Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- US Esports Content Creation Market

- Content Type Analysis

- Platform Analysis

- Creator Type Analysis

- Revenue Model Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

The Esports Content Creation Market size is expected to be worth around USD 43.6 Billion By 2034, from USD 2.2 billion in 2024, growing at a CAGR of 34.8% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 32.4% share, holding USD 0.7 Billion revenue.

The esports content creation market is experiencing significant expansion, driven by the increasing popularity of gaming worldwide. This sector benefits from the broad audience base of platforms such as Twitch, which boasts over 140 million unique monthly viewers, and YouTube, with its extensive reach of over 2 billion monthly active users.

The growth of the esports content creation market can be attributed to several key drivers. Technological advancements in streaming technology and video production tools have greatly enhanced the quality of content that creators can produce, making it more appealing to a global audience. Increased viewer engagement and the expansion of monetization avenues, such as sponsorships, advertisements, and subscriptions, have made content creation a viable career path for many.

According to Market.us, the global esports market is projected to grow significantly, reaching USD 16.7 billion by 2033, up from USD 2.3 billion in 2023. This expansion represents a CAGR of 21.9% from 2024 to 2033. In 2023, North America led the market, capturing a 36.3% share, with revenue amounting to USD 0.83 billion.

Based on data from Influencer Marketing Hub, younger audiences in the U.S. are the biggest eSports fans. 43% of people aged 18-34 consider themselves avid or casual viewers. The 2023 League of Legends World Championship hit a new record with 6.4 million peak viewers, making it the most-watched eSports event ever. Additionally, 66% of all eSports content in 2023 was viewed through official streaming channels.

As stated by industry report, sponsorship deals in eSports are expected to generate $1.05 billion by 2025. Dota 2 remains the highest-paying game in the industry, with total prize money reaching $346.43 million as of April 2024. Fortnite also continues to dominate Twitch, with 5.53 million streamers between April 2023 and April 2024.

According to eSports Statistics, the largest prize pool in an eSports tournament exceeded $40 million. As of April 2024, Team Liquid stands as the highest-earning team in eSports history, accumulating $48.8 million in winnings.

Key Takeaways

- The Esports Content Creation Market is expected to grow significantly in the coming decade, driven by increasing audience engagement, rising investments, and the expansion of streaming platforms. The market is projected to reach USD 43.6 Billion by 2034, up from USD 2.2 Billion in 2024, growing at a CAGR of 34.8% from 2025 to 2034.

- North America held the dominant position in the esports content creation market, accounting for 32.4% of total market revenue, reaching USD 0.7 Billion in 2024.

- The United States led the market in North America, generating USD 0.57 Billion in revenue, with a projected CAGR of 32.2% during the forecast period.

- Live Streaming emerged as the leading segment, contributing 45.4% of the total market share in esports content creation. The increasing popularity of real-time gaming events and interactive streaming features has fueled this growth.

- Streaming Platforms dominated the market with a 52.6% market share, reflecting the growing reliance on platforms like Twitch, YouTube Gaming, and Facebook Gaming for content distribution.

- Professional Players and Teams played a crucial role in content creation, holding a 34.6% share of the market. High-profile gamers and esports organizations have become key influencers, driving viewership and engagement.

- Subscriptions remained the most significant revenue model in esports content creation, capturing 65.7% of the total market share. Subscription-based monetization models continue to gain traction due to exclusive content offerings and premium memberships.

Analysts’ Viewpoint

The market demand for esports content is propelled by the increasing number of esports enthusiasts who are not just interested in playing games but also in watching tournaments and gameplay streams. This trend is supported by the growing accessibility of esports through various digital platforms, making it easier for fans to connect with content creators and access their favorite content anytime and anywhere.

Adoption rates for esports content are high, with approximately 80% of gamers more likely to purchase games after watching them played or reviewed by content creators. The demand for quality esports content is driven by its ability to influence purchasing decisions and enhance the gaming experience, creating a lucrative market for skilled content creators

The growing influence of esports content creators presents significant investment opportunities. Brands and investors can capitalize on this trend by partnering with content creators for advertising, sponsorships, and collaborative content development. These partnerships not only drive brand awareness and sales but also tap into the content creators’ loyal and engaged audiences, offering a high return on investment.

