Global Eco-Friendly Packaging Market Size, Share, Growth Analysis Type (Recyclable, Reusable, Degradable), Material Type (Paper and Paperboard, Plastic, Metal, Glass, Starch-Based Materials, Others), Product Type (Boxes, Bags, Pouches and Sachets, Containers, Films, Trays, Tubes, Bottles and Jars, Cans, Others), Technique (Alternate Fiber Packaging, Active Packaging, Molded Packaging, Others), Layer (Primary Packaging, Secondary Packaging, Tertiary Packaging), Application (Food and Beverages, Pharmaceutical, Personal Care, Home Care, Others), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178395

- Number of Pages: 213

- Format:

-

keyboard_arrow_up

Quick Navigation

Market Overview

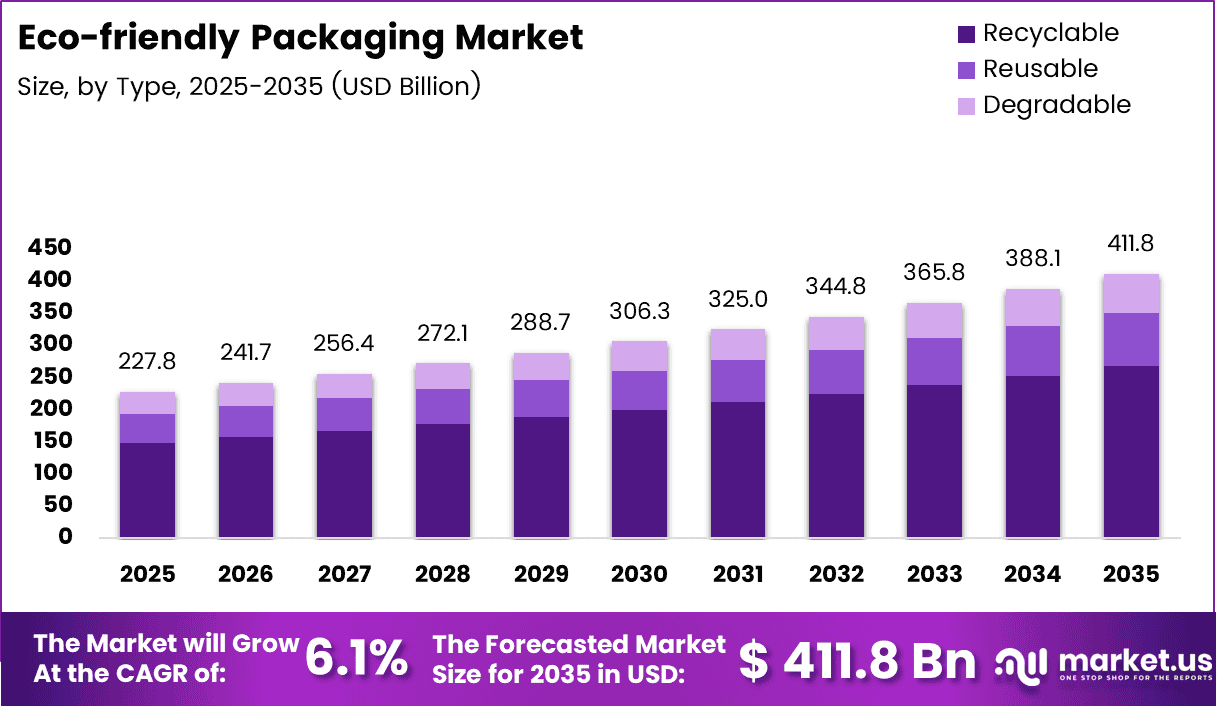

Global Eco-Friendly Packaging Market size is expected to be worth around USD 411.8 Billion by 2035 from USD 227.8 Billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

Eco-friendly packaging refers to packaging solutions designed to minimize environmental impact. These solutions use materials that are recyclable, reusable, biodegradable, or compostable. Moreover, they help reduce carbon emissions, plastic waste, and landfill pressure across global supply chains.

The market spans a wide range of materials including paper, cardboard, glass, metal, and bio-based alternatives. Consequently, industries from food and beverages to pharmaceuticals and personal care are adopting these solutions. This shift reflects a broader transition toward sustainable production and responsible consumption practices.

Growth in this market is driven by increasing regulatory pressure on single-use plastics worldwide. Governments across Europe, North America, and Asia Pacific have introduced bans and compliance mandates. Additionally, corporate sustainability commitments from major FMCG and e-commerce brands are accelerating adoption at scale.

Investment in eco-friendly packaging innovation continues to rise steadily. Green startups and established manufacturers are collaborating to develop lightweight, compostable, and water-soluble materials. Furthermore, circular economy frameworks are being integrated into packaging supply chains, creating long-term structural demand across multiple industries.

According to a joint report by the World Economic Forum and Ellen MacArthur Foundation, packaging takes up almost a third of all plastics production, yet only 14% of it is recycled. Additionally, around 36% of all plastics produced are used in packaging, making it the largest generator of single-use plastic waste globally.

According to DHL, cardboard boxes reduce oil and CO2 emissions by 60% compared to plastic alternatives. Furthermore, recent data reveals that 44% of customers choose to buy from brands with a clear commitment to sustainability, reinforcing demand for eco-friendly packaging across consumer-facing industries.

Key Takeaways

- The Global Eco-Friendly Packaging Market was valued at USD 227.8 Billion in 2025 and is projected to reach USD 411.8 Billion by 2035.

- The market is expected to grow at a CAGR of 6.1% during the forecast period 2026 to 2035.

- By Type, Recyclable packaging held the dominant position with a 65.2% market share in 2025.

- By Material Type, Paper and Paperboard led the segment with a 48.4% share in 2025.

- By Product Type, Boxes dominated with a 32.5% share in 2025.

- By Technique, Alternate Fiber Packaging held the largest share at 44.7% in 2025.

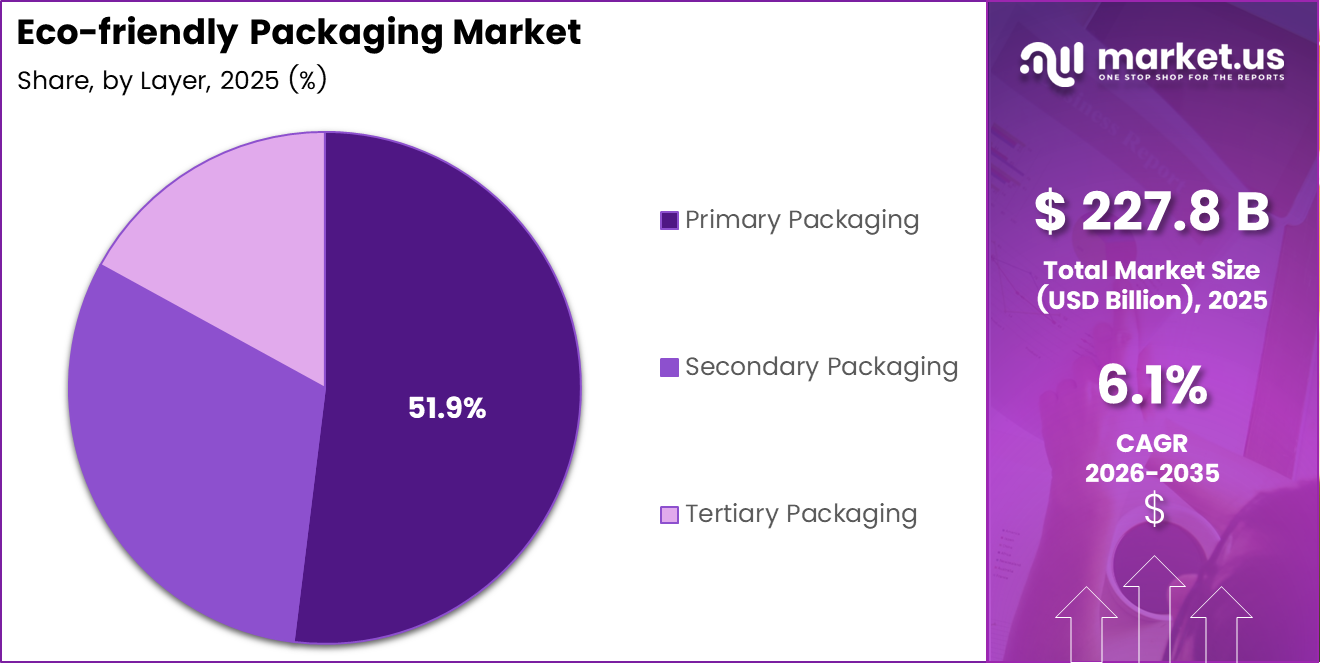

- By Layer, Primary Packaging led with a 51.9% share in 2025.

- By Application, Food and Beverages was the leading segment with a 37.1% share in 2025.

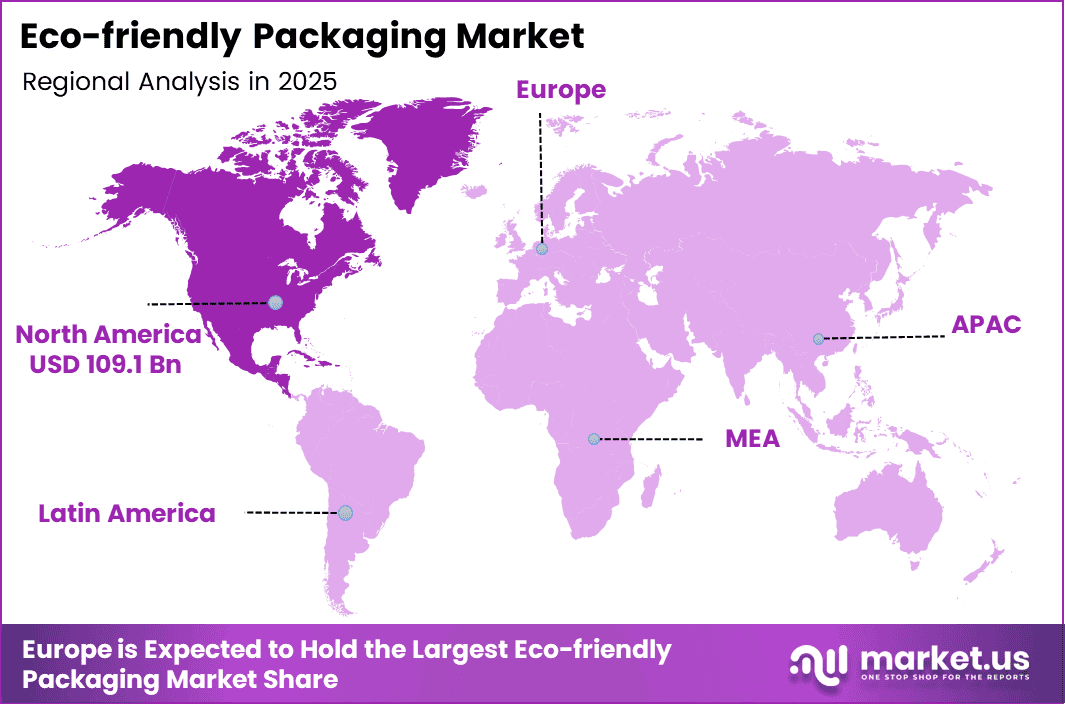

- North America dominated the regional landscape with a 47.90% share, valued at USD 109.1 Billion in 2025.

Type Analysis

Recyclable packaging dominates with 65.2% due to widespread regulatory support and consumer preference for materials that can re-enter production cycles.

In 2025, Recyclable held a dominant market position in the Type segment of the Eco-Friendly Packaging Market, with a 65.2% share. This leadership reflects growing policy mandates and strong retailer demand for packaging that supports closed-loop recycling systems. Moreover, recyclable formats are compatible with existing waste management infrastructure globally.

Reusable packaging is gaining traction as brands explore refill and return models to reduce single-use waste. Consequently, this sub-segment is attracting investment from FMCG companies committed to long-term sustainability targets. However, logistics complexity and consumer behavior remain key challenges for broader adoption.

Degradable packaging addresses waste management needs where recycling infrastructure is limited. Therefore, it is particularly relevant in emerging markets and foodservice sectors. Additionally, ongoing material innovation is improving the performance and cost-effectiveness of degradable options across multiple end-use applications.

Material Type Analysis

Paper and Paperboard dominates with 48.4% due to its biodegradability, wide availability, and compatibility with sustainable packaging goals across industries.

In 2025, Paper and Paperboard held a dominant market position in the Material Type segment of the Eco-Friendly Packaging Market, with a 48.4% share. This material offers strong recyclability and biodegradability, making it a preferred choice for brands reducing plastic usage. Moreover, it supports branding and printing requirements across food, retail, and e-commerce sectors.

Plastic remains in use within eco-friendly packaging through recycled and bio-based variants. However, regulatory pressure is steadily pushing manufacturers to develop cleaner alternatives. Consequently, investment in recyclable and compostable plastic substitutes is increasing among packaging companies globally.

Metal packaging is widely valued for its strength, durability, and superior barrier properties against light, moisture, and oxygen. It is commonly used in food, beverage, and industrial applications where long shelf life is critical. High recyclability further supports its role in sustainable packaging systems.

Glass offers excellent product protection due to its non-reactive and impermeable nature. It is preferred in pharmaceuticals, beverages, and premium food packaging for preserving purity and taste. Its infinite recyclability without quality loss enhances its environmental appeal.

Starch-based materials are gaining traction as biodegradable and compostable packaging alternatives. Derived from renewable agricultural sources, they help reduce dependence on fossil-based plastics. These materials are increasingly used in disposable packaging and food service applications.

Others category includes materials such as paper composites, bioplastics, and hybrid packaging solutions.These materials address specific functional needs like flexibility, lightweighting, or cost efficiency. Innovation in this segment supports niche applications and customized packaging requirements.

Product Type Analysis

Boxes dominate with 32.5% due to their structural versatility, recyclability, and widespread use across e-commerce and food packaging.

In 2025, Boxes held a dominant market position in the Product Type segment of the Eco-Friendly Packaging Market, with a 32.5% share. Their adaptability across product categories and compatibility with paper-based materials make them a top choice. Moreover, the e-commerce boom has significantly elevated demand for sustainable corrugated and folding box formats.

Bags are widely used for their flexibility, lightweight structure, and ease of handling. They support bulk as well as retail packaging across food, agriculture, and consumer goods. Customization options further enhance branding while ensuring functional product protection.

Pouches and sachets are preferred for single-use and portion-controlled packaging formats. They offer cost efficiency, reduced material consumption, and extended shelf life. Their compact design aligns well with convenience-driven and on-the-go consumer behavior.

Containers ensure secure storage for solid, liquid, and semi-solid products across industries. They are valued for durability, stackability, and product safety. Multiple material options enable use in both industrial and consumer applications.

Films are extensively used for wrapping, sealing, and protective layering applications. They help preserve freshness, enhance visibility, and provide moisture resistance. Ongoing advancements focus on thinner, stronger, and more sustainable film solutions.

Trays are commonly used for food presentation, packaging, and product organization. They provide stability, portion control, and ease of display at retail. Lightweight designs improve handling efficiency without compromising strength.

Tubes are ideal for packaging creams, gels, and semi-liquid formulations. They support controlled dispensing while maintaining hygiene and product integrity. Demand continues to grow in personal care, cosmetics, and pharmaceutical sectors.

Bottles and jars are widely used for beverages, food products, and personal care items. They offer strong protection, resealability, and product visibility. Innovation in this segment focuses on lightweighting and recyclable materials.

Cans are known for their excellent barrier properties and long shelf life. They are extensively used for beverages, processed foods, and aerosol products. High recyclability makes them a key component of circular packaging systems.

Others include specialized and hybrid packaging formats designed for niche applications. These solutions address unique requirements such as premium aesthetics or technical performance. Innovation in this segment supports evolving industry-specific packaging demands.

Technique Analysis

Alternate Fiber Packaging dominates with 44.7% due to its role as a scalable, plant-based alternative to plastic and conventional materials.

In 2025, Alternate Fiber Packaging held a dominant market position in the Technique segment of the Eco-Friendly Packaging Market, with a 44.7% share. This technique uses agricultural residues and non-wood plant fibers to create sustainable packaging formats. Moreover, it supports waste reduction goals while offering competitive performance characteristics for various product categories.

Active Packaging incorporates functional elements such as oxygen absorbers and moisture regulators to extend product shelf life. Therefore, it is gaining adoption in food and pharmaceutical sectors. Consequently, its integration with eco-friendly materials is opening new opportunities for sustainable performance packaging.

Molded packaging utilizes pulp and fiber-based materials formed into rigid, protective shapes for fragile goods. It offers strong cushioning performance while remaining biodegradable and recyclable. This format is widely adopted in electronics, food service, and consumer goods for sustainable protection.

Other formats include water-soluble and edible packaging designed to eliminate post-use waste. These solutions support zero-waste goals and reduce reliance on conventional plastics. Growing brand focus on circular economy models is driving investment in these emerging technologies.

Layer Analysis

Primary Packaging dominates with 51.9% as it directly contacts the product and is the most critical layer for material innovation and compliance.

In 2025, Primary Packaging held a dominant market position in the Layer segment of the Eco-Friendly Packaging Market, with a 51.9% share. It is the layer in direct contact with the product, making material safety and sustainability especially important. Moreover, regulatory requirements on food contact materials are driving brands to adopt certified eco-friendly primary packaging solutions.

Secondary Packaging groups and protects primary units during retail display and transport. Consequently, paper-based and recyclable materials are replacing plastic shrink wraps and foam inserts in this layer. Additionally, minimalist secondary packaging design is gaining popularity as brands pursue waste reduction targets.

Tertiary Packaging is used for bulk handling and logistics operations. Therefore, sustainable corrugated and fiber-based materials are increasingly preferred by distributors and retailers. Furthermore, optimizing tertiary packaging for weight and volume is helping companies reduce overall supply chain emissions and packaging waste.

Application Analysis

Food and Beverages dominates with 37.1% due to high packaging volume, strict regulatory requirements, and strong consumer demand for sustainable food packaging.

In 2025, Food and Beverages held a dominant market position in the Application segment of the Eco-Friendly Packaging Market, with a 37.1% share. This sector generates the highest packaging volumes globally and faces increasing scrutiny over single-use plastic waste. Moreover, retailer sustainability mandates are pushing food brands to transition rapidly toward recyclable and compostable formats.

Pharmaceutical packaging is focused on ensuring product integrity, safety, and compliance with strict regulations. It protects medicines from contamination, moisture, and environmental factors. Features such as tamper evidence and precise dosing are essential to build consumer trust.

Personal care packaging emphasizes both functionality and visual appeal to attract consumers. It supports easy dispensing, portability, and protection of formulations. Innovative designs and premium finishes are widely used to strengthen brand identity.

Home care packaging is designed to be durable and user-friendly while safely containing chemical-based products. It enables controlled usage and minimizes the risk of leakage or spills. Increasing demand for recyclable and eco-friendly materials is influencing packaging development.

Others category includes specialized packaging applications across diverse industries. These solutions are tailored to meet unique storage, handling, or presentation requirements. Continuous innovation supports emerging use cases and customized packaging needs.

Key Market Segments

By Type

- Recyclable

- Reusable

- Degradable

By Material Type

- Paper and Paperboard

- Plastic

- Metal

- Glass

- Starch-Based Materials

- Others

By Product Type

- Boxes

- Bags

- Pouches and Sachets

- Containers

- Films

- Trays

- Tubes

- Bottles and Jars

- Cans

- Others

By Technique

- Alternate Fiber Packaging

- Active Packaging

- Molded Packaging

- Others

By Layer

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

By Application

- Food and Beverages

- Pharmaceutical

- Personal Care

- Home Care

- Others

Drivers

Escalating Government Regulations and Corporate Sustainability Goals Drive Eco-Friendly Packaging Market Growth

Governments worldwide are enforcing strict regulations to reduce single-use plastics across retail, foodservice, and industrial sectors. Bans on plastic bags, straws, and non-recyclable packaging are now active across the European Union, parts of Asia, and North America. Consequently, manufacturers are under direct regulatory pressure to transition toward compliant sustainable packaging formats.

Rising corporate sustainability commitments are reinforcing market demand, particularly among FMCG and e-commerce brands. Moreover, major retailers are setting internal targets to eliminate non-recyclable packaging from their supply chains by fixed deadlines. Therefore, packaging suppliers that offer certified eco-friendly solutions hold a strong competitive advantage in procurement decisions.

Growing consumer awareness of packaging waste is also a key demand driver. Additionally, research confirms that 44% of customers prefer brands with a clear sustainability commitment. This behavioral shift is compelling brands across food, personal care, and home care sectors to adopt eco-friendly packaging as a core part of their market positioning strategy.

Restraints

Higher Costs and Material Performance Gaps Restrain Broader Adoption of Eco-Friendly Packaging

One of the primary challenges facing the eco-friendly packaging market is the higher production cost compared to conventional plastic packaging. Bio-based and compostable materials often require specialized processing and certification, which increases unit costs. Consequently, smaller manufacturers and price-sensitive markets find it difficult to justify the cost premium over traditional alternatives.

Limited availability of high-performance biodegradable materials remains a significant barrier to adoption. Moreover, many compostable or bio-based options do not yet match the barrier properties, shelf life performance, or mechanical strength of conventional plastics. Therefore, industries such as pharmaceuticals and fresh food face particular challenges in sourcing viable eco-friendly packaging solutions at commercial scale.

Supply chain constraints further complicate the transition for global packaging buyers. Additionally, inconsistent quality standards and variable raw material availability affect production reliability. Furthermore, the absence of harmonized international regulations on what qualifies as eco-friendly or compostable packaging creates confusion and compliance complexity for multinational brands operating across multiple markets.

Growth Factors

Compostable Materials, Emerging Market Demand, and Innovation Drive Eco-Friendly Packaging Growth

The expanding adoption of compostable and bio-based packaging materials is creating significant growth opportunities globally. As industrial composting infrastructure improves, brands are integrating fully compostable solutions into their packaging strategy. Moreover, innovations such as packaging that returns to organic waste within 24 weeks in industrial and home compost conditions are advancing circular packaging models.

Emerging economies in Asia Pacific, Latin America, and Africa represent a major untapped opportunity for the eco-friendly packaging market. Consequently, rising urbanization, expanding retail sectors, and increasing regulatory activity in these regions are generating new demand. Additionally, growing middle-class consumer awareness of environmental issues is accelerating preference for sustainable product packaging in these high-growth markets.

Strategic partnerships between established packaging manufacturers and green technology startups are accelerating innovation. Therefore, new lightweight, recyclable, and reusable packaging designs are entering commercial production at faster rates. Furthermore, investment in circular economy models is restructuring packaging supply chains, creating long-term structural growth for eco-friendly packaging solutions across multiple industries.

Emerging Trends

Plant-Based Materials, Zero-Waste Design, and Circular Economy Models Shape the Future of Eco-Friendly Packaging

A prominent trend reshaping the eco-friendly packaging landscape is the shift toward plant-based and fiber-derived packaging solutions. Manufacturers are increasingly using agricultural waste, bamboo, and sugarcane fiber as raw materials. Moreover, these alternatives offer strong sustainability credentials while delivering functional performance comparable to conventional paper and plastic formats.

Minimalist and zero-waste packaging concepts are gaining commercial traction across consumer goods and e-commerce sectors. Consequently, brands are reducing packaging layers, eliminating unnecessary components, and prioritizing designs that generate less post-consumer waste. Additionally, this approach aligns with tightening Extended Producer Responsibility regulations in Europe and North America that hold brands accountable for packaging waste outcomes.

The integration of circular economy models into packaging supply chains is becoming a defining feature of the market. Therefore, packaging is increasingly designed for reuse, refill, or complete material recovery. Furthermore, rising adoption of water-soluble and edible packaging materials signals a broader industry shift toward innovations that fundamentally eliminate packaging waste at the point of consumption.

Regional Analysis

North America Dominates the Eco-Friendly Packaging Market with a Market Share of 47.90%, Valued at USD 109.1 Billion

North America leads the global eco-friendly packaging market, accounting for a 47.90% share valued at USD 109.1 Billion in 2025. Strong regulatory frameworks targeting single-use plastics and robust corporate sustainability commitments across the United States and Canada are primary growth drivers. Moreover, advanced recycling infrastructure and high consumer awareness further support market leadership in this region.

Europe Eco-Friendly Packaging Market Trends

Europe represents a highly mature and regulation-driven market for eco-friendly packaging. The European Union’s Single-Use Plastics Directive and Extended Producer Responsibility frameworks are enforcing rapid transitions across member states. Consequently, demand for certified compostable, recyclable, and reusable packaging formats is among the highest globally, particularly in Germany, France, and the UK.

Asia Pacific Eco-Friendly Packaging Market Trends

Asia Pacific is emerging as the fastest-growing regional market for eco-friendly packaging. Rapid industrialization, expanding e-commerce, and growing government initiatives against plastic waste are driving adoption across China, India, Japan, and South Korea. Additionally, increasing consumer awareness and retailer sustainability mandates are accelerating the transition to sustainable packaging formats in this region.

Latin America Eco-Friendly Packaging Market Trends

Latin America is showing steady growth in the eco-friendly packaging market, supported by rising environmental awareness and evolving plastic waste regulations. Brazil and Mexico are the largest contributors, driven by consumer goods manufacturing and food processing sectors. However, cost sensitivity and fragmented recycling infrastructure remain key challenges to faster adoption across the region.

Middle East and Africa Eco-Friendly Packaging Market Trends

The Middle East and Africa region is at an early but accelerating stage of eco-friendly packaging adoption. Government sustainability initiatives in GCC countries and growing retail modernization are creating new demand. Moreover, international brand presence and export-oriented food processing industries are introducing sustainable packaging standards, gradually influencing local manufacturing and consumer markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

International Paper is one of the world’s largest producers of renewable fiber-based packaging, pulp, and paper. The company has made significant strides in sustainable packaging by expanding its recyclable and fiber-based product lines. Moreover, its broad manufacturing footprint and supply chain capabilities position it as a foundational supplier to global FMCG, e-commerce, and industrial packaging customers.

WestRock Company operates as a leading integrated provider of paper and packaging solutions with a strong sustainability focus. The company delivers corrugated containers, folding cartons, and consumer packaging designed to meet evolving eco-friendly standards. Additionally, WestRock’s investment in recyclable material innovation and its partnerships with major retail and consumer brands reinforce its competitive standing in sustainable packaging.

Oji Holdings Corporation is a major Japanese packaging and paper group with a diversified portfolio spanning containerboard, industrial packaging, and specialty paper products. The company is actively expanding its eco-friendly packaging capabilities across Asia Pacific markets. Consequently, its focus on renewable fiber sourcing and recyclable packaging innovation aligns well with regional sustainability regulations and growing corporate environmental commitments.

Smurfit Kappa is a leading European-based provider of paper-based packaging solutions serving customers across more than 30 countries. The company specializes in corrugated and solid board packaging with a strong emphasis on circular economy principles. Furthermore, Smurfit Kappa’s investment in sustainable design tools and its commitment to fully renewable packaging materials make it a benchmark player in the global eco-friendly packaging industry.

Key Players

- International Paper

- WestRock Company

- Oji Holdings Corporation

- Smurfit Kappa

- Mondi plc

- Klabin SA

- Billerudkorsnas

- Stora Enso

- Daio Paper Construction

- Nordic Paper

Recent Developments

- August 2025 – BioPak acquired sustainable packaging company Bygreen, reported to be Australia’s top importer of eco-friendly straws, barware, and wooden tableware. This acquisition strengthens BioPak’s sustainable product portfolio and expands its distribution reach across the Australian market.

- November 2025 – TIPA Compostable Packaging, together with its European subsidiary Bio4Pack, announced the acquisition of SEALPAP, a pioneer in recyclable paper-based packaging. This strategic move broadens TIPA’s product range by adding recyclable paper-based solutions to its existing compostable flexible packaging portfolio.

Report Scope

Report Features Description Market Value (2025) USD 227.8 Billion Forecast Revenue (2035) USD 411.8 Billion CAGR (2026-2035) 6.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Type (Recyclable, Reusable, Degradable), Material Type (Paper and Paperboard, Plastic, Metal, Glass, Starch-Based Materials, Others), Product Type (Boxes, Bags, Pouches and Sachets, Containers, Films, Trays, Tubes, Bottles and Jars, Cans, Others), Technique (Alternate Fiber Packaging, Active Packaging, Molded Packaging, Others), Layer (Primary Packaging, Secondary Packaging, Tertiary Packaging), Application (Food and Beverages, Pharmaceutical, Personal Care, Home Care, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape International Paper, WestRock Company, Oji Holdings Corporation, Smurfit Kappa, Mondi plc, Klabin SA, Billerudkorsnas, Stora Enso, Daio Paper Construction, Nordic Paper Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Eco-friendly Packaging MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Eco-friendly Packaging MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- International Paper

- WestRock Company

- Oji Holdings Corporation

- Smurfit Kappa

- Mondi plc

- Klabin SA

- Billerudkorsnas

- Stora Enso

- Daio Paper Construction

- Nordic Paper

Our Clients

- 178395

- Feb 2026