Global Facial Care Market Size, Share, Growth Analysis By Product (Lotion Face, Creams & Moisturizers, Cleansers & Face Wash, Facial Serums, Face Sheet Masks, Sunscreen/Sun Care, Others), By End Use (Women, Men), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Pharmacy & Drugstore, Online, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180141

- Number of Pages: 237

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

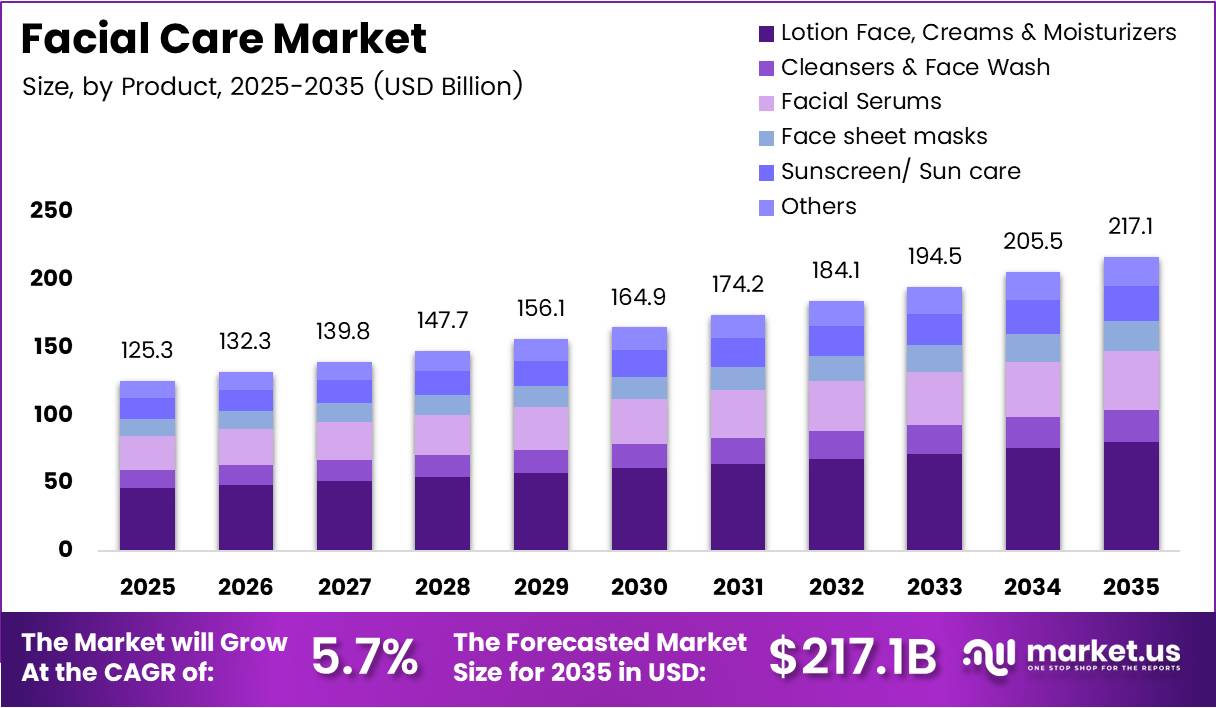

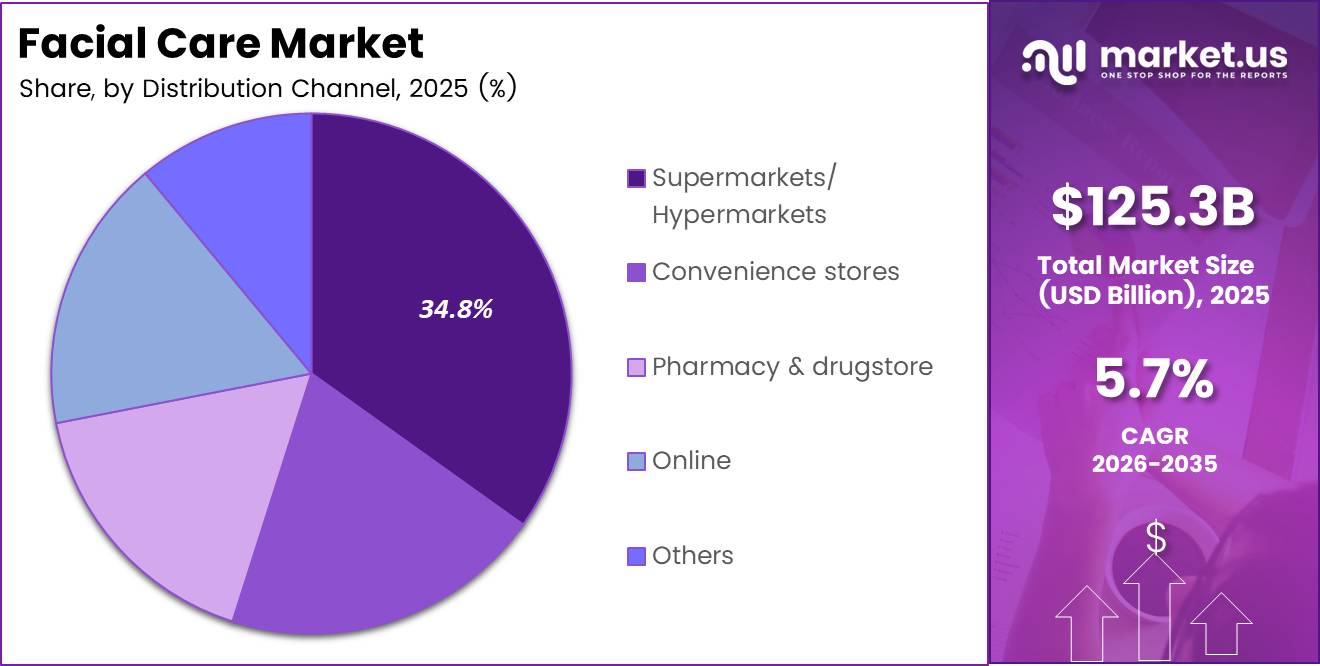

Global Facial Care Market size is expected to be worth around USD 217.1 Billion by 2035 from USD 125.3 Billion in 2025, growing at a CAGR of 5.7% during the forecast period 2026 to 2035.

The facial care market covers products designed for daily cleansing, moisturizing, sun protection, and treatment of the face. It spans lotions, creams, serums, face washes, sheet masks, and sunscreen formulations. Consumers across age groups now treat facial care as a non-negotiable part of daily health management, not an occasional indulgence.

This shift in consumer mindset has fundamentally changed the purchase cycle. Buyers no longer replace products when they run out — they upgrade continuously as new formulations, ingredients, and application technologies reach the shelf. Consequently, average transaction values rise even when unit volumes remain stable.

Premium and dermatologist-recommended product lines now command a disproportionate share of shelf space and online search traffic. Brands that can demonstrate clinical efficacy — rather than just cosmetic benefit — close sales faster and at higher margins. This dynamic increasingly favors companies with dermatology partnerships and ingredient transparency.

Government investment in dermatology awareness programs, combined with stricter cosmetic ingredient regulations across the EU and North America, is reshaping product development cycles. Manufacturers must now reformulate products more frequently to meet evolving safety standards, which raises barriers for undercapitalized entrants and strengthens incumbents with established R&D infrastructure.

In April 2024, Estée Lauder expanded its Re-Nutriv luxury skincare line with the Ultimate Diamond Transformative Energy Eye Creme — a move that signals continued premiumization momentum across the facial care category and validates the high-margin opportunity in luxury facial treatment products.

According to the American Academy of Dermatology, about 80% of Americans say skincare is part of their regular health routine. This figure reveals that facial care purchases are now driven by health conviction rather than beauty aspiration — a structural shift that makes the category more recession-resistant and less seasonal.

According to Cosmetics Europe, around 62% of Europeans use facial skincare products at least once per day. Daily use at this scale means replenishment demand is predictable and recurring — creating stable revenue foundations for established brands and reliable volume forecasts for retail channel partners.

Key Takeaways

- The global Facial Care Market is valued at USD 125.3 Billion in 2025 and is forecast to reach USD 217.1 Billion by 2035.

- The market grows at a CAGR of 5.7% during the forecast period 2026 to 2035.

- By Product, Lotion Face, Creams & Moisturizers holds the dominant share at 36.8% in 2025.

- By End Use, Women lead the segment with a 76.2% share in 2025.

- By Distribution Channel, Supermarkets/Hypermarkets command the largest share at 34.80% in 2025.

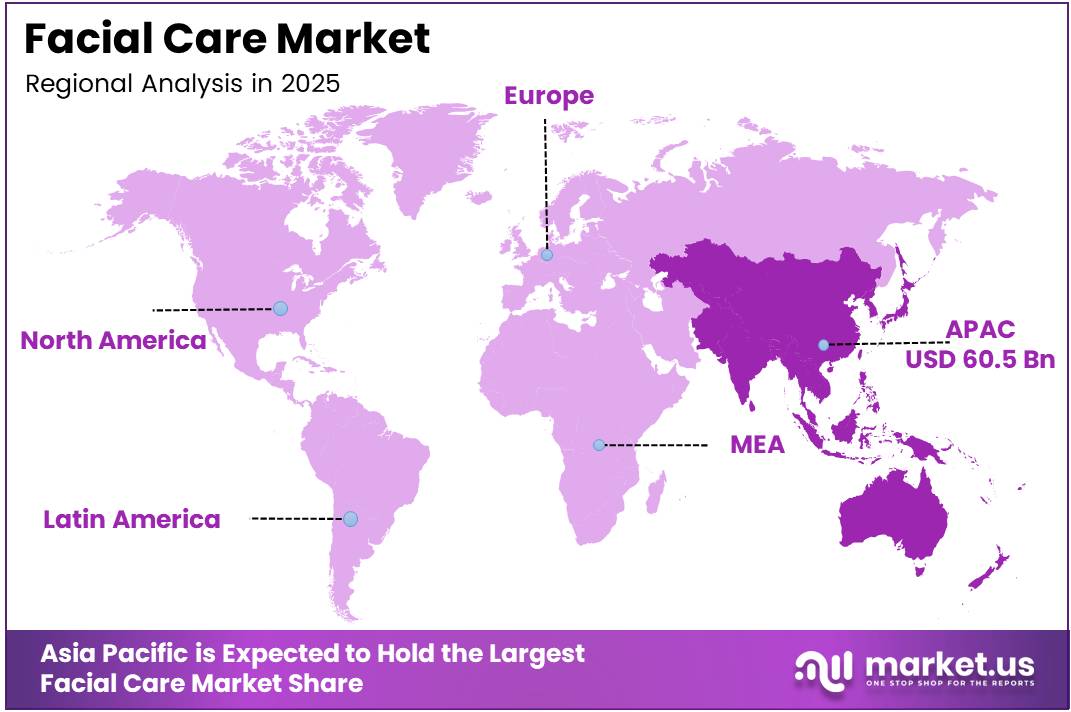

- Asia Pacific leads all regions with a 48.40% share, valued at USD 60.5 Billion in 2025.

Product Analysis

Lotion Face, Creams & Moisturizers dominates with 36.8% due to daily-use necessity across all demographics.

In 2025, Lotion Face, Creams & Moisturizers held a dominant market position in the By Product segment of the Facial Care Market, with a 36.8% share. This leadership reflects the subcategory’s role as the non-negotiable baseline of any facial routine. Consumers purchase moisturizers first and build their routine around them, making this the highest-velocity replenishment subcategory for retailers.

Cleansers & Face Wash serve as the entry point for new facial care consumers. Most first-time buyers enter the category through a basic cleanser before expanding to serums or treatments. This structural role means cleansers carry high trial volume and strong repeat purchase rates, giving brands a critical acquisition lever across both drugstore and online channels.

Facial Serums carry the highest average selling price per unit within the facial care category. Consumers associate serums with targeted, clinical-grade results — including anti-aging, brightening, and barrier repair. This perception supports premium pricing and drives trading-up behavior, particularly among millennials and Gen Z buyers who research ingredients before purchasing.

Face Sheet Masks differentiate through their ritual and sensory experience rather than daily utility. Their use tends to be weekly or occasion-driven, which limits replenishment velocity. However, they generate strong impulse and gifting purchases, making them a high-margin item for promotional display in both physical retail and e-commerce storefronts.

Sunscreen/Sun Care occupies a unique dual position — straddling skincare and health protection. Regulatory mandates around sun exposure awareness and increasing dermatologist recommendations for daily SPF use are expanding the everyday application base. However, only a minority of consumers currently apply sunscreen daily, indicating a large underpenetrated user base within an existing product-aware market.

Others in the product segment include eye creams, lip care, exfoliants, and facial oils. These subcategories serve consumers who have moved beyond basic routines and seek specialized solutions. Their growth signals increasing sophistication in buyer behavior and creates upsell opportunities for brands with broad product portfolios.

End Use Analysis

Women dominate with 76.2% due to higher routine complexity and product adoption rates.

In 2025, Women held a dominant market position in the By End Use segment of the Facial Care Market, with a 76.2% share. Women’s facial care routines involve more product steps and higher SKU diversity than men’s routines. This complexity creates greater wallet spend per consumer and higher lifetime value for brands that can retain female buyers across product categories.

Men represent the fastest-shifting demographic in the facial care category. Social normalization of male grooming, combined with targeted product lines addressing oiliness, shaving-related sensitivity, and aging, is expanding male participation. Brands that invest in dedicated men’s facial care lines now position themselves ahead of a buyer cohort that is entering the market with low brand loyalty and high switching potential.

Distribution Channel Analysis

Supermarkets/Hypermarkets dominate with 34.80% due to high foot traffic and broad product accessibility.

In 2025, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the Facial Care Market, with a 34.80% share. Their dominance reflects consumer preference for physically evaluating skincare products before purchase. High foot traffic, promotional shelf space, and cross-category visibility reinforce their role as the primary volume channel for mass-market facial care brands.

Convenience Stores serve time-constrained consumers seeking immediate replenishment. Their shelf mix skews toward single-use formats, travel sizes, and entry-level price points. While transaction values are lower, the frequency advantage makes convenience stores a reliable channel for brand visibility in densely populated urban areas.

Pharmacy & Drugstores carry the highest credibility signal in facial care distribution. Consumers trust pharmacist adjacency as an implicit endorsement of product efficacy and safety. This trust advantage benefits dermatologist-recommended brands and clinical skincare lines, allowing them to command premium shelf placement and higher per-unit margins in this channel.

Online channels enable the widest product discovery and price comparison for facial care buyers. Direct-to-consumer brands benefit most from this channel, bypassing retailer margins while building direct relationships with consumers. Ingredient-educated shoppers — particularly Gen Z — rely on online research and social proof before converting, making digital content strategy inseparable from online sales performance.

Others in distribution include specialty beauty retailers, department stores, and salon channels. These venues serve premium and prestige buyers who seek a curated, service-assisted purchase experience. For luxury facial care brands, these channels function as brand equity amplifiers rather than pure volume drivers.

Key Market Segments

By Product

- Lotion Face, Creams & Moisturizers

- Cleansers & Face Wash

- Facial Serums

- Face Sheet Masks

- Sunscreen/ Sun Care

- Others

By End Use

- Women

- Men

By Distribution Channel

- Supermarkets/ Hypermarkets

- Convenience Stores

- Pharmacy & Drugstore

- Online

- Others

Drivers

Social Media Influence and Preventive Skincare Awareness Drive Mass Adoption of Daily Facial Care Routines

Consumer behavior in facial care has shifted from reactive treatment to proactive daily maintenance. Skincare influencers and beauty content creators on digital platforms now function as de facto purchasing advisors for millions of consumers. This shift compresses the gap between product awareness and purchase decision — benefiting brands with strong content strategies.

According to TikTok platform data, skincare-related content has generated over 100 billion views on the hashtag #skincare. This scale of engagement confirms that consumer education is now occurring primarily through social channels rather than traditional advertising. Brands that invest in creator partnerships gain disproportionate reach at significantly lower cost per impression than broadcast media.

In February 2024, La Roche-Posay introduced the MelaB3 Serum targeting hyperpigmentation and uneven skin tone — a product directly aligned with the skin concern categories most frequently discussed in social skincare communities. This launch illustrates how dermatology brands translate social listening into product development, accelerating their relevance among digitally informed consumers.

Restraints

Skin Sensitivity Concerns and Counterfeit Products Undermine Consumer Trust and Limit Category Penetration

A growing number of consumers report adverse reactions to active ingredients such as retinol, AHAs, and niacinamide — ingredients that are now widespread in accessible facial care products. When buyers experience irritation, they retreat to simpler formulations or exit the category entirely. This creates a ceiling on how aggressively brands can formulate without risking consumer backlash.

According to the American Academy of Dermatology, only 12% of men and 29% of women apply sunscreen to their face daily. This low compliance, despite broad product availability, signals that sensitivity concerns and texture preferences actively suppress daily usage. For manufacturers, this underuse represents both a retention failure and a product reformulation imperative.

The proliferation of counterfeit and low-quality facial skincare products through online marketplaces compounds the problem. A single negative experience with a counterfeit product erodes trust not just in the fake brand but in the entire online channel. This forces legitimate brands to invest in authentication technology and channel policing — costs that are not revenue-generative but are competitively necessary.

Growth Factors

Personalized Skincare, Men’s Dedicated Lines, and Biotech Ingredients Open New Revenue Frontiers

AI-based skin analysis tools now allow brands to offer clinically tailored product recommendations at scale. This personalization layer shifts the purchase dynamic from mass-market browsing to prescribed regimen building. Consumers who receive personalized recommendations spend more per transaction and demonstrate higher repurchase rates — improving both revenue quality and customer retention metrics.

According to Cosmetics Europe, over 70% of European consumers say ingredient transparency influences their skincare purchasing decisions. This preference creates a direct commercial advantage for brands that invest in biotechnology-derived and lab-validated active ingredients. Consumers who understand what an ingredient does and why it works pay premiums willingly — making ingredient storytelling a genuine growth lever, not just a marketing tactic.

In February 2025, Amorepacific launched an upgraded Sulwhasoo First Care Activating Serum targeting global demand for premium herbal-based facial care products. This product advancement reflects how biotechnology-backed formulation and heritage ingredient platforms can coexist — and together unlock new consumer segments across both mature and emerging urban markets.

Emerging Trends

Skin Barrier Repair, Minimalist Routines, and At-Home Devices Redefine What Consumers Expect from Facial Care

The skin barrier repair trend has moved from dermatology clinics into mainstream retail. Consumers now actively seek products containing ceramides, prebiotics, and microbiome-supporting actives. This shift rewards brands that can credibly communicate barrier science over those relying solely on hydration marketing. It also opens new formulation territory previously occupied only by medical-grade products.

According to Google search trend insights, search interest for “skin care routine” increased more than 200% globally between 2020 and 2024. This search growth indicates that millions of consumers are actively building knowledge before they buy — meaning product discovery now happens before retail channel entry. Brands that own this informational moment through content and SEO convert passive researchers into buyers with notably higher intent.

At-home facial devices — including LED masks, microcurrent tools, and ultrasonic cleansing systems — are pulling professional clinic treatments into the domestic routine. Consumers willing to invest in devices also invest in companion product regimens, creating a hardware-software revenue model for facial care brands. This trend compresses the perceived gap between clinical-grade and consumer-grade skincare outcomes.

Regional Analysis

Asia Pacific Dominates the Facial Care Market with a Market Share of 48.40%, Valued at USD 60.5 Billion

Asia Pacific leads the global facial care market with a 48.40% share, valued at USD 60.5 Billion in 2025. This leadership reflects deeply embedded multi-step skincare rituals in South Korea, Japan, and China — markets where facial care spending per capita significantly exceeds global averages. The region also incubates product formats and ingredient trends that later diffuse globally, giving it an innovation advantage alongside its volume scale.

North America Facial Care Market Trends

North America represents a mature but continuously premiumizing market. Consumers increasingly shift from mass-market brands toward dermatologist-endorsed and clinical skincare lines. Strong e-commerce infrastructure and high digital engagement mean that North American brands scale new product launches faster than most other regions, supporting rapid revenue concentration among winning SKUs.

Europe Facial Care Market Trends

Europe benefits from strict cosmetic regulatory standards under the EU Cosmetics Regulation, which functions as a de facto quality signal for consumers. Ingredient scrutiny is higher here than in any other region. Brands that achieve compliance and clearly communicate ingredient provenance command premium shelf positions, particularly in Germany, France, and the UK where ingredient-literate consumers are most concentrated.

Latin America Facial Care Market Trends

Latin America shows strong urbanization-led demand for facial skincare products across Brazil and Mexico. Rising disposable incomes in secondary cities are pulling new consumer cohorts into the market for the first time. Value-positioned premium products — offering clinical positioning at accessible price points — find the strongest commercial traction in this channel context.

Middle East and Africa Facial Care Market Trends

The Middle East and Africa region presents a bifurcated opportunity: GCC consumers lean toward prestige and luxury facial care brands, while sub-Saharan Africa remains largely underpenetrated at the mass market level. Both segments are growing, but through different channels — specialty retail and e-commerce in the Gulf, and expanding modern trade in key African urban centers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Coty Inc. positions itself at the intersection of mass and prestige facial care, with a portfolio designed to capture consumer trading-up behavior. Its strategic strength lies in brand licensing and acquisition, allowing rapid entry into high-growth skincare segments without full R&D build-out. However, managing brand equity across a wide price range remains an ongoing tension in its facial care growth agenda.

Estée Lauder Companies Inc. operates the most visible prestige facial care portfolio in the global market. Its multi-brand architecture — spanning clinical, luxury, and dermatological positioning — allows it to capture consumer spending across every price tier simultaneously. The April 2024 expansion of its Re-Nutriv luxury line confirms its continued commitment to the ultra-premium facial treatment segment, where margins are highest and price sensitivity is lowest.

Johnson & Johnson Services, Inc. applies clinical heritage and consumer health credibility to its facial skincare positioning. Its dermatology-backed brand identity gives it a structural trust advantage in pharmacy and healthcare retail channels. This credibility is difficult for beauty-only brands to replicate — positioning J&J to capture consumers who treat facial care as a health decision rather than a cosmetic purchase.

L’Oréal leads the global facial care market through its breadth of distribution, formulation capability, and acquisition strategy. Its March 2024 acquisition of a 10% stake in Galderma following its IPO signals a deliberate push into prescription-adjacent dermatological skincare — a move that extends its addressable market well beyond over-the-counter facial care and into clinician-recommended treatment territory.

Key Players

- Coty Inc.

- ESTEE LAUDER COMPANIES INC.

- Johnson & Johnson Services, Inc.

- L’Oréal

- Oriflame Cosmetics AG

- Procter and Gamble

- Revlon

- Shiseido Company

- The Avon Company

- Unilever

Recent Developments

- January 2024 – Shiseido launched the new Ultimune Power Infusing Serum globally, featuring an upgraded skin-defense formula designed for anti-aging facial care. This product launch reinforced Shiseido’s positioning in the premium facial serum segment and addressed the growing consumer priority around long-term skin resilience.

- March 2024 – L’Oréal acquired a 10% stake in Galderma following its IPO to strengthen its position in dermatology-based skincare and facial treatment solutions. This strategic investment extends L’Oréal’s reach into clinician-recommended facial care, a segment commanding higher price points and lower price sensitivity than mainstream retail channels.

- May 2025 – e.l.f. Beauty announced the acquisition of Rhode to strengthen its presence in the fast-growing celebrity-driven facial skincare segment. This move signals e.l.f.’s intent to compete in premium facial care beyond its value-positioned core, accessing a younger, digitally native consumer base with high brand affinity for Rhode.

- March 2025 – Procter & Gamble expanded its facial skincare portfolio through new Olay Super Serum product launches focused on multi-benefit anti-aging skincare. These launches target the multi-functional product trend directly, allowing Olay to address the minimalist routine consumer who demands clinical results from a single SKU.

Report Scope

Report Features Description Market Value (2025) USD 125.3 Billion Forecast Revenue (2035) USD 217.1 Billion CAGR (2026-2035) 5.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Lotion Face, Creams & Moisturizers, Cleansers & Face Wash, Facial Serums, Face Sheet Masks, Sunscreen/Sun Care, Others), By End Use (Women, Men), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Pharmacy & Drugstore, Online, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Coty Inc., ESTEE LAUDER COMPANIES INC., Johnson & Johnson Services, Inc., L’Oréal, Oriflame Cosmetics AG, Procter and Gamble, Revlon, Shiseido Company, The Avon Company, Unilever Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Coty Inc.

- ESTEE LAUDER COMPANIES INC.

- Johnson & Johnson Services, Inc.

- L'Oréal

- Oriflame Cosmetics AG

- Procter and Gamble

- Revlon

- Shiseido Company

- The Avon Company

- Unilever

Our Clients

- 180141

- Mar 2026