Quick Navigation

Report Overview

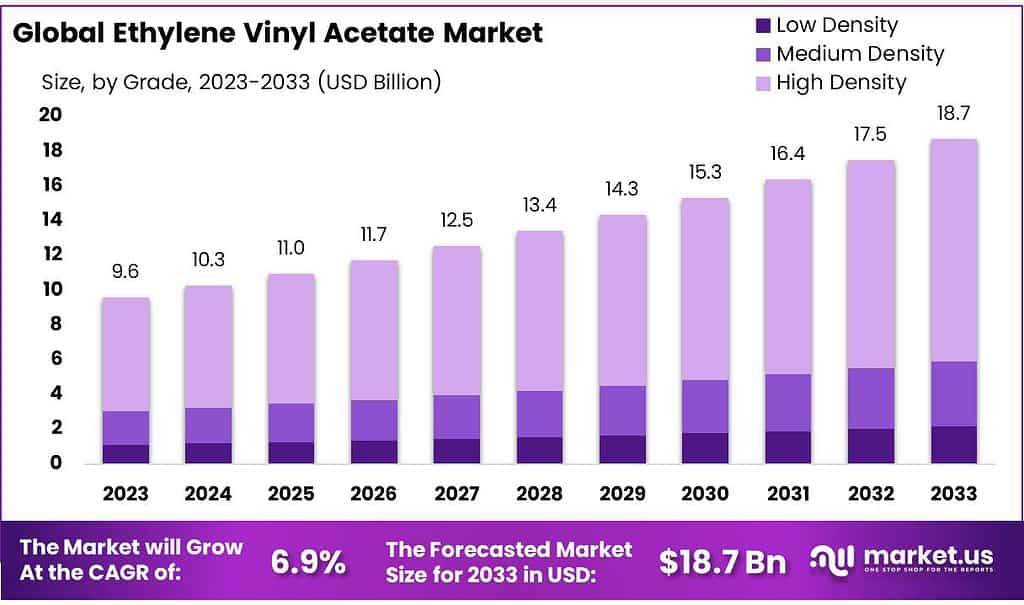

The global Ethylene Vinyl Acetate Market size is expected to be worth around USD 18.7 billion by 2033, from USD 9.6 billion in 2023, growing at a CAGR of 6.9% during the forecast period from 2023 to 2033.

Ethylene Vinyl Acetate (EVA) is a highly versatile type of plastic known for its exceptional clarity, flexibility, and resistance to UV radiation. EVA’s unique properties make it a favored choice for a broad range of applications, from flexible packaging films and foams to hot melt adhesives and solar panel encapsulation. Its ability to be processed like other thermoplastics, combined with its superior flexibility and resilience, allows it to serve varied industries including sports equipment, automotive, and healthcare.

The global demand for EVA is significantly influenced by government incentives aimed at promoting renewable energy sources. These incentives have particularly boosted the use of EVA in the solar industry, as it plays a critical role in the production of photovoltaic panels, especially in key markets like the Asia-Pacific region. This region stands out as a significant player in the global photovoltaic market due to strong governmental support and substantial market demand.

To keep up with the increasing global demand, major chemical companies are continually expanding their production capacities. In strategic regions such as North America and Asia, these expansions are not just about increasing volume but also about enhancing the supply chain and market reach.

The EVA market is also characterized by vigorous merger and acquisition activities, partnerships, and innovations aimed at refining product offerings and penetrating new market areas. These strategic activities are particularly focused on catering to high-growth sectors like solar energy and high-performance packaging solutions, where EVA’s unique properties can be leveraged to meet specific industrial needs.

Additionally, the import-export dynamics of EVA are heavily dictated by the production capabilities and industrial demands of major regions like North America, and Asia-Pacific, particularly the U.S., China, and India. These countries are crucial in the global EVA trade, owing to their extensive production capacities and substantial domestic demands that influence global supply chains.

Key Takeaways

- The global Ethylene Vinyl Acetate (EVA) market is projected to grow from USD 9.6 billion in 2023 to USD 18.7 billion by 2033, at a CAGR of 6.9%.

- High-density EVA held a dominant 68.5% market share in 2023, valued for its strength and thermal resistance, ideal for automotive and industrial applications.

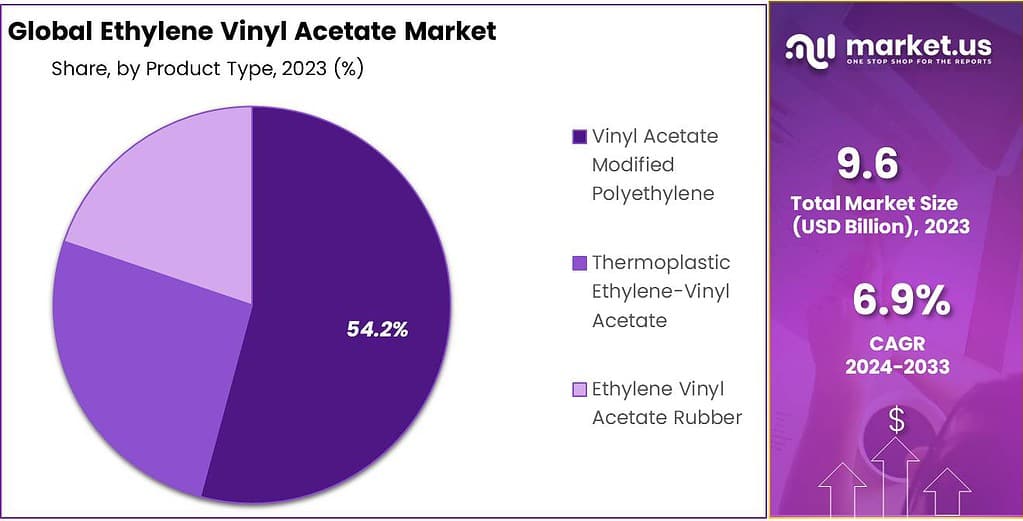

- Vinyl Acetate Modified Polyethylene dominated with a 54.2% market share in 2023, preferred for its clarity and flexibility.

- Photovoltaic Cells led with a 31.6% share in 2023, essential for solar panel encapsulation.

- Packaging held a 41.6% share in 2023, driven by demand in the food, beverage, and personal care industries.

- Asia Pacific: Dominates the market with a 45.4% share, driven by rapid industrialization and economic growth.

By Grade

In 2023, High-Density Ethylene Vinyl Acetate (EVA) held a dominant market position, capturing more than a 68.5% share. This grade of EVA is favored for its superior strength and thermal resistance, making it ideal for applications requiring robust, durable materials, such as in the automotive and industrial sectors. High Density EVA’s significant market share is also bolstered by its use in photovoltaic panels where its properties ensure longevity and protection against environmental factors.

Medium Density EVA, while holding a smaller market share, is recognized for its balanced properties between flexibility and strength. It serves well in the footwear and sports equipment industries, where both comfort and performance are key.

Low-Density EVA is appreciated for its excellent flexibility and clarity, which makes it a popular choice in consumer goods and packaging. This type of EVA is particularly used in applications that require soft, flexible plastic films and is critical in the packaging of perishable goods, providing not only physical protection but also clarity for aesthetic appeal.

By Product Type

In 2023, Vinyl Acetate Modified Polyethylene held a dominant market position, capturing more than a 54.2% share. This product type is highly valued for its enhanced properties, including better clarity and flexibility compared to standard polyethylene. These characteristics make it particularly suitable for packaging applications that require a clear view of the contents and flexible handling, such as food packaging and consumer goods.

Thermoplastic Ethylene-Vinyl Acetate follows, recognized for its versatility and ease of use in molding and extrusion processes. This type of EVA is extensively utilized in both the consumer and industrial sectors for products like toys, gaskets, and hoses, where flexibility and impact resistance are crucial.

Ethylene Vinyl Acetate Rubber, while holding a smaller segment of the market, is indispensable for its application in automotive and consumer electronics. It is favored for its excellent barrier properties and resistance to stress-cracking, key factors in applications that demand durability and performance under stress, such as seals and insulation in electronics.

By Application

In 2023, Photovoltaic Cells held a dominant market position in the Ethylene Vinyl Acetate (EVA) market, capturing more than a 31.6% share. This significant market share reflects the critical role of EVA as an encapsulant in solar panels, enhancing their efficiency and durability by protecting sensitive photovoltaic cells from environmental factors.

Following closely, EVA applications in Film also constitute a major segment, utilized extensively for its flexibility and barrier properties in packaging films and laminates. This application benefits sectors requiring durable and protective film solutions, including food packaging and industrial materials.

EVA Foam represents another key application, favored for its cushioning properties, which are essential in sports equipment, footwear, and automotive interiors. The versatility and comfort provided by EVA foam contribute significantly to its demand across these diverse industries.

Hot Melt Adhesives, incorporating EVA, are renowned for their strong bonding capabilities without the need for solvents. This application is pivotal in packaging, woodworking, and electronics manufacturing, where quick setting and robust adhesive properties are required.

By End-Use

In 2023, Packaging held a dominant market position, capturing more than a 41.6% share of the Ethylene Vinyl Acetate (EVA) market. This segment’s growth is primarily driven by the rising demand for flexible packaging solutions in the food, beverage, and personal care industries. EVA’s properties, such as flexibility, clarity, and durability, make it a preferred material for packaging applications.

The Building & Construction segment is another significant end-use category for EVA, accounting for a substantial share of the market. EVA is widely used in construction materials, such as roofing sheets, flooring, and sealants, due to its flexibility, durability, and resistance to environmental factors.

The ongoing infrastructure development in developing regions, such as Asia-Pacific and the Middle East, is expected to drive the demand for EVA in construction applications. Government initiatives and investments in large-scale infrastructure projects are key factors contributing to this growth.

In the Electronics sector, EVA finds extensive use in encapsulating photovoltaic cells in solar panels, which is a critical application given the global shift towards renewable energy. The growing adoption of solar energy, supported by government incentives and environmental policies, has led to an increased demand for EVA in the photovoltaic industry. This segment is poised for significant growth as countries around the world continue to invest in expanding their solar energy capacities.

The Automotive segment utilizes EVA in various applications, including interior trims, soundproofing, and sealing. The increasing production of automobiles globally, along with the rising demand for lightweight and fuel-efficient vehicles, drives the demand for EVA. Its use in manufacturing vehicle components helps reduce overall vehicle weight and enhances fuel efficiency, which is crucial in meeting stringent environmental regulations.

Key Market Segments

By Grade

- Low Density

- Medium Density

- High Density

By Product Type

- Vinyl Acetate Modified Polyethylene

- Thermoplastic Ethylene-Vinyl Acetate

- Ethylene Vinyl Acetate Rubber

By Application

- Film

- Foam

- Hot Melt Adhesives

- Photovoltaic Cells

- Others

By End-Use

- Footwear

- Packaging

- Agriculture

- Photovoltaic Panels

- Pharmaceuticals

- Other

Drivers

Rising Demand in the Solar Energy Sector

The growing adoption of solar energy is a significant driving factor for the ethylene vinyl acetate (EVA) market. The shift towards renewable energy sources has been spurred by global environmental concerns and government initiatives aimed at reducing carbon emissions. EVA is a crucial material used in the encapsulation of photovoltaic (PV) cells in solar panels due to its excellent adhesive and durable properties.

According to the International Energy Agency (IEA), global solar PV capacity additions are expected to reach 1,000 gigawatts (GW) by 2030, more than tripling from the 2020 level of 260 GW. This rapid expansion is driven by decreasing costs of solar technologies and supportive government policies. For example, the European Union has set a target to install over 320 GW of solar power by 2030 as part of its Green Deal.

In the United States, the Department of Energy (DOE) has implemented the Solar Energy Technologies Office (SETO) program, which aims to reduce the cost of solar energy by 50% between 2020 and 2030. The DOE’s initiative is expected to boost the deployment of solar technologies, further increasing the demand for EVA in solar panel manufacturing.

China, the largest market for solar PV, continues to lead the way with significant investments and policies favoring renewable energy. According to the National Energy Administration (NEA) of China, the country aims to achieve 1,200 GW of solar and wind capacity by 2030. In 2023 alone, China added approximately 48.2 GW of solar PV capacity, which represents a substantial market for EVA used in solar panel production.

India is also emerging as a key player in the solar energy market, with ambitious targets under the National Solar Mission to achieve 100 GW of solar capacity by 2022 and 450 GW by 2030. Government initiatives, such as subsidies and incentives for solar power installations, are expected to drive significant growth in the EVA market as demand for solar panels increases.

The Middle East and Africa region is witnessing rapid adoption of solar energy as well, driven by abundant sunlight and the need for sustainable energy solutions. Countries like Saudi Arabia and the United Arab Emirates are investing heavily in solar projects. Saudi Arabia’s Vision 2030 includes plans to generate 50% of its electricity from renewable sources, with solar energy playing a central role.

Restraints

Volatility in Raw Material Prices

A major restraining factor for the ethylene vinyl acetate (EVA) market is the volatility in raw material prices. EVA is produced from ethylene and vinyl acetate monomers, which are derived from petroleum and natural gas. The prices of these raw materials are highly susceptible to fluctuations in crude oil prices, geopolitical tensions, and supply chain disruptions.

According to the U.S. Energy Information Administration (EIA), crude oil prices have seen significant fluctuations over the past decade, with prices ranging from as low as $20 per barrel in early 2020 due to the COVID-19 pandemic, to over $80 per barrel in 2022 due to supply chain disruptions and geopolitical issues. These fluctuations directly impact the cost of producing ethylene and vinyl acetate, thereby affecting the overall cost of EVA production.

The International Energy Agency (IEA) highlights that geopolitical tensions, such as those seen in major oil-producing regions like the Middle East, can lead to sudden spikes in crude oil prices. For instance, conflicts and production cuts in countries like Saudi Arabia and Iran can disrupt the global supply of crude oil, leading to price increases. This uncertainty in raw material costs poses a significant challenge for EVA manufacturers, as it can erode profit margins and create instability in pricing strategies.

Furthermore, the availability of raw materials is another concern. Natural disasters, such as hurricanes in the Gulf of Mexico, can disrupt the supply of natural gas and crude oil, leading to shortages and price hikes. For example, Hurricane Harvey in 2017 caused significant disruptions to the petrochemical industry in the United States, leading to a sharp increase in the prices of ethylene and other petrochemical products.

Government regulations and environmental policies also play a role in the volatility of raw material prices. For instance, stricter environmental regulations on the extraction and production of petroleum and natural gas can increase operational costs for raw material suppliers. The European Union’s Emissions Trading System (ETS) is one such regulatory framework that aims to reduce greenhouse gas emissions by imposing costs on carbon emissions. This can lead to increased costs for petrochemical companies, which in turn affects the pricing of ethylene and vinyl acetate.

Additionally, the global push towards renewable energy and reducing reliance on fossil fuels could lead to decreased investment in oil and gas exploration and production. This reduction in investment may result in lower availability of petroleum-based raw materials in the future, thereby impacting the supply and cost stability of ethylene and vinyl acetate.

Opportunity

Expansion in the Solar Energy Sector

The expansion of the solar energy sector represents a significant growth opportunity for the Ethylene Vinyl Acetate (EVA) market. EVA is a crucial material used in the encapsulation of photovoltaic (PV) cells within solar panels, providing protection and enhancing the longevity and performance of solar modules.

The global push towards renewable energy, driven by both environmental concerns and governmental policies, is accelerating the adoption of solar power. According to the International Energy Agency (IEA), the installed capacity of solar PV is expected to increase by over 150 GW annually, reaching nearly 1,200 GW by 2030. This rapid growth is underpinned by decreasing costs of solar technology and supportive government policies across various regions.

In the United States, the Department of Energy (DOE) has launched the Solar Energy Technologies Office (SETO) program, which aims to cut the cost of solar energy by 50% by 2030. This initiative is expected to drive significant growth in the solar sector, thereby increasing the demand for EVA in solar panel manufacturing. The DOE’s ambitious goals highlight the critical role of EVA in achieving cost-effective and efficient solar energy solutions.

China, the world’s largest producer of solar energy, is a major market for EVA due to its extensive investments in renewable energy infrastructure. The National Energy Administration (NEA) of China aims to achieve 1,200 GW of solar and wind capacity by 2030. In 2023, China added approximately 48.2 GW of new solar PV capacity, demonstrating a substantial and ongoing demand for EVA used in solar modules.

India is also poised to become a significant market for EVA, driven by its National Solar Mission, which aims to reach 100 GW of solar capacity by 2022 and 450 GW by 2030. Government initiatives, such as subsidies and incentives for solar installations, are expected to propel the growth of the solar sector. This expansion will, in turn, drive the demand for EVA encapsulant materials essential for manufacturing reliable and durable solar panels.

The European Union’s Green Deal, which targets climate neutrality by 2050, includes plans to install over 320 GW of solar power by 2030. This policy framework supports the growth of the renewable energy sector and emphasizes the role of solar energy in reducing carbon emissions. The increasing adoption of solar energy across Europe will drive the demand for EVA in the region.

In the Middle East and Africa, countries like Saudi Arabia and the United Arab Emirates are investing heavily in solar projects as part of their strategies to diversify energy sources and reduce carbon footprints. Saudi Arabia’s Vision 2030 includes plans to generate 50% of its electricity from renewable sources, with solar energy playing a central role. These investments are expected to significantly boost the demand for EVA in the solar energy sector in these regions.

Trends

Increased Use of Bio-based Ethylene Vinyl Acetate

A significant trend in the Ethylene Vinyl Acetate (EVA) market is the increased use of bio-based EVA, driven by the global shift towards sustainable and eco-friendly materials. This trend is gaining traction as industries and governments alike emphasize reducing the environmental impact of chemical products.

Bio-based EVA is derived from renewable resources such as sugarcane, as opposed to traditional EVA, which is produced from petroleum-based ethylene. The shift towards bio-based alternatives is supported by various environmental benefits, including lower carbon footprints and reduced dependency on fossil fuels. According to the International Energy Agency (IEA), bio-based chemicals and materials could reduce greenhouse gas emissions by approximately 70% compared to their petroleum-based counterparts.

Leading chemical companies are actively investing in the development and production of bio-based EVA. For instance, Braskem, a prominent player in the EVA market, has been producing bio-based EVA from sugarcane ethanol since 2018. Braskem’s I’m green™ EVA is already being used in various applications, including footwear, automotive parts, and packaging. The company reports that its bio-based EVA can capture up to 3.09 tons of CO2 per ton produced, showcasing its environmental benefits.

Government initiatives and policies also support the adoption of bio-based materials. The European Union’s Green Deal, which aims for climate neutrality by 2050, encourages the use of renewable and bio-based materials in manufacturing. Similarly, the United States Department of Agriculture (USDA) promotes the development and use of bio-based products through its BioPreferred Program, which includes bio-based EVA as an eligible product.

In addition to environmental benefits, bio-based EVA offers comparable performance characteristics to traditional EVA, making it an attractive alternative for manufacturers. It retains the same flexibility, durability, and processing properties, enabling a seamless transition for industries looking to adopt more sustainable practices without compromising product quality.

The footwear industry is a notable sector where bio-based EVA is gaining popularity. Companies like Adidas and Nike are increasingly incorporating sustainable materials into their products. Adidas, for example, has launched shoes using Braskem’s I’m green™ EVA, aligning with their commitment to sustainability and reducing environmental impact.

The automotive industry also benefits from the use of bio-based EVA in applications such as interior trims and seals. The push towards sustainable materials in the automotive sector is driven by regulatory requirements and consumer demand for eco-friendly vehicles. The European Automobile Manufacturers’ Association (ACEA) supports the use of sustainable materials to meet the European Union’s stringent environmental standards.

Regional Analysis

The global Ethylene Vinyl Acetate (EVA) market demonstrates significant regional disparities, with distinct growth patterns and market dynamics. In North America, the EVA market is bolstered by the thriving packaging and solar industries. The region’s market growth is driven by increased demand for sustainable packaging solutions and the expansion of solar energy projects.

The presence of major players and technological advancements further support market growth. Europe follows suit with substantial market contributions from the automotive and footwear industries. The stringent environmental regulations and emphasis on sustainability in Europe have led to the adoption of EVA in various applications, fostering market expansion.

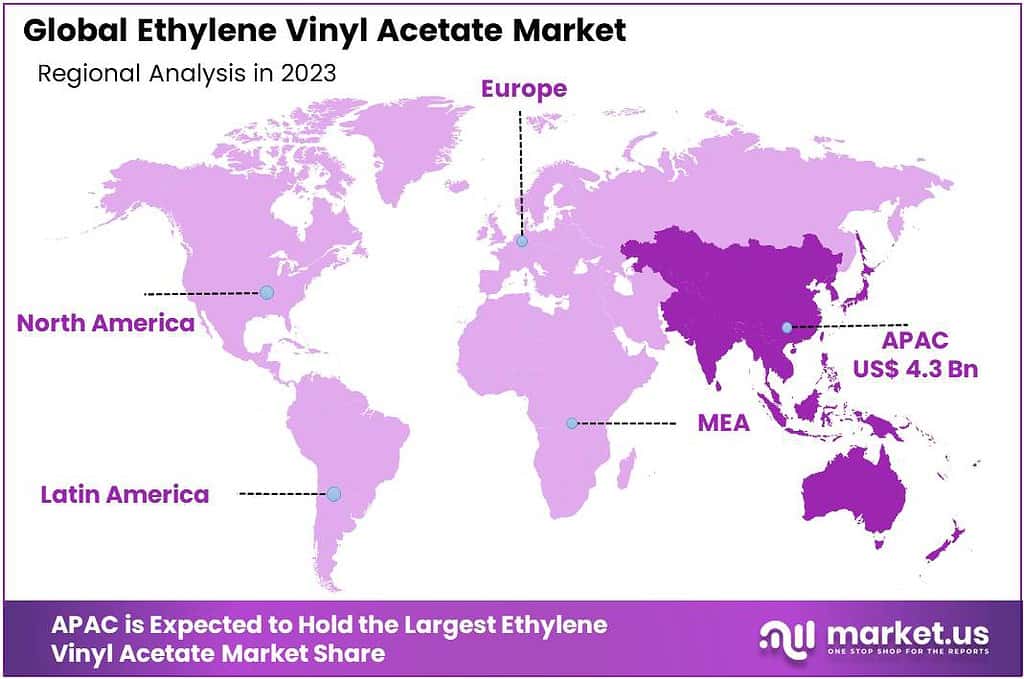

The Asia Pacific (APAC) region, however, dominates the global EVA market, accounting for 45.4% of the total market share, valued at approximately USD 4.35 billion. The rapid industrialization, urbanization, and economic growth in countries like China, India, and Japan significantly contribute to this dominance.

The booming construction sector, coupled with the rising demand for lightweight and durable materials in automotive and electronics, propels the market forward. Moreover, the region’s favorable government policies and investments in renewable energy projects, particularly in solar power, further amplify market growth.

In the Middle East & Africa, the EVA market experiences steady growth, primarily driven by the construction and packaging sectors. The region’s growing construction activities and infrastructural developments create substantial demand for EVA-based materials. Latin America, though a smaller market, exhibits promising growth potential.

The region’s increasing focus on industrialization and modernization, along with rising investments in renewable energy and packaging industries, contributes to the EVA market expansion. The regional market dynamics and growth prospects highlight the diverse and evolving nature of the global EVA market, with APAC leading the charge in market share and value.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Frequently Asked Questions (FAQ)

Ethylene Vinyl Acetate Market size is expected to be worth around USD 18.7 billion by 2033, from USD 9.6 billion in 2023

The Ethylene Vinyl Acetate Market is expected to grow at 6.9% CAGR (2024-2033).

Exxon Mobil Corporation, Dow Chemical Company, LyondellBasell Industries Holdings BV, Celanese Corporation, Braskem, Borealis AG, Mitsui Chemicals Inc., Sumitomo Chemical Co. Ltd., Hanwha Chemical Corp, Versalis S.p.A., LG Chem, Formosa Plastics Corporation, Westlake Chemical Corporation, Lotte Chemical Corporation, Indorama Ventures Public Company Limited