Advancements in technology are significantly shaping the esports content creation space. Innovations such as AI-powered game highlight tools, advanced streaming software, and interactive platforms are enhancing how content is produced and consumed. These technologies allow for higher quality streams, better audience engagement tools, and more personalized content, which are crucial for maintaining viewer interest and engagement.

US Esports Content Creation Market

The US esports content creation market, valued at USD 0.57 billion in 2024, is witnessing a rapid growth trajectory with an impressive 32.2% CAGR. This growth underscores the dynamic expansion within the sector, driven by increasing consumer engagement and technological advancements that enhance the viewing experience.

Technological innovations, particularly in artificial intelligence and virtual reality, are revolutionizing the esports landscape by creating more immersive and interactive gaming experiences. These technologies not only enrich the gameplay but also open up new avenues for content creators to engage with a broader audience. The integration of AI and VR into gaming platforms is expected to attract a new wave of enthusiasts, thereby expanding the market size.

Investment in media rights, advertising, and sponsorships forms the backbone of revenue generation in the US esports market. Media rights deals, especially with platforms like Twitch and YouTube, are increasingly lucrative, reflecting the growing mainstream appeal of esports. The surge in advertising and sponsorships is fueled by the sector’s ability to reach a young, tech-savvy demographic, which is highly valued by advertisers.

Furthermore, the market is significantly influenced by major esports events and leagues that drive community engagement and viewer participation. These events not only enhance the visibility of esports but also contribute to substantial revenue through merchandise sales, ticket sales, and exclusive broadcasting deals.

In 2024, North America held a dominant market position in the esports content creation market, capturing more than a 32.4% share with revenues amounting to USD 0.7 billion. This prominent standing can be attributed to several key factors that uniquely position North America as a leader in the esports industry.

Firstly, North America benefits from a highly developed digital infrastructure, which is essential for the high-bandwidth demands of esports platforms and live streaming. The region’s robust internet services enable seamless live broadcasts and interactive gaming experiences that are critical for engaging audiences and hosting large-scale esports events.

This infrastructure supports not only the streaming of high-stakes tournaments but also the day-to-day content creation by thousands of individual creators and teams. Furthermore, the region hosts a large number of major esports leagues and tournaments, such as the League of Legends Championship Series and the Overwatch League.

These events attract significant viewership both online and offline, driving revenue through ticket sales, merchandise, and media rights. The presence of these leagues has established North America as a hub for esports, fostering a culture that encourages and celebrates esports content creation.

Content Type Analysis

In 2024, the Live Streaming segment held a dominant market position in the esports content creation landscape, capturing more than a 45.4% share. This leadership can be attributed to several key factors that are intrinsic to the nature and appeal of live streaming in the esports world.

Live streaming’s popularity stems from its ability to offer real-time engagement and a communal viewing experience that resonates deeply with the esports audience. Fans value the immediacy of live streaming, which allows them to witness events as they unfold, enhancing the thrill and suspense associated with competitive gaming.

This format supports interactive features such as live chats and instant reactions, which foster a sense of community among viewers and create a dynamic interaction between the audience and the streamers. Moreover, the widespread accessibility of robust internet connections and advanced streaming technologies has enabled a seamless live streaming experience that can support large volumes of viewers without compromising on quality.

These technological advancements have been crucial in maintaining the high engagement levels seen in live streaming, as they cater to the expectations of a tech-savvy audience looking for high-quality, uninterrupted content.

The economic model of live streaming also significantly contributes to its dominance. It attracts substantial revenue from advertisements, subscriptions, and sponsorships, driven by the large and engaged viewer base that live streams can pull in. The ability to monetize live streaming content effectively through various channels ensures that it remains a lucrative component of the esports content creation market.

Platform Analysis

In 2024, the Streaming Platforms segment held a dominant market position in the esports content creation industry, capturing more than a 52.6% share. This prominence is driven by several pivotal factors that highlight the central role of streaming platforms like Twitch, YouTube Gaming, and regional giants such as DouYu and Huya in the esports ecosystem.

Streaming platforms are the primary venue for live esports events, offering fans around the world instant access to tournaments and gameplay. These platforms cater to the growing demand for live digital entertainment, providing a space where viewers can watch their favorite gamers and teams in real time.

The interactive nature of these platforms, which allows viewers to engage directly with content creators through features like chat and donations, significantly enhances user engagement and retention rates. Moreover, streaming platforms have become highly effective at monetizing their content through advertising, subscriptions, and partnerships.

They offer tailored advertising opportunities to brands looking to reach a youthful, tech-savvy demographic, thus generating considerable revenue. The presence of built-in monetization tools helps content creators to earn a living, thereby attracting more creators to the platform and expanding the variety and quality of available content.

Technological advancements in streaming quality and accessibility have also contributed to the dominance of this segment. Improvements in video quality, streaming latency, and mobile accessibility ensure that fans can enjoy a high-quality viewing experience on any device, further solidifying the appeal of these platforms.

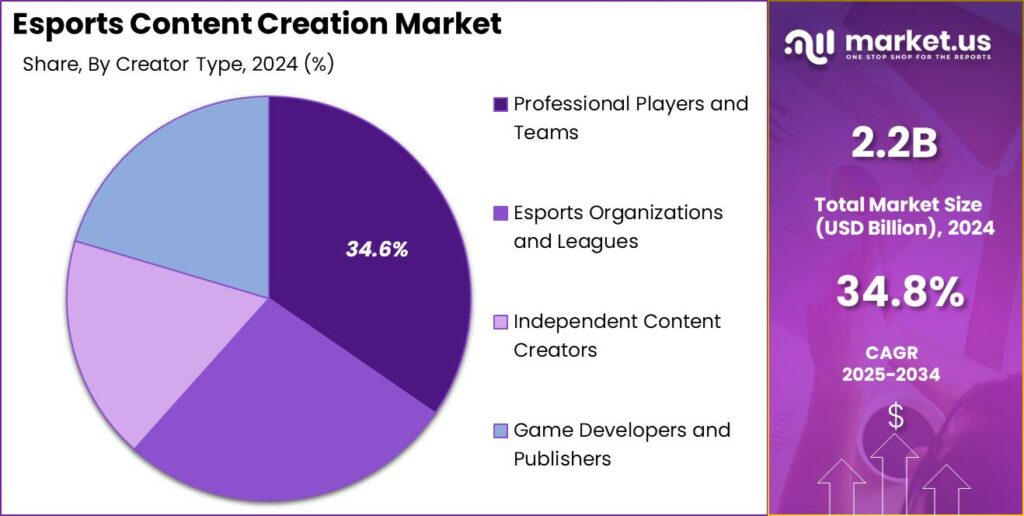

Creator Type Analysis

In 2024, the Professional Players and Teams segment held a dominant market position in the esports content creation industry, capturing more than a 34.6% share. This segment’s leadership is significantly attributed to its direct influence on fan engagement and content monetization strategies, which are pivotal in driving the growth of the esports ecosystem.

Professional players and teams are at the core of esports content, as they are the primary performers and competitors in tournaments that attract vast audiences both online and offline. Their gameplay, strategies, and personalities become a focal point for content across various platforms, making them central figures in broadcasting and streaming.

This direct connection with the audience cultivates a loyal fanbase eager to consume content that features their favorite teams and players, thereby enhancing viewer retention and engagement. Moreover, professional players and teams often have contractual agreements with esports organizations and sponsors that include content creation as a key component.

This arrangement not only helps in promoting the sponsors’ products but also ensures a steady stream of professionally produced content that maintains high production values. Such content is crucial for attracting sponsorship deals, which are a major revenue source in the esports industry.

Additionally, the content generated by professional players and teams extends beyond gameplay to include behind-the-scenes looks, training sessions, and personal vlogs, which provide a more comprehensive view of the players’ lives and routines. This variety enriches the content landscape, offering fans a closer, more personal connection to their esports heroes, and further solidifying the segment’s dominance in the market.

Revenue Model Analysis

In 2024, the Subscriptions segment held a dominant market position in the esports content creation market, capturing more than a 65.7% share. This significant market share can be attributed to several key factors that highlight the strength and appeal of the subscription revenue model in the digital entertainment sector.

Firstly, subscriptions offer a steady revenue stream for content creators and platforms, providing financial stability and predictability that is essential for long-term planning and investment. This model appeals to both independent creators and large organizations as it ensures consistent income based on viewer loyalty, rather than fluctuating ad-based revenues which can vary significantly month-to-month.

Moreover, subscribers typically enjoy a premium viewing experience devoid of advertisements, access to exclusive content, and other perks such as special emotes or badges in chat environments. This enhances viewer satisfaction and engagement, leading to higher retention rates. The value-added features provided with subscriptions encourage viewers to maintain their subscriptions over time, thereby sustaining the revenue flow for content creators and platforms.

Additionally, the subscription model aligns well with the community and fan-driven nature of esports. Fans are often willing to pay a subscription fee to support their favorite teams and players directly, which not only fosters a deeper connection between fans and creators but also enhances the community feeling around the content.

This model has proven particularly effective on platforms like Twitch and YouTube, where many viewers prefer uninterrupted access to content and are willing to pay for a more curated and enhanced viewing experience. The growth of this segment is bolstered by the widespread adoption of digital payment methods and the increasing willingness of consumers to pay for digital content, trends that are particularly strong among the tech-savvy esports audience.

Key Market Segments

By Content Type

- Live Streaming

- Professional tournament broadcasts

- Individual player streams

- Team practice sessions

- Behind-the-scenes content

- Video-on-Demand (VOD)

- Match highlights and replays

- Player interviews and profiles

- Strategy guides and tutorials

- Esports news and analysis

- Written Content

- Match reports and recaps

- Player and team profiles

- Industry news and updates

- Strategy articles and guides

By Platform

- Streaming Platforms

- Twitch

- YouTube Gaming

- Other regional platforms (e.g., DouYu, Huya)

- Social Media

- TikTok

- Others

- Dedicated Esports Websites

- Team and league websites

- Esports news portals

- Community forums

By Creator Type

- Professional Players and Teams

- Esports Organizations and Leagues

- Independent Content Creators

- Game Developers and Publishers

By Revenue Model

- Pay-per-use (PPU)

- Subscriptions

Driver

Expansion of Streaming Platforms

The expansion of streaming platforms represents a significant driver in the Esports Content Creation market. Platforms such as Twitch, YouTube Gaming, and Facebook Gaming have been pivotal in delivering content to a global audience, offering live streams, replays, and highlights of esports tournaments.

This accessibility allows fans to engage directly with their favorite players and teams through interactive features like live chats, donations, and subscriptions, thus driving viewer engagement and monetization opportunities.

Traditional media companies like ESPN and BBC have also ventured into esports, broadcasting events on television and digital channels, thereby further legitimizing esports as a mainstream form of entertainment.

Restraint

Lack of Profitability

A major restraint in the esports industry is its struggle with profitability. Despite substantial viewership and participation growth, core esports organizations such as tournament organizers and professional teams often do not see adequate financial returns.

This challenge stems from an underdeveloped revenue model compared to other entertainment sectors like film or traditional sports, where revenue streams are more diversified and stable. Esports events primarily serve as marketing tools for game publishers rather than profitable ventures, limiting the financial sustainability of the industry.

Opportunity

Mobile and Immersive Technologies

Mobile esports and immersive technologies like virtual reality present significant growth opportunities. The popularity of mobile gaming has surged, driven by the accessibility of smartphones and improvements in mobile internet reliability, such as the advent of 5G technology.

Games like PUBG Mobile and Free Fire have attracted vast audiences, especially in emerging markets. Moreover, the potential integration of esports with the metaverse and VR technologies promises a more engaging and immersive fan experience, opening new avenues for content creation and fan engagement.

Challenge

Regulatory and Ethical Issues

Regulatory and ethical issues pose a major challenge to the esports industry. The lack of standardized regulations and governance structures can lead to problems such as match-fixing and cheating. Furthermore, concerns over player welfare and burnout are growing, given the intense schedules and high expectations placed on professional players.

Addressing these issues will require collaborative efforts among industry stakeholders to establish clear guidelines and support systems that ensure the integrity and viability of esports as both a competitive sport and a form of entertainment.

Growth Factors

The esports industry has witnessed substantial growth, fueled by several key factors. One significant driver is the increase in sponsorship and media rights investments. Brands like Coca-Cola and Mercedes-Benz are leveraging the platform to reach a younger, digitally-savvy audience, which has propelled the popularity of esports events to new heights.

The rise of mobile esports also contributes significantly, driven by the ubiquity of smartphones and the increasing quality of mobile games.Furthermore, the integration of advanced technologies, including artificial intelligence and virtual reality, is enhancing player training and spectator experiences, promising continued growth and diversification of the esports realm.

Emerging Trends

Emerging trends within the esports industry are shaping its future trajectory. Notably, mobile gaming is rapidly gaining traction, broadening the audience base by making competitive gaming more accessible through smartphones and tablets.

Additionally, technologies like augmented and virtual reality are being increasingly adopted, offering immersive experiences that could redefine spectator engagement in esports. Another growing trend is the emphasis on sustainability and inclusivity, with initiatives aimed at reducing environmental impacts and promoting diversity within the gaming community.

Business Benefits

Esports offers multiple avenues for revenue, making it an attractive sector for investments and business operations. The primary revenue streams include sponsorships, media rights, advertising, merchandise, and ticket sales. Sponsorship remains a dominant force, with major brands investing in teams and events to reach younger, tech-savvy audiences effectively.

Media rights are also witnessing significant growth, with revenues increasing due to the demand for content across various streaming platforms. The sector’s expansion into educational and institutional areas further presents opportunities for growth in training, development, and professionalization of esports.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

The Esports Content Creation Market has witnessed significant activity from key players such as Activision Blizzard, Tencent Holdings, and Modern Times Group, each employing strategies to solidify their market positions through acquisitions, new product launches, and mergers.

Activision Blizzard has been a prominent figure in the market, known for strategic acquisitions that enhance their capabilities and expand their reach within the esports sector. Notably, their acquisition strategy aims to integrate and broaden their esports and entertainment offerings, ensuring a dominant presence in the market.

Tencent Holdings is another major player that has significantly influenced the market through strategic partnerships and investments. The company’s approach to mergers and acquisitions has been pivotal in establishing its foothold in various regional markets, thereby driving their global expansion strategy.

Modern Times Group (MTG) has also made impactful moves through acquisitions and strategic partnerships. MTG’s approach focuses on diversifying their portfolio and enhancing their competitive edge in the esports content creation space.

Top Key Players in the Market

- Tencent Holdings Ltd.

- Microsoft Corporation

- Activision Blizzard, Inc.

- Electronic Arts Inc. (EA)

- Riot Games, Inc.

- Epic Games, Inc.

- NetEase, Inc.

- Valve Corporation

- FaZe Clan

- Others

Recent Developments

- Tencent has continued to expand its esports ecosystem by investing heavily in user-generated content (UGC) and new intellectual properties (IPs). In January 2025, Tencent announced partnerships with local developers to create culturally relevant esports content, further strengthening its global reach.

- Valve revamped its Counter-Strike ecosystem in early 2025, introducing a decentralized tournament model that allows multiple organizers to host events. This shift aims to increase accessibility and diversity in Counter-Strike esports.

- Microsoft has integrated esports into its Xbox Game Pass ecosystem, focusing on community-driven tournaments. In February 2025, it launched a new feature enabling players to host competitive events directly from the platform, enhancing grassroots esports participation.

- Activision Blizzard is focusing on expanding its flagship esports titles. In January 2025, it announced a major update to the Overwatch League, introducing regional tournaments and revenue-sharing models for teams to drive sustainability.

- EA emphasized player engagement through innovative esports strategies. In January 2025, it introduced virtual naming rights for in-game assets in FIFA and Apex Legends esports, allowing brands to sponsor virtual items, a move aimed at monetizing user engagement.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.2 Bn |

| Forecast Revenue (2034) | USD 43.6 bn |

| CAGR (2025-2034) | 34.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Content Type (Live Streaming (Professional tournament broadcasts, Individual player streams, Team practice sessions, Behind-the-scenes content), Video-on-Demand (VOD)(Match highlights and replays, Player interviews and profiles, Strategy guides and tutorials, Esports news and analysis), Written Content (Match reports and recaps, Player and team profiles, Industry news and updates, Strategy articles and guides)), By Platform (Streaming Platforms (Twitch, YouTube Gaming, Other regional platforms (e.g., DouYu, Huya)), Social Media (Twitter, Instagram, TikTok, Facebook, Others), Dedicated Esports Websites (Team and league websites, Esports news portals, Community forums)), By Creator Type (Professional Players and Teams, Esports Organizations and Leagues, Independent Content Creators, Game Developers and Publishers), By Revenue Model (Pay-per-use (PPU), Subscriptions) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Tencent Holdings Ltd., Microsoft Corporation, Activision Blizzard, Inc., Electronic Arts Inc. (EA), Riot Games, Inc., Epic Games, Inc., NetEase, Inc., Valve Corporation, FaZe Clan, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |