunications

- Automotive

- Consumer Electronics

- Aerospace & Defense

- Industrial Automation

- Others

By Technology

- Single-Mode FPGAs

- Multi-Mode FPGAs

- System-on-Chip (SoC) FPGAs

By End-User Industry

- Healthcare

- Information Technology

- Education

- Financial Services

- Energy and Utilities

- Others

By Design Type

- Custom Design FPGAs

- Standard Design FPGAs

- Application-Specific FPGAs

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Emerging Trends

Integration of AI and Edge Computing in Flash-Based FPGAs

Flash-based Field-Programmable Gate Arrays (FPGAs) are increasingly being integrated into artificial intelligence (AI) and edge computing applications. Their reprogrammable nature and low power consumption make them well-suited for real-time data processing at the edge, such as in autonomous vehicles and smart sensors.

By enabling on-device processing, these FPGAs reduce latency and reliance on cloud computing, enhancing performance and security. Furthermore, the flexibility of flash-based FPGAs allows for rapid adaptation to evolving AI algorithms, providing a competitive advantage in fast-paced technological environments.

As industries continue to embrace AI and edge computing, the demand for adaptable and efficient hardware solutions like flash-based FPGAs is expected to increase, offering substantial growth potential in this emerging market segment.

Business Benefit

Cost Reduction through Instant-On Capability

Flash-based FPGAs offer significant business benefits, particularly in reducing system costs and improving efficiency. Their instant-on capability eliminates the need for external configuration memory and reduces system complexity. This feature not only conserves energy but also enhances reliability in mission-critical applications like aerospace and medical devices.

Additionally, the non-volatile nature of flash memory allows these FPGAs to retain their configuration even when powered off, which is a practical advantage for power-constrained missions. By simplifying design and reducing the bill of materials, flash-based FPGAs enable businesses to develop cost-effective solutions without compromising on performance or reliability.

Driver

Ultra-Low Power Consumption Enhancing Energy Efficiency

Flash-based FPGAs are increasingly favored for their ultra-low power consumption, making them ideal for energy-sensitive applications. Devices like Microchip’s IGLOO series demonstrate this advantage, consuming as little as 5 µW in Flash*Freeze mode while retaining full functionality. This capability is particularly beneficial in battery-powered devices, such as wearables and remote sensors, where energy efficiency is paramount.

The non-volatile nature of flash memory allows these FPGAs to be “instant-on,” eliminating the need for external configuration memory and reducing system complexity. This feature not only conserves energy but also enhances reliability in mission-critical applications like aerospace and medical devices. As industries increasingly prioritize energy efficiency, the demand for flash-based FPGAs is expected to grow, driven by their ability to deliver performance without compromising on power consumption.

Restraint

High Initial Development Costs and Design Complexity

Despite their advantages, flash-based FPGAs present challenges in terms of high initial development costs and design complexity. The specialized knowledge required for hardware description languages (HDLs) and the intricate design processes can be barriers for small and medium-sized enterprises. Additionally, the need for skilled professionals and advanced tools increases the overall cost of development.

These factors can deter adoption, particularly in cost-sensitive markets. While larger organizations may absorb these costs, smaller companies might find the investment prohibitive, potentially limiting innovation and slowing the adoption rate of flash-based FPGAs in certain sectors. Addressing these challenges through improved design tools and training could help mitigate these restraints and broaden the technology’s appeal.

Opportunity

Integration in AI and Edge Computing Applications

The rise of artificial intelligence (AI) and edge computing presents significant opportunities for flash-based FPGAs. Their reprogrammable nature and low power consumption make them well-suited for AI applications that require real-time data processing at the edge, such as autonomous vehicles and smart sensors.

Furthermore, the flexibility of flash-based FPGAs allows for rapid adaptation to evolving AI algorithms, providing a competitive advantage in fast-paced technological environments. As industries continue to embrace AI and edge computing, the demand for adaptable and efficient hardware solutions like flash-based FPGAs is expected to increase, offering substantial growth potential in this emerging market segment.

Challenge

Design Complexity and Skill Shortage

The complexity of designing with flash-based FPGAs poses a significant challenge, particularly due to the shortage of skilled professionals proficient in HDLs and FPGA architecture. The intricate nature of FPGA design requires a deep understanding of both hardware and software, which can be a steep learning curve for engineers accustomed to traditional programming.

This skill gap can lead to longer development times and increased costs, potentially hindering the adoption of flash-based FPGAs. To overcome this challenge, investments in education and training are essential, along with the development of more user-friendly design tools that can lower the barrier to entry. By addressing the skill shortage and simplifying the design process, the industry can facilitate broader adoption and unlock the full potential of flash-based FPGAs.

Key Player Analysis

Achronix Semiconductor Corporation offers high-performance FPGAs and embedded FPGA (eFPGA) IP solutions, catering to data center, networking, and AI applications. Their Speedster7t FPGAs are designed for high-bandwidth workloads, integrating features like 400G Ethernet and PCIe Gen5 interfaces. Achronix’s eFPGA IP enables integration into SoCs, providing flexibility and performance benefits.

QuickLogic Corporation specializes in ultra-low-power FPGAs and eFPGA IP for consumer, industrial, and aerospace applications. Their solutions are optimized for always-on voice and sensor processing, with a focus on AI and IoT edge devices. QuickLogic’s Aurora eFPGA IP allows for customization in SoC designs, enhancing adaptability.

Cobham Limited provides radiation-hardened FPGAs suitable for aerospace and defense sectors. Their flash-based FPGAs are designed to withstand harsh environments, ensuring reliability in space and military applications. Cobham’s solutions support long-term missions where durability is critical.

Top Key Players Covered

- Achronix Semiconductor Corporation

- Quick Logic Corporation

- Cobham Limited

- Efinix Inc

- Flex Logix Technologies

- Intel Corporation

- Xilinx

- Aldec

- GOWIN Semiconductor Corp

- Lattice Semiconductor

- Omnitek

- EnSilica

- Gidel

- BitSim AB

- ByteSnap Design

- Cyient

- Enclustra

- Mistral Solution Pvt. Ltd.

- Microsemi Corporation

- Nuvation

- Others

Recent Developments

- Integration with Faraday’s FlashKit: In April 2025, QuickLogic’s eFPGA technology was integrated into Faraday’s FlashKit-22RRAM SoC platform, enhancing post-silicon hardware adaptability.

- Speedster® AC7t800 FPGA: In October 2024, Achronix introduced the Speedster® AC7t800, a mid-range FPGA offering 12 Tbps of fabric bandwidth, 400GE, and PCIe Gen5 interfaces, targeting AI/ML, 5G/6G, and data center applications.

- Acquisition of Flex Logix: In November 2024, ADI acquired Flex Logix, a pioneer in embedded FPGA and AI IP technology, to bolster its digital capabilities and integrate FPGA fabric into SoCs and ASICs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.4 Bn |

| Forecast Revenue (2034) | USD 11.6 Bn |

| CAGR (2025-2034) | 10.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Product Type (Low-End FPGAs, Mid-Range FPGAs, High-End FPGAs), By Application (Telecommunications, Automotive, Consumer Electronics, Aerospace & Defense, Industrial Automation, Others), By Technology (Single-Mode FPGAs, Multi-Mode FPGAs, System-on-Chip (SoC) FPGAs), By End-User Industry (Healthcare, Information Technology, Education, Financial Services, Energy and Utilities, Others), By Design Type (Custom Design FPGAs, Standard Design FPGAs, Application-Specific FPGAs) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Achronix Semiconductor Corporation, Quick Logic Corporation, Cobham Limited, Efinix Inc, Flex Logix Technologies, Intel Corporation, Xilinx, Aldec, GOWIN Semiconductor Corp, Lattice Semiconductor, Omnitek, EnSilica, Gidel, BitSim AB, ByteSnap Design, Cyient, Enclustra, Mistral Solution Pvt. Ltd., Microsemi Corporation, Nuvation, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |