Quick Navigation

Report Overview

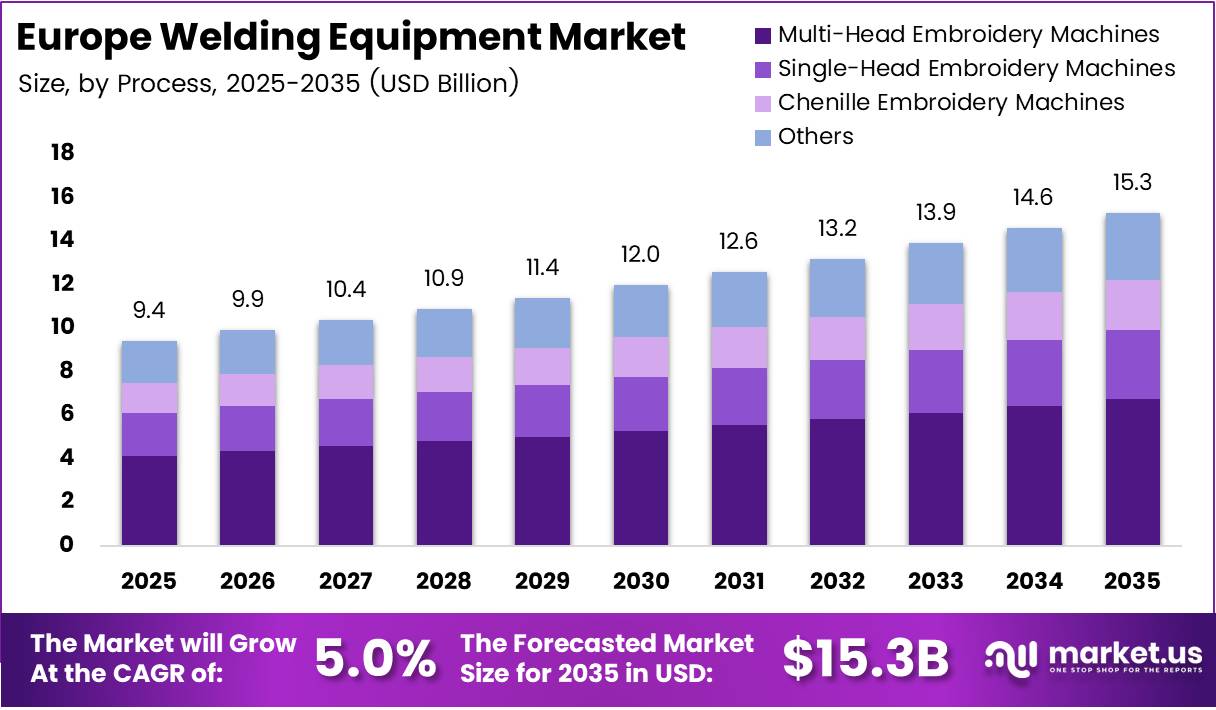

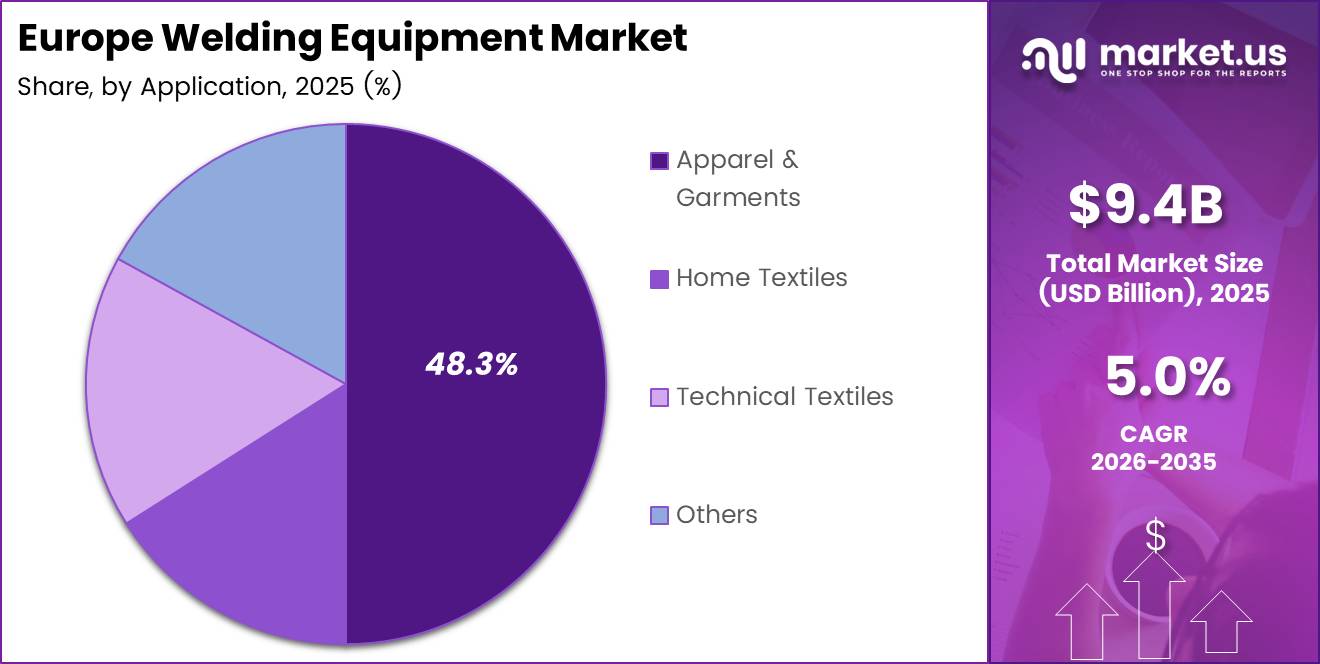

Europe Welding Equipment Market size is expected to be worth around USD 15.3 Billion by 2035 from USD 9.4 Billion in 2025, growing at a CAGR of 5.0% during the forecast period 2026 to 2035.

Europe’s welding equipment sector sits at the intersection of industrial modernization and energy transition. Infrastructure upgrades across transportation networks, offshore wind installations, and electric vehicle production lines all require precision metal joining at scale. This convergence of demand sources gives the market structural depth that single-sector markets rarely achieve.

Robotic and automated welding systems now represent the fastest-expanding product category across European manufacturing facilities. Manufacturers replacing aging manual setups with automated cells are not simply cutting labor costs. They are repositioning their quality standards, reducing rework rates, and qualifying for higher-value contracts in aerospace, automotive, and energy sectors.

The electric vehicle transition directly reshapes welding technology requirements across European production plants. Battery enclosures, lightweight aluminum frames, and structural components demand welding processes that deliver precision at high throughput. Welding equipment suppliers targeting EV-focused facilities face a buyer segment that prioritizes accuracy and repeatability over unit price.

Renewable energy infrastructure, particularly offshore wind, creates a distinct high-volume demand segment for heavy-duty welding systems. Offshore wind tower fabrication requires large-format, high-amperage equipment built for continuous operation. European governments have committed to substantial wind capacity additions through 2030, which translates into a defined pipeline for welding system procurement over the next several years.

Smart factory investments across Germany, France, and Scandinavia are accelerating adoption of IoT-enabled welding equipment. Connected welding cells provide real-time quality monitoring, remote diagnostics, and predictive maintenance data. Facilities that deploy these systems reduce unplanned downtime and generate compliance documentation automatically, which matters particularly under European workplace safety regulations.

According to a University of North Dakota PhD dissertation published in January 2025, cobotic weldments proved 13.5% to 37% stronger than manual welds across tested parts and configurations. This performance gap signals a structural shift in buyer expectations. Procurement teams at tier-one automotive and aerospace suppliers now treat weld strength consistency as a specification requirement, not a variable outcome.

According to EVS International’s 2026 technical guide, robotic welding systems achieved defect rates below 1% compared to typical 5% to 8% for manual operations in calibrated industrial applications. A defect rate gap of this magnitude represents a compelling total cost of ownership argument. For high-value fabrication where rework or rejection costs are substantial, this data point drives capital investment decisions faster than any list-price comparison.

Key Takeaways

- The Europe Welding Equipment Market was valued at USD 9.4 Billion in 2025 and is forecast to reach USD 15.3 Billion by 2035.

- The market advances at a CAGR of 5.0% during the 2026 to 2035 forecast period.

- By Process, Multi-Head Embroidery Machines held the dominant share at 38.5% in 2025.

- By Automation Level, Automatic and Robotic systems led with 58.1% share in 2025.

- By Application, Apparel and Garments captured 48.3% of total market share in 2025.

- By End-User, Industrial Use accounted for 45.9% of market share in 2025.

- North America leads regional market positioning, supported by large-scale infrastructure and manufacturing investment.

- Robotic welding defect rates fall below 1%, compared to 5% to 8% for manual welding operations.

- Cobotic welding systems deliver weld strength improvements of 13.5% to 37% over manual processes.

Process Analysis

Multi-Head Embroidery Machines dominate with 38.5% due to high-volume parallel processing capability.

In 2025, Multi-Head Embroidery Machines held a dominant market position in the By Process segment of the Europe Welding Equipment Market, with a 38.5% share. Their throughput advantage over single-head configurations makes them the default choice for industrial-scale operations where cycle time directly affects unit economics. Buyers at volume-sensitive facilities treat multi-head capability as a baseline specification.

Single-Head Embroidery Machines serve a distinct buyer profile focused on flexibility and smaller production runs. These systems attract commercial workshops and small manufacturers that prioritize quick job changeovers over maximum throughput. However, as production volumes rise and labor costs tighten, many single-head operators are evaluating the economics of upgrading to multi-head configurations.

Chenille Embroidery Machines address a specialized segment requiring textured, loop-based output that standard flat embroidery cannot replicate. Their application base is narrower but the switching cost is high, which creates a stable installed base. Vendors targeting this niche compete on machine reliability and consumable compatibility rather than headline speed specifications.

Others in the process segment capture emerging and hybrid configurations that serve application-specific needs. This sub-segment reflects ongoing process innovation where vendors test new configurations before they achieve sufficient volume for standalone categorization. Early adopters in technical textiles and specialty apparel drive most of the procurement activity here.

Automation Level Analysis

Automatic/Robotic systems dominate with 58.1% due to superior output consistency and reduced labor dependency.

In 2025, Automatic and Robotic systems held a dominant market position in the By Automation Level segment of the Europe Welding Equipment Market, with a 58.1% share. European manufacturers facing labor shortages and rising wage floors have accelerated capital investment in automated systems. The majority share reflects a structural shift, not a temporary purchasing trend, and positions automated equipment vendors as primary beneficiaries of ongoing factory modernization budgets.

Manual systems retain relevance in applications where setup complexity, job variety, or low volume make automation economically impractical. Skilled operators using manual equipment still command premium positioning in bespoke fabrication and repair contexts. However, the addressable base for manual-only procurement is contracting as hybrid options become more accessible to smaller operators.

Semi-automatic systems occupy the middle ground between operator skill and machine consistency. These configurations appeal to mid-size manufacturers transitioning away from fully manual workflows without committing to full robotic integration. The segment benefits from cost-sensitive buyers who require quality improvements but face capital constraints on fully automated cells.

Application Analysis

Apparel and Garments dominate with 48.3% due to consistent high-volume production demand across European facilities.

In 2025, Apparel and Garments held a dominant market position in the By Application segment of the Europe Welding Equipment Market, with a 48.3% share. This application segment drives equipment purchase volumes more than any other vertical. Buyers in this space prioritize speed, repeatability, and low consumable cost, which shapes the product specifications that vendors must meet to remain competitive at the core of the market.

Home Textiles represent a stable but slower-growth application segment. Production facilities serving this vertical tend to run longer job cycles with fewer configuration changes. Equipment durability and low maintenance requirements rank higher in purchase decisions than raw throughput speed. This buyer behavior creates an opportunity for vendors offering service-bundled equipment contracts.

Technical Textiles present the highest growth potential within the application breakdown. Defense, automotive, and medical sectors increasingly source technical textile components from European manufacturers. These buyers require equipment that can handle engineered fabrics and precision placement tolerances that standard apparel machines cannot deliver reliably.

Others in the application segment include niche verticals such as promotional products, footwear, and industrial labeling. While individually small, these applications collectively generate consistent replacement and upgrade demand. Vendors with broad application support capabilities convert these buyers into long-term service and consumables customers.

End-User Analysis

Industrial Use dominates with 45.9% due to large facility scale and continuous production requirements.

In 2025, Industrial Use held a dominant market position in the By End-User segment of the Europe Welding Equipment Market, with a 45.9% share. Large manufacturing facilities operate multi-shift production schedules where equipment downtime translates directly into contract penalties. This operational reality makes industrial buyers the most predictable and highest-value customer segment for both capital equipment and aftermarket services.

Home and Personal Use represents the smallest share of the end-user breakdown but contributes to market resilience through distributed purchasing. Individual buyers are price-sensitive and brand-aware. Vendors that build strong retail and online channel presence convert this segment into a consistent volume base that partially offsets cyclicality in industrial procurement.

Commercial and Small Business Use is the segment most sensitive to economic conditions and financing availability. Small embroidery shops and custom print operations make capital purchase decisions based on order backlog visibility. When their client pipelines are strong, this segment generates meaningful equipment replacement and upgrade demand. Vendors with flexible financing programs hold a structural advantage here.

Key Market Segments

By Process

- Multi-Head Embroidery Machines

- Single-Head Embroidery Machines

- Chenille Embroidery Machines

- Others

By Automation Level

- Automatic / Robotic

- Manual

- Semi-automatic

By Application

- Apparel & Garments

- Home Textiles

- Technical Textiles

- Others

By End-User

- Industrial Use

- Home/Personal Use

- Commercial/Small Business Use

- Others

Drivers

Infrastructure Modernization and Industrial Automation Fuel Sustained Equipment Investment Across Europe

European governments and private operators are committing capital to transportation networks, energy grids, and manufacturing facilities at a pace that sustains multi-year welding equipment procurement cycles. Rail upgrades, port expansions, and bridge rehabilitation projects each require certified welding work at volume. This public infrastructure pipeline provides a demand floor that insulates the market from short-cycle industrial downturns.

Industrial automation adoption is not a future ambition across European manufacturing. It is a current capital deployment priority. Automotive, aerospace, and heavy engineering facilities are replacing manual welding stations with robotic cells to address labor shortages, meet quality certification requirements, and reduce variable cost exposure. In September 2025, Fronius International launched the Fortis series for manual MIG/MAG welding, targeting small and medium-sized metalworking companies with enhanced connectivity features, which signals that automation-enabling connectivity is now a specification baseline even at the entry-level segment.

According to a February 2025 ScienceDirect study, a dual-driven physics and data model for autonomous welding parameter optimization achieved 88.81% accuracy, representing a 7.42% improvement over physical models alone, with a 66.6% enhancement in weld stability. This level of process control accuracy justifies the capital cost of advanced welding systems. Procurement teams at tier-one manufacturers are now benchmarking against these performance standards when evaluating new equipment purchases.

Restraints

Regulatory Compliance Costs and Rising Energy Prices Compress Margins for Welding Equipment Operators

European environmental and workplace safety regulations impose material compliance costs on welding equipment manufacturers and end-users alike. Fume extraction requirements, noise limits, and emissions standards require facility upgrades that can equal or exceed the cost of the welding equipment itself. Smaller fabrication shops face disproportionate compliance burdens because they cannot spread these fixed costs across large production volumes.

Energy prices across Europe have structurally reset at levels that make operational cost a decisive factor in equipment selection. High-amperage welding processes consume significant electrical power per operating hour. A facility running multiple welding stations across two or three shifts faces energy bills that directly erode production margins. This pressure shifts buyer preference toward inverter-based and energy-optimized systems, but the transition requires upfront capital that not all operators can commit.

According to a 2025 Springer study, a four-wheeled linear welding robot reduced welding time by approximately 40% compared to manual welding. This efficiency gain illustrates why compliance costs create an uneven market. Operators who can afford automation capture both the regulatory compliance benefits and the productivity gains. Those who cannot afford to automate face rising compliance costs without the offsetting efficiency advantages, which creates a two-tier competitive dynamic within the European fabrication sector.

Growth Factors

Laser Welding Adoption and Offshore Wind Expansion Create High-Value Revenue Streams for Equipment Suppliers

Aerospace and high-precision manufacturing applications are shifting from conventional arc welding to laser-based processes that deliver narrower heat-affected zones and superior dimensional accuracy. Laser welding systems command significantly higher unit prices and generate recurring revenue through optics maintenance and process consumables. Vendors with established aerospace and defense sales channels are positioned to capture this upgrade cycle before generalist competitors build application-specific expertise.

Offshore wind project pipelines across the North Sea, Baltic, and Mediterranean corridors require specialized heavy-duty welding systems built for continuous outdoor operation in corrosive marine environments. Tower fabrication, monopile production, and subsea structure assembly each demand equipment that standard industrial welding cells cannot reliably support. According to the Emerging Technologies Institute’s December 2025 report, Italian shipbuilder Fincantieri achieved a 60% reduction in power consumption and a 90% reduction in welding consumables through robotic laser welding adoption. This data point demonstrates the total cost of ownership case that offshore contractors are evaluating when specifying new equipment.

According to a University of North Dakota PhD dissertation published in January 2025, cobotic welding in high-mix low-volume manufacturing environments reduced energy consumption by 41% to 71% in single-sided applications compared to manual welding, alongside a 39% reduction in cycle time. Smart factory programs across Germany, France, and Scandinavia are funding connected welding equipment installations as part of broader IoT infrastructure investments. Equipment that integrates with factory management systems generates data streams that create ongoing service relationships between vendors and customers, converting one-time capital sales into multi-year engagement contracts.

Emerging Trends

AI-Powered Monitoring, Energy Efficiency Standards, and AR Training Are Redefining Welding Equipment Specifications

Artificial intelligence integration in welding quality monitoring is moving from pilot projects to standard procurement specifications at large European manufacturers. AI systems that detect weld anomalies in real time and trigger parameter corrections reduce scrap rates and eliminate the need for post-weld inspection on every joint. Vendors that embed AI monitoring natively into their equipment platforms hold a meaningful competitive advantage over those offering it as an optional add-on.

Energy-efficient inverter-based welding equipment is transitioning from a premium option to a baseline requirement across European industrial facilities. Regulatory pressure on facility-level energy consumption, combined with high electricity costs, means procurement teams now include energy consumption data in equipment comparisons as a standard input. According to Fronius International’s September 2025 product launch, the Fortis Duo and Fortis XT variants deliver energy savings of up to 16% for industrial welding operations. This positions energy performance as a commercial selling point rather than an incidental specification detail.

Augmented reality welding training simulators are entering workforce development programs at European vocational training centers and large manufacturers. These systems reduce training costs, eliminate consumable waste during skill development, and allow trainees to practice on simulated versions of high-value materials before touching real production work. Collaborative welding robots that work alongside human operators in flexible manufacturing cells are extending the productivity case for automation into lower-volume, higher-variety production environments where full automation has historically been difficult to justify.

Key Company Insights

Lincoln Electric Holdings Inc. positions itself as the broadest-capability welding solutions provider in the European market. Its product range spans manual, semi-automatic, and fully automated systems, which allows it to serve both small fabricators and tier-one industrial manufacturers from a single vendor relationship. This breadth is a commercial advantage in large-account procurement where consolidation of suppliers is a buyer priority. However, breadth also requires sustained R&D investment to remain competitive across all categories simultaneously.

ESAB Corp. strengthened its European automation footprint through the acquisition of EWM GmbH in June 2025. This move adds specialized European-engineered welding automation capability to ESAB’s existing portfolio. The acquisition signals a strategic bet that industrial automation demand in Europe will sustain premium pricing for specialist systems. Integration execution will determine whether ESAB can convert EWM’s customer relationships into long-term platform sales rather than one-time equipment transactions.

Fronius International GmbH builds its competitive positioning around energy efficiency and connectivity. The September 2025 launch of the Fortis series with worldwide voltage compatibility and up to 16% energy savings demonstrates a product strategy aligned directly with European regulatory and cost pressures. Fronius targets small and medium metalworking companies with this line, a segment that competitors often underserve with overly complex or expensive configurations. This positioning creates a loyal mid-market installed base that generates recurring service and consumables revenue.

Kemppi Oy concentrates its market position on digital welding management and connected equipment platforms. Its software-enabled approach allows fabricators to manage weld quality data, operator performance, and compliance documentation from a centralized system. This creates switching costs that are difficult for competitors to overcome purely on hardware specifications or price. As European manufacturers face tighter quality audit requirements, Kemppi’s data-driven positioning becomes more valuable with each compliance cycle.

Key Players

- Lincoln Electric Holdings Inc.

- ESAB Corp.

- Fronius International GmbH

- Kemppi Oy

- voestalpine Böhler Welding

- Carl Cloos Schweißtechnik GmbH

- AMADA WELD TECH

- EWM AG

- Hobart Welders

- J Denyo Co. Ltd

Recent Developments

- June 2025 – ESAB Corporation announced the acquisition of EWM GmbH, strengthening its welding automation and industrial equipment capabilities across European markets. This deal directly expands ESAB’s footprint in precision and high-amperage welding segments.

- September 2025 – Fronius International introduced the Fortis Duo and Fortis XT variants featuring dual wire spool capability, worldwide voltage compatibility, and energy savings of up to 16% for industrial welding operations. These variants target facilities requiring flexible, energy-efficient welding configurations across multi-shift production schedules.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 9.4 Billion |

| Forecast Revenue (2035) | USD 15.3 Billion |

| CAGR (2026-2035) | 5.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Process (Multi-Head Embroidery Machines, Single-Head Embroidery Machines, Chenille Embroidery Machines, Others), By Automation Level (Automatic/Robotic, Manual, Semi-automatic), By Application (Apparel & Garments, Home Textiles, Technical Textiles, Others), By End-User (Industrial Use, Home/Personal Use, Commercial/Small Business Use, Others) |

| Competitive Landscape | Lincoln Electric Holdings Inc., ESAB Corp., Fronius International GmbH, Kemppi Oy, voestalpine Böhler Welding, Carl Cloos Schweißtechnik GmbH, AMADA WELD TECH, EWM AG, Hobart Welders, J Denyo Co. Ltd |

| Customization Scope | Customization for segments will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |