Global Firmware Signing Platform Market By Component (Software, Hardware, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small and Medium Enterprises, Large Enterprises), By Application (Consumer Electronics, Automotive, Industrial Control Systems, Healthcare Devices, IoT Devices, Others), By End-User (Manufacturing, Automotive, Healthcare, IT and Telecommunications, Consumer Electronics, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 179477

- Number of Pages: 342

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component

- By Deployment Mode

- By Organization Size

- By End User

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

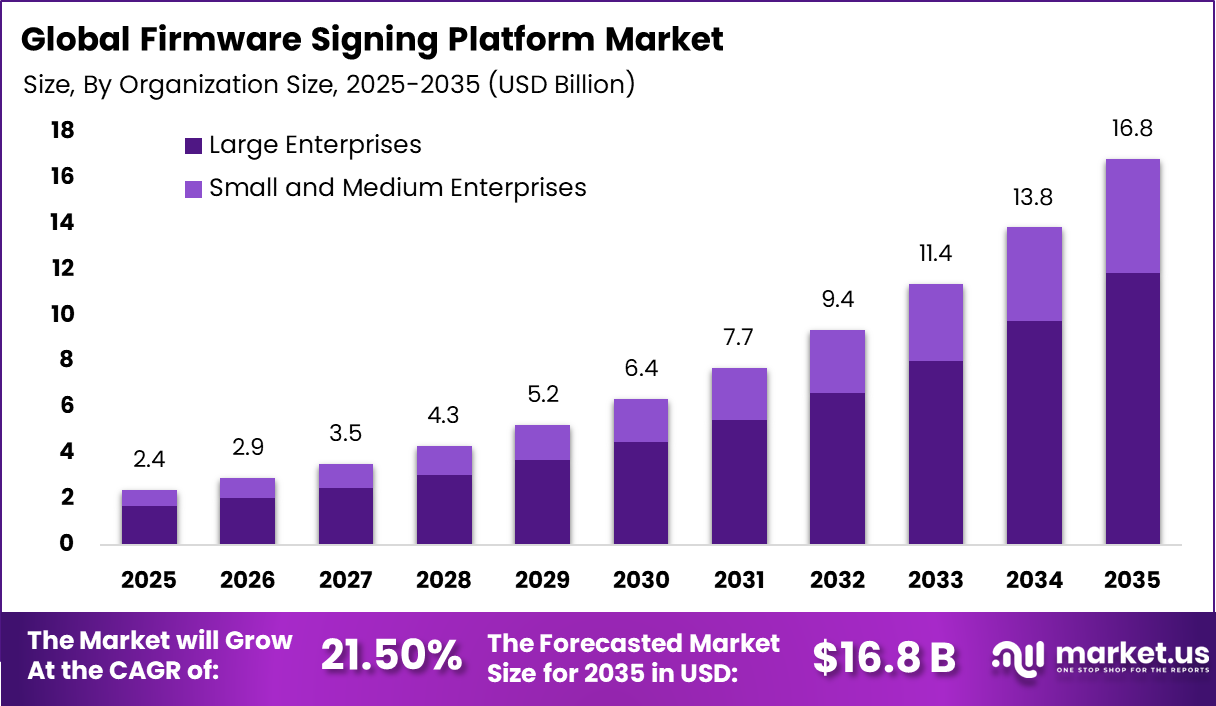

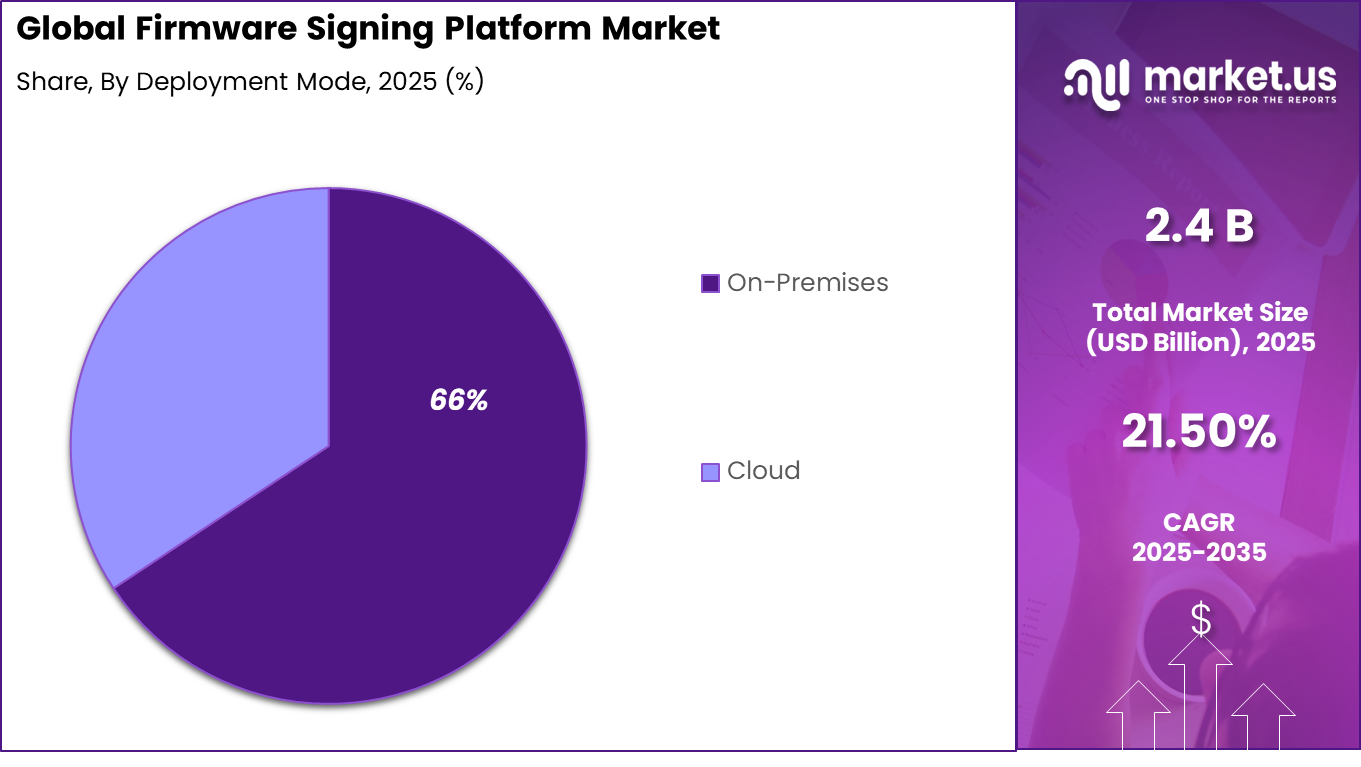

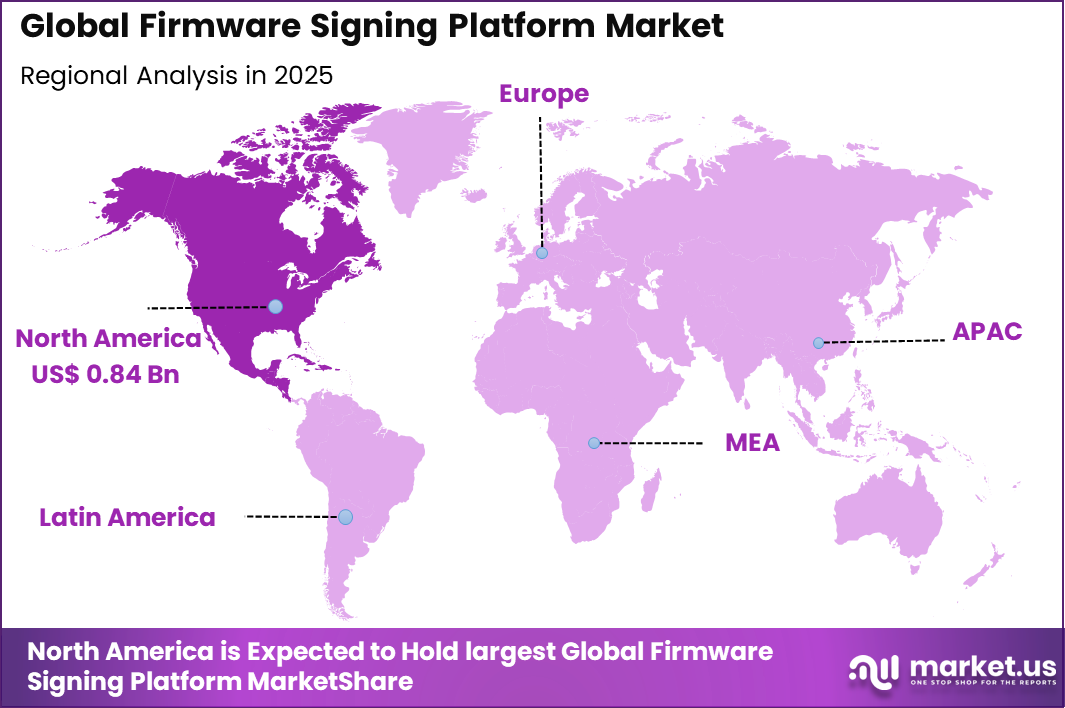

The Global Firmware Signing Platform Market generated USD 2.4 billion in 2025 and is predicted to register growth from USD 2.9 billion in 2026 to about USD 16.8 billion by 2035, recording a CAGR of 21.50% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 35.2% share, holding USD 0.84 Billion revenue.

The firmware signing platform market consists of software and services that authenticate and verify firmware integrity before deployment to hardware devices. Firmware is low-level software embedded in machines, connected devices, and industrial equipment that controls basic functions. Firmware signing platforms use cryptographic methods to attach digital signatures to firmware packages, ensuring that only verified and untampered code can be installed on endpoints.

As connected and embedded systems proliferate across consumer electronics, industrial automation, and Internet of Things environments, the need to secure foundational software components has increased. Firmware signing platforms provide trust anchors that help manufacturers and operators enforce update policies, verify authenticity during boot processes, and maintain long-term device integrity.

A key growth driver is the rising concern over firmware attacks that exploit insecure update channels or compromised software releases. Firmware vulnerabilities can enable persistent threats, unauthorized access, or malicious control of critical devices. Firmware signing platforms prevent installation of unauthorized code by validating cryptographic signatures at the device level, reducing exposure to tampering and supply chain attacks.

Top Market Takeaways

- By Component, hardware leads with 55.3% share, featuring Hardware Security Modules (HSMs) and Trusted Platform Modules (TPMs) for root-of-trust key generation and tamper-resistant firmware attestation.

- By Deployment Mode, on-premises dominates at 65.7%, enabling air-gapped signing ceremonies, sovereign key custody, and integration with secure build pipelines.

- By Organization Size, large enterprises capture 70.4%, orchestrating firmware signing across global device fleets with automated approval workflows and audit trails.

- By End-User, manufacturing holds 40.7%, protecting PLCs, robots, and IoT edge devices against firmware tampering and remote code execution vulnerabilities.

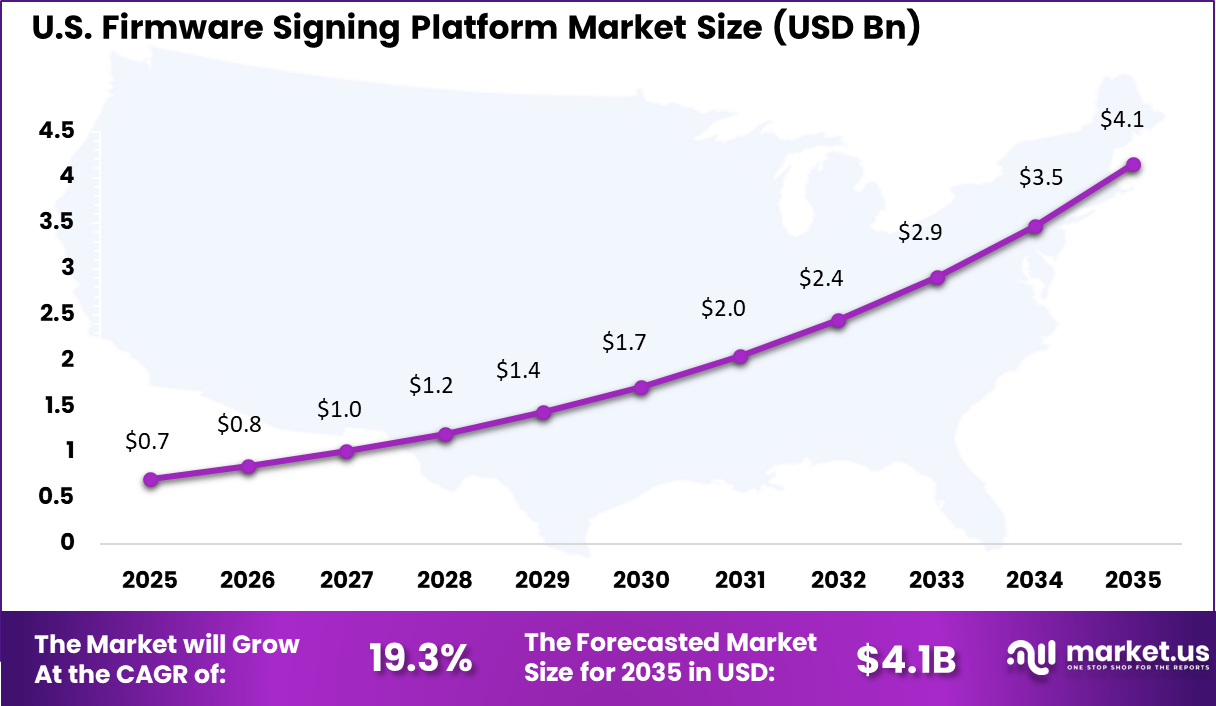

- Regionally, North America accounts for 35.2% global share, with the U.S. market valued at USD 0.71 billion and a CAGR of 19.3%, driven by NIST 800-193 compliance and critical infrastructure protection initiatives.

Drivers Impact Analysis

Key Drivers Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Strategic Importance Rising Firmware-level Cyber Attacks +4.5% North America, Europe Short to Long Term Drives mandatory secure boot and signing policies Growth in IoT and Connected Devices +3.9% APAC, North America Medium to Long Term Expands device authentication requirements Increasing Regulatory Compliance for Device Security +3.2% North America, Europe Medium Term Enforces trusted code validation Adoption of Secure Software Development Lifecycle +2.8% Global Medium Term Integrates signing into CI/CD workflows Expansion of Automotive and Industrial Automation +2.3% Europe, APAC Long Term Requires protected firmware updates Restraints Impact Analysis

Key Restraints Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Market Constraint Level High Implementation and Key Management Costs -2.4% Emerging Markets Short to Medium Term Budget limitations in small manufacturers Complexity of Legacy Embedded Systems -2.0% Europe, APAC Medium Term Integration challenges Limited Cryptographic Expertise in SMEs -1.7% Global Medium Term Slows adoption pace Fragmentation Across Device Ecosystems -1.4% Global Medium to Long Term Standardization gaps By Component

Hardware accounts for 55.3% of the market, reflecting the importance of physical security modules in protecting cryptographic keys and signing credentials. Secure hardware elements such as hardware security modules and trusted platform modules are widely deployed to prevent unauthorized firmware modification. These solutions provide tamper resistance and isolated key storage, which are essential for safeguarding device integrity.

The dominance of hardware is supported by regulatory and compliance expectations in sectors managing critical infrastructure. Organizations require strong cryptographic assurance to protect firmware updates from malicious interference. As connected devices increase across industrial and consumer environments, hardware based signing mechanisms continue to serve as the foundation of secure firmware ecosystems.

By Deployment Mode

On premises deployment represents 65.7% of the market, indicating a strong preference for direct control over cryptographic infrastructure. Many enterprises manage sensitive intellectual property and proprietary firmware code, which necessitates internal key management and signing environments. On premises solutions provide greater customization and strict access controls aligned with internal security policies.

Industries handling mission critical operations often avoid external hosting environments due to regulatory and operational risks. Maintaining firmware signing systems within controlled data centers reduces exposure to third party vulnerabilities. As cybersecurity threats targeting supply chains increase, organizations continue to prioritize internalized deployment models.

By Organization Size

Large enterprises account for 70.4% of market adoption due to their extensive device portfolios and complex operational networks. These organizations often manage thousands of connected endpoints, requiring centralized and standardized firmware validation processes. Dedicated cybersecurity teams and structured governance frameworks enable large enterprises to implement comprehensive signing platforms.

The scale of firmware distribution in large enterprises increases the risk of exploitation if security controls are weak. Formalized signing procedures ensure authenticity before firmware is deployed across production systems. As digital manufacturing and smart infrastructure initiatives expand, large enterprises remain the primary adopters of advanced signing platforms.

By End User

Manufacturing holds 40.7% of market adoption, driven by the rapid integration of connected machinery and industrial control systems. Smart factories rely on secure firmware updates to maintain operational continuity and protect against cyber intrusion. Compromised firmware in industrial equipment can result in production disruption and financial losses.

Manufacturers are increasingly implementing secure development lifecycle practices to strengthen product integrity. Firmware signing ensures that only verified updates are deployed across robotics, programmable logic controllers, and embedded sensors. As industrial automation continues to expand, secure firmware validation remains a strategic requirement.

Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Venture Capital Very High High North America, Israel Strong focus on embedded security startups Private Equity High Medium North America, Europe Attractive recurring enterprise security models Strategic Semiconductor and IoT Vendors Medium to High Low to Medium Global Portfolio expansion through integration Government & Sovereign Funds Medium Low North America, Asia Critical infrastructure and defense priority Institutional Investors Medium Medium Developed Markets Long-term cybersecurity allocation Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Adoption Momentum Hardware Security Modules Integration +3.6% North America, Europe Medium to Long Term Strengthens cryptographic key protection Secure Boot and Root of Trust Architectures +3.1% Global Short to Medium Term Ensures device integrity at startup Cloud-based Key Management Systems +2.7% APAC, North America Medium Term Enables scalable signing operations AI-driven Firmware Integrity Monitoring +2.2% North America Long Term Detects unauthorized firmware changes Post-Quantum Cryptography Adoption +1.8% Europe, North America Long Term Future-proof encryption strategies Emerging Trends

In the Firmware Signing Platform market, a strong trend is the use of integrated signing processes that connect development tools with verification checks before firmware is deployed. Rather than treating signing as a final step, organisations are embedding checks earlier in the development cycle so that every build carries a clear assurance of authenticity and origin.

This approach supports a more dependable process where devices can verify the source of updates and reject unauthorised code before it runs. Another pattern emerging is the presentation of signing results in clear, human-readable summaries that help engineers and operations teams understand what was signed, when, and why, reducing uncertainty during update rollouts.

Growth Factors

A key growth driver in this market is the increasing reliance on connected devices and systems that depend on regular firmware updates for security and functionality. When firmware is not signed properly, devices can be vulnerable to tampered code or unintended behaviour, which erodes trust in product safety. Signing platforms help reinforce confidence by making sure each update carries a verifiable signature.

Another important factor is the growing emphasis on accountability across the device lifecycle. Organisations and users want reassurance that updates and patches are genuine, and a structured signing process provides a clear record of how firmware was authenticated. This combination of security assurance and operational clarity supports broader adoption of signing practices that feel reliable and transparent to all stakeholders.

Key Market Segments

By Component

- Software

- Hardware

- Services

By Deployment Mode

- On-Premises

- Cloud

By Organization Size

- Small and Medium Enterprises

- Large Enterprises

By Application

- Consumer Electronics

- Automotive

- Industrial Control Systems

- Healthcare Devices

- IoT Devices

- Others

By End-User

- Manufacturing

- Automotive

- Healthcare

- IT and Telecommunications

- Consumer Electronics

- Others

Regional Analysis

North America holds a 35.2% share of the firmware signing platform market, supported by strong presence of semiconductor, automotive, industrial automation, and connected device manufacturers. Organizations in the region are adopting secure firmware signing solutions to ensure code integrity, prevent unauthorized modifications, and protect embedded systems from cyber threats. Demand is driven by increasing deployment of IoT devices, regulatory focus on device security, and the need to safeguard over-the-air firmware updates across distributed hardware environments.

The U.S. market is valued at USD 0.71 Bn and is expanding at a CAGR of 19.3%, reflecting rising emphasis on secure software supply chains and hardware-level protection. Adoption is influenced by growing cybersecurity risks targeting connected infrastructure, automotive electronics, and industrial control systems. Growth is further supported by integration of hardware security modules, secure boot architectures, and automated signing workflows that enhance device authenticity and long-term operational resilience.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The Firmware Signing Platform Market is strongly influenced by global technology leaders that integrate secure boot and code signing capabilities within operating systems and device ecosystems. Microsoft Corporation, Google LLC, and Apple Inc. embed firmware validation frameworks across desktops, mobile devices, and cloud infrastructure. These companies define security standards that are widely adopted by OEMs and enterprise customers.

Cybersecurity and digital certificate providers strengthen the authentication layer of firmware signing solutions. Symantec Corporation under Broadcom Inc., DigiCert Inc., and McAfee LLC deliver encryption, key management, and code integrity verification services. Industrial and security focused firms such as Thales Group and Siemens AG provide hardware backed security modules for critical infrastructure. Their expertise supports compliance with global cybersecurity standards and secure supply chain requirements.

Semiconductor and embedded system providers form the hardware backbone of the market. Infineon Technologies AG, Renesas Electronics Corporation, Microchip Technology Inc., Texas Instruments Incorporated, and NXP Semiconductors N.V. integrate secure elements and trusted platform modules within chips. Technology infrastructure firms including Wind River Systems, Inc., Hewlett Packard Enterprise, Cisco Systems, Inc., Samsung Electronics Co., Ltd., Intel Corporation, and Arm Holdings plc further strengthen ecosystem integration.

Top Key Players in the Market

- Microsoft Corporation

- Google LLC

- Apple Inc.

- IBM Corporation

- Symantec Corporation (Broadcom Inc.)

- DigiCert Inc.

- McAfee LLC

- Thales Group

- Infineon Technologies AG

- Siemens AG

- Renesas Electronics Corporation

- Microchip Technology Inc.

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- Wind River Systems, Inc.

- Hewlett Packard Enterprise (HPE)

- Cisco Systems, Inc.

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Arm Holdings plc

- Others

Future Outlook

The future outlook for the Firmware Signing Platform Market is positive as more device manufacturers and industries focus on improving security for embedded systems. Demand for firmware signing platforms is expected to grow because these solutions help ensure firmware updates are authentic and protected from tampering.

Adoption of automated signing, secure key management, and integration with development workflows will improve trust and reduce risk. Growth can be attributed to rising cyber threats targeting firmware, stronger regulatory requirements, and the need to protect connected devices. Overall, the market is expected to expand as businesses prioritize secure and reliable firmware practices.

Recent Developments

- Broadcom’s Symantec handles EV certs for firmware. In November 2025, they updated their platform for NIST-compliant signing ceremonies. It’s steady evolution post-Broadcom acquisition.

- DigiCert dominates cert issuance for devices. They launched automated firmware signing workflows in September 2025, cutting manual steps by half. HSM integration shines for scale.

Report Scope

Report Features Description Market Value (2025) USD 2.4 Billion Forecast Revenue (2035) USD 16.8 Billion CAGR(2025-2035) 21.50% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Software, Hardware, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small and Medium Enterprises, Large Enterprises), By Application (Consumer Electronics, Automotive, Industrial Control Systems, Healthcare Devices, IoT Devices, Others), By End-User (Manufacturing, Automotive, Healthcare, IT and Telecommunications, Consumer Electronics, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Microsoft Corporation, Google LLC, Apple Inc., IBM Corporation, Symantec Corporation (Broadcom Inc.), DigiCert Inc., McAfee LLC, Thales Group, Infineon Technologies AG, Siemens AG, Renesas Electronics Corporation, Microchip Technology Inc., Texas Instruments Incorporated, NXP Semiconductors N.V., Wind River Systems, Inc., Hewlett Packard Enterprise (HPE), Cisco Systems, Inc., Samsung Electronics Co., Ltd., Intel Corporation, Arm Holdings plc, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Firmware Signing Platform MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Firmware Signing Platform MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Microsoft Corporation

- Google LLC

- Apple Inc.

- IBM Corporation

- Symantec Corporation (Broadcom Inc.)

- DigiCert Inc.

- McAfee LLC

- Thales Group

- Infineon Technologies AG

- Siemens AG

- Renesas Electronics Corporation

- Microchip Technology Inc.

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- Wind River Systems, Inc.

- Hewlett Packard Enterprise (HPE)

- Cisco Systems, Inc.

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Arm Holdings plc

- Others

Our Clients

- 179477

- Feb. 2026