Global ECG Machine Market By Product Type (ECG Holter Monitoring System, ECG Resting System, Cardiopulmonary Stress Testing System and ECG Stress Testing System), By Technology (Digital and Analog), By Modality (Wireless and Wired), By End User (Hospitals, Specialty Clinics and Ambulatory Surgical Centers), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179023

- Number of Pages: 233

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

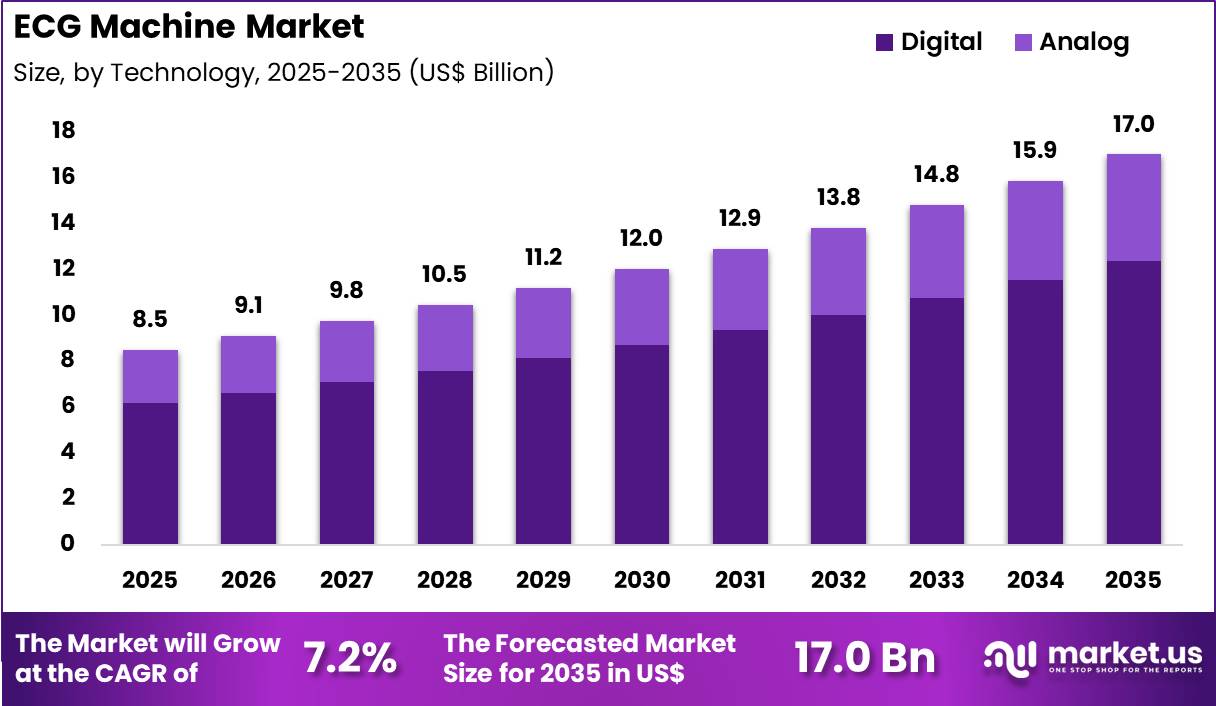

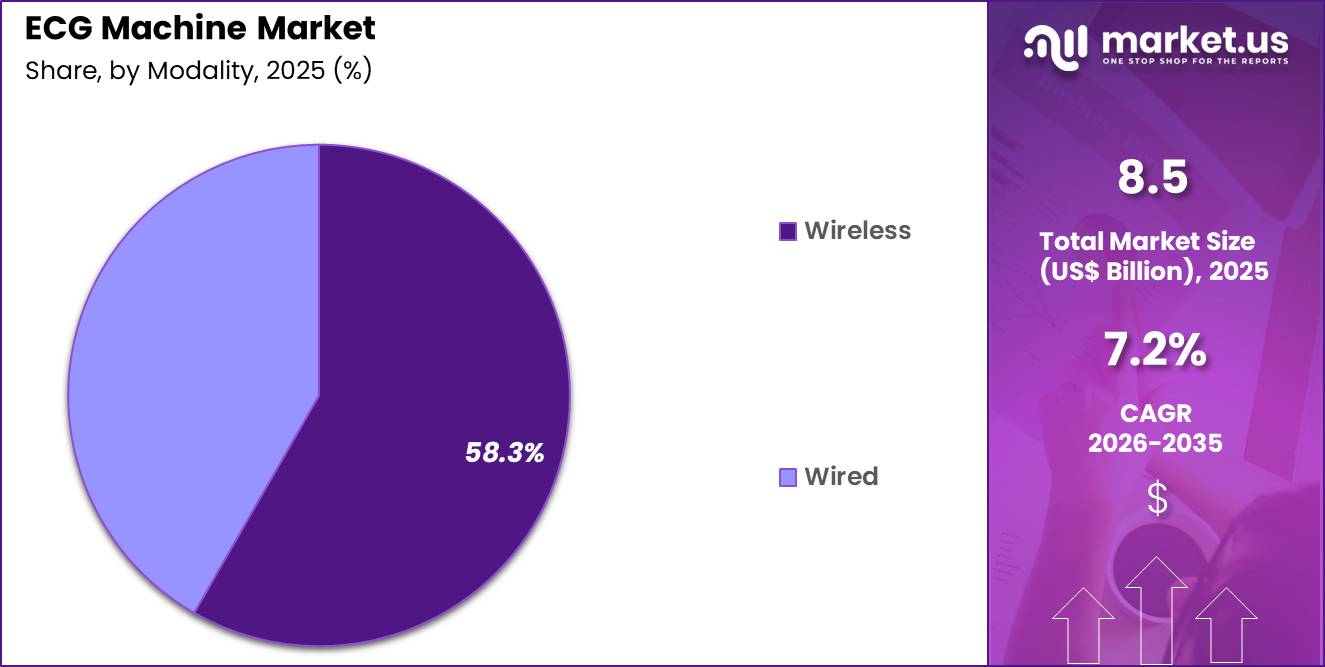

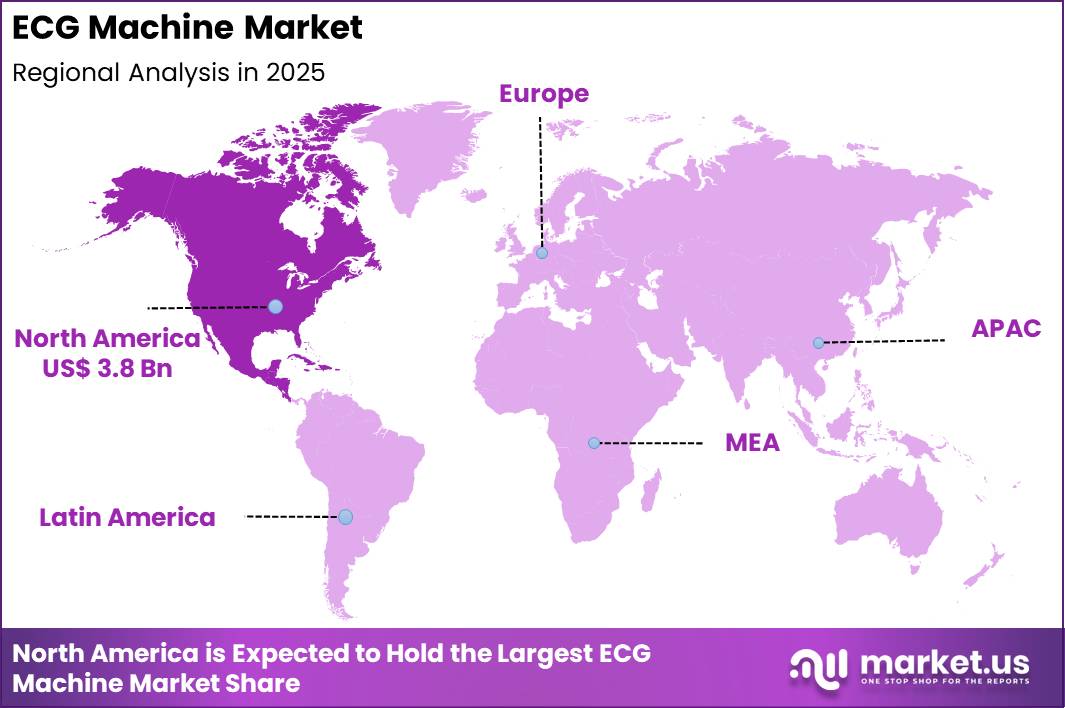

The Global ECG Machine Market size is expected to be worth around US$ 17.0 Billion by 2035 from US$ 8.5 Billion in 2025, growing at a CAGR of 7.2% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 45.1% share with a revenue of US$ 3.8 Billion.

Rising prevalence of cardiovascular diseases and the emphasis on early detection propel the ECG machine market as healthcare providers require reliable, high-fidelity tools to capture electrical activity of the heart and support timely clinical decisions.

Cardiologists increasingly utilize 12-lead ECG systems in outpatient clinics to diagnose arrhythmias, myocardial ischemia, and conduction abnormalities during routine screenings and symptomatic evaluations. These devices support emergency department applications by enabling rapid identification of ST-elevation myocardial infarction, guiding immediate reperfusion strategies in acute coronary syndromes.

Primary care physicians apply portable ECG machines for ambulatory monitoring of palpitations and syncope, facilitating detection of intermittent atrial fibrillation and guiding anticoagulation decisions.

In hospital settings, clinicians employ continuous ECG monitoring in intensive care units to track hemodynamic stability in post-surgical and critically ill patients. Telemedicine platforms integrate compact, wireless ECG devices for remote assessments, allowing specialists to review tracings in real time for patients with suspected heart failure or electrolyte imbalances.

Manufacturers pursue opportunities to embed artificial intelligence algorithms that automate rhythm interpretation and flag abnormalities, expanding applications in high-volume screening programs and primary care settings where rapid triage enhances efficiency.

Developers advance wearable and patch-based ECG systems with extended recording capabilities, broadening utility in long-term arrhythmia detection and post-ablation monitoring. These innovations facilitate integration with mobile health platforms, enabling patients to transmit data directly to providers for proactive management of chronic conditions.

Opportunities emerge in multi-parameter devices combining ECG with pulse oximetry and blood pressure, supporting comprehensive cardiac assessments in home care. Companies invest in cloud-connected systems that enable secure data sharing and longitudinal trend analysis. Recent trends emphasize user-friendly interfaces, enhanced noise reduction, and predictive analytics, positioning ECG machines as foundational tools in preventive cardiology and value-based care delivery.

Key Takeaways

- In 2025, the market generated a revenue of US$ 8.5 Billion, with a CAGR of 7.2%, and is expected to reach US$ 17.0 Billion by the year 2035.

- The product type segment is divided into ECG holter monitoring system, ECG resting system, cardiopulmonary stress testing system and ECG stress testing system, with ECG holter monitoring system taking the lead with a market share of 36.9%.

- Considering technology, the market is divided into digital and analog. Among these, digital held a significant share of 72.6%.

- Furthermore, concerning the modality segment, the market is segregated into wireless and wired. The wireless sector stands out as the dominant player, holding the largest revenue share of 58.3% in the market.

- The end user segment is segregated into hospitals, specialty clinics and ambulatory surgical centers, with the hospitals segment leading the market, holding a revenue share of 49.8%.

- North America led the market by securing a market share of 45.1%.

Product Type Analysis

ECG holter monitoring systems accounted for 36.9% of growth within product type and led the ECG machine market due to rising demand for long-term cardiac rhythm assessment. Physicians rely on Holter systems to detect intermittent arrhythmias that standard resting ECGs fail to capture.

Increasing prevalence of atrial fibrillation and other rhythm disorders strengthens adoption across cardiology practices. Continuous ambulatory monitoring improves diagnostic accuracy and treatment planning.

Growth strengthens as wearable technologies enhance patient comfort and data recording duration. Digital data storage and cloud connectivity improve physician access to detailed rhythm reports. Expanding preventive cardiology programs further increase monitoring utilization.

Integration with telecardiology platforms supports remote analysis. The segment is expected to remain dominant as long-duration cardiac monitoring continues to address growing cardiovascular disease burdens.

Technology Analysis

Digital systems generated 72.6% of growth within technology and emerged as the leading segment due to superior signal clarity and data management capabilities. Healthcare providers prefer digital ECG machines because they offer automated interpretation and seamless integration with electronic health records. Advanced software algorithms improve waveform analysis and reduce interpretation errors. Digital systems also support remote data sharing and centralized storage.

Growth accelerates as hospitals modernize diagnostic infrastructure and replace analog devices. Improved cybersecurity and interoperability standards enhance digital adoption. Compact and user-friendly interfaces further strengthen clinical efficiency. Regulatory emphasis on digital documentation supports system upgrades. The segment is projected to maintain leadership as digital transformation continues across cardiovascular diagnostics.

Modality Analysis

Wireless systems contributed 58.3% of growth within modality and led the ECG machine market due to enhanced mobility and patient convenience. Clinicians favor wireless ECG devices for bedside monitoring and outpatient cardiac evaluation. Cable-free operation reduces motion artifacts and improves patient comfort during extended monitoring. Wireless transmission supports real-time data review and faster clinical decision-making.

Growth strengthens as healthcare systems expand remote cardiac monitoring services. Integration with mobile applications increases patient engagement in follow-up care. Advancements in battery life and connectivity reliability enhance usability. Portable wireless units support home-based monitoring programs. The segment is anticipated to remain dominant as telehealth and mobile diagnostics continue to gain traction.

End-User Analysis

Hospitals accounted for 49.8% of growth within end user and dominated the ECG machine market due to high patient throughput and comprehensive cardiovascular care services. Emergency departments and intensive care units rely on continuous ECG monitoring to manage acute cardiac events. Hospitals invest in advanced systems to support multidisciplinary cardiac teams. Centralized procurement and standardized protocols increase equipment utilization.

Growth continues as cardiovascular disease prevalence rises globally. Hospitals expand cardiac diagnostic units and integrate digital monitoring solutions. Accreditation standards emphasize reliable cardiac assessment infrastructure.

Teaching hospitals further increase demand through training and research initiatives. The segment is expected to remain the primary growth driver as hospitals continue to anchor acute and chronic cardiac care management.

Key Market Segments

By Product Type

- ECG Holter Monitoring System

- ECG Resting System

- Cardiopulmonary Stress Testing System

- ECG Stress Testing System

By Technology

- Digital

- Analog

By Modality

- Wireless

- Wired

By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

Drivers

Increasing prevalence of cardiovascular diseases is driving the market.

The rising incidence of cardiovascular diseases globally has created substantial demand for ECG machines to support early detection, diagnosis, and ongoing monitoring of heart conditions. Improved screening programs and greater clinical awareness have resulted in more frequent identification of arrhythmias and ischemic events.

Hospitals and cardiology clinics are expanding their ECG capabilities to manage the growing number of patients with chronic heart disease. The direct relationship between CVD mortality and the need for accessible diagnostic tools continues to propel procurement of both 12-lead and portable ECG systems. Public health authorities consistently report that cardiovascular diseases remain the leading cause of death worldwide.

ECG machines provide critical real-time electrical data that guides immediate clinical decisions in acute settings. National health priorities increasingly include widespread access to cardiac monitoring equipment. Manufacturers are responding by developing systems with improved signal quality and user interfaces.

This driver supports long-term investment in both hospital-based and ambulatory ECG solutions. An estimated 19.8 million people died from cardiovascular diseases in 2022, representing approximately 32% of all global deaths.

Restraints

High cost of advanced ECG systems is restraining the market.

The elevated purchase price of modern multi-channel ECG machines equipped with advanced algorithms and connectivity features restricts their adoption in budget-constrained healthcare facilities. Complex engineering for noise reduction, wireless transmission, and long battery life contributes to higher manufacturing costs.

Many public hospitals and primary care centers continue using legacy systems due to limited capital budgets. Regulatory requirements for electrical safety and performance testing add to the total acquisition expense. In low-resource settings, these costs often lead to reliance on basic single-channel devices despite reduced diagnostic capability.

Providers frequently defer upgrades, which limits access to the latest interpretation software and data integration capabilities. This restraint is especially pronounced in rural and developing regions where reimbursement rates remain low.

Industry attempts to offer modular or refurbished options provide only partial relief. Despite clear clinical advantages, financial barriers continue to slow the replacement cycle. The high cost of ECG equipment remains a major restraint in the market.

Opportunities

Rapid growth of ambulatory and home monitoring demand is creating growth opportunities.

The accelerating shift toward ambulatory ECG monitoring and home-based cardiac assessment creates significant potential for portable and wearable ECG solutions. Governmental initiatives supporting chronic disease management outside hospitals are driving reimbursement for remote cardiac monitoring.

Patients with atrial fibrillation and post-myocardial infarction conditions increasingly require long-term rhythm surveillance. Partnerships between device manufacturers and telehealth platforms facilitate seamless data transmission to clinicians. The large population of patients with known or suspected arrhythmias magnifies demand for convenient monitoring devices.

Educational programs for primary care physicians promote the use of ambulatory ECG in routine practice. This opportunity allows manufacturers to expand beyond traditional hospital placements. Leading companies are developing lightweight, adhesive patch monitors optimized for extended wear.

Overall, ambulatory growth aligns with efforts to reduce hospital admissions through proactive monitoring. The number of Medicare beneficiaries enrolled in remote cardiac monitoring services grew substantially between 2022 and 2024, reflecting this shift.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the ECG machine market through healthcare capital budgets, outpatient diagnostic volumes, and reimbursement stability. Inflation raises costs for circuit boards, display units, cables, and logistics, which increases manufacturing and distribution expenses.

Higher interest rates limit access to affordable financing for equipment purchases, which slows upgrades in smaller clinics and rural hospitals. Geopolitical tensions disrupt semiconductor supply and electronic component sourcing, creating procurement delays and cost fluctuations.

Current US tariffs on imported electronic assemblies and finished devices increase landed costs, which tightens margins and complicates pricing strategies. These pressures can postpone purchasing decisions in cost sensitive healthcare settings.

At the same time, providers strengthen domestic supplier relationships and focus on durable, multi functional systems to optimize value. Rising prevalence of cardiovascular disease and growing demand for portable monitoring solutions continue to sustain long term market growth.

Latest Trends

Integration of artificial intelligence for automated ECG interpretation is a recent trend in the market.

In 2024, the incorporation of artificial intelligence algorithms in ECG machines has advanced automated rhythm and morphology interpretation with high diagnostic accuracy. These systems utilize deep learning models trained on millions of annotated ECG tracings to identify subtle abnormalities. Manufacturers have focused on regulatory clearance for AI modules to ensure clinical reliability.

Clinical studies in 2024 demonstrated reduced interpretation times and fewer missed findings with AI assistance. GE HealthCare received FDA clearance in 2024 for its AI-powered ECG interpretation module integrated into the MAC series electrocardiographs. This development supports faster triage in emergency departments and primary care settings.

The trend emphasizes seamless integration with electronic health records for immediate clinical decision support. Regulatory pathways have evolved to accommodate validated AI features in diagnostic devices. Industry collaborations continue to refine algorithms for diverse patient populations. These innovations aim to enhance diagnostic consistency while addressing cardiologist workload challenges.

Regional Analysis

North America is leading the ECG Machine Market

North America accounted for a 45.1% share of the ECG Machine market in 2024, reflecting strong demand for cardiac diagnostics across hospitals, clinics, and home care settings. Healthcare providers expanded routine electrocardiography screening to detect arrhythmias, ischemic changes, and heart failure at earlier stages.

Growth in outpatient cardiology services and ambulatory surgical centers increased the need for compact and portable cardiac monitoring systems. Integration with electronic health records and cloud-based data platforms improved workflow efficiency and remote interpretation. Rising adoption of wearable and mobile cardiac monitoring solutions further strengthened device utilization beyond traditional hospital environments.

Preventive health initiatives and employer-sponsored wellness programs also encouraged broader cardiovascular screening. A relevant supporting indicator comes from the Centers for Disease Control and Prevention, which reported in 2023 that heart disease remains the leading cause of death in the United States, accounting for approximately 695,000 deaths annually, underscoring sustained clinical need for reliable cardiac monitoring technologies.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The ECG Machine market in Asia Pacific is expected to grow steadily during the forecast period as cardiovascular disease burden increases across rapidly urbanizing populations. Governments prioritize early detection and management of heart conditions through expanded primary care screening programs.

Hospitals invest in modern diagnostic equipment to strengthen cardiac care infrastructure. Rising prevalence of hypertension and diabetes increases the need for routine electrocardiographic assessment. Private healthcare providers expand cardiology services in metropolitan and tier two cities, boosting procurement of advanced monitoring systems.

Regional manufacturers introduce affordable and portable devices to widen accessibility. A verifiable signal of underlying demand appears in 2023 data from the World Health Organization, which confirmed that cardiovascular diseases account for nearly one third of global deaths, highlighting strong long-term growth potential across Asia Pacific.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the ECG machine market grow by enhancing signal fidelity, expanding lead configurations, and integrating advanced analytics that support arrhythmia detection and streamline clinician interpretation across point-of-care and hospital environments.

They also strengthen product value by embedding connectivity with electronic health records and cloud-based platforms, enabling seamless data sharing, longitudinal tracking, and remote monitoring that align with evolving care models.

Firms pursue strategic partnerships with telehealth providers, cardiac care networks, and ambulatory service programs to broaden deployment and capture recurring service demand. Geographic expansion into North America, Europe, and high-growth Asia Pacific diversifies revenue and responds to rising cardiovascular disease prevalence and preventive screening initiatives worldwide.

Philips Healthcare exemplifies a diversified medical technology company with a comprehensive cardiovascular portfolio, strong sales and service infrastructure, and coordinated commercialization strategies that align device performance with clinician priorities.

The company advances its competitive agenda through disciplined investment in product innovation, targeted collaborations that extend interoperability, and a customer-centric approach that translates technological enhancements into measurable clinical and operational benefits.

Top Key Players

- GE HealthCare

- Philips Healthcare

- Nihon Kohden

- Schiller AG

- Mindray

- Edan Instruments

- BPL Medical Technologies

- Hillrom

- Mortara Instrument

- Contec Medical Systems

Recent Developments

- In 2026, GE HealthCare reported that its Patient Care Solutions segment, which includes its diagnostic ECG portfolio, generated US$ 3 billion in revenue for fiscal year 2025. According to company disclosures, the February 2026 launch of ReadyFix technology now enables remote maintenance and software updates for MAC VU360 ECG workstations to improve clinical workflows in the US.

- In 2026, Nihon Kohden Corporation disclosed that its consolidated net sales for the first nine months of fiscal year 2025 reached approximately US$ 1.08 billion. As per recent financial results, while domestic demand saw adjustments, the company’s ECG product lines achieved double-digit growth in international markets, particularly within the Asia Pacific and Latin America.

Report Scope

Report Features Description Market Value (2025) US$ 8.5 Billion Forecast Revenue (2035) US$ 17.0 Billion CAGR (2026-2035) 7.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (ECG Holter Monitoring System, ECG Resting System, Cardiopulmonary Stress Testing System and ECG Stress Testing System), By Technology (Digital and Analog), By Modality (Wireless and Wired), By End User (Hospitals, Specialty Clinics and Ambulatory Surgical Centers) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape GE HealthCare, Philips Healthcare, Nihon Kohden, Schiller AG, Mindray, Edan Instruments, BPL Medical Technologies, Hillrom, Mortara Instrument, Contec Medical Systems Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- GE HealthCare

- Philips Healthcare

- Nihon Kohden

- Schiller AG

- Mindray

- Edan Instruments

- BPL Medical Technologies

- Hillrom

- Mortara Instrument

- Contec Medical Systems

Our Clients

- 179023

- Feb 2026