Quick Navigation

Report Overview

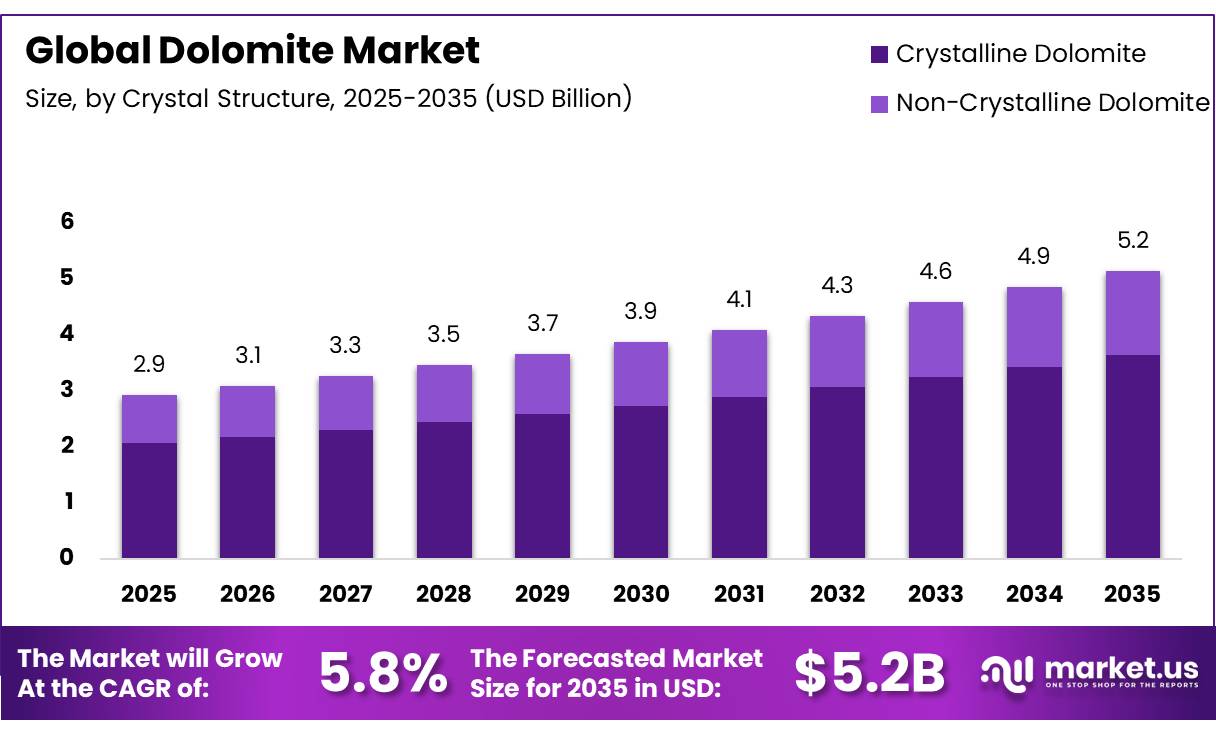

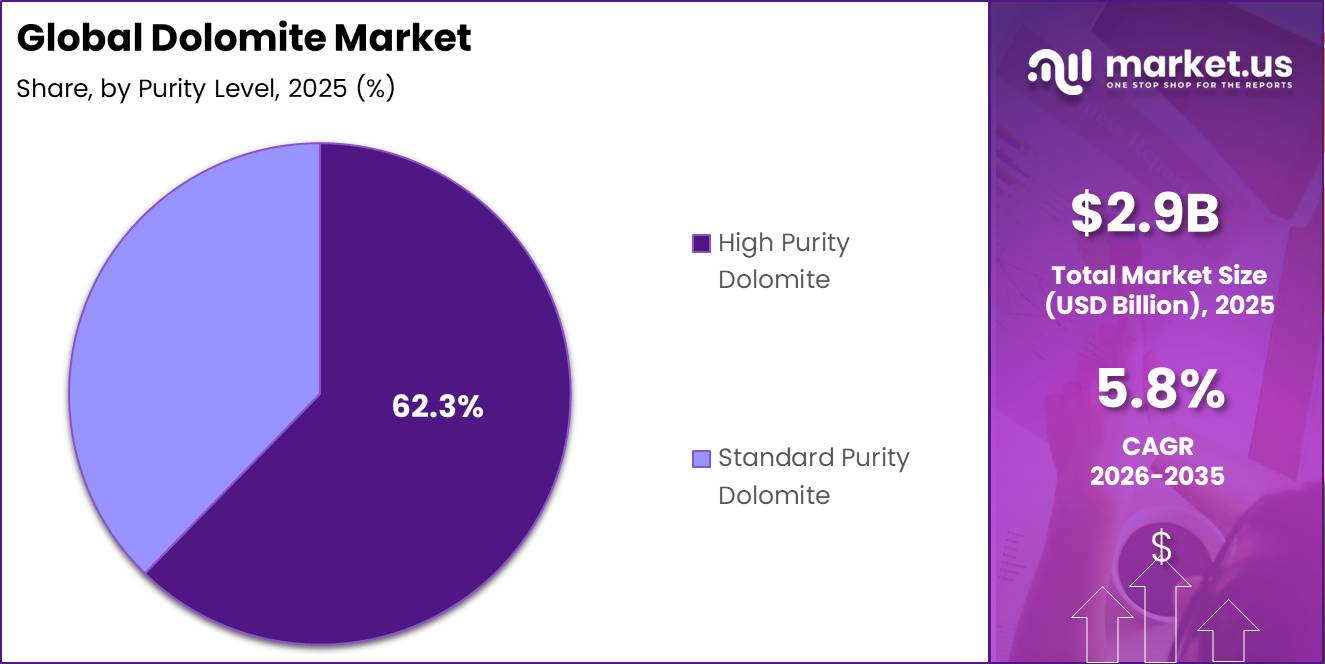

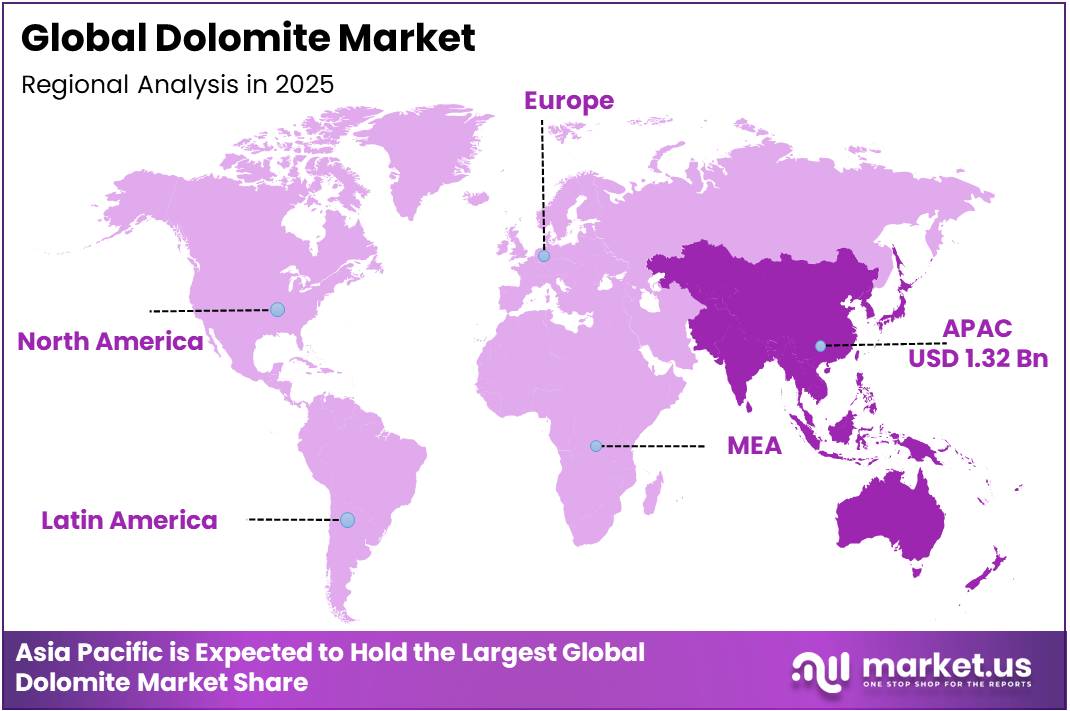

In 2025, the Global Dolomite Market was valued at US$2.9 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.8%, reaching about US$5.2 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 45.2% share, holding USD 1.32 billion in revenue.

Key Takeaways

- The global Dolomite market was valued at US$ 2.9 billion in 2025.

- The global Dolomite market is projected to grow at a CAGR of 5.8% and is estimated to reach US$ 5.2 billion by 2035.

- On the basis of Product Type, Crushed & Ground Dolomite dominated the market, constituting 35.6% of the total market share.

- Based on the Crystal Structure, Crystalline Dolomite dominated the market, with a substantial market share of around 70.6%.

- Based on the Form, Powder led the market, comprising 40.6% of the total market.

- Based on the Purity Level, High Purity Dolomite dominated the market, accounting for 62.3% of the total market share.

- Among the End-Use Industries, the Iron & Steel industry held a major share in the Dolomite market, with 30.5% of the market share.

- In 2025, Asia Pacific was the most dominant region in the global Dolomite market, accounting for 45.2% of the total global consumption.

Dolomite is a naturally occurring calcium magnesium carbonate mineral that serves as a critical industrial raw material across steel making, construction, glass, ceramics, agriculture, and environmental applications. Its high thermal stability, fluxing capability, and magnesium content make it indispensable for refractory linings and impurity removal during steel production. The industrial outlook remains favorable as demand from heavy industries and infrastructure development continues to strengthen.

- According to the World Steel Association, global crude steel production reached approximately 1.88 billion tonnes in 2024, sustaining strong demand for flux minerals such as dolomite used in blast furnaces and electric arc furnaces. Meanwhile, the U.S. Geological Survey reported in January 2025 that the United States produced an estimated 15 million tons of lime in 2025, with steel making remaining the largest end-use sector, highlighting continued consumption of carbonate minerals including dolomite in metallurgical operations.

Future growth opportunities are supported by global decarbonization strategies and sustainable industrial manufacturing. The International Energy Agency stated in 2025 that achieving near-zero-emission steel and cement production requires rapid deployment of low-carbon materials and process improvements, increasing the importance of high-quality refractory and flux minerals such as dolomite.

Additionally, stricter environmental regulations are accelerating investment in water treatment and flue-gas purification systems, where dolomite is increasingly utilized for pH control and contaminant removal. These trends, combined with technological advancements in mineral processing and circular manufacturing, are expected to strengthen long-term industrial demand while supporting more efficient and sustainable resource utilization.

Dolomite Market Segments

Crystal Structure Analysis

Crystalline Dolomite Represents the Dominant Segment in the Market by Crystal Structure

Crystalline dolomite accounts for a significant 70.6% of the global dolomite market by crystal structure, owing to its superior physical and chemical properties, which make it indispensable in high-performance industrial applications. Its well-defined crystal lattice provides exceptional hardness, chemical stability, and thermal degradation resistance properties that are essential in demanding environments such as steel furnace linings, refractory manufacturing, and high-quality construction applications.

Dolomite’s purity has a significant impact on its value and target applications. High-purity crystalline grades command premium prices and are preferred across specialized industrial end-uses that require consistent mineralogical composition and predictable performance under stress.

Non-Crystalline Dolomite represents the fastest growing region and is used in more general-purpose industrial applications where structural precision is not critical, such as basic construction aggregates and lower-grade soil conditioning in agriculture.

Purity Level Analysis

High Purity Dolomite Represents the Dominant Segment in the Market by Purity Level

High Purity Dolomite accounts for 62.3% of the global dolomite market by purity level, reflecting an increasing industrial preference for refined, contaminant-free grades in a wide range of sophisticated applications. High-purity dolomite commands high prices and is increasingly being targeted at niche chemical applications and tailored solutions for sustainable construction markets where even trace levels of impurities can jeopardize product quality, safety compliance, or end-use performance. The migration of dolomite into pharmaceuticals, food processing, and specialty chemical manufacturing has been a major driver of this dominance, as these industries demand purity standards far higher than those required by traditional industrial applications.

Standard Purity Dolomite is the fastest growing segment and continues to serve high-volume, cost-sensitive applications such as road base construction, general-purpose soil conditioning, and lower-specification industrial uses where premium-grade material is not required or economically justified.

Form Type Analysis

Powder Form Represents the Dominant Segment in the Market by Form

Powder held the largest share of the global dolomite market at 40.6% owing to its excellent flowability, uniform particle size, and high chemical reactivity, making it the preferred form for steelmaking, glass manufacturing, ceramics, paints, plastics, rubber, and agricultural applications. Its fine texture enables better mixing, faster reaction kinetics, and improved process efficiency compared with coarser forms, while also reducing material losses during production. The versatility of dolomite powder allows manufacturers to use the same material across multiple industrial processes, supporting its widespread adoption and reinforcing its position as the dominant form in the market.

Dolomite chips are gaining traction due to their increasing use in filtration media, refractory products, and construction applications, where high mechanical strength and uniform sizing are essential. Their durability and ease of handling continue to support gradual demand growth across industrial and infrastructure projects

Product Type Analysis

Crushed & Ground Dolomite Represents the Dominant Segment in the Market by Product Type

Crushed and Ground Dolomite dominates the global dolomite market, accounting for 35.6% of the total market share, owing to its unmatched versatility and cost-effectiveness across multiple industries. Its dominance is due to its processing simplicity, cost-effectiveness, and versatile application capabilities when compared to specialized thermal treatments in commercial industrial operations, making it the preferred product form for everything from road construction and concrete production to steel manufacturing and agricultural soil conditioning. The sheer scale of global infrastructure development, particularly in emerging economies, has only strengthened its position as the most popular product type in the market.

Calcined Dolomite is widely used in steel fluxing and glass manufacturing due to its high purity and thermal properties. Sintered Dolomite is used in various applications ranging from refractory linings to heavy metal industries. Agglomerated dolomite is becoming increasingly important in construction, agriculture, and specialized chemical processing.

End-Use Industry Analysis

Dolomite Is Majorly Used In Iron & Steel Industry

The iron and steel industry represents the dominant end-use segment of the global dolomite market, accounting for 30.5% of total demand. This dominance is driven by dolomite’s important role in steelmaking, where it is used as a fluxing material and refractory input. It helps support slag formation, impurity removal, furnace lining protection, and process efficiency in high-temperature operations.

After calcination, dolomite is used in refractory applications for basic steelmaking furnaces, converters, ladles, and electric arc furnace operations. This makes demand more process-driven than preference-driven, as steel producers require stable mineral inputs for efficient production. Other end-use industries, including glass and ceramics, chemicals, water treatment, mining and metallurgy, pharmaceuticals, and industrial manufacturing, provide diversified demand support for the market.

Key Market Segments

By Product Type

- Crushed & Ground

- Calcined Dolomite

- Sintered Dolomite

- Agglomerated Dolomite

By Crystal Structure

- Crystalline Dolomite

- Non-Crystalline Dolomite

By Form

- Powder

- Granules

- Lumps

- Chips

By Purity Level

- High Purity Dolomite

- Standard Purity Dolomite

By End-Use Industry

- Iron & Steel

- Building & Construction

- Agriculture

- Chemicals

- Glass & Ceramics

- Water Treatment

- Mining & Metallurgy

- Pharmaceuticals

- Industrial Manufacturing

- Others

Drivers

Restraints

Opportunity

Trends

Geopolitical Impact Analysis

Strategic Mineral Policies and Regional Sourcing Accelerating Dolomite Industry Resilience

Geopolitical uncertainty and trade disruptions have prompted governments to strengthen domestic mineral supply chains, indirectly supporting demand for industrial minerals such as dolomite used in steel, glass, refractories, and infrastructure. According to the European Commission’s Critical Raw Materials Act (2024), the European Union has set targets to source at least 10% of its annual strategic raw material consumption through domestic extraction, process 40% within the EU, and recycle 25% by 2030. Although dolomite is not classified as a strategic raw material, these policies are encouraging investment in regional mineral processing and reducing dependence on external suppliers, creating a favorable environment for industrial mineral producers.

Geopolitical diversification is also reshaping downstream industries that consume dolomite. According to the U.S. Department of Energy, the United States allocated US$6 billion in March 2024 under the Industrial Demonstrations Program to accelerate decarbonization across energy-intensive industries, including iron and steel, cement, and glass manufacturing. As these sectors expand domestic production capacity and modernize facilities, demand for refractory and flux materials such as dolomite is expected to strengthen alongside regional supply chain development.

Regional Analysis

Asia Pacific Held the Largest Share in the Global Dolomite Market

Asia Pacific leads the global dolomite market with about 45.2% of total consumption in 2025, supported by strong demand from steel, cement, glass, and construction industries. China and India remain major contributors due to large infrastructure projects, expanding urban housing, and high steel output. The region also benefits from abundant dolomite reserves, low mining costs, and strong domestic supply chains that support consistent industrial consumption across key manufacturing hub markets.

The region’s dominance is further supported by growing agricultural use of dolomitic lime to improve acidic soils and enhance crop productivity. Rapid industrialization in Southeast Asia is also increasing dolomite use in ceramics, refractories, water treatment, and environmental applications.

Asia Pacific’s dominance in the global dolomite market is powered by multiple strong industries driving demand simultaneously rather than dependence on a single sector. Construction and steel form the most prominent consumption pillars, while agriculture adds an equally vital dimension dolomite is widely used to neutralize soil acidity, restore magnesium and calcium levels, and improve crop productivity across the region’s vast farmlands.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global dolomite market operates within a moderately consolidated competitive landscape, where a handful of well-established multinational players collectively account for a dominant share of global production capacity, processing capability, and distribution reach. The global market remains moderately consolidated, with top-tier companies such as Lhoist Group and Imerys together total market influence and production capacity a concentration that reflects decades of strategic investment in mining infrastructure, vertical integration, and geographic expansion across key consuming regions. The competitive edge that major dolomite players hold over smaller regional counterparts runs far deeper than production volume alone it lies in their exceptional ability to cater to a wide and diverse spectrum of end-use industries simultaneously, from steel and construction to agriculture and pharmaceuticals, through carefully developed and grade-specific product portfolios that demand a level of technical sophistication, operational scale, and geographic reach that emerging players simply cannot match.

The major Players In The Industry

- Imerys SA

- RHI Magnesita NV

- Sibelco

- Lhoist Group

- Essel Mining & Industries Ltd.

- JFE Mineral Co., Ltd.

- Carmeuse

- Nordkalk Corporation

- Calcinor SA

- Omya AG

- CEMEX S.A.B. de C.V.

- KHD Humboldt Wedag International AG

- Grupo Calidra

- Minerals Technologies Inc.

- Dillon & Company

- Other Key Players

Key Development

- In March 2025, Lhoist Group announced a major capacity expansion across its dolomite mining and processing facilities in Europe and North America, investing significantly in modernizing its extraction technologies and increasing output to meet the growing demand from the steel, construction, and agricultural sectors across key global markets.

- In July 2025, Omya AG launched a comprehensive sustainability program across its global dolomite operations, introducing low-carbon processing technologies and committing to a measurable reduction in its carbon footprint across all major production facilities, directly responding to the growing pressure from industrial buyers and regulators to adopt more environmentally responsible mineral processing practices.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$2.9 Bn |

| Forecast Revenue (2035) | US$5.2 Bn |

| CAGR (2026-2035) | 5.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Crushed and Ground, Calcined Dolomite, Sintered Dolomite, and Agglomerated Dolomite), By Crystal Structure (Crystalline Dolomite and Non-Crystalline Dolomite), By Form (Powder, Granules, Lumps, and Chips), By Purity Level (High Purity Dolomite and Standard Purity Dolomite), By End-Use Industry (Iron and Steel, Building and Construction, Agriculture, Chemicals, Glass and Ceramics, Water Treatment, Mining and Metallurgy, Pharmaceuticals, Industrial Manufacturing, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Imerys SA, RHI Magnesita NV, Sibelco, Lhoist Group, Essel Mining & Industries Ltd., JFE Mineral Co. Ltd., Carmeuse, Nordkalk Corporation, Calcinor SA, Omya AG, CEMEX S.A.B. de C.V., KHD Humboldt Wedag International AG, Grupo Calidra, Minerals Technologies Inc., E. Dillon & Company, other players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |