Quick Navigation

- Report Overview

- Key Takeaways

- Component Analysis

- Fault type Analysis

- Technology Analysis

- End-Use Industries Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Regional Analysis

- Key Player Analysis

- Top Opportunities Awaiting for Players

- Recent Developments

- Report Scope

Report Overview

The Global Fault Detection and Classification (FDC) Market size is expected to be worth around USD 12.7 Billion By 2033, from USD 5.2 Billion in 2023, growing at a CAGR of 9.30% during the forecast period from 2024 to 2033. In 2023, North America dominated the Fault Detection and Classification (FDC) market, capturing over 33.7% share, which translated to approximately USD 1.7 billion in revenue.

Fault Detection and Classification (FDC) refers to a set of techniques and processes used to identify and classify faults in a system, machine, or process. The primary goal of FDC is to detect abnormal conditions, diagnose the cause, and classify the severity or type of fault, enabling proactive maintenance and repair actions. This technology plays a crucial role in industries, where early detection of faults can reduce downtime, enhance system reliability, and improve overall safety.

The Fault Detection and Classification (FDC) market has witnessed significant growth over recent years due to increasing demand for advanced monitoring and predictive maintenance solutions. The market’s expansion is largely driven by the need for enhanced operational efficiency, reduced downtime, and improved safety standards across various industries. The adoption of automation and the shift toward Industry 4.0 have also created a favorable environment for FDC technologies.

The Fault Detection and Classification market is being driven by several key factors. One of the primary drivers is the growing demand for automation and smart technologies across industries, which requires advanced systems for fault detection and diagnostic capabilities. Increasing industrial complexity and the need for operational efficiency are pushing organizations to adopt FDC systems to minimize downtime and prevent costly disruptions.

Moreover, the growing emphasis on predictive maintenance, which aims to identify potential failures before they occur, is also contributing to market expansion. Rising awareness about the importance of system reliability, along with regulatory pressures to maintain high operational standards, further supports the demand for FDC solutions.

The demand for Fault Detection and Classification systems is surging across sectors such as manufacturing, automotive, aerospace, and energy. In the manufacturing sector, the emphasis on automation and the increasing complexity of production lines have necessitated the adoption of real-time monitoring systems capable of detecting faults quickly and accurately.

In the automotive industry, the shift towards electric vehicles (EVs) and autonomous driving technologies has also driven the demand for advanced FDC systems to ensure vehicle reliability and safety. The Fault Detection and Classification market offers several growth opportunities, especially with the ongoing advancements in AI, machine learning, and data analytics.

The application of AI-based algorithms for predictive maintenance is seen as a key growth area, as it enables systems to learn from historical data and detect faults with greater accuracy. The integration of FDC technologies into Industry 4.0 frameworks offers another significant opportunity, as it facilitates the real-time exchange of data across the value chain, enhancing overall system performance.

Technological advancements in the FDC market are primarily focused on the integration of artificial intelligence (AI) and machine learning (ML) algorithms, which are significantly improving fault detection accuracy. These advancements enable systems to not only detect faults but also predict potential failures, thereby offering a proactive approach to maintenance.

Additionally, advancements in sensor technologies are enhancing the ability to monitor real-time data more precisely, while the integration of IoT devices allows for more seamless and remote monitoring of critical assets. Cloud computing and edge computing are also playing a significant role in enhancing data processing capabilities, allowing for faster and more reliable fault detection.

Key Takeaways

- The Global Fault Detection and Classification (FDC) Market size is projected to reach approximately USD 12.7 Billion by 2033, up from USD 5.2 Billion in 2023, growing at a CAGR of 9.30% from 2024 to 2033.

- North America held a dominant position in the FDC market in 2023, capturing more than 33.7% share, which equated to around USD 1.7 billion in revenue.

- In 2023, the Hardware segment led the FDC market with more than 43% share.

- In 2023, the Machine Learning Algorithm segment captured more than 38.2% share in the FDC market.

- The Electronic and Semiconductor segment accounted for more than 31.2% share in the FDC market in 2023.

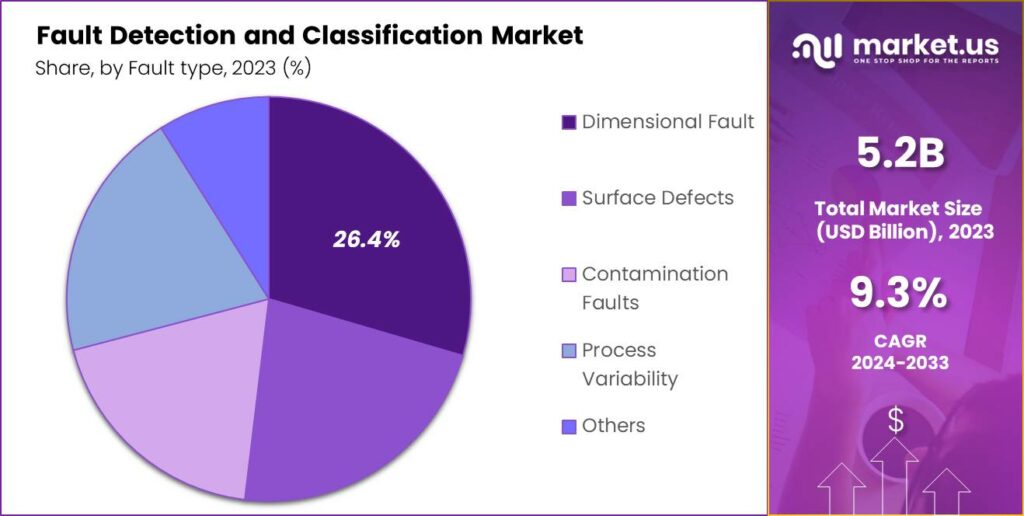

- In 2023, the Dimensional Fault segment held a dominant position in the FDC market, capturing more than 26.4% share.

Component Analysis

In 2023, the Hardware segment held a dominant position in the Fault Detection and Classification (FDC) market, capturing more than a 43% share. This segment comprises the physical components and devices essential for the implementation of FDC systems, including sensors, processors, and other monitoring equipment.

Hardware is critical because it forms the backbone of FDC systems, directly influencing their efficiency and accuracy in detecting faults. The robustness of these components ensures reliable data collection, which is crucial for the accurate monitoring and analysis of semiconductor manufacturing processes.

The leadership of the Hardware segment can be attributed to the continuous advancements in sensor technology and the integration of sophisticated electronics into manufacturing equipment. As semiconductor processes become more complex, the demand for high-precision monitoring tools that can operate under stringent conditions has increased.

Another factor driving the prominence of the Hardware segment is the increasing adoption of Industry 4.0 principles, where automation and data exchange in manufacturing technologies are pivotal. In this context, the hardware used in FDC systems is designed to seamlessly integrate with existing manufacturing infrastructure, enabling real-time data transfer and communication.

Fault type Analysis

In 2023, the Dimensional Fault segment held a dominant position in the Fault Detection and Classification (FDC) market, capturing more than a 26.4% share. This segment’s leadership can be attributed to the critical importance of dimensional accuracy in semiconductor manufacturing.

Dimensional faults, which include issues like layer thickness deviations and line width variations, can significantly impact the functionality and yield of semiconductor devices. As device architectures become more complex and feature sizes shrink, the precision required in dimensional measurements increases, driving demand for robust FDC systems that specialize in detecting these faults.

The Surface Defects segment also plays a vital role in the FDC market. Surface defects, such as scratches, pits, and particulate contamination on the wafer surface, can lead to device failure or underperformance. The need to maintain high surface integrity has become more pronounced with the advancement in semiconductor technologies, where even minor imperfections can lead to significant losses.

Another key segment in the FDC market is Contamination Faults. These faults occur when unwanted particles or chemicals contaminate the wafer during the manufacturing process, leading to potential device failure or degradation.

Technology Analysis

In 2023, the Machine Learning Algorithm segment held a dominant position in the Fault Detection and Classification (FDC) market, capturing more than a 38.2% share. This leading stance can be attributed to the advanced capabilities of machine learning algorithms to analyze and interpret complex datasets, far surpassing the efficiency of traditional statistical methods.

The superiority of machine learning algorithms in fault detection lies in their adaptability and learning prowess. Unlike static statistical methods, these algorithms can improve over time, adapting to new conditions without explicit programming.

This feature is particularly advantageous in sectors such as semiconductor manufacturing and heavy machinery, where equipment conditions can vary widely and unpredictably. Machine learning algorithms’ ability to self-adjust and learn from new data helps in accurately predicting faults before they lead to system failures.

Another factor contributing to the dominance of the Machine Learning Algorithm segment is the integration of IoT and big data technologies in industrial operations. As industries continue to embrace digital transformation, the influx of data from IoT devices has become overwhelming for traditional data processing methods.

End-Use Industries Analysis

In 2023, the Electronic and Semiconductor segment held a dominant market position in the Fault Detection and Classification (FDC) market, capturing more than a 31.2% share. This segment’s leadership is primarily driven by the critical need for precision and operational efficiency in semiconductor manufacturing, where the cost of faults can be exceedingly high.

The demand for FDC systems in the electronics and semiconductor industry is further propelled by the miniaturization of electronic components and the rapid pace of technological advancements. As components become smaller and circuitry more complex, the margin for error narrows significantly.

Machine learning algorithms within FDC systems excel in detecting and classifying even the minutest discrepancies that traditional methods might overlook, thus preventing costly production delays and ensuring the reliability of electronic devices.

Additionally, the electronic and semiconductor industry’s shift towards automation and Industry 4.0 technologies has made FDC systems indispensable. These industries are leveraging FDC to not only detect faults but also predict them before they occur, thereby reducing downtime and maintenance costs.

Predictive maintenance enabled by advanced FDC systems helps in scheduling repairs and maintenance activities without disrupting the manufacturing process, which is vital for maintaining a continuous production flow.

Key Market Segments

By Component

- Software

- Hardware

- Services

By Fault type

- Dimensional Fault

- Surface Defects

- Contamination Faults

- Process Variability

- Others

By Technology

- Statistical Methods

- Machine Learning Algorithm

- Others

By End-Use Industries

- Automotive

- Electronic and Semiconductor

- Metals and Machinery

- Food and Packaging

- Pharmaceuticals

Driver

Increasing Complexity in Industrial Processes

As industries evolve, their systems and processes become more intricate, incorporating advanced technologies and interconnected components. This complexity heightens the risk of faults, making traditional manual monitoring insufficient.

Fault Detection and Classification (FDC) systems address this challenge by providing automated, real-time monitoring and analysis. They utilize sensors and data analytics to detect anomalies promptly, ensuring operational efficiency and product quality. The growing complexity of industrial processes necessitates robust FDC solutions to maintain system reliability and prevent costly downtimes.

Restraint

High Initial Investment Costs

Implementing FDC systems requires substantial upfront investments in hardware, software, and integration into existing processes. These costs can be a significant barrier, especially for small and medium-sized enterprises with limited budgets.

Additionally, the complexity of integrating FDC solutions into diverse manufacturing environments may necessitate specialized expertise, further increasing expenses. While the long-term benefits of FDC systems include improved efficiency and reduced downtime, the initial financial outlay can deter some organizations from adopting these technologies.

Opportunity

Adoption of Artificial Intelligence (AI) in FDC Systems

The integration of AI technologies into FDC systems presents significant opportunities for enhancing fault detection capabilities. AI-driven FDC solutions can analyze vast amounts of data in real-time, identify complex patterns, and predict potential faults before they occur.

This predictive maintenance approach minimizes downtime and optimizes operational efficiency. Furthermore, AI enables continuous learning and adaptation to new fault types, making FDC systems more robust and versatile across various industrial applications.

Challenge

Shortage of Skilled Professionals

The effective implementation and operation of FDC systems require skilled professionals proficient in both the technological and operational aspects of these solutions. However, there is a notable shortage of such expertise in the workforce.

This skills gap can impede the adoption and optimization of FDC systems, as organizations may struggle to find qualified personnel to manage and maintain these technologies. Addressing this challenge necessitates investment in training and education to develop a workforce capable of supporting advanced FDC implementations.

Emerging Trends

Fault Detection and Classification (FDC) systems are becoming more advanced, especially with the integration of artificial intelligence (AI) and machine learning. These technologies enable FDC systems to analyze complex data patterns, leading to quicker and more accurate fault identification.

In the manufacturing sector, there’s a growing emphasis on quality control. FDC systems play a crucial role by continuously monitoring processes and detecting deviations, which helps in maintaining high product quality.

The adoption of smart manufacturing, which combines digital technologies, data analytics and automation, is also driving the use of FDC systems. These systems help in monitoring complex manufacturing processes, ensuring efficiency and reducing downtime.

Business Benefits

Implementing Fault Detection and Classification (FDC) systems offers several business benefits. They enhance operational efficiency by identifying and addressing faults promptly, which reduces downtime and maintenance costs. This leads to increased productivity and better resource utilization.

FDC systems improve product quality by monitoring manufacturing processes in real-time and detecting anomalies. This ensures that products meet quality standards, leading to higher customer satisfaction and reduced returns or recalls.

Additionally, FDC systems support predictive maintenance strategies by analyzing equipment performance data to predict potential failures. This proactive approach allows businesses to schedule maintenance activities before issues escalate, extending equipment lifespan and optimizing maintenance schedules.

Furthermore, the integration of FDC systems with cloud-based solutions facilitates scalability and accessibility. Businesses can monitor operations across multiple locations in real-time, making it easier to manage and maintain consistent quality and performance standards.

Regional Analysis

In 2023, North America held a dominant position in the Fault Detection and Classification (FDC) market, capturing more than a 33.7% share, which equated to approximately USD 1.7 billion in revenue. This region’s leadership in the market can be primarily attributed to its advanced semiconductor manufacturing capabilities and the presence of numerous leading technology firms.

North America’s dominance is further bolstered by its robust technological infrastructure and substantial investments in research and development. This environment fosters the development of advanced hardware and software solutions that are critical to the effective implementation of FDC systems. The continuous push for miniaturization of electronic components in the region also necessitates the deployment of sophisticated FDC systems to maintain high yield rates and quality standards.

Moreover, the high adoption rate of Industry 4.0 technologies in North American manufacturing processes has significantly contributed to the growth of the FDC market in this region. Local manufacturers are keen on integrating artificial intelligence and machine learning with FDC systems to further automate and optimize manufacturing.

Additionally, the stringent regulatory standards for product quality in industries such as aerospace, automotive, and electronics in North America compel semiconductor manufacturers to invest in reliable FDC systems. These systems ensure compliance with quality standards by enabling manufacturers to detect and rectify faults at early stages, thereby reducing the risk of costly recalls and enhancing brand reputation.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

In the Fault Detection and Classification (FDC) market, several key players stand out due to their innovative solutions and substantial market influence.

Keyence Corporation has established itself as a pivotal player in the FDC market. Known for its high-quality sensors and imaging systems, Keyence’s technology is integral to the accurate detection and classification of faults in semiconductor production. Their commitment to research and development allows for continuous improvements in their FDC offerings.

Siemens is another major force in the FDC market, renowned for its comprehensive approach to industrial automation and digitalization. Siemens’ FDC systems are part of a broader portfolio of digital factory solutions that include sophisticated software and analytics tools.

OMRON Corporation specializes in automation and healthcare equipment, but its contributions to the FDC market are marked by innovations in sensor technology and artificial intelligence. OMRON’s FDC solutions leverage advanced AI to predict and identify defects in manufacturing processes more quickly and accurately than conventional methods.

Top Key Players in the Market

- Keyence Corporation

- Siemens

- OMRON Corporation

- Cognex Corporation

- Tokyo Electron Limited

- KLA Corporation

- Synopsys Inc.

- Applied Materials Inc.

- einnoSys Technologies Inc.

- PDF Solutions.

Top Opportunities Awaiting for Players

Exploring the top opportunities in the Fault Detection and Classification (FDC) market reveals several promising areas for industry players to capitalize on.

- Expansion of Smart Manufacturing: The shift towards Industry 4.0 and the integration of smart manufacturing processes offer significant opportunities for the implementation of FDC systems. These systems are crucial in enhancing manufacturing efficiency and product quality through real-time monitoring and automated quality control. As industries continue to adopt these advanced technologies, the demand for FDC solutions is expected to grow.

- Rising Complexity in Manufacturing: As manufacturing processes become more complex and the precision requirements increase, particularly in industries like semiconductor and electronics, there is a growing need for effective fault detection systems. FDC solutions can address these complexities by ensuring high-quality production standards are maintained, thus opening up substantial market opportunities.

- Advancements in Industry 4.0 Technologies: The integration of technologies such as the Internet of Things (IoT) and artificial intelligence into FDC systems enhances their capability to detect and classify faults more efficiently. This technological evolution not only improves the functionality of FDC systems but also broadens their applicability across various industrial sectors.

- Increasing Demand in Semiconductor and Electronics Industries: The semiconductor and electronics sectors are significant users of FDC systems due to their stringent quality control requirements. With the ongoing advancements in electronic devices and the continuous scaling down of semiconductor chip sizes, the demand for precise and reliable fault detection solutions is expected to rise, providing a lucrative opportunity for market players.

- Cloud-Based FDC Solutions: The trend towards cloud-based FDC systems is gaining momentum due to their cost-effectiveness, scalability, and flexibility. These systems allow for remote monitoring capabilities and easier integration with existing manufacturing infrastructure, which can significantly benefit companies looking to enhance their operational efficiencies and data management practices.

Recent Developments

- In September 2023, Synopsys released ‘Fab.da,’ an AI-driven process analytics and control solution designed to enhance operational efficiency in semiconductor fabs. Fab.da integrates data from product design, equipment sensors, fab operations, and testing to monitor equipment health, optimize processes and predict outcomes.

- In February 2024, Applied Materials introduced an AI-enhanced eBeam defect review system that combines advanced imaging with artificial intelligence. This system improves the identification and classification of defects in semiconductor manufacturing, enhancing yield and process control.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 5.2 Bn |

| Forecast Revenue (2033) | USD 12.7 Bn |

| CAGR (2024-2033) | 9.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Software, Hardware, Services), By Fault type (Dimensional Fault, Surface Defects, Contamination Faults, Process Variability, Others), By Technology (Statistical Methods, Machine Learning Algorithm, Others), By End-Use Industries (Automotive, Electronic and Semiconductor, Metals and Machinery, Food and Packaging, Pharmaceuticals) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Keyence Corporation, Siemens, OMRON Corporation, Cognex Corporation, Tokyo Electron Limited, KLA Corporation, Synopsys Inc., Applied Materials Inc., einnoSys Technologies Inc., PDF Solutions. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